This year, the global IPO is expected to raise $160 billion, and the competition for the liquidity dividend race has already begun.

Written by: DWF Ventures

Translated by: Saoirse, Foresight News

Key Points:

- The duration of corporate privatization has greatly increased. Since the 1990s, the average period for companies to go public has doubled. The most valuable growth stages remain locked in the private market, prompting ordinary retail investors to seek on-chain Pre-IPO investment channels.

- Currently, the market has generated three structurally different forms of Pre-IPO investment targets: SPV-backed tokens, synthetic perpetual contracts, and closed-end funds. These three types of products differ in their asset-backed endorsements, price anchoring mechanisms, redemption rules, and regulatory attributes, each suitable for investors with different risk preferences.

- Pre-IPO stocks have consistently traded at a premium of 20%-40% compared to the latest round of private market valuations, and most trading platforms lack the short-selling hedging power to correct this premium deviation.

- As institutional and public demand for Pre-IPO assets continues to rise, any platform that can resolve liquidity issues and mitigate the various potential risks mentioned in reports will face huge market opportunities.

The original intention of the public market is quite simple: to create inclusive wealth appreciation tools for the general public. Traditionally, an IPO is an important way for startups to absorb massive social capital, support subsequent development and expansion, and enhance industry visibility. Investors can also use this opportunity to invest in early-stage growth companies and share the returns from the company's long-term development. However, with a large influx of private capital and institutions, quality price discovery opportunities have gradually become restricted to the private market.

This has distorted the free market attributes that stocks should possess, and IPOs have gradually become a liquidity window for institutional investors to cash out. The emergence of the cryptocurrency industry has reshaped the market landscape, with initial token offerings and project tokenization becoming standard configurations for various projects, allowing anyone globally to participate in investment without permission. This concept is no longer limited to crypto-native assets; asset tokenization has become a core application scenario on-chain. Public stocks, commodities, and now the Pre-IPO market are all beginning to migrate on-chain, creating a new price discovery track outside the traditional financial system.

