Written by: Thejaswini M A

Translated by: Saoirse, Foresight News

Once upon a time, trading cryptocurrency was as simple as entering SOL, selecting USDC, and clicking exchange. It was a time of simplicity and purity, where the only concern was whether one could get a better trading price.

Now, times have changed, and the industry landscape has become complex. The crypto market is transitioning from grassroots amateur projects to a professional, institutional trading system. Financial institutions from Wall Street are entering the field to lay out the underlying infrastructure, and ordinary retail investors are gradually losing their previous enthusiasm. Now, we must question: where do seemingly favorable prices actually come from? Who are the counterparties for each order?

If cryptocurrency is to stand firm in the fintech field and develop sustainably, the entire industry needs to maintain a sense of caution and skepticism.

You might think that trading stocks on a brokerage platform puts you in a public trading market, but that is not the case; you are actually in a private trading network. Nowadays, trading software for retail investors continues to use a controversial order routing mechanism. This mechanism was first birthed in the 1980s, with electronic trading pioneer Bernie Madoff being one of its early large-scale users. Bernie Madoff discovered that by paying compliance rebates to retail brokers, he could gain early access to customer orders and complete operations before they entered public exchanges.

This model gave rise to private intermediary institutions sitting between traders and public ledgers, and they extract profits from the price differential of each transaction.

The original intention of cryptocurrency was to completely eliminate such centralized intermediaries.

The core principle of decentralized finance (DeFi) was transparency and openness, where all trading activities could be traced. However, over the past year, Solana's public chain has taken a completely different path of development.

Jupiter is the core trading hub within the Solana ecosystem, but the underlying logic supporting platform trading operations has fundamentally changed. Today, platform trading mostly relies on private trading pools. This article will unveil the hidden "black box" of the Solana trading market.

Early automatic market makers (AMMs) had complete transparency. Their essence was a liquidity pool composed of two types of tokens along with publicly verifiable calculation formulas, allowing anyone to view the code on GitHub and clearly understand the flow of their funds. Trading on platforms like Raydium and Orca was akin to using a completely transparent device, with operational logic being evident.

However, Prop AMM (using automatic market makers) is a completely different model. Its trading prices are generated by servers from private companies; the contracts deployed on the Solana chain are merely shells, serving only as data gateways. Users' trading instructions are directly forwarded to off-chain servers, where private institution algorithms complete the final trade execution. "Prop" stands for proprietary and private; such institutions will never disclose their profit models to the outside world.

Just one year ago, this model seemed out of place, yet it has now dominated Solana's spot trading market.

