Where has all the money gone?

The S&P 500 was still hitting historical highs last week, and the Nasdaq finished nearly seven weeks of consecutive gains. The yield on the 30-year U.S. Treasury bond surged to 5.12%, the highest since 2007. SpaceX's Pre-IPO contracts on Hyperliquid generated $40 million in transactions on the first day.

Funds are flowing in everywhere, except for crypto. BTC just stood above $82,000 on May 14 but has dropped below $77,000 these past few days. ETH fared slightly better, falling nearly 10% during the week, from the $2,300 range to $2,110. Solana completely retraced its recent gains, falling back from a nearly $100 high to $84. It seems that the crypto industry has nothing concrete to show besides HYPE.

Why is crypto lagging behind despite being a risky asset?

30-Year Bond Yield Hits Nearly 20-Year High

The bond market is becoming the gravitational center of global capital once again.

The yield on the 30-year U.S. Treasury bond reached its highest level since June 2007, rising from 4.63% at the end of February to 5.12%. Meanwhile, the yield on the 10-year Treasury bond hit 4.6%, and the two-year bond yield increased to 4.08%.

It's not just the U.S. Apollo Global Management's Chief Economist Torsten Slok noted in a report on Sunday, May 17, that G7 nations' 10-year or longer government bond yields have reached the highest levels since 2004, collectively approaching 5%.

Governments worldwide are expanding fiscal deficits, needing to borrow more money and issue more bonds. The U.S. fiscal deficit still accounts for about 6% of GDP. Rising borrowing costs make it harder for governments to escape crises through fiscal spending, especially as many countries face crises due to wars.

Jim Reid from Deutsche Bank pointed out in a report on May 18 that the issue of bonds is likely to be one of the agendas at the two-day G7 Finance Ministers' meeting that started in Paris on that day. However, the structural problems in the bond market cannot be resolved by any single ministerial meeting.

In times of heightened geopolitical tension, global capital increasingly favors assets with certain returns.