Market Status

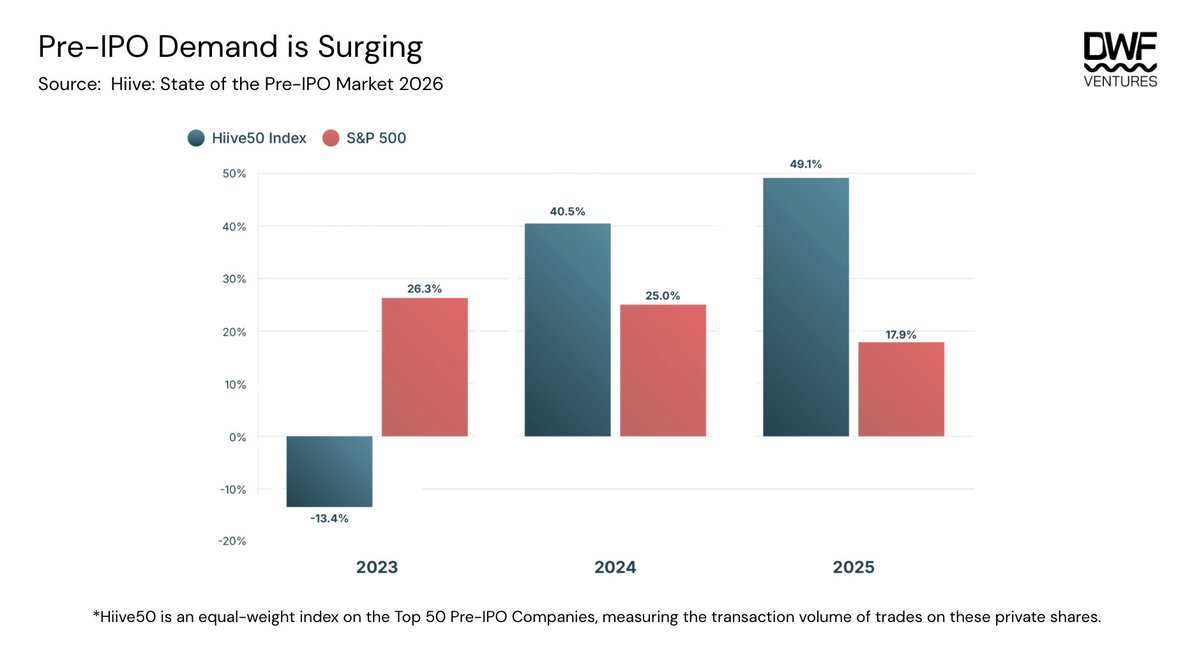

The Pre-IPO market has seen exponential growth, primarily because the cycle from establishment to IPO has significantly lengthened. In the 1990s, companies could complete their listings in an average of 4-5 years, but this cycle has now stretched to 12 years. Leading companies like SpaceX, OpenAI, and Anthropic plan to initiate IPO filings at historically high valuations, leading to unprecedented demand for investment channels in the private market. The private secondary market is booming, with Hiive's report on the "Current Status of the Pre-IPO Market" showing that its Hiive50 secondary market index, which measures yield performance, has surpassed the S&P 500 index.

The Hiive50 index for the Pre-IPO market in 2024-2025 significantly outperforms the S&P 500, reflecting a sharp increase in demand for Pre-IPO assets

Market demand is highly concentrated in three major tracks: cryptocurrency, artificial intelligence, and fintech. From the number of targets, AI companies have the highest representation in the index, while the demand for equity transfer from single cryptocurrency companies is even more robust. The Hiive platform has set a historical high for trading volume, with trading premiums for leading companies soaring to 100%-200%.

By 2025, the average transaction size on the Hiive platform has exceeded $1 million, indicating that the platform primarily serves institutional buyers. Due to regulatory restrictions, the platform is only open to accredited investors, who tend to invest larger amounts and have longer investment timelines. As a result, the demand for Pre-IPO investments from ordinary retail investors has remained unmet, leading to competition in the on-chain track.