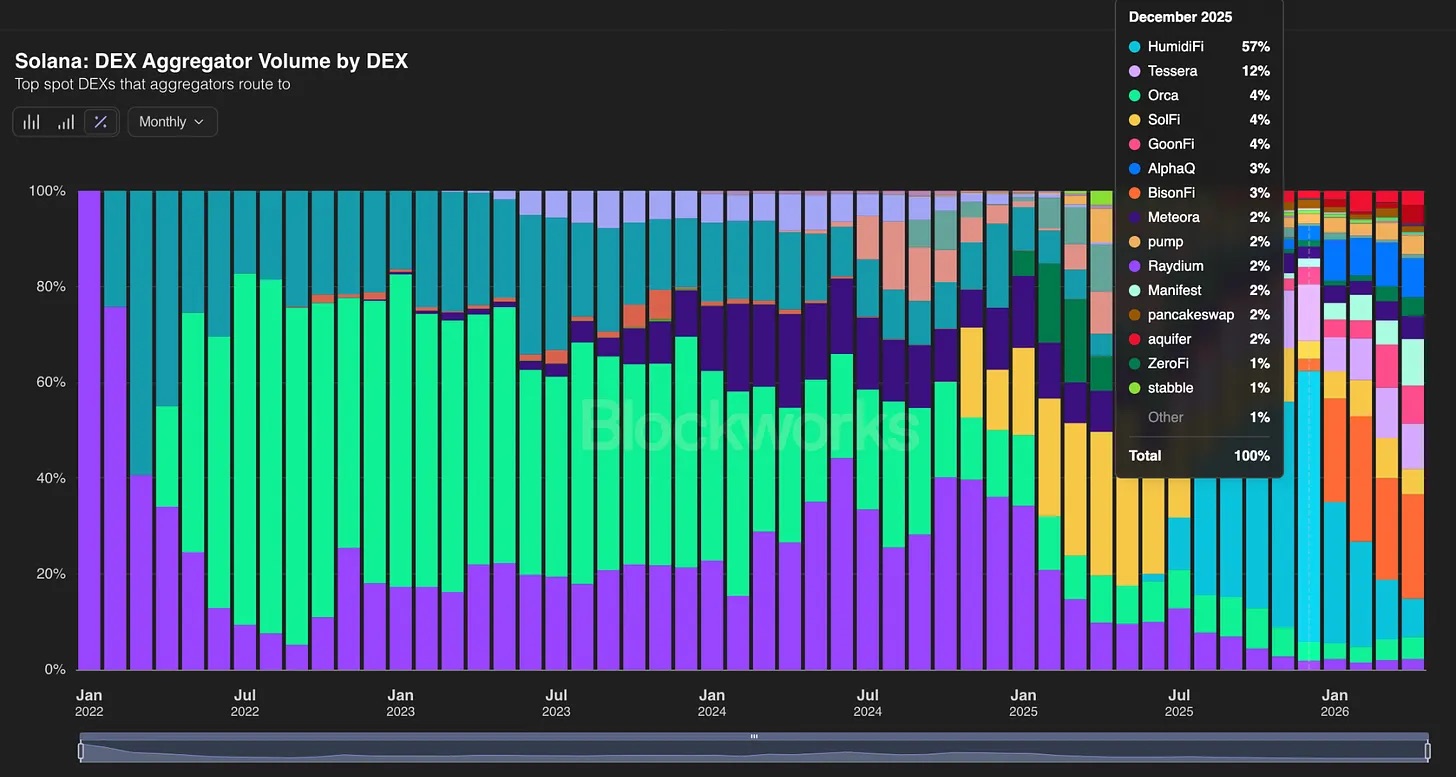

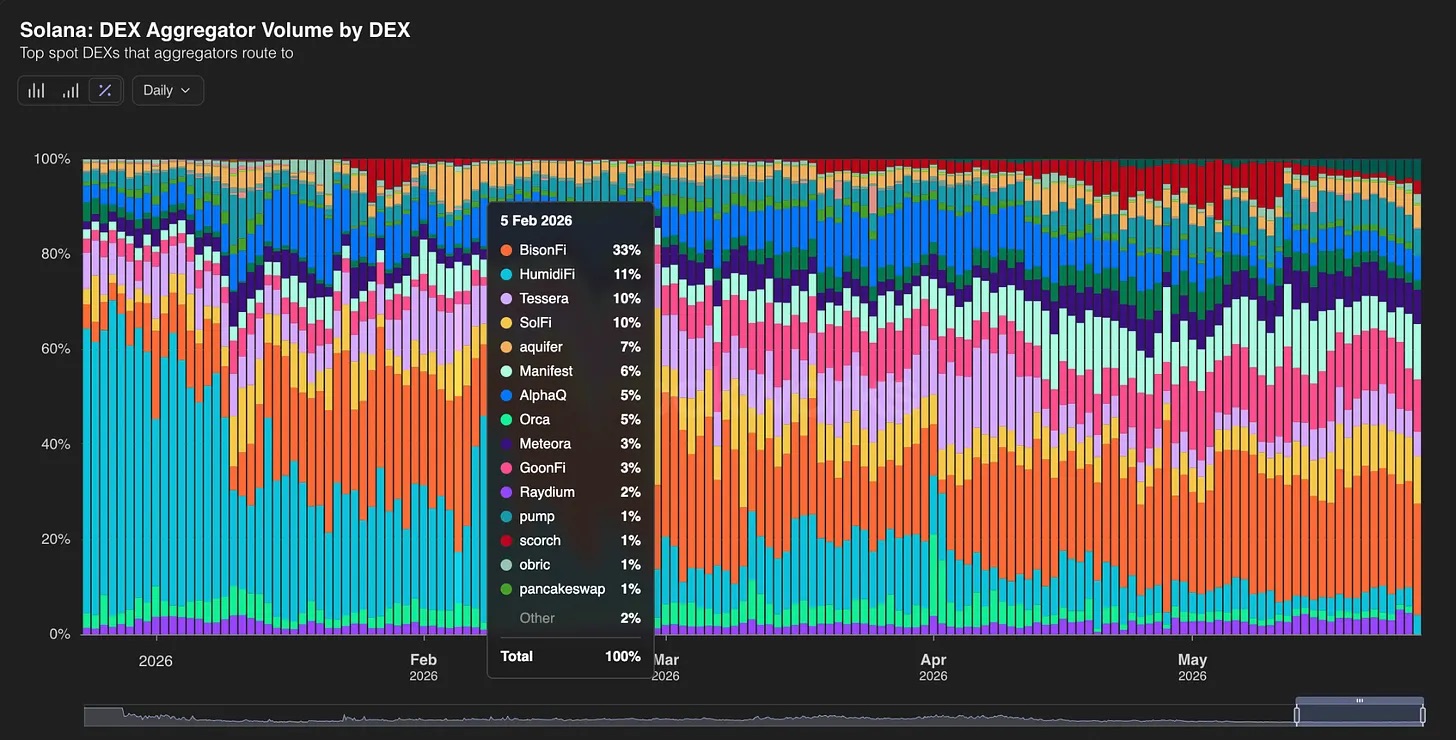

HumidiFi went live in June 2025. By December 2025, HumidiFi alone accounted for 57% of the trading volume of the entire Solana aggregator; during the same period, Raydium's share dropped to 2%, Orca accounted for 5%, and Tessera took up 12%. By late January 2026, Prop AMM had entirely captured approximately 92% of Jupiter's order routing business.

Change in the composition of trading volume routed through DEX aggregators on the Solana chain, source: @blockworks.com