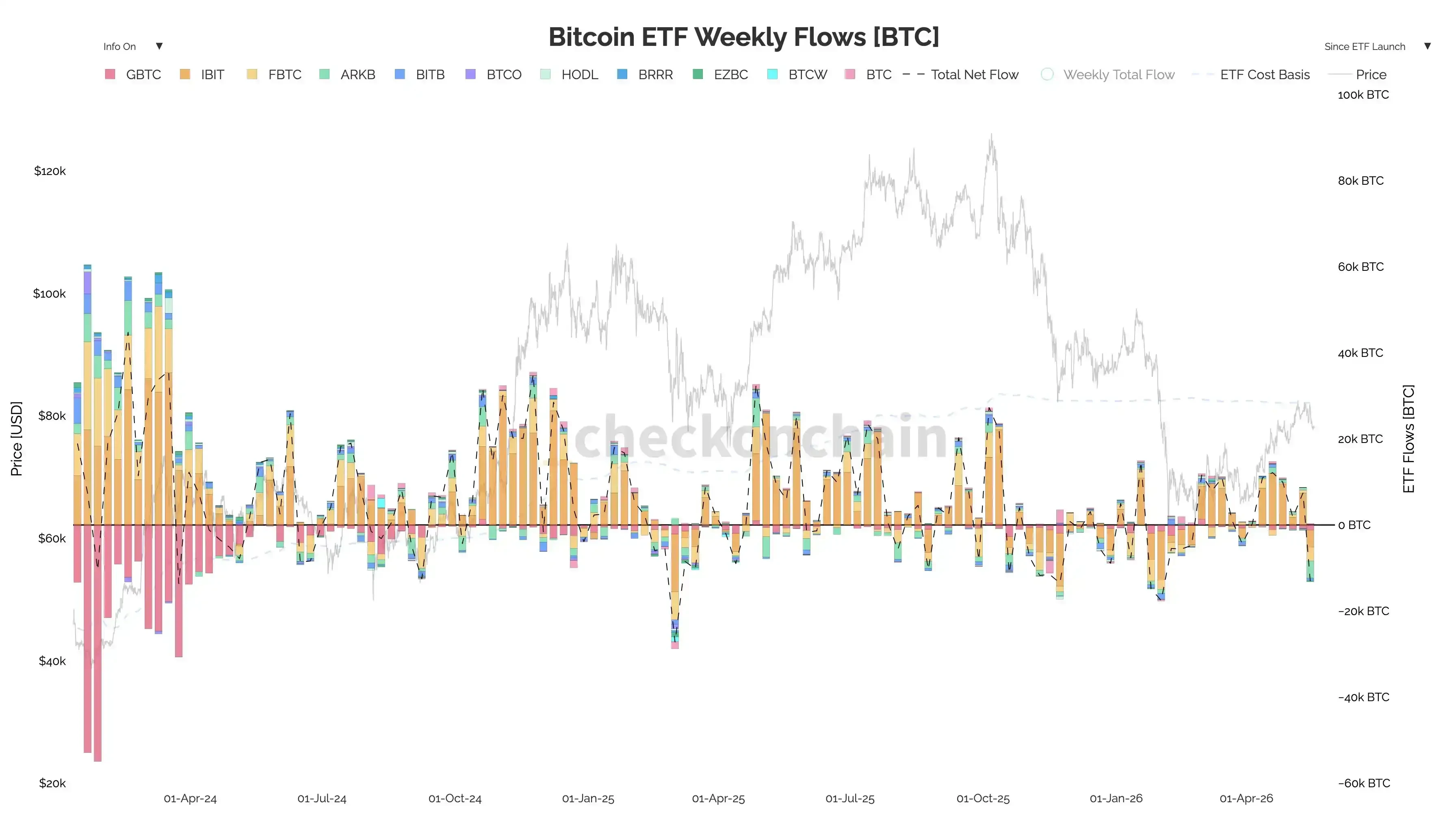

The data outflow from Bitcoin ETFs can also support this point.

According to SoSoValue data, Bitcoin spot ETFs faced a net outflow of $1.039 billion during the week of May 11 to May 15, ending a six-week streak of inflows, marking the largest single-week outflow since the end of January.

On a product level, ARKB saw a net outflow of $324 million in a week, while IBIT had a net outflow of $317 million, with both leading products bleeding simultaneously. Daily data presented a sharper picture. On May 12, there was a net outflow of $233 million, on May 13 there was a single-day withdrawal of $635 million, and on Friday, May 15, 11 Bitcoin ETFs collectively saw an outflow of $290 million, indicating that institutional funds are withdrawing in an orderly manner.

Comparing with data from previous weeks highlights the magnitude of the turning point. The week of April 17 saw nearly $1 billion in inflows, the week of April 24 had inflows of $824 million, and the week of May 8 still saw inflows of $623 million. In just one week, the funding landscape reversed from "continuous inflow" to "single-week outflow of $1 billion."

During that same period, Ethereum ETFs also experienced a net outflow of $255 million, marking five consecutive days of negative outflows. The entire crypto ETF asset class saw a collective trend reversal in mid-May.

As the attractiveness of the bond market increases, the relative appeal of crypto naturally diminishes.

$4 Trillion IPO, How Can Crypto Win?

The funds drawn away by bonds are from risk-averse investors. The money drawn away by IPOs is from risk-seeking capital, which can be said to be the most direct liquidity withdrawal from crypto.

There is still $4 trillion in IPOs queued up waiting to grab capital by 2026. This is a figure large enough to reshape the global capital allocation landscape.

SpaceX has become the next focal point of the market. In this environment, Pre-IPO and initial offering strategies provide an appeal that bonds cannot offer, namely non-linear wealth effects.

Simultaneously, the AI narrative is again the main storyline for 2026. Evercore analysts noted in a report on May 15 that U.S. economic data shows demand remains strong, especially with a surge in AI-related capital expenditures. The other side of this AI capital expenditure boom is that AI leaders in the secondary market create life-changing wealth effects.

Names like Nvidia and Cerebras make any crypto narrative seem less attractive.

What's more, even the blockchain itself is helping traditional markets grab funds.