Inclusive Price Discovery

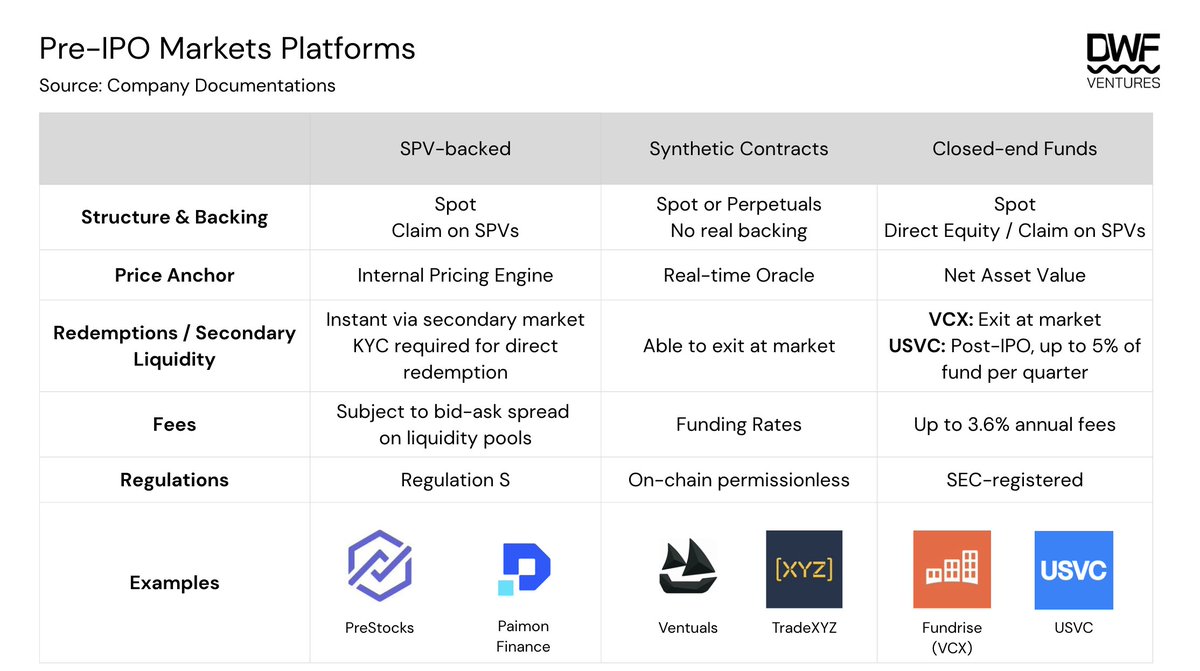

Ordinary investors participating in Pre-IPO investments primarily fall into three categories: SPV-backed, synthetic contracts, and closed-end funds. The three differ significantly in product structure, underlying asset endorsements, pricing logic, redemption mechanisms, transaction fees, and regulatory rules.

The core differences in underlying structure, pricing, liquidity, fees, and regulation of the three mainstream Pre-IPO investment platforms: SPV-backed tokens, synthetic contracts, and closed-end funds, along with representative platforms

Structure and Underlying Asset Backing

Investors can allocate to Pre-IPO assets through the spot market or perpetual contract market, with perpetual contracts currently only offered on-chain. Platforms that provide spot targets typically hold the corresponding Pre-IPO company equity through special purpose entities (SPV) or direct shareholding. Theoretically, such tokens have a price floor, making them more acceptable to investors; once the company completes its IPO, these tokens can be redeemed for USDC or the corresponding company's actual stocks.

On the other hand, the synthetic targets in perpetual contract form rely solely on oracles for real-time pricing and lack any underlying asset endorsements or equity recourse. The underlying structure of closed-end funds like VCX and USVC is even more indirect, with lower transparency. Even if VCX directly holds company equity, the related shareholder rights are not distributed to fund share holders; USVC mainly indirectly allocates to Pre-IPO companies through venture capital funds, leading to multiple layers of transaction paths, ultimately facing serious liquidity issues at redemption.

Price Anchoring Mechanism

The price oracles on various platforms generally combine the latest transaction prices from the off-chain private secondary market with the on-chain supply and demand to form a marked price moving average for integrated pricing. The pricing algorithms and update frequencies across different platforms vary significantly: the PreStocks oracle has no fixed update rhythm, while Ventuals refreshes prices every 3 seconds. For SPV-backed platforms and compliant registered funds, net asset value (NAV) serves as the pricing benchmark; however, due to the influence of total token issuance and market sentiment, transaction prices often reflect premiums relative to net value.

Ventuals has implemented multiple risk control rules to suppress price fluctuations: the marked price, updated every 3 seconds, is restricted to a movement of less than 1% and always locked within the oracle price ±20% range. Its oracle price is composed of off-chain data and the two-hour index moving average of the marked price, coupled with a lack of short-selling liquidity in the market, easily forming a single-sided bullish market, where the marked price gradually reaches the upper limit through a self-feedback mechanism. Currently, the open contract size per asset on the platform is limited to between $5 million and $7.5 million, making it challenging to accommodate large orders; the price discovery function is severely limited. Once the holding size reaches its upper limit, the funding rate will drastically increase, forcing holders to reduce their positions, making it difficult to hold significant positions long-term.

Ventuals has optimized its funding rate mechanism: when the marked price approaches the oracle ±20% price range threshold, the funding rate will climb exponentially to incentivize short sellers and weaken the self-reinforcing effect of a one-sided market, ensuring the stability of the trading ecosystem.

Redemption Mechanism and Secondary Market Liquidity

On-chain platforms can rely on the secondary market to exit at any time, but due to funding pool depth limitations, it is challenging to execute large orders in one go; most exchange transactions will also incur 0.5%-1% slippage costs. VCX, as a New York Stock Exchange-listed fund, possesses comparable liquidity flexibility, allowing investors to sell at market prices on any trading day.

The direct redemption model has strict limitations and higher risks: redeeming USDC through SPV settlement requires waiting for underlying equity to be sold on the private secondary market, a lengthy process without a clear payout timeline. Fund products have even more restraints: USVC has no obligation for mandatory share buybacks; even if buybacks are initiated, the buyback amount per quarter cannot exceed 5% of net assets, and is subject to the platform's discretion. Investors may need to wait for several years for a full exit, and if the fund's net value continues to decline after the company's IPO, the principal returns are not guaranteed.

