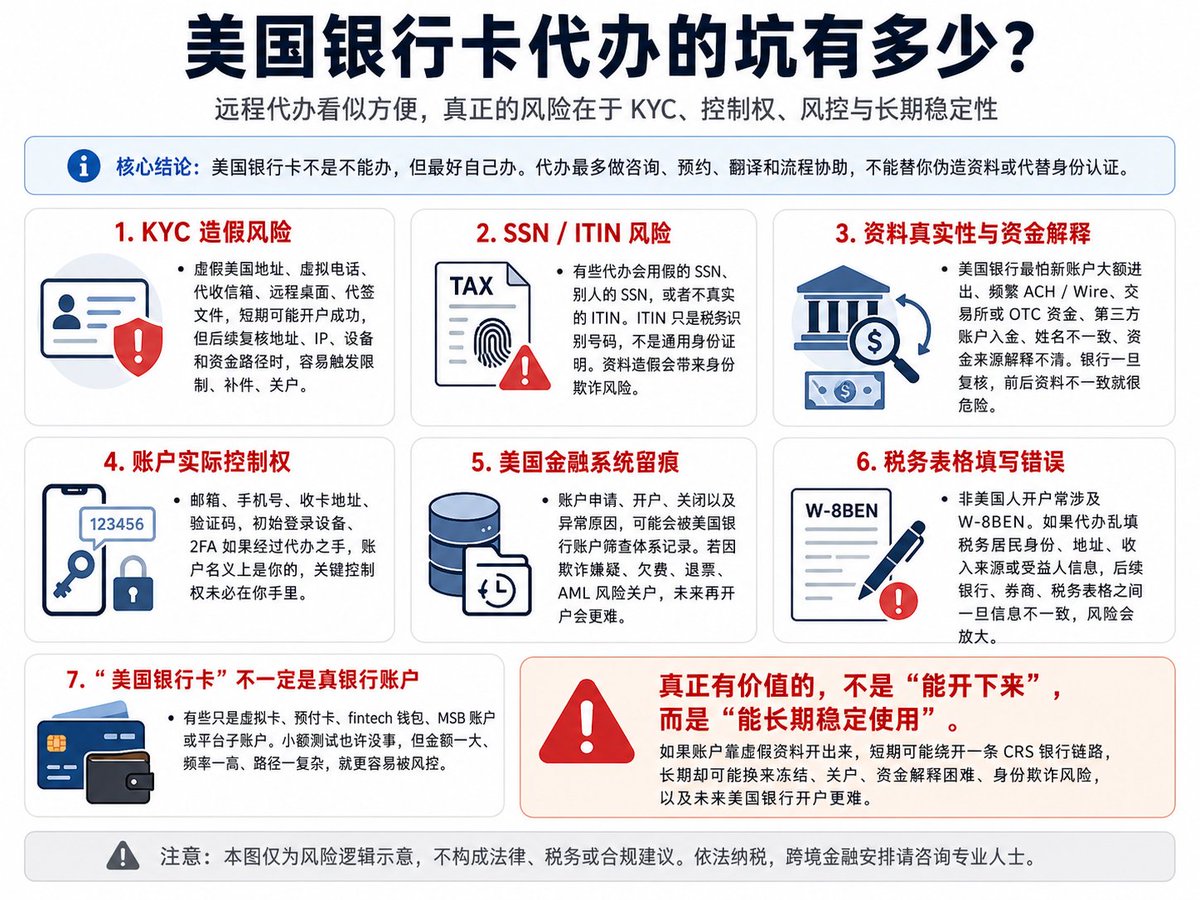

How many pitfalls are there in the agency for American bank cards?

In a previous tweet about CRS, I mentioned that even with American brokers, if it’s not an American bank card, it may still be counted by CRS due to bank and bank card transfers. Then some friends privately messaged me asking if there are many agencies for American bank cards now, can they be used?

From my personal perspective, American bank cards are not difficult to obtain, but most need to be applied for in the U.S., and only a few can be opened online, such as Velo, which comes with quite a few restrictions, and almost all "remote agency American bank cards" have pitfalls, and there are quite a few.

