NVIDIA's financial report has nothing much to say, just toothpaste-like data. There’s a feeling that market investors have normalized the expectation of NVIDIA exceeding forecasts, and unless there is a significant upside, they basically won't buy it!

However, coming back to the point, for a company of this size, significantly exceeding expectations is itself quite difficult. The good news is the $80 billion buyback and increased dividends, which can be seen as a consolation for shareholders!

What draws my most attention is that Jensen Huang mentioned the launch of Vera Rubin mass production shipments in Q3 this year. I believe this is the key weapon for NVIDIA to break through $10 trillion. Currently, many institutions are raising their price targets for NVIDIA's stock, from $260 to over $300.

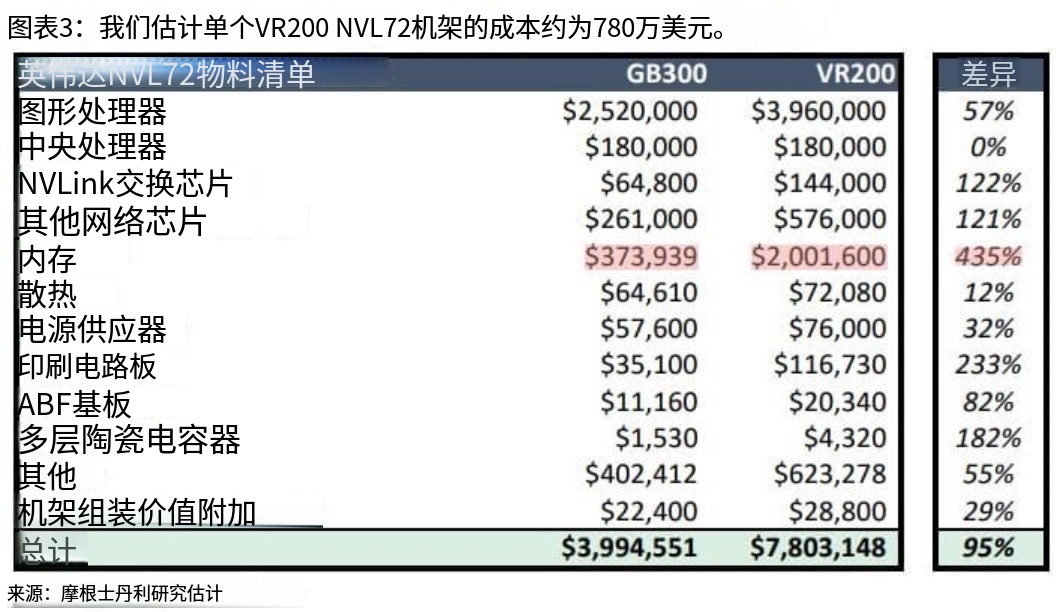

Today, Morgan Stanley simultaneously released a research report that deserves attention, comparing the production costs of two generations of NVIDIA products. Among them, the GB300 represents NVIDIA's flagship work under the current Blackwell architecture, while the VR200 is the flagship cabinet solution from the latest Q3 volume production of the Vera Rubin architecture.

The most noteworthy material price, with the largest increase, is the memory chips. A VR200 cabinet costs $7.8 million, with memory accounting for $2 million, which is 26% of the total cost, an increase of 435% from the previous generation GB300 cost.

Those who understand this know that memory chips can still be speculated for at least another year. I continue to hold Micron Technology (#MU), Samsung, and SK Hynix. In South Korea, I mainly hold the #EWY Korea Index ETF and Hong Kong stock 07709, which is twice leveraged long on SK Hynix. 🧐

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。