Author: Duck TATAYA

When Trading Ability Itself Becomes a Scarce Commodity

When we previously discussed Hong Kong stocks, US stocks, and global asset allocation, the primary concern was often "what to buy." After the "5.22" incident, a more fundamental question was brought to the forefront: what channels are still available for trading, and whether these channels are compliant, stable, and sustainable. The concentrated rectification of illegal cross-border securities, futures, and fund operations by eight departments has redefined the boundaries for some overseas internet brokerages providing services to mainland Chinese users. The incident itself is not merely a regulatory storm for a few brokerages, but more like a reminder at the infrastructure level: trading is not a naturally available public good. Accounts, deposits, withdrawals, quotes, matching, clearing, custody, taxation, and cross-border regulation are all part of trading capability.

In this context, crypto platforms and on-chain RWA have regained the spotlight. They are not necessarily safer, nor inherently more compliant, but they do provide a set of trading organization methods different from traditional brokerages.

5.22, Countdown to the Cleaning of Cross-Border Brokerages

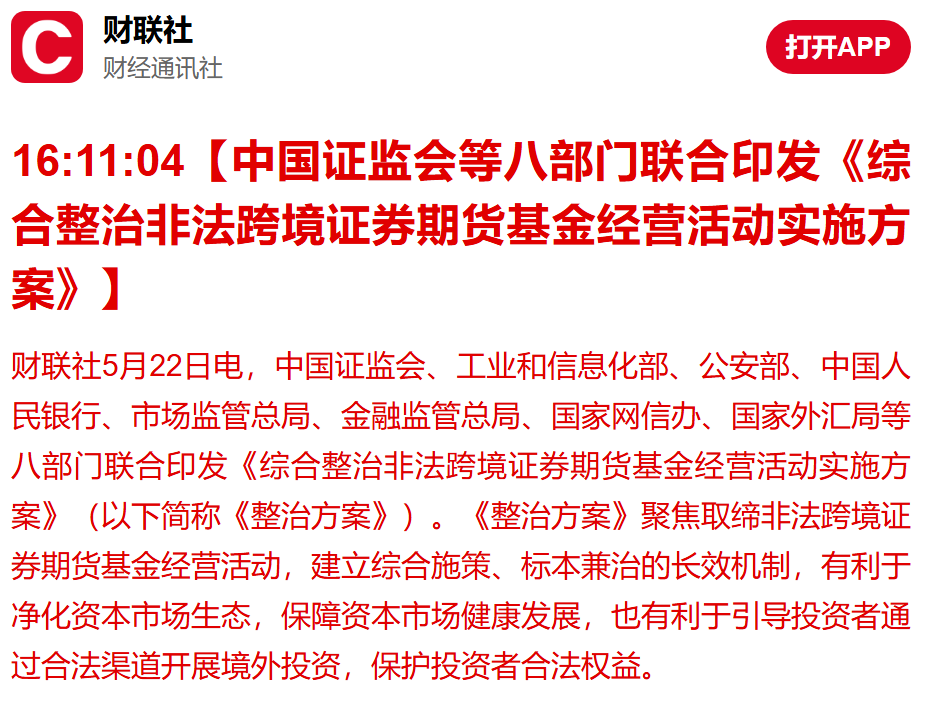

On May 22, 2026, the China Securities Regulatory Commission and other eight departments jointly issued the "Implementation Plan for Comprehensive Rectification of Illegal Cross-Border Securities, Futures, and Fund Operations." The rectification goal has progressed from the early focus of "curbing increment" to "cleaning up stock." Since 2022, the regulatory focus has mainly been on prohibiting overseas institutions from further illegally soliciting domestic investors and opening new accounts; this round of the plan further requires the complete ban of illegal cross-border operations by overseas institutions after two years of concentrated rectification.

For existing investors, the policy arrangement is not to immediately close accounts or forcibly cancel accounts, but to establish a one-way exit mechanism. During the concentrated rectification period, overseas institutions are not allowed to continue illegally providing buying transactions, transferring funds, and other services for domestic existing investors; they are only allowed to provide selling transactions and fund withdrawals. After the concentrated rectification period ends, relevant institutions should completely shut down domestic websites, trading software, and associated services.

