The rise of the East and the decline of the West may not necessarily be just a relocation of market value, but it is likely an opportunity for the layout of compliance dividends.

Written by: Chloe, ChainCatcher

While the eyes of the world are focused on the United States promoting the Clarity Act, a new wave of capital and market layout is quietly surging in the Asia-Pacific (APAC) region.

The Asia-Pacific region accounts for 60% of the world's population and features a youthful demographic, a high smartphone penetration, along with fears of fiat currency inflation, making it the most fertile ground for cryptocurrency. Japan is seen as stable and compliant, South Korea as a speculative casino, and Singapore as an institutional safe haven. The current Asia-Pacific cryptocurrency landscape may be experiencing a rise in the East and a decline in the West.

Macroeconomic Data: Why is the Asia-Pacific the World Center?

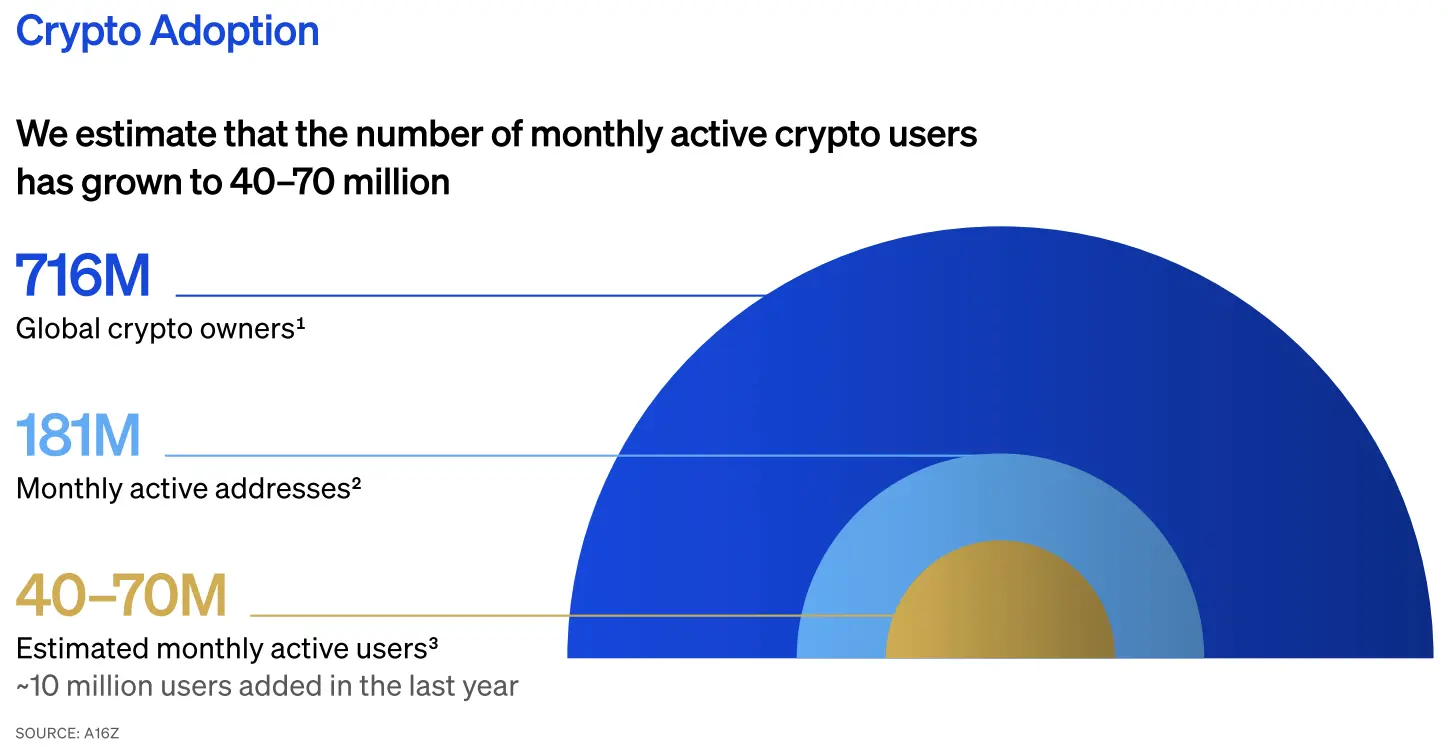

According to Bitgo's latest report for 2026, the number of cryptocurrency owners worldwide will exceed 700 million, with the number of active users in the cryptocurrency space estimated to be between 40 million and 70 million each month. This represents an increase of about 10 million from last year.