Transaction Fees

Multi-layered funds may incur compounded management fees: if a parent fund invests through underlying sub-funds, an additional layer of management fee is imposed on top of the original fee, which gradually erodes returns through long-term compounding. After accounting for underlying fund fees, USVC's annual comprehensive fee rate reaches 3.61%, and this fee is not disclosed clearly, making it easy to underestimate actual costs and lower net returns for ordinary investors.

On-chain platforms do not charge fixed management fees, with transaction costs embedded in the buy-sell spread; the actual entry and exit costs depend on transaction size and funding pool liquidity. Ventuals' synthetic contracts charge an additional funding rate with a settlement cycle of every 8 hours, differing from the hourly settlement of mainstream crypto exchanges; the longer settlement cycle reduces the capital cost of holding Pre-IPO positions long-term, suitable for investors waiting for a company's IPO.

Regulatory Rules

SPV-backed platforms primarily apply the U.S. Regulation S securities exemption rules, only open to non-U.S. investors; apart from this restriction, most platforms are globally accessible, with only a few countries facing additional entry restrictions.

Closed-end funds like VCX registered with the U.S. SEC operate under a completely different regulatory framework. As NYSE-listed securities, any investor with a securities account can participate, making this category the most compliant in coverage.

Synthetic perpetual contracts fall under unlicensed on-chain products and are not subject to any financial regulatory constraints.

Other Potential Risks

- Tokenized equity transfer risk: compared to on-chain platforms, funds like USVC face greater risk. OpenAI and Anthropic have publicly condemned unauthorized Pre-IPO token issuances and stated that they will strictly control equity transfer permissions. Fund valuations are highly dependent on the authenticity of the underlying SPV assets; once equity transfers are restricted, risks similar to a bank run may arise, rendering the book value unobtainable.

- Closed-end fund underperformance risk: funds configured as index packages of Pre-IPO assets prevent investors from independently managing single company holdings. If a fund's directional allocation misaligns with actual return tracks, the overall yield may fall far below that of a concentrated portfolio of a single quality target.

- Absence of short-selling mechanisms in the market: this represents a structural shortcoming of the industry. The inability to short spot targets and the dearth of hedging channels for perpetual contracts directly leads to the long-term maintenance of high premiums for Pre-IPO assets. Ventuals is one of the few platforms offering short trading, but the market's inherent scarcity of hedge counterparties means that short liquidity remains weak.