On the same day, the Securities Regulatory Commission also disclosed the advance notice of investigations and administrative penalties against Tiger Brokers (NZ) Limited, Futu Securities International (Hong Kong) Limited, and Changqiao Securities (Hong Kong) Limited regarding their domestic and foreign related entities. The core of the regulatory determination is that they have, without approval from the China Securities Regulatory Commission, engaged in securities marketing, processing trading instructions, and other services within China and received profits.

Therefore, the essence of this incident is a reaffirmation by regulatory authorities of the boundaries of cross-border financial services: providing securities, funds, futures, and derivative-related operational services to investors in mainland China must comply with the domestic regulatory framework.

Pallid Response, the Cut Between Growth and Compliance

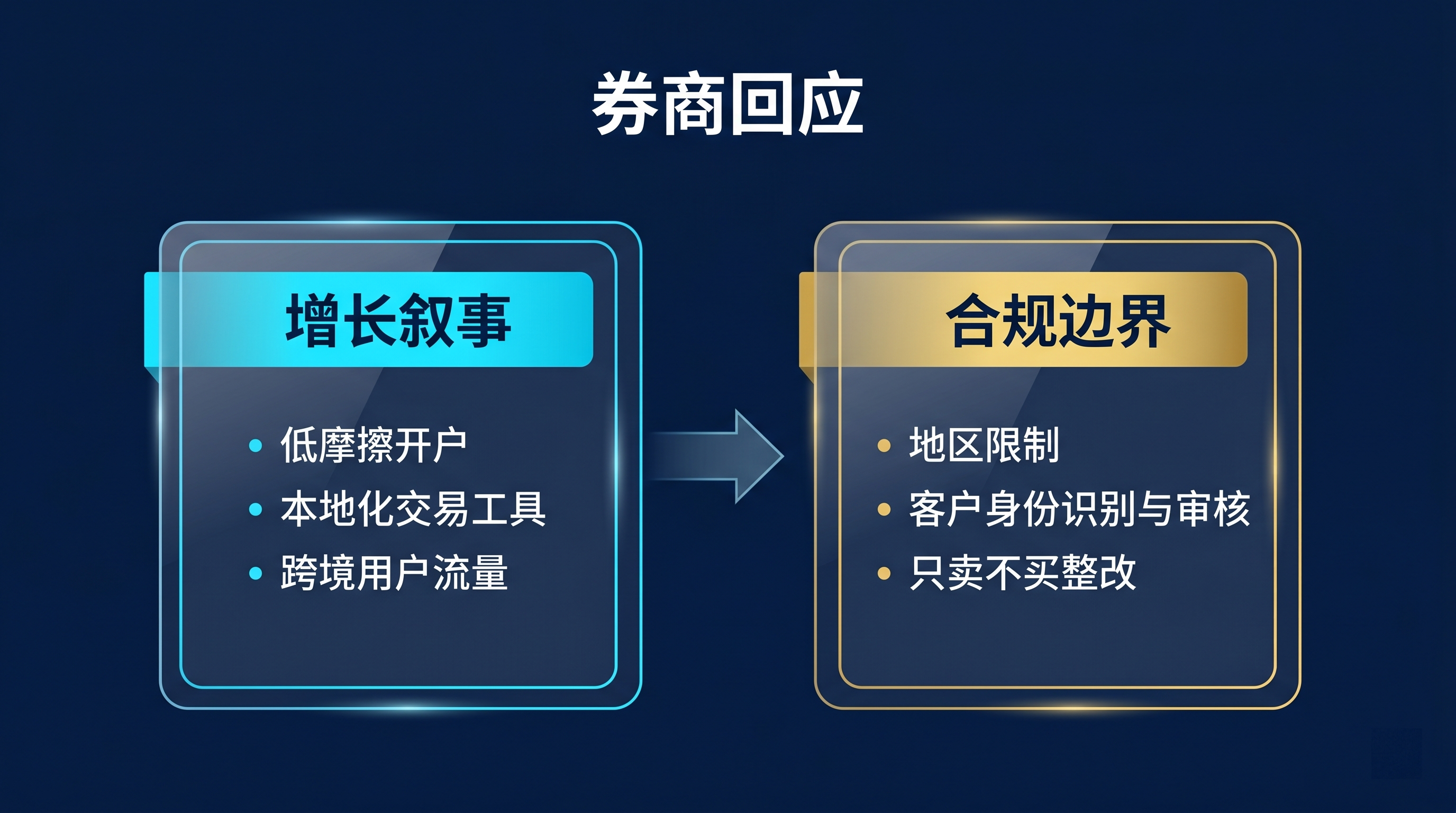

From the public responses, the statements from related brokerages show a similar direction: they no longer emphasize growth among mainland users, but rather stress rectification, regional isolation, disposal of existing accounts, and the safety of customer assets.