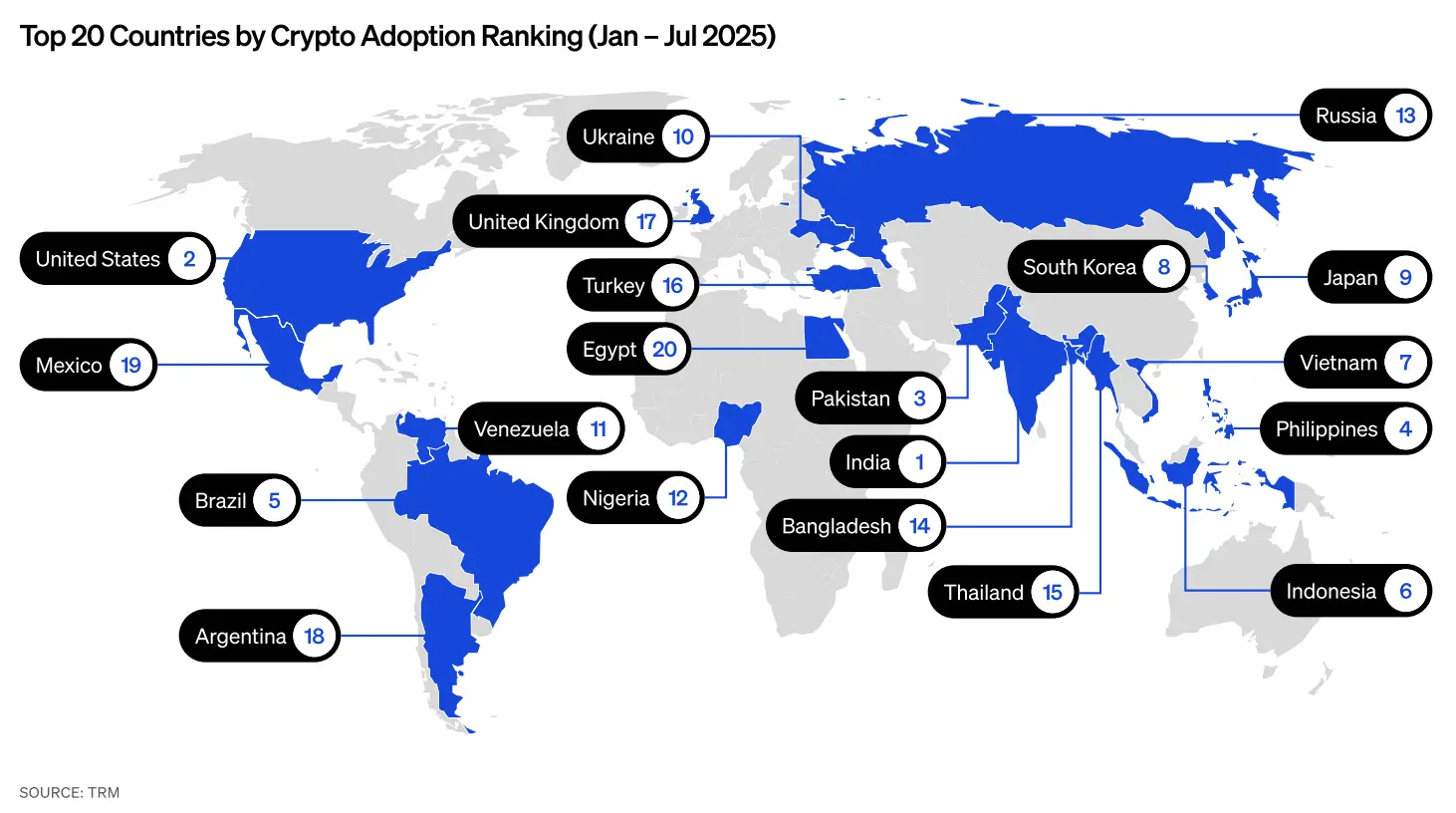

In the ranking of the top ten countries adopting cryptocurrencies, seven of the top ten are located in the Asia-Pacific region, indicating the potential and development of cryptocurrency in this area, whether in terms of user volume or actual usage.

