Author: Winnie, CryptoPulse

In the past few years, there has been a peculiar phenomenon in the crypto market. The market has daily trading volumes of hundreds of billions of dollars, but the entities that tend to make the most stable profits are often not public chains, but exchanges.

Whether in a bull market or bear market, as long as the market has volatility, platforms like Binance, OKX, and Bybit can continue to collect fees, capture liquidity, and earn trading volumes. So, to some extent, the most stable business model in the crypto industry has never been about issuing coins, but about creating trading markets.

Now, Hyperliquid is truly bringing this model onto the chain for the first time. More importantly, Wall Street seems to have begun to realize this.

1. The most profitable business in Crypto——User Trading

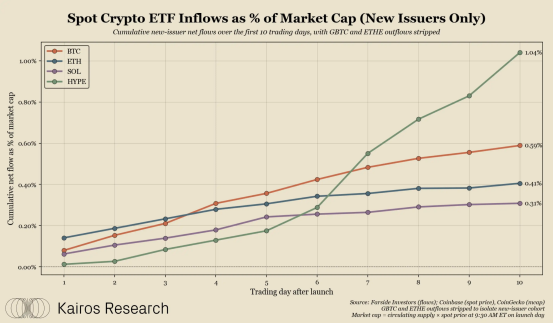

On May 27, Kairos Research data indicated that in just 10 trading days since the launch of the HYPE spot ETF, it had already absorbed funds amounting to 1.04% of the total HYPE market capitalization.

This data directly sets a new record for the debut of crypto spot ETFs. Even when compared to mainstream assets like BTC, ETH, and SOL, the capital-raising efficiency of HYPE remains far ahead.

If we exclude existing products that have been converted from trusts, like Grayscale GBTC and ETHE, HYPE can be considered the most formidable newly issued crypto ETF currently.

This may signify a larger change, which is that the capital market is re-evaluating crypto exchanges.

Many people in the past have understood the crypto industry by emphasizing public chains, AI, Memes, RWA, and other hot tracks. However, looking back over the past decade, one would find that most tracks exhibit strong cyclicality.

When a hot trend emerges, it can be quite fierce, but it can also recede rapidly. The trading market is different; regardless of market fluctuations, as long as there are trades, exchanges can continue to profit.

This was true during the 2021 bull market, also true during the 2022 crash, and will still be true in the 2024 ETF bull market. This is why Binance can consistently maintain the strongest profitability in the entire industry.

Because trading is essentially the most stable source of cash flow in the crypto world. What is special about Hyperliquid is that it has truly enabled on-chain exchanges to offer an experience close to that of centralized platforms for the first time.

Many on-chain derivatives platforms in the past faced a major problem: it was not that the concepts were bad, but they simply could not accommodate real large funds. With insufficient liquidity, high latency, and poor depth, professional traders could not use them for the long term.

But Hyperliquid chose another path. It did not continue with the traditional AMM model, but instead adopted order book matching, built its own Layer 1, and optimized performance to public chain standards.

The outcome is that it increasingly resembles a "Binance on the chain." This is also why, over the past six months, more and more high-frequency traders and quantitative teams have begun to migrate.

For professional traders, what is truly important has never been about decentralization or not. It is about whether the depth is sufficient, whether the latency is low, whether the fees are high, and whether it can consistently generate profits.

Hyperliquid has genuinely fulfilled these conditions for the first time. This is also an important reason why it has begun to be reassessed by institutional funds.

2.The HYPE ETF explosion is essentially betting on “on-chain Wall Street”

Many people still understand HYPE ETF as an ordinary crypto ETF. But in reality, it is very different from BTC ETFs and ETH ETFs.

BTC ETFs are more like digital gold, while ETH ETFs lean towards blockchain infrastructure. However, HYPE ETFs are essentially betting on the trading capabilities of the entire on-chain financial market.

In other words, what institutions are really focused on may not be the HYPE token itself, but rather the trading ecosystem behind Hyperliquid. This can already be clearly seen from the on-chain data.

Data from May 27 shows that the Hyperliquid ETF achieved a net inflow of 20.4 million USD in a single day. Among these, BHYP had a net inflow of 19 million USD, and THYP saw a net inflow of 1.4 million USD.

More crucially, this type of ETF has achieved net inflow for 15 consecutive days, with total capital exceeding 101 million USD. This indicates that institutional funds are not short-term speculation, but are in a phase of ongoing allocation.

At the same time, the on-chain fundamentals of Hyperliquid are also beginning to strengthen. The platform's TVL has reached 5.529 billion USD.

This is a new high since the "10.11 crash." The open interest also rose to 9.647 billion USD, marking the highest level since February of this year.

The trading volume over the past 24 hours reached 7 billion USD. Notably, about 28.1% of the trading volume has come from traditional markets in the HIP-3 ecosystem.

This means that Hyperliquid is no longer just being used by crypto users. It is starting to absorb traffic from traditional financial markets.

In some ways, Hyperliquid is beginning to do one thing: bringing the NASDAQ, foreign exchange markets, and traditional derivatives trading gradually onto the chain.

This might be where the true excitement of capital lies.

3.HYPE ETF is forming a new capital flywheel

Many people still discuss Hyperliquid within the context of the DeFi track. But in reality, what it is challenging might not be GMX or dYdX, but Binance.

Because over the past few years, centralized exchanges have always firmly held the core power of the industry. Liquidity, user assets, contract trading, and market pricing power are almost all concentrated in leading platforms.

In the on-chain world, for the most part, it can only accommodate long-tail demands. But the emergence of Hyperliquid has allowed the market to see another possibility: the on-chain can also support mainstream trading markets.

This situation is actually very dangerous. Because once the on-chain trading experience approaches that of centralized platforms, future market makers, quantitative funds, and high-frequency trading institutions may gradually migrate.

And once trading migrates, liquidity migration will inevitably follow. After the migration of liquidity, pricing power will also begin to shift.

This is why more and more people are starting to see Hyperliquid as a combination of an on-chain version of CME and Binance. It is no longer just a DeFi project; it resembles a growing on-chain financial infrastructure.

More importantly, the emergence of ETFs will further reinforce this trend. ETFs bring institutional funds to HYPE, and institutional funds drive the increase in market attention.

More users and traders enter Hyperliquid; the platform's trading volume and TVL continue to grow, ultimately reinforcing HYPE's valuation logic with on-chain cash flow. This will create a very typical financialization flywheel.

Historically, the major cycles in the crypto market have often arisen from this resonance between capital and fundamentals. BTC ETFs were like this, stablecoins were like this, and RWA was like this. Now, the on-chain perpetual contract market may also be entering this stage.

Of course, risks still exist. Regulatory issues, security, extreme market liquidity pressures, and competition with giants like Binance will all be challenges Hyperliquid must face in the future.

Conclusion

Especially after experiencing the "10.11 crash," the market remains vigilant regarding on-chain high-leverage systems. But it is undeniable that the explosion of the HYPE ETF has released a very clear signal. What Wall Street is genuinely interested in may no longer just be holding crypto assets, but rather starting to directly participate in the trading market of the crypto world itself.

This may also imply that the biggest battle in the next round of the crypto industry will no longer just be a public chain contest. Instead, on-chain exchanges will begin to challenge the traditional centralized trading empires.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。