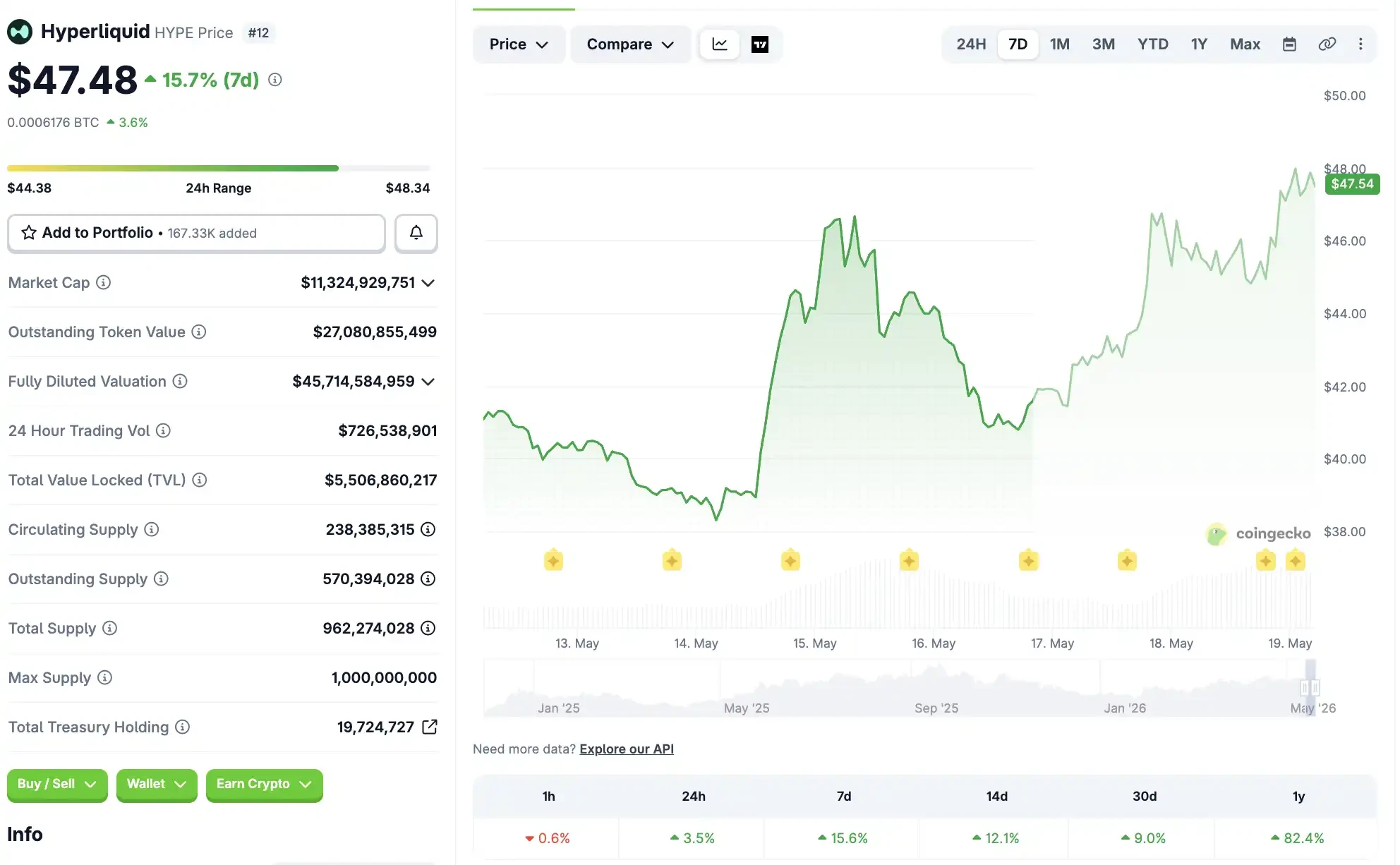

On the night SpaceX launched on Trade.xyz, the Pre-IPO contracts on Hyperliquid transacted $40 million on the first day. The HIP-3 platform is using perpetual contracts for price discovery in traditional stocks. Because of this, Hyperliquid itself surged 10% to $45, becoming the only mainstream asset to rise against the trend in the crypto market. Related reading: “The Biggest Winner of the SpaceX IPO May Be Trade.xyz.”

In the short term, this does not bode well for crypto-native assets.