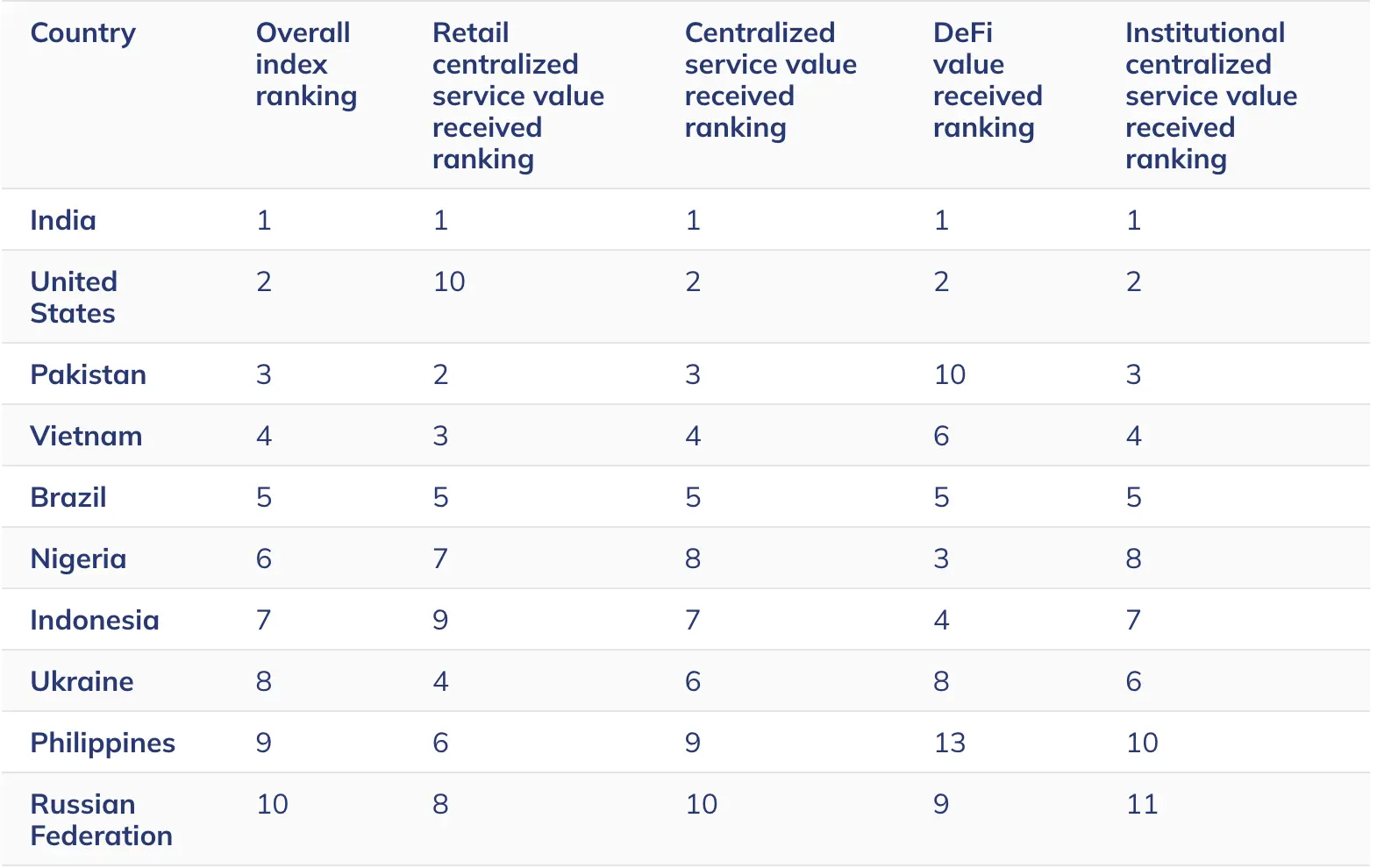

Moreover, according to Chainalysis' "2025 Global Cryptocurrency Adoption Index," India ranks first, followed by the United States, Pakistan, Vietnam, and Brazil, with five of the top ten being from the Asia-Pacific: India, Pakistan, Vietnam, Indonesia, and the Philippines.