First, KYC fraud.

American banks have their own BSA, AML, and KYC systems. FinCEN's customer due diligence rules require financial institutions to identify and verify customer identities, understand the purposes of account relationships, and continuously monitor suspicious transactions.

Many agencies will use fake American addresses, virtual phones, mail forwarding addresses, remote desktops, and signed documents. This may not be an issue for opening accounts, but in the long run, if the bank reviews addresses, IPs, login devices, sources of funds, and payment paths, it could limit accounts, require additional documentation, close accounts, or even list them as high-risk customers.

Second, the risks of SSN and ITIN.

Some agencies claim to help obtain ITINs or open accounts using American identity information. However, in reality, an ITIN is a tax identification number for individuals who are not eligible for an SSN but require it for federal tax purposes; it does not provide immigration status or work authorization, nor is it a standard form of identification.

If an agency opens an account using a fake SSN, someone else’s SSN, or a false ITIN, it results in identity fraud risk, and this goes beyond just account closure issues.

Third, the authenticity of American bank card information.

What American banks fear the most is high amounts being deposited or withdrawn right after the account is opened, frequent ACH or wire transfers, money from exchanges, OTCs, third-party accounts, or accounts with inconsistent names, or unclear sources of funds.

If the bank requires an explanation of the source of funds, what’s needed is a complete trail. Where the money comes from, why it entered the U.S. account, whether it matches the account owner, whether there are transaction records, whether there are tax documents, whether there is proof of legitimate income.

If the information is genuine and the source of funds can be explained, there isn't much of an issue. However, if the account was opened using a fake address, virtual phone, or signed documents by an agency, then the bank will find inconsistencies upon review.

Fourth, the issue of actual control over the account.

Many agencies claim to help with account opening, but in reality, the email, phone number, card receiving address, verification methods, initial login devices, and even 2FA might be controlled by the agency. In other words, the account may be nominally yours, but the key control may not be entirely in your hands.

Especially since American bank cards generally involve debit cards, online banking, SMS verification, email verification, and address verification, if these things are controlled by the agency initially, then in the future, if a dispute arises, it will be hard to prove that you are the sole actual controller.

The most important thing is that the impact of agency cards is recorded in the American financial system. The U.S. has bank account screening systems similar to ChexSystems, which record the applications, openings, closings, and reasons for closing checking accounts.

If an account is closed due to unusual usage, fraud suspicion, overdue payments, bounced checks, or AML risk, it may become even harder to open another American bank account in the future.

Sixth, the issue of tax forms.

Non-Americans opening accounts with U.S. brokers or some American financial institutions usually involve the W-8BEN form to prove they are not U.S. tax residents. If the agency incorrectly fills in the tax residency status, address, income source, or beneficiary information, it may lead to incorrect tax identity reporting.

What’s even more troublesome is that some people, for the convenience of opening accounts, may be guided by the agency to fill in American addresses, American phone numbers, American identity information, ultimately packaging themselves as if they are U.S. tax residents, leading to inconsistencies between banks, brokers, the IRS, and tax forms, resulting in greater risks.

Seventh, it’s important to clarify what American bank cards really are.

Many agencies sell “American bank cards,” but what they actually provide may just be virtual cards, prepaid cards, fintech wallets, MSB accounts, or even sub-accounts of certain platforms. They may be able to receive money, transfer money, and make purchases, but it does not equate to having a stable, compliant, and long-term capable American bank account.

The biggest problem with such accounts is that using small amounts may be fine, but once the amounts get larger, the frequency increases, and the paths become complex, they are easily flagged by risk control. Moreover, once frozen, when it comes to explaining the source of funds, identity information, and account opening information, you may not even know who is really reviewing you.

So my personal opinion is simple: it is best to handle American banking personally, using real identity, real address, real contact information, with control over the email, phone, online banking, card receiving address, and 2FA.

Agencies can at most provide consultation, appointment scheduling, translation, and process guidance; they cannot complete identity verification for you, nor can they sign documents, create addresses, create phone numbers, create SSNs, or create ITINs for you.

If an American account is opened with fake information, it actually carries even greater risks.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。