Futu's response focuses on its ongoing communication with the China Securities Regulatory Commission, implementing rectification measures for its mainland business; it also emphasizes that its operations in regions outside mainland China are normal. The statement from Tiger International centers on having stopped opening accounts for users with mainland Chinese identities since 2023, simultaneously ceasing external advertising, marketing promotions, and activities, while strengthening account audits, identity verification, and anti-fraud management. Changqiao Securities emphasizes that its licensed entity is regulated by the Hong Kong Securities and Futures Commission and other foreign regulatory agencies, with customer funds isolated from the company's operating funds, US stocks and Hong Kong stocks being held by the respective custody and settlement systems, and will implement rectification requirements.

These responses indicate that the business logic of internet brokerages is switching. In the past, the competitive focus of mobile internet brokerages was on low-threshold account opening, Chinese interfaces, low commissions, market tools, and community operations; now, the key issues have become the jurisdiction of the service target, the location of marketing activities, how trading instructions are processed, and whether the platform has regulatory permission to operate in the target market.

The current situation is that the "user experience narrative" of the brokerage industry is yielding to the "compliance boundary narrative." When a service crosses multiple jurisdictions, the convenience of the front-end app is no longer the only evaluation standard; the underlying legal relationships and regulatory permissions determine whether the service can continue to exist.

The Real Meaning of Licenses, White Labels, and Clearing Links

To better understand this incident, we need to distinguish three concepts: brokerage licenses, introducing broker models, and clearing capabilities.

In the US stock market, introducing brokers and white label models are not inherently gray. Introducing brokers are responsible for front-end customer acquisition, product interfaces, and customer service, while upstream clearing agents are responsible for trade execution, clearing, custody, and underlying account capabilities. The two usually delineate responsibilities through clearing agreements and are subject to corresponding regulatory rules. What users see is the app of a brokerage; but from the asset link perspective, where the funds enter which bank, which system the securities are custodied in, and who clears the trades, are the core risk control issues.

Data shows that Tiger previously conducted business through a New Zealand entity and upstream clearing links before listing, and later upgraded to a US-regulated entity through the acquisition of a local US brokerage. Futu relied more on Hong Kong licenses and US upstream clearing links in its early days, subsequently establishing a more complete US clearing capability through Futu Clearing Inc. Changqiao possesses relevant brokerage qualifications, but its underlying clearing arrangements differ from those of Futu and Tiger.

The so-called compliance qualifications for US stock brokerages are not a single label, but a combination of arrangements such as SEC registration, FINRA membership, CRD number, DTC/NSCC clearing or transfer capabilities, and SIPC protection. Among them, having independent clearing capabilities determines whether a platform can keep more trading, custody, and risk control processes within its own system.

However, this does not equal to "having overseas licenses means serving mainland Chinese users." Overseas licenses address the question of whether business can be conducted in the corresponding overseas market but do not automatically solve the issues of soliciting customers, opening accounts, processing trading instructions, and transferring funds in mainland China. The essence of the current regulation touches the boundaries of the business targets and service locations.

New and Old Demands Intertwined, Crypto and RWA Back in the Spotlight

Financial needs do not typically disappear because a channel contracts. For some users, the underlying needs behind US stocks, Hong Kong stocks, and global asset allocation include exposure to dollar assets, growth exposure of tech companies, hedging against local currency asset volatility, and higher volatility trading opportunities. When traditional internet brokerage entrances are restricted, these needs may shift to other channels.

Crypto has regained the spotlight firstly because stablecoins provide a unified unit of valuation and circulation. Stablecoins like USDT and USDC abstract "funds" into digital balances that can move between multiple platforms, wallets, and protocols. Secondly, centralized exchanges provide accounts, matching, market data, leverage, and liquidity. Thirdly, on-chain wallets and DEX allow asset issuers to expose tokenized stocks, funds, bonds, or commodities to on-chain users. Lastly, perpetual contracts provide 24/7 trading, leverage, long and short positions, and cross-asset margin as risk expression tools.

This is also why on-chain RWA has received attention. For crypto users, stock tokens are not meant to replicate traditional brokerages but to transform traditional financial assets into an asset format understandable by crypto trading systems.

