The track everyone is flocking to is actually shrinking.

Written by: Vaidik Mandloi

Translated by: Chopper, Foresight News

Recently, I saw a regular person named Robert on the social media platform Reddit. He is 49 years old, works for a construction company in Houston, Texas, and every two weeks sends $300 to his parents living in Puebla, Mexico, to cover their daily groceries and rent expenses. Every other Friday, he goes to Western Union, fills out a form, pays in cash, and sends the money. He has been repeating this process for nine years and doesn’t even know what a stablecoin is.

By 2025, the remittance market in Latin America is expected to reach $174 billion. After six months of field research in five countries, Bybit reached a key conclusion: the vast majority of fintech companies entering this market have chosen the wrong direction, target users, and products.

I delved deeply into the data of various remittance channels and frontline research results, and what I saw was a stark contrast to the commonly held perceptions in the market.

Choosing the Wrong Track: Treating Latin America as a Single Market

The first fatal misconception for fintech companies entering the Latin American market is treating Latin America as a unified whole.

The business pitch deck might state this clearly: directly displaying the potential market size of $174 billion, encircling the entire Latin American region. But in reality, Latin America actually consists of three completely fragmented remittance markets, each with different operational logic.

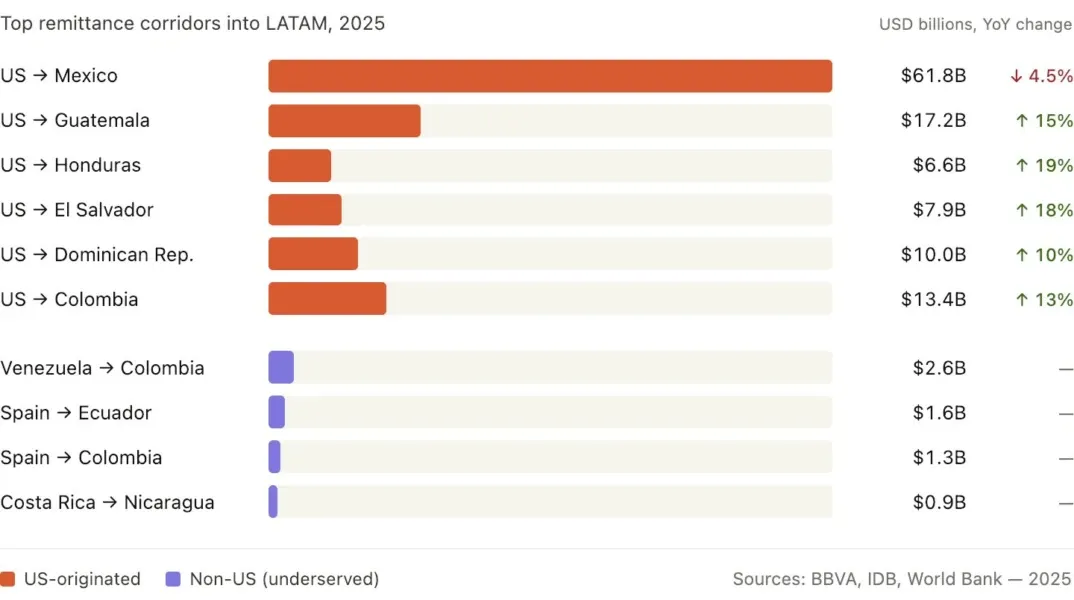

Mexico is the most mature market and the first stop for those entering Latin America, with an annual remittance scale of $62 billion; it is the largest single flow of funds channel in the Western Hemisphere. Mexico boasts one of the world's top instant bank transfer systems, SPEI; it has 3.7 million residents living in the United States, many of whom have settled there for decades; the regulatory environment is clear, with comprehensive data infrastructure and a mature industry cooperation ecosystem. Naturally, all fintech and crypto startups flock to establish their presence in Mexico first.

However, this most popular track has begun to shrink for the first time in 11 years.

The market attributes the reasons to U.S. policy, but the downward trend had already begun to show in November 2023, 20 months ahead of any regulatory overhaul. Long-term remittance providers like Robert are aging; their children are growing up in Houston and their emotional ties to their ancestral home in Mexico are weakening; the number of new immigrants to Mexico has sharply decreased, while 3.5 million people from other Latin American countries have already surged into the United States.

All mature immigrant communities go through this cycle: it was the same for immigrants from Italy, Ireland, and Greece, and now Mexico is entering the same stage.

In contrast, Central America is experiencing rapid growth in the remittance market: Honduras has increased by 25.3% year-on-year, Guatemala by 18.7%, and El Salvador by 17.9%.