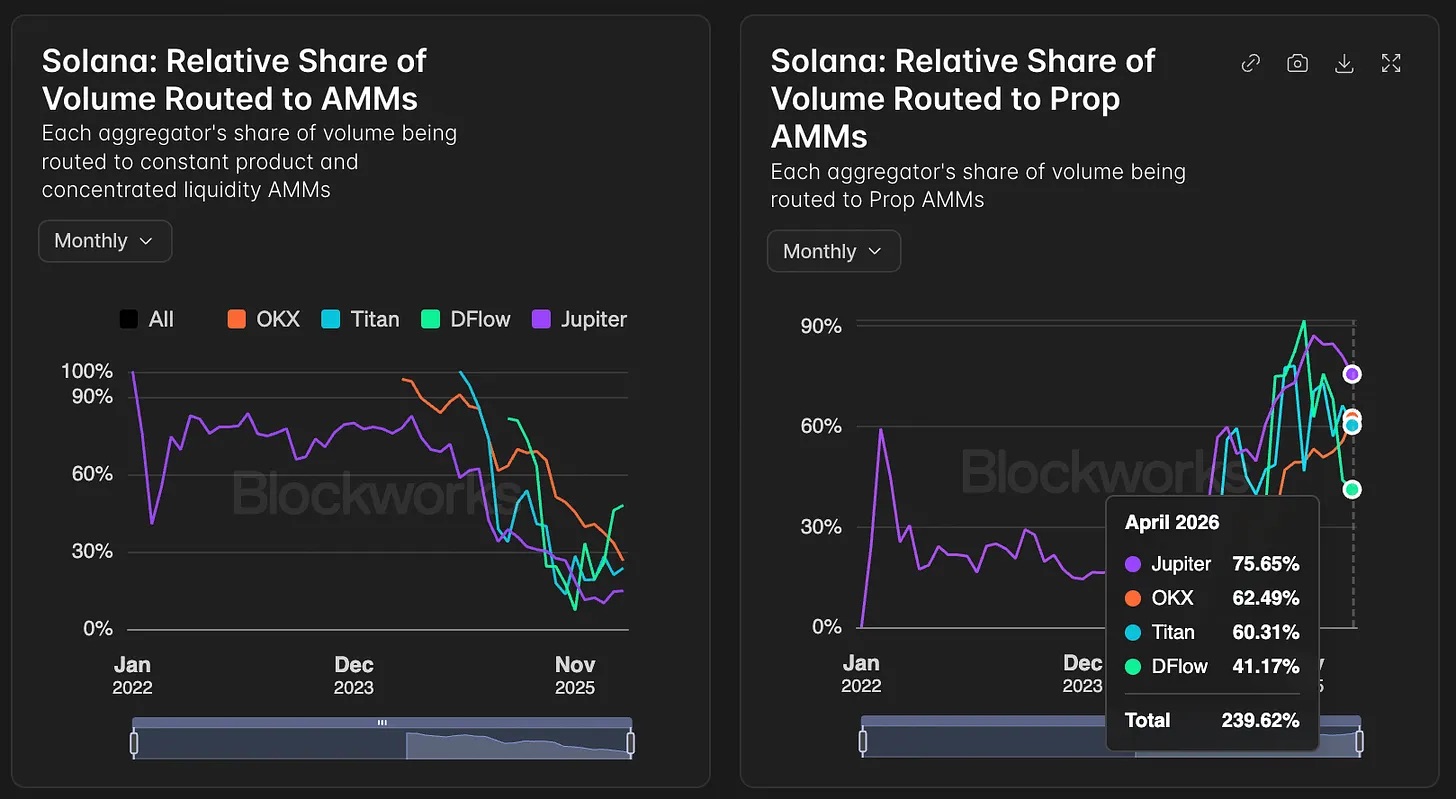

Jupiter accounted for 75% to 80% of the trading volume of Solana's aggregators, meaning that once Prop AMM took control of Jupiter, it effectively seized the entire spot trading market on Solana.

Market share of AMM trading volume (left 2022-2025) versus Prop AMM trading volume (right 2022-2026.04), source: @Blockworks

The price differential is the core inducement behind this, which also serves as the implicit fee traders pay to market makers to complete trades. The financial industry typically uses basis points as the measurement unit for differentials, with one basis point representing one-hundredth of one percent. Even in regular trading, this fee accumulates over time and is not negligible. According to Dune data, private trading platforms like HumidiFi and Tessera have extremely low differentials.

In contrast, using traditional public liquidity pools for token exchanges incurs significantly higher costs. Low trading costs make private market makers the preferred choice for users. Research from Jump confirms that completing regular trades on these private platforms even yields better prices than top centralized exchanges like Binance and Coinbase.

So, who are the operating entities behind this? The operator of TesseraV is Wintermute, which has provided market-making services for platforms like Binance and Coinbase for five years.

SolFi belongs to Ellipsis Labs, a quantitative trading team funded by Paradigm. HumidiFi is operated by Temporal, which controls the largest portion of extractable value (MEV) infrastructure on Solana. These institutions are all professional trading teams, equipped with dedicated legal and compliance personnel, and utilize professional financial tools like Bloomberg terminals.

In the traditional financial markets where these institutions originally operated, they had to register with the U.S. Securities and Exchange Commission (SEC) and strictly adhere to various regulatory rules: prohibiting front-running customer orders, rigorously checking for fraudulent trading practices, and having trading algorithms subject to review. The entire mature regulatory system was designed to constrain institutional compliance operations.

It's akin to Citadel paying Robinhood hundreds of millions every year; though there is currently no evidence that such actions harm user interests, it always leaves a lingering unease.

Yet in the Solana ecosystem, all regulatory rules are essentially nonexistent. These established trading institutions continue to use the same trading models without having to comply with exchange and securities regulatory constraints. Over 90% of Solana aggregator order flows pass through Jupiter into these private institutions.

Outsiders often label DeFi as "anonymous," but this is actually a misunderstanding. Participants are all well-known professional trading teams in the industry, and their transition to the on-chain market is primarily because of looser regulations and fewer constraints.