However, the migration of demand does not mean the disappearance of risks. Risks are even more likely to descend from licensed brokerages to cash flows, OTC, KYC, smart contracts, price oracles, market makers, and tax declarations. Regulation may also extend from brokerages to stablecoin entrances, exchange regional restrictions, on-chain address identification, and cross-border tax information exchange. Therefore, the rise of crypto does not signify free expansion in a regulatory vacuum, but a new way of risk bearing.

Multiple Paths, What is Mainstream?

When discussing "buying stocks with fiat/stablecoins," the most common misunderstanding is conflating different products. In reality, there are at least four types of paths.

The first type is traditional compliant alternative paths. This includes QDII funds, Hong Kong Stock Connect, cross-border wealth management connect, Hong Kong bank or brokerage accounts, overseas compliant brokerages, etc. This path has relatively clear regulatory relationships, but limits, thresholds, target ranges, and trading experiences vary.

The second type is stock token spot markets. xStocks on Kraken, some exchanges that connect to xStocks or Ondo assets typically attempt to provide users with price exposure corresponding to US stocks or ETFs. Official sources for xStocks indicate that its products are issued by Backed, with some products supported by a 1:1 underlying asset; Ondo Global Markets has extended tokenized US stocks and ETFs to the BNB Chain and other on-chain ecosystems. The key is that what users hold is an on-chain token or an arrangement for claiming underlying value, not the original stocks in a traditional brokerage account. Voting rights, dividend handling, redemption qualifications, regional restrictions, and investor protection must be based on specific product documentation.

The third type is wallets and on-chain swap entrances. For example, Binance Wallet, on-chain DEX, or aggregators may allow users to access tokenized assets like Ondo. This path is more open but requires users to identify networks, contract addresses, slippage, pool depth, and smart contract risks on their own. Just because an asset is visible in a wallet does not mean it has adequate liquidity.

The fourth type is CFD, perpetual stock contracts, and Pre-IPO/RWA certificates. These products are closer to trading tools rather than long-term holding instruments. CFDs provide exposure through contracts for difference, perpetual contracts offer leverage and funding rate mechanisms, while Pre-IPO or private equity certificates involve more complex issues regarding information asymmetry, custody, valuation, and exit. They have stronger trading attributes and cannot simply be labeled as "buying stocks."

Therefore, stock tokens, CFDs, perpetual contracts, and real stocks are not the same type of asset. They may track the same price symbols, but their legal rights, trading times, liquidity sources, price formation mechanisms, and default risks differ. The correct question is not "which platform can I buy on," but "what rights does the product grant, who bears the risk, and what are the exit paths."

Looking Ahead, Tokenize OR Re-control Everything

In the coming years, the tokenization of global assets and the re-boundarization of sovereign regulation may accelerate simultaneously. On one side is Tokenize Everything: stocks, bonds, funds, gold, private equity, and index exposure are all attempting to enter the on-chain system. On the other side is Re-control Everything: regulators around the world will redefine boundaries around investor protection, foreign exchange management, anti-money laundering, tax transparency, and cross-border enforcement.

In this tug-of-war, the user structure may be re-layered. Ordinary investors may return more to compliant channels such as QDII, Hong Kong Stock Connect, and domestic funds; high-net-worth individuals may continue to allocate global assets through Hong Kong, Singapore, or offshore structures; and native crypto users may continue to seek higher efficiency trading entrances on-chain, but bear higher risks related to cash flows, taxes, platforms, and contracts.

Platforms will also differentiate. The more mainstream the exchange, the more it will require regional restrictions, KYC, product layering, and compliance disclosures; the more open on-chain protocols may face issues such as dispersed liquidity, information opacity, and insufficient regulatory reach.

Returning to the topic, when trading itself becomes a threshold, the elevation of crypto platforms is not a simple substitute for traditional finance. It is more like a redistribution of trading demand, regulatory boundaries, and risk-bearing methods. Traditional brokerages provide a clear legal relationship account system; crypto platforms offer high liquidity and combinability in trading interfaces. The two will re-divide labor in more complex collaborative ways among different users, different jurisdictions, and different risk preferences.

(This article discusses changes in market structure and does not constitute any investment advice, platform recommendations, or regulatory evasion advice. The parts involving specific institutions and products are only used to illustrate the differences in trading models and infrastructure.)

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。