The driving forces behind this growth are intriguing. Immigrants from these countries fear deportation, resulting in a 27% increase in the average amount sent per remittance compared to last year. Women are working extra hours to increase income, and men are taking second jobs, sending as much money as possible to their families back home while they still can.

Remittances are deeply tied to the local economy: remittances represent 30% of GDP in Honduras, 27% in El Salvador, and 21% in Guatemala. The local consumer economy is entirely built on the continuous influx of remittances, influencing prices, labor markets, and consumer spending habits. This is reminiscent of Gulf countries that rely on oil income; if remittances fluctuate by 20% in a year, all downstream economic links will change accordingly.

Compared to Mexico, the infrastructure here is very lacking. There is no instant transfer system comparable to SPEI, digital payment channels are scarce, and 45% of remitters are still using cash for remittances. Even in digitized Mexico, where 99% of remittances have shifted online, 51% of recipients still have to withdraw cash offline. The remittance side has long been digitized, but the families receiving the money back in their hometown still have to rush to offline outlets to collect cash.

South America operates under a completely different logic, represented by Argentina, Colombia, and Venezuela. The core demand has long shifted from simply cross-border remittances to acquiring dollar-denominated assets, which will be explained in detail later.

Outside of Mexico, other remittance markets in Latin America amount to approximately $112 billion. A single corridor from Venezuela to Colombia has a remittance scale of $2.6 billion annually. This corridor has long operated on a peer-to-peer stablecoin exchange via WhatsApp. After the local banking system collapsed, the public spontaneously established private money transfer channels.

In the past five years, fintech companies have flooded into the saturated $62 billion market in Mexico, while the emerging track worth $112 billion that is still growing rapidly has hardly any players investing deeply.

Getting the Product Wrong: The Core is Never the Transfer Itself

The second misunderstanding among fintech companies is a complete misinterpretation of the products that users truly need. The narrative of remittances in all crypto sectors in Latin America emphasizes optimizing the transfer experience: faster, cheaper, using stablecoins to replace SWIFT's traditional channels.

However, the transfer is precisely the least relevant part of the entire chain. Robert insists on using Western Union not because the transfer experience is good, but because nine years ago, he just happened to pass by a location on his way home and has continued using the same process ever since.

User choice logic is concentrated on both ends: how the remitter initiates the transfer and how the recipient uses the money after receiving it. Virtually no company is making products related to these two key stages.

Felix Pago is a typical example. Last year it handled over $1 billion in transactions and served 300,000 immigrant users, operating entirely through WhatsApp, requiring no app downloads, wallet registration, or complicated entry processes.

Users just need to send a message number, and a chatbot interacts in a local dialect of Spanish; clicking a link completes the payment, and funds arrive directly in a Mexican bank account within 60 seconds. The underlying operations rely on USDC issued on the Stellar blockchain and settled through the Bitso exchange, but users are completely unaware of the existence of crypto assets.

Felix reduced the single transaction fee from $4.98 to $2.99, resulting in higher revenue per transaction post-price drop because stablecoin settlements eliminate the hefty costs of advance payments and the maintenance of large reserves needed by companies like Western Union. The most receptive user groups are millennials and older men who spend all day on WhatsApp. Felix’s key to success lies in rooting itself in the scenarios users are already using, rather than purely building better remittance channels.

More significant product opportunities focus on the receiving end and are unrelated to the remittance business itself. Bybit's six months of field research yielded the core conclusion: Latin American users do not need to use stablecoins for transfers; they need to use stablecoins to hold dollar-denominated assets. The balance itself is the product; trading is merely a secondary action.

Since 2018, the Argentine peso has depreciated by 97% against the dollar, the inflation rate has soared to 211%, and the official monthly foreign exchange purchase limit is restricted to $200. The public can only purchase USDT at a 30% premium through WhatsApp groups, solely to separate their salary savings from the continuously depreciating local currency. Among cryptocurrency purchases in Argentina, 70% is concentrated in stablecoins like USDC and USDT, while Bitcoin accounts for only 8%, with users' primary demand being to preserve the purchasing power of their salaries.

The financial platform Lemon Cash seized this pain point, and within two years, its user base surged from less than 10,000 to 2 million. Its product logic is straightforward: users immediately convert pesos to USDC after receiving their salary, then convert back to pesos when using their Visa bank card for daily purchases. By providing the dollar savings account function absent in local banks, the circulation of stablecoins in Argentina has reached $11 billion, accounting for 27% of the country's narrow money supply M1.