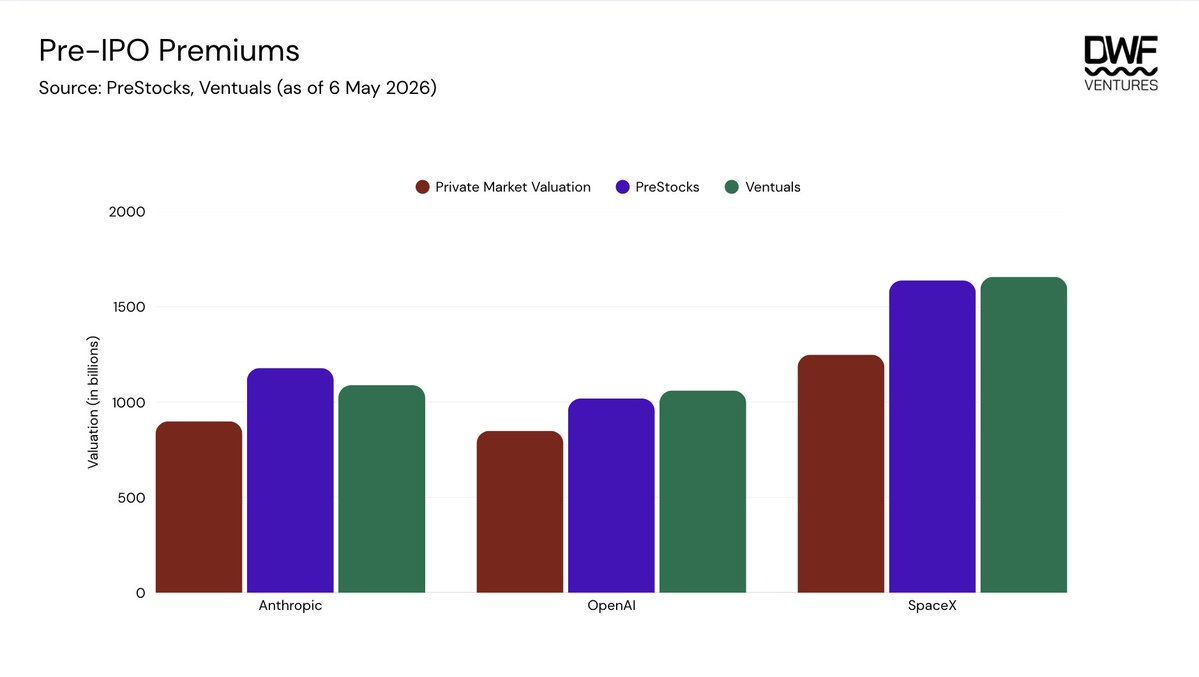

- Uncertainty after a company completes its IPO: Currently, the trading prices for Pre-IPO assets on the PreStocks and Ventuals platforms generally exhibit a premium of 20%-40% over private market valuations. A company's IPO does not necessarily provide immediate liquidity, especially for equity held through SPV structures, which must undergo separate liquidation processes. Historical data shows that average valuation at listing is 25% higher than the fundraising amount, greatly compressing profit margins for investors entering at a premium. For funds, net value depreciation often outpaces the speed of capital returns, leaving investors long exposed to loss risks.

The trading valuations of three popular companies, Anthropic, OpenAI, and SpaceX, on the PreStocks and Ventuals platforms, are significantly higher than their official valuations in the private market, showing a clear Pre-IPO premium

New Entrants in the Industry

The scale of the Pre-IPO market continues to expand, and industry competition is becoming increasingly fierce. Leading exchanges like Binance and Bitget have listed Pre-IPO tokenized targets by connecting with PreStocks or through self-developed synthetic contracts. On-chain native platforms are also accelerating their layout, with TradeXYZ recently launching Perpetual Contracts for Pre-IPO, achieving a trading volume of $7 million on the first day, with current trading prices reflecting a premium of about 90% compared to expected IPO valuations, corresponding to a stock price of about $160 per share.

New business models are constantly emerging: Backpack, in collaboration with Superstate and the Solana blockchain, has launched compliant on-chain IPOs, with issued shares possessing legitimate security attributes, allowing investors to directly enjoy the benefits of actual equity. Traditional IPO resources have long been monopolized by institutions and accredited investors, and the realization of compliant on-chain IPOs will open a new investment gateway for ordinary retail investors.

Value Flow and Future Outlook

The wave of asset tokenization will only intensify: the longer the corporate privatization cycle, the higher the market demand for Pre-IPO asset allocations. This investment demand is no longer limited to retail levels; governments, large institutions, and professional funds worldwide are vying to get in on the action. For example, the South Korean government recently launched a National Growth Fund open to public participation, focusing on investments in the local AI and semiconductor emerging industries. This year, the global IPO is expected to raise $160 billion, and the competition for this liquidity dividend race has already begun.

New players continuously entering the market confirm the genuine demand for Pre-IPO assets, but questions remain regarding product structure, compliance, and long-term sustainability; the industry has not yet undergone a true extreme scenario stress test. In the short term, platforms that can resolve liquidity pain points will seize market opportunities; in the long run, the ability to adapt to regulatory compliance will be the core barrier. The U.S. SEC and the Commodity Futures Trading Commission have released significant reports on regulatory applicability to digital asset securities, and many SPV-packaged Pre-IPO tokens may face regulatory scrutiny and enforcement adjustments after the underlying companies go public. In the future, only platforms that balance liquidity, product structure, and compliance requirements can carve out a share in this blue ocean market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。