Frequent Changes in Industry Leadership

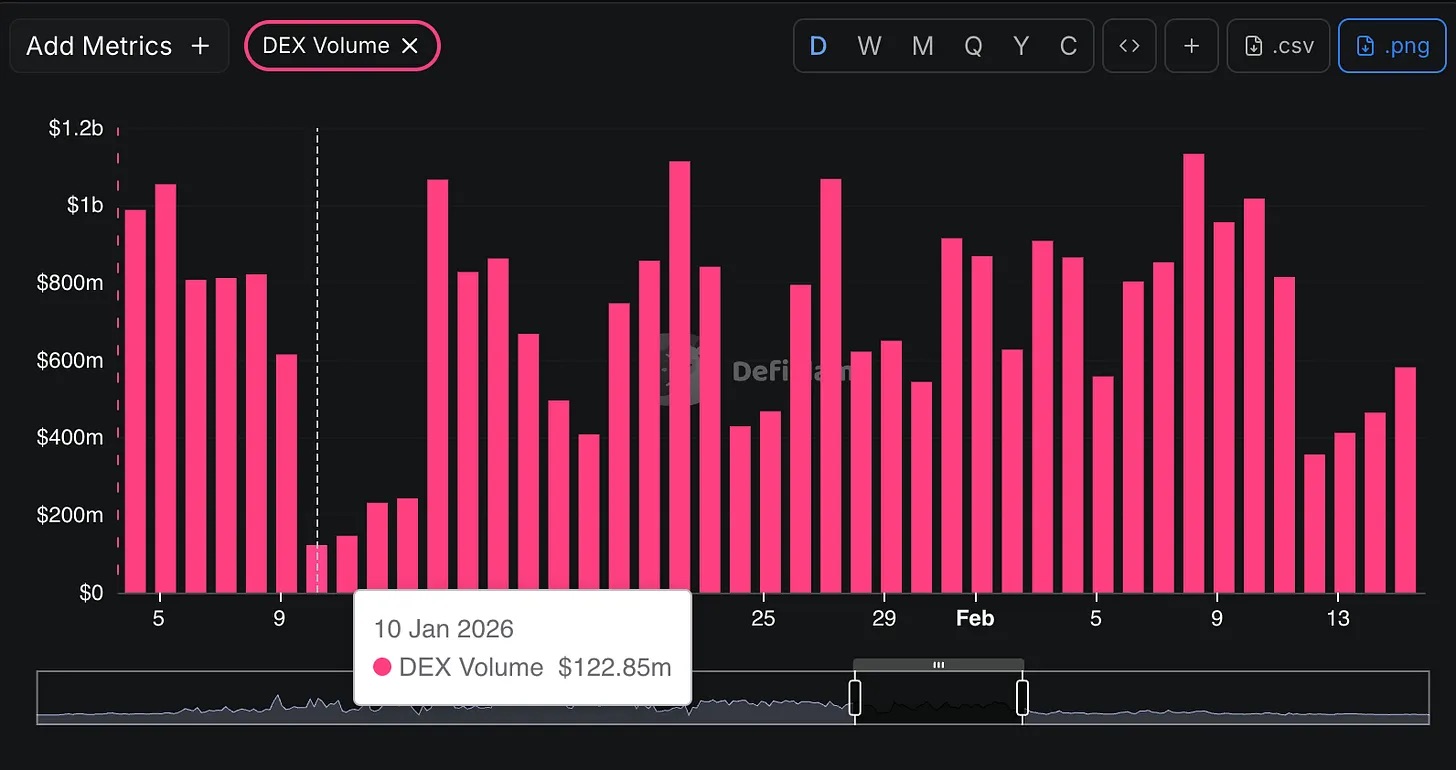

The competition logic in this market is quite abnormal: one institution can capture 68% of the market share within five months, yet lose more than half of that within just thirty days. In December 2025, HumidiFi's trading volume proportion in the Prop AMM track reached 68%, but a month later it plummeted to 26%, simply because competitors announced better prices.

From January 10 to 13, 2026, HumidiFi's daily trading volume fell off a cliff by 80%, yet the institution provided no explanations to the outside world.

Daily trading volume bar chart from January to February 2026, source: @defillama

BisonFi seized the opportunity and rose rapidly. In just three weeks, its daily trading volume soared from $180 million to $1.43 billion, with a total trading volume of $11.5 billion over the week.

By early February, BisonFi commanded 34% to 35% of the Prop AMM routing business, while HumidiFi maintained at 26%. BisonFi thus solidified its top position in the industry and has continued to uphold this advantage to this day.

Changes in market share of DEX aggregator routing trading volume on the Solana chain from early 2026 to May, source: @Blockworks

BisonFi was initially launched by the listed company Forward Industries at the end of 2025, with the company chairman being Kyle Samani of Multicoin. However, during the boom in trading volume, Forward Industries issued a statement saying that BisonFi was not one of its projects. Currently, the project's official domain name is also listed for sale. The identity of the leading project in Solana's largest order flow market has thus become vague and intriguing.

In this race, no one can maintain leadership indefinitely. Jupiter instigates bidding auctions for quotes in every block, promptly identifying the institution with the best quote and allocating orders to them. This mechanism encourages institutions to quickly provide quotes that align with the market midpoint. Globally, only about twenty teams possess the technical capabilities to do this, and even leading players can be displaced by other quantitative teams within weeks.

On January 28, Solana's second-largest decentralized exchange aggregator, DFlow, suspended connections with HumidiFi, claiming it was just routine maintenance. At that time, HumidiFi's on-chain contracts remained operational, but trading volume was significantly impacted, and long-term users of that trading channel received no notice, as Jupiter directly rerouted the order flow to other platforms.

Jupiter itself is a legitimate enterprise, possessing treasury assets, platform tokens, full-time employees, and complete financial statements. Each exchange transaction conducted through routing contracts incurs a fee, with higher fees for activating high-speed trading modes. Holders of the JUP token can participate in the sharing of these fees. Jupiter's core competitiveness lies in providing Solana users with top-notch trading execution services, which is also why massive trading volume continues to pool there.