Similarly, in Colombia, banks require a minimum deposit of $5,000 to open a dollar account, which is almost astronomical for ordinary Colombian workers. Stablecoins have become the only channel for Colombians to hold dollars, with 52% of local cryptocurrency purchases flowing into stablecoins. The banking system has kept the masses out of basic dollar wealth management, while stablecoins have filled the gap.

Brazil faces entirely different issues. The Brazilian real's exchange rate is relatively stable, and the public does not need dollars for preservation in the same way that Argentines and Colombians do; the local PIX payment system is projected to reach a transaction volume of $45 trillion by 2024, already being one of the world's top instant payment infrastructures. Brazil's core demand for stablecoins is to provide a more efficient clearing layer for local currency transactions. The stablecoin BRLA, pegged to the real, directly connects to the PIX system, with monthly transactions soaring from zero to $400 million by early 2026. Data from the Brazilian Central Bank shows that 90% of local cryptocurrency trading volume is related to stablecoins.

To summarize, Argentina needs dollar savings, Colombia needs dollar channels, and Brazil needs settlement infrastructure.

Adapting a product to one country and deploying it in the other two is likely to fail; trying to meet the demands of all three will ultimately lead to failure in all areas.

Who Can Truly Win the Latin American Market

Since the industry has generally chosen the wrong track and misaligned products, who can dominate the Latin American remittance market? Frankly, there isn’t yet a player who has run through the ultimate model, but the core factors determining success and failure in the industry are already clear.

Western Union’s market share in the remittance market from the U.S. to Latin America plummeted from 29% to 16.8% within four years, nearly halving. Its response was to spend $500 million to acquire Intermex and hastily launch its own stablecoin, USDP. This established giant had indeed noticed the shifts in the industry, yet it could only follow the trend and imitate, unable to reshape the ecosystem.

During the same period, Remitly, with its superior digital remittance product, increased its market share from 14% to 22.7%. However, it still lacks infrastructure like wallets and debit cards, failing to allow users to retain dollar assets.

Bitso, leveraging stablecoin channels, accounts for 10% of the transaction volume of the entire remittance corridor from the U.S. to Mexico. However, as a crypto exchange, it lacks local payment ecosystem integration and cannot provide a simple experience adapted for regular users like Robert.

The ultimate winner must connect the entire transaction chain, replicating the lightweight remittance experience of Felix Pago based on WhatsApp, while also incorporating savings functionalities like those of Lemon Cash, allowing users to retain dollar balances; simultaneously, it must connect to local payment channels such as SPEI, PIX, and PSE, and provide debit cards for direct consumption and yield-generating balance management. The entire ecosystem must be adaptable for ordinary people using entry-level Android phones who have never used crypto apps.

This requires a complete financial infrastructure, and the only feasible path is a gradual construction.

Regulatory structure is also crucial. The Brazilian Central Bank has introduced three new regulations that classify stablecoin trading as foreign exchange transactions, requiring crypto companies to have a registered capital of at least $2 million to $6.9 million, setting a very high entry barrier; Mexico's 2018 fintech law mandates that businesses dealing in virtual assets must be licensed and obtain prior approval from the Central Bank, with strict license approval processes.

Both Brazil and Mexico are mature markets with very tough entry requirements. In contrast, Colombia and Argentina have lower compliance thresholds and more friendly regulatory sandbox policies, allowing for greater experimentation and iteration of products.

A common industry misconception is to prioritize entry into the largest Brazilian market, but it is precisely the most challenging for entry. A smarter strategy is to first conquer Colombia and Argentina, refining dollar savings and asset entry products, and perfecting the entire operational strategy for integrating debit card infrastructure and local payments; then, replicate the mature model to enter Brazil, maintaining the same foundational infrastructure, only needing to adapt to local currency settlement needs.

A Larger Macroeconomic Context

Last year, the United States passed the "One Big Beautiful Bill Act," imposing a 1% federal tax on cash cross-border remittances. Nearly half of Latin American remitters still operate through offline cash outlets, and in the future, the costs of these traditional channels will rise directly; meanwhile, digital and crypto channels for remittances generally enjoy tax exemptions.

Regular individuals like Robert who insist on using Western Union for cash remittances will have to bear higher costs for their established habits in the future; while digital channels like Felix's WhatsApp remittances and Mexico’s OXXO SPIN Wallet will not require additional taxes.

The average remittance fee in Latin America still hovers around 6%, with some markets like Paraguay nearing 12%, whereas crypto channels can reduce fees to under 2%. For a regular user sending $300 every two weeks, the saved fees could sustain a family’s typical food expenses for nearly a month.

The ultimate race for Latin American remittances essentially revolves around who can win the trust of ordinary people and manage a dollar balance account that supports family living expenses. Whoever controls the balance of users' assets will dominate the Latin American fintech market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。