Our new report "How Far Can Saylor Stretch It" is now live!

STRC has become the center of Strategy’s BTC accumulation model.

The question now is whether each new raise can still add BTC per share after accounting for the common issuance needed to service the preferred stack.

Strategy’s earlier BTC purchases were powered by a wide equity premium. MSTR traded far above the value of its BTC holdings which made new share issuance accretive.

At ~1.24x EV-based mNAV, that math is weaker. Common issuance sits close to the breakeven line and no longer gives Strategy the same clean path to BTC/share growth.

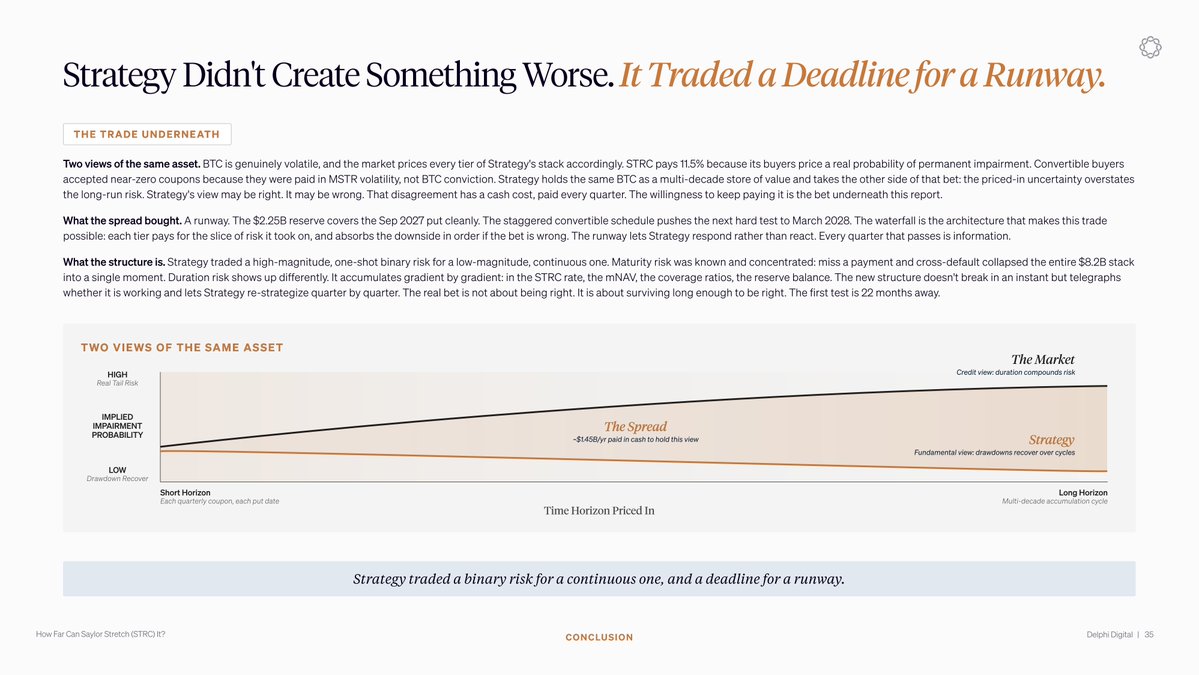

Convertibles were useful because buyers accepted low coupons for MSTR volatility. They also left behind $8.2B of principal and a repayment schedule that starts to matter in September 2027.

STRC now carries more of the load. It gives Strategy access to yield buyers underwriting an 11.5% annual dividend paid monthly, rather than MSTR equity upside. The proceeds can keep flowing into BTC without adding another convert maturity.

The tradeoff is the recurring claim STRC creates. Each raise adds Bitcoin today and another dividend obligation tomorrow. If BTC rises and MSTR’s premium holds, the structure can absorb that cost. If BTC chops sideways, the obligation stack grows while common issuance becomes less efficient.

The stress case is whether STRC-funded BTC purchases can keep outrunning the common issuance needed to service the preferred stack. Strategy’s $2.25B dollar reserve can handle the ~$1B September 2027 put. This buys time but the larger 2028 wall still needs an answer.

The next boundary is the $28.3B STRC authorization cap. Before the cap, STRC can keep adding BTC and offsetting dividend-related dilution.

Without an extension to STRC issuance capacity, reaching the cap means the BTC-buying offset can slow or stop while the dividend obligation remains.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。