In terms of momentum growth, from the end of June 2025 over the previous 12 months, the on-chain transaction volume in the Asia-Pacific region skyrocketed from $1.4 trillion to $2.36 trillion, a year-on-year increase of 69%, making it the fastest-growing region globally, compared to just a 27% growth rate the previous year, essentially doubling in speed within a year.

In other words, while North America relies on ETFs and institutional entries to drive "compliance-based" growth, the Asia-Pacific relies on real retail trading, cross-border remittances, and stablecoin demand to drive "usage-based" growth.

The nature of these two growth curves is distinctly different; the former is about the movement of existing capital, and the latter is about the influx of new users.

Vietnam: A National Team Experiment from Grey Markets to Closed Platforms

Over the past decade, Vietnam has been one of the markets with the highest cryptocurrency adoption rates in the world, yet also the most unregulated. According to Chainalysis data, Vietnam's global cryptocurrency adoption rate was ranked first for two consecutive years in 2021 and 2022, with over 20% (around 17 million people) of the Vietnamese population holding digital assets.

However, this vast market has been operating long outside legal frameworks, with the public engaging in P2P trading on overseas exchanges like Binance and OKX, making it impossible for the state to impose taxes or combat money laundering.

This situation began to change in the second half of 2025. On June 14, 2025, the Vietnamese National Assembly passed the "Digital Technology Industry Law," making Vietnam the first country in the world to establish specific laws for the digital technology industry, with the law officially taking effect on January 1, 2026.

The law distinguishes digital assets for the first time at a legal level into two categories: "virtual assets" and "cryptographic assets," requiring that activities involving cryptographic assets must comply with cybersecurity and anti-money laundering regulations.

Shortly after, on September 9, the Vietnamese government issued Resolution 05/2025/NQ-CP, initiating a five-year pilot for cryptocurrency trading. However, the thresholds for this pilot are extremely high: the minimum registered capital for companies must be 100 trillion Vietnamese Dong, three times that of the minimum registered capital for commercial banks, and all issuance, trading, and settlement of cryptocurrency must be conducted using the Vietnamese Dong; shareholders must have been profitable for two consecutive years before applying.

The core logic of this system is a closed platform: opening up while locking all risks and funds domestically. Domestic players such as TCEX under Techcombank, VIXEX under VIX Securities, and DNEX under HVA Group are already queuing up to apply for licenses. The parent company of South Korea's largest exchange, Upbit, has also signed an MOU with MB Bank, which falls under the Vietnamese Ministry of Defense, to export the South Korean exchange model and technology to create the country's first national-level digital asset exchange.

In March 2026, the market experienced a policy shift when the Vietnamese Ministry of Finance indicated in an internal document that authorities plan to prohibit citizens from trading digital assets on overseas platforms like Binance and OKX and require all activities to be directed towards an officially regulated domestic system.

This is not without reason; it may be part of a national initiative with a clear timetable. According to recent reports, a Deputy Minister of Finance in Vietnam stated that the country could officially launch its cryptocurrency market in the third quarter of 2026.

In other words, from legislation to pilot programs to platform launches, Vietnam has given the market less than 18 months of transition time.

This closed system is considered imperative due to remarkable pressure from capital outflows. As of June 2025, the amount of digital assets flowing within Vietnam has surpassed $200 billion, with authorities believing that uncontrolled cryptocurrency and stablecoin trading have become major conduits for capital outflows.

Supporting measures are equally stringent: individual investors trading through licensed platforms must pay a 0.1% income tax, while institutional profits face a 20% corporate tax, and accounting standards require exchanges to completely separate customer assets from proprietary assets.

In short, Vietnam's strategy is to impose the strictest compliance thresholds to "nationalize" the world's fourth-largest cryptocurrency market from Binance. A market with an annual trading volume exceeding $800 billion and over twenty million users is moving towards centralized regulation.

For local financial groups such as Techcombank and VPBank, this is a license dividend, but for international exchanges that have long viewed Vietnam as a vital incremental market in Southeast Asia, this may be the largest regional retreat since China's 2017 prohibition.