The liquidity on the chain is being directed towards pricing traditional stock targets like SpaceX rather than flowing back to Bitcoin, ETH, or Solana. Even the increase in Hyperliquid is essentially due to the narrative bonuses from traditional assets, not from crypto narratives.

Warsh Takes Office, But Rate Cuts May Be Overturned

The bond market and IPO market have drawn liquidity out of the crypto space; looking over at the Federal Reserve, we may not expect the new liquidity that we had anticipated.

Powell's term ended on May 15. Warsh received Senate confirmation last week to become the Fed Chair and is currently awaiting formal appointment from the president's approval committee and completing asset liquidations to comply with ethical standards.

However, even before Warsh officially took his oath, he is already facing several challenges.

Trump nominated Warsh partly hoping he would be more cooperative with the White House's cost-cutting agenda than Powell. Treasury Secretary Bessent has been writing the reduction of Treasury borrowing costs into the core of the White House's cost-cutting commitments over the past few months, as he thoroughly mentioned in a speech last fall at the New York Fed—reducing Treasury borrowing costs means lowering corporate borrowing costs, lowering mortgage rates, and reducing car loan payments, thus increasing affordability for all Americans.

But as previously mentioned, today's reality is that the bond market has already pushed future five-year inflation expectations to 2.7%, the highest since 2023. Yardeni Research pointed out directly in a report on May 17 that the two-year Treasury yield of 4.08% indicates that the market is signaling to the Fed that the current target range of 3.50%-3.75% is too low.

According to Warsh's own logic, he should continue to raise interest rates; at the very least, he should not cut rates. However, the political demand for a rate cut from the White House, especially from Trump himself, is almost public.

On the other hand, those who heard Warsh's testimony before taking office will know that he spent a lot of time discussing AI at the hearings. He believes AI will enhance productivity and lower inflation, thus supporting rate cuts. But the issue is that short-term data shows no signs of this.

José Torres, a senior economist at Interactive Brokers, reflects the views of a significant portion of people in his report on May 15, stating that due to a lack of progress in geopolitical conflicts, the market has abandoned bets on interest rate tightening.

If Warsh chooses to bow to Trump's political pressure and cuts rates against his better judgment, the bond market will respond with higher long-end yields, making all duration assets worse off. If Warsh chooses a hawkish stance, then this year's expectations for rate cuts will be dashed, requiring a complete repricing of market bets on liquidity easing.

This means that the market's past few months of betting on a rate cut after Warsh's appointment could be completely overturned.

HYPE Leads Crypto

After October 10, the corrective period in the crypto market following the burst of leverage should have been completed by the inflow of new funds.

With $4 trillion in IPOs queued up for 2026 and AI continuing to create wealth effects, the appeal of altcoins is being continuously diluted. Even the most institutional-grade crypto asset, Bitcoin, is starting to give way to traditional markets. The ETF outflow of $1 billion in a week is the most direct evidence.

The high interest rates in the bond market and the outflows from Bitcoin ETFs prolong the correction period indefinitely, preventing crypto from keeping up with the overall rising rhythm of risk assets.

However, it is worth noting that there are already some signs of differentiation within the crypto market.

Hyperliquid surged 15% to $48, with a year-to-date increase of 69%, thanks to the price discovery narrative on HIP-3's Pre-IPO. Assets capable of telling new stories and entering traditional markets continue to rise, while purely beta-driven assets are being squeezed in their pricing, with Bitcoin even forced to take a back seat.

Looking at the overall financial market from a broader perspective, three forces have simultaneously withdrawn liquidity from the crypto space in recent weeks. The bond market is pulling risk-free money back with a 5% yield, IPOs are mopping up additional risk budgets with a queued scale of $4 trillion, and the newly appointed Federal Reserve Chair Warsh may not fulfill expectations for a rate cut this year.

However, there are still favorable catalysts for Bitcoin in the next phase.

The upward catalyst is the implementation of the CLARITY Act in August. This is the largest policy window for crypto this year, and the increase in regulatory certainty will directly release some suppressed institutional demand.

The downward risk is that before the catalysts are fulfilled, there may be a need to retest the $70,000 level. If the current position of $77,000 cannot hold, the next significant support is likely around $70,000.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。