Regarding the current situation where private closed-source entities control over half of Solana’s spot trading, Jupiter has no motivation to change. If Prop AMM were to be abandoned, the quality of trade execution would decline, overall trading volume would shrink, and profits for all involved parties would suffer. Even if these types of institutions were removed, the Jupiter platform would still operate, but the trading experience would significantly deteriorate: trading slippage would increase markedly, instantaneous best quotes would vanish, and the entire ecosystem would lose its core competitiveness.

Currently, the industry widely believes that the various risks mentioned in the article have never materialized, implying that these risks will never arise. However, looking at the history of financial development, the market has always held such a mentality before each systemic risk explodes.

Reflecting on the 1998 collapse of Long-Term Capital Management (LTCM): The fund was managed by one of Wall Street's top quantitative teams, relying on confidential mathematical models to derive profits, operating smoothly for a long time, leading the market to believe risks had been entirely mitigated by the model. Yet when a global crisis unexpectedly struck, its internal algorithms completely failed, private liquidity evaporated instantly, and the entire trading system collapsed within just a few days.

If the private programs that Jupiter connects to have pricing vulnerabilities, users often only realize after their assets are diminished. In contrast, open-source projects like Raydium, even if high-risk vulnerabilities arise, undergo a transparent repair process; whereas vulnerabilities in Prop AMM’s type would be completely concealed.

Traditional financial markets strictly prohibit market makers from front-running customer orders and impose strict regulations. However, within the Solana ecosystem, private trading teams have full control over their pricing rhythms, able to cease providing quotes at any time. Due to Solana’s trading ordering mechanism, it is impossible for outsiders to verify whether these institutions engage in behavior that bets against users, nor can the possibility be ruled out.

Even amid numerous risks, the entire ecosystem still accepts this model. The reason is that while open-source liquidity pools can meet the trading needs of basic crypto tokens, they cannot adapt to on-chain stocks, forex, and other real-world assets. If pricing for tokenized U.S. stocks and forex assets relies solely on simple passive formulas, high-frequency traders will exploit time differentials to siphon off liquidity pool assets.

Prop AMM addresses this issue by moving complex risk calculations off-chain. Private servers continuously push high-speed real-time quotes to Solana-customized programs, enabling them to swiftly respond to real market information, thereby clearing barriers for bringing traditional Wall Street assets on-chain. However, this also buries significant risks: if a private institution's server goes down, the program malfunctions, or incorrect data is pushed during market panic, the liquidity of the relevant assets could vanish instantly, leading the entire on-chain trading market into a standstill.

The original tenet of DeFi was to have codes public and accessible to all.

Now, although platform interfaces indicate that orders are routed through channels like TesseraV and SolFi, the actual entities responsible for pricing trades remain traditional financial institutions like Wintermute and Ellipsis Labs.

Players involved in this field are not limited to just those mentioned above; the entire industry is gradually evolving into a secret trading network composed of various private entities. For example, the Bebop platform connects directly to 12 to 15 private market makers for quotes; there are also low-profile protocols like Lifinity, ZeroFi, and Obric, which are categorized as "dark pool automated market makers" that do not have official websites, conduct no promotions, and have no communities, solely connecting to Jupiter in code form to capture user order flows. Traditional trading teams like Wincent continue to compete in this clandestine bidding for quotes.

I do not assert that users are being treated unfairly here. Objectively speaking, compared to most meme coin liquidity pools, professional institutions like Wintermute are indeed more reliable trading counterparties. Prop AMM compresses trading differentials almost to zero, objectively pushing the entire market towards maturity. Perhaps, this is a necessary path for the growth of an industry.

The crypto market's inclusiveness lies in the fact that if you adhere to decentralized principles and reject private closed-source technology, you can entirely bypass aggregators and complete token exchanges directly in public and transparent traditional liquidity pools.

However, the fact that private trading networks can occupy such a large market share is enough to prove that the core demand of the vast majority of users is simply to pursue the lowest trading cost.

We have long criticized traditional finance being controlled by Wall Street algorithms, with a closed system and lack of transparency. Yet when the crypto industry had the opportunity to build a new system from scratch, it ultimately replicated traditional finance's model—because this model is faster, cheaper, and more efficient.

Ultimately, every participant needs to make a choice: do you value low trading costs more, or decentralization and trading transparency?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。