Taiwan Relies on the Competitiveness of Compliant Operators

If Vietnam represents the "rise," then Taiwan is another epitome of the compliance process in the Asia-Pacific, but with a rhythm distinctly different from that of Vietnam. Taiwan is taking a traditional financial route of "gradual regulation."

Four-Stage Regulatory Path: From Anti-Money Laundering to Specialized Legislation

According to Taiwan's regulatory planning, the regulation of the virtual currency industry is divided into four major stages: the first stage is the release of the VASP anti-money laundering measures, the second stage is the establishment of an industry association, the third stage is to add VASP registration system to the Anti-Money Laundering Act, and the fourth stage is to promote the enactment of specialized laws. So far, the first three stages have been established, and the fourth stage is entering deliberation.

VASP Registration System Takes Effect, Entering the Era of Enhanced Regulation

On November 30, 2024, Article 6 of the Anti-Money Laundering Law was amended and implemented, officially transitioning VASP from a "declaration system" to a "registration system." Those who do not complete the anti-money laundering registration are prohibited from providing virtual asset services, with violations subject to up to two years of imprisonment and a fine of up to 5 million New Taiwan dollars.

The deadline for existing operators to complete the registration is by the end of September 2025. In the end, a total of eight operators have completed anti-money laundering registration, which includes local exchanges such as MaiCoin/MAX, BitoPro, XREX, HOYA BIT, TWEX, Chainss, KryptoGO, and Zone Wallet.

On March 25, 2025, Taiwanese regulators officially previewed the draft of the "Virtual Asset Service Act." According to the contents of the draft, those who issue stablecoins without permission could face imprisonment of up to seven years and a fine of up to 100 million New Taiwan dollars; if involved in market manipulation or fraudulent practices, the penalties are even harsher, with imprisonment of three to ten years, and fines of up to 200 million New Taiwan dollars.

It can be said that once Taiwan's Virtual Asset Special Law is enacted, it will take a "highly regulated" approach similar to that of financial institutions, setting strict standards on operators' capital, internal audit, and financial structures.

Prioritize Financial Institutions, No Delisting of Overseas Apps

Additionally, two key designs in the Taiwan model are worth contrasting with Vietnam.

The first is the "priority of financial institutions" principle concerning the issuance of stablecoins, which means that while the issuance of stablecoins is not restricted to banks, it is mainly led by financial institutions or businesses with significant capital and risk control capabilities in the initial phase. Furthermore, issuers must issue and redeem stablecoins according to their face value and cannot refuse redemption requests from holders, nor can they provide interest or returns on the issued stablecoins.

This framework is essentially a mix of MiCA and Japan's "Payment Services Act," indicating that stablecoins in New Taiwan Dollars will be dominated by banks rather than crypto-native teams.

The second is the "no delisting" stance towards overseas exchanges. While the draft law references regulations from various regions, it still retains Taiwan's own space for adjustment, particularly regarding issues like delisting overseas platform apps, which have ultimately not been included in the draft due to considerations of user voluntary usage and technical operations.

This contrasts sharply with Vietnam. Vietnam has opted for crypto-nationalism, whereas Taiwan has chosen to "strengthen domestic operations while preserving overseas ones." The former relies on national execution, while the latter depends on the competitiveness of compliant operators.

On the other hand, statistics show that between 2023 and 2025, 17 VASP operators in Taiwan have been found to have deficiencies, and as of now, fines have been imposed on 11 operators, accumulating to over 13 million. In other words, the eight operators that can surpass the compliance threshold and have completed registration will enjoy a relatively closed license dividend in the next 3 to 5 years, but they will also bear compliance costs several times higher than before.

The Differentiated Chess Game in the Asia-Pacific: Japan and South Korea Go Their Own Ways

Vietnam and Taiwan are just two extreme samples; the entire Asia-Pacific region is actually playing out a differentiated regulatory chess game.

South Korea: The Invisible King of Stablecoin Trading Pools

South Korea continues its "speculative casino" identity. The "Virtual Asset User Protection Act," which will take effect in 2024, is reshaping the activities of large domestic exchanges, with the amount of KRW used to buy stablecoins reaching $64 billion over the 12 months ending June 2025, indicating a strong demand from traders for liquidity, hedging, and rapid asset rotation.

Local exchanges like Upbit and Bithumb still dominate the world's deepest KRW stablecoin trading pool, and the next step being discussed in Seoul is to establish a regulatory framework for KRW-pegged stablecoins.

Japan: Tax Reforms Loosen, The Cryptocurrency Market Awakens After Years of Slumber

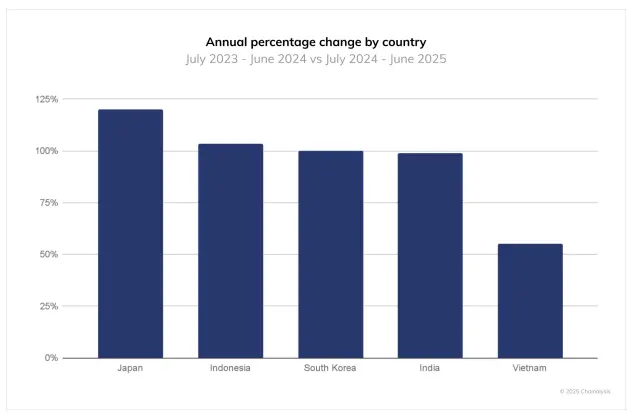

Japan plays a role of robust compliance, but from 2025, there is a structural loosening. According to the "2025 Cryptocurrency Geographic Report," Japan has the strongest growth among the top five markets in the Asia-Pacific, with on-chain transaction amounts growing by 120% year-on-year during the 12 months ending June 2025, surpassing Indonesia (103%), South Korea (100%), India (99%), and Vietnam (55%), backed by tax reforms and the issuance of the first license for a stablecoin issuer in yen.

Japan has long been seen as the ceiling of compliance in the Asia-Pacific, and this rebound indicates that excessive regulation is being moderately loosened.

Singapore and Hong Kong: The Tale of Two Safeguard Cities for Institutions

Singapore and Hong Kong continue to play the role of "institutional safe havens," with the former attracting institutions with the MAS licensing system, while the latter reshapes its role as an offshore financial center through the SFC's virtual asset service provider licensing system and the listing of spot ETFs.

Additionally, last month, the Hong Kong Monetary Authority officially issued the first two stablecoin issuer licenses to Anchor Financial Technologies Ltd. and HSBC Hong Kong, marking an important step for Hong Kong in virtual asset regulation.

According to an analysis by the Fudan Financial Review, the issuance of the first stablecoin licenses in Hong Kong aims to redefine the position of stablecoins in Hong Kong's financial system. They are transitioning from auxiliary tools for cryptocurrency trading to the underlying infrastructure for cross-border payments, local payments, tokenized asset trading, and programmable finance.

"The first licensed institutions also hint at this signal. Anchor Financial Technologies is backed by Standard Chartered Hong Kong, Hong Kong Telecom, and Animoca Brands, and HSBC is also among the first licensed institutions. This means that Hong Kong's stablecoin pilot is not just about the compliance of crypto-native projects, but also an institutional integration of banking credit, payment gateways, and on-chain capabilities."

Conclusion: Compliance Premium is Being Redefined in the Asia-Pacific

Today, while the United States discusses the Clarity Act, what is being discussed in the Asia-Pacific?

The Asia-Pacific is discussing how to convert the "usage dividends" accumulated over the past decade into "institutional dividends." Vietnam is using a national team to claim territory, Taiwan is upgrading through specialized laws, South Korea is reshaping trading behaviors with user protection laws, and Japan is loosening regulations to prompt institutional entry. Each region has its own path, but the direction is consistent: to structure gray areas, institutionalize retail activities, and make capital flow traceable.

For global exchanges, this means a dimension of competition that did not exist before is emerging: the value of regional compliance licenses may be more important than global brands. The same compliance license transferred to Vietnam or Taiwan could be the only pass to enter a market with ten million users.

In other words, the next wave of excess premium in the crypto industry is no longer the "extra-legal dividend," but rather "compliance scarcity," and this scarcity is currently accumulating in the Asia-Pacific; the rise of the East and the decline of the West may not just be a relocation of market value, but probably an opportunity for the layout of compliance dividends.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。