The exchanges are beginning to directly confront the structural issues within the cryptocurrency market.

Written by: Eric, Foresight News

DaiDai, Maitong MSX

On May 7, local time in the United States, Coinbase announced its first quarter financial report. The revenue, which fell 30% year-on-year and over 20% quarter-on-quarter, along with a net loss of nearly $400 million, caused Coinbase's stock price to drop nearly 5% in after-hours trading. Although excluding factors such as impairment of self-held crypto assets, Coinbase's EBITDA for the last quarter was recorded at $303.3 million, but it still represented a significant decline compared to the $929.9 million during the same period last year.

The good news is that Coinbase's overall market share has increased to 8.8%, and the growth of new products like derivatives and prediction markets is rapid. The bad news is that this growth does not mask the existing fatigue within Coinbase.

Coinbase has set 2026 as the execution year for its "Everything Exchange" strategy, hoping to transform from a simple cryptocurrency exchange into a "full-stack financial infrastructure". From the first quarter financial report, the cost of this transformation is already apparent, but the outcome remains unclear.

Behind the dense numbers in the report, we read about Coinbase's current predicament.

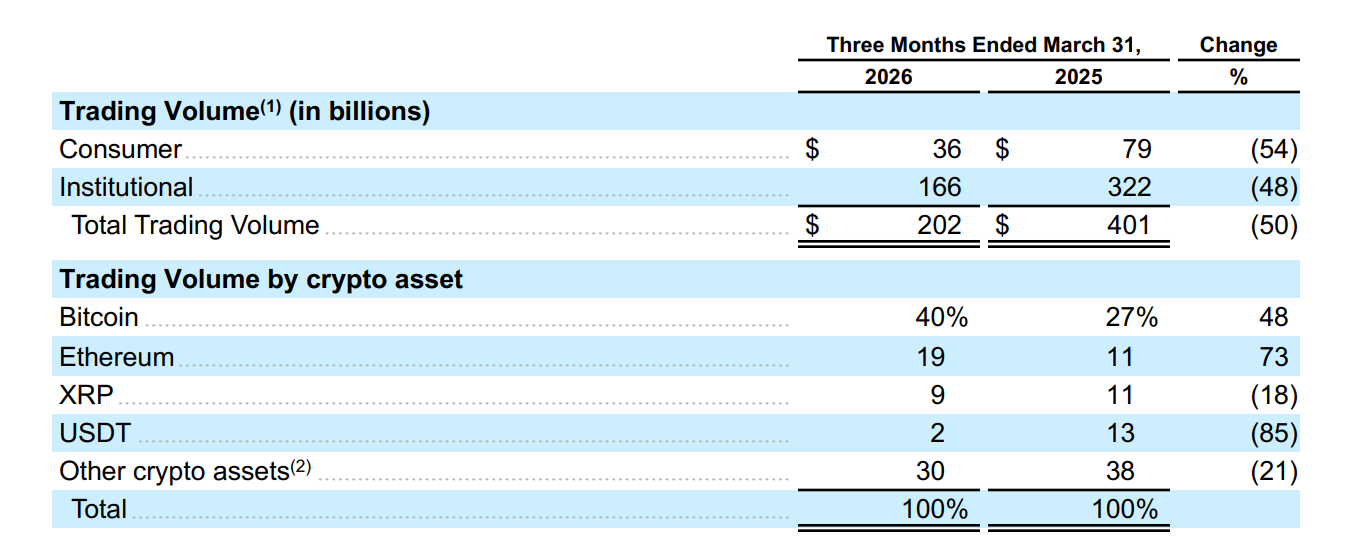

First Aspect: Trading Volume

In the first quarter of 2026, Coinbase's total cryptocurrency trading volume was approximately $202 billion, a decline of nearly 50% compared to $393 billion in Q1 2025, and a quarter-on-quarter drop of about 25%.

The worst performance for Coinbase this season was not the institutional trading volume, but the retail trading volume.

Q1 retail trading revenue for Coinbase fell from $1.096 billion in the same period last year to $567 million, a 48% year-on-year decline; retail trading volume dropped from $79 billion to $36 billion, a 54% year-on-year decline. The company also specifically noted that changes in retail trading volume have a greater impact on trading revenue because consumer rates are higher than those of institutions; within the retail sector, Advanced user rates are lower than Simple user rates.

Of course, the decline in trading volume is not a problem unique to Coinbase. Next door, Robinhood also saw its cryptocurrency trading volume decline by 48% year-on-year and 29% quarter-on-quarter in the first quarter. Even including Bitstamp, Robinhood's nominal cryptocurrency trading volume of $66 billion in Q1 also decreased by about 20% quarter-on-quarter.

In terms of decline ratio, the trading enthusiasm among users in the first three months of this year indeed decreased significantly compared to the same period last year and the end of last year, but trading volume is not the only dimension to assess the platform's capabilities and predict future conditions; user activity remains important.

Maitong MSX US stock analyst DaDai stated, "Coinbase's biggest problem is retaining users. Robinhood can retain users through stocks, options, etc., even if they don't trade crypto." Data also supports this assertion, showing that Coinbase had approximately 8.2 million active users in Q1, a decline of 15.5% from 9.5 million during the same period in 2025.

In contrast, Robinhood's active user count in Q1 2026 was 13.5 million, which was only a decrease of about 6% from 14.4 million during the same period in 2025, and it increased by about 4% quarter-on-quarter. Meanwhile, the commonly used metric by Robinhood, "the number of users with funds in their accounts," was 27.4 million, a year-on-year increase of 6%. At the same time, the largest spot Bitcoin ETF in the world, the IBIT issued by BlackRock, saw an average daily trading volume of about $3 billion in Q1 2026, a quarter-on-quarter increase of 7%.

What Coinbase fears is not that Robinhood will take away professional traders, but that it will take away these types of users:

"I just want to buy some BTC/ETH, I don’t want to study wallets, chains, gas, order books, nor do I want to open a dedicated account at a crypto exchange."

These types of users are crucial for Coinbase because they often use Simple Buy, which has a higher fee and better profit margin. Coinbase also stated in its report that institutional user rates are lower than retail, and within retail, Advanced user rates are lower than Simple user rates; thus, any migration of user structure away from Simple to Advanced or external platforms will suppress trading revenue.

The present issue confronting Coinbase is very tricky: altcoins have long since gone quiet, and the trading of Bitcoin, Ethereum, and some high-market-cap altcoins is facing fierce competition from other cryptocurrency exchanges, brokerages, and traditional financial giants. Purchasing Bitcoin and Ethereum on Coinbase offers no advantages in terms of trading fees or taxable complexity compared to other options where users can freely deposit and withdraw, which may lead to increasing pressures on Coinbase regarding spot trading in the future.

Second Aspect: Stablecoins

As a "ballast" in all of Coinbase's businesses, the stability of Coinbase's collaboration with Circle in the stablecoin sector has always been a sword of Damocles.

In the first quarter, Coinbase recorded $305 million in revenue from its stablecoin business, representing a year-on-year growth of 11.4% and a slight quarter-on-quarter decrease of 1%. Not only did its share in subscription and service revenue increase from 41% to 52%, but its share of total revenue also increased from 13.5% a year ago to 21.6%, becoming the only major revenue category that experienced year-on-year growth last quarter.

In Q1, the USDC balance on and off the Coinbase platform grew, excluding the portion reduced due to interest rate declines, resulting in an income increase of $31 million. However, after deducting the $13 million increase in marketing expenses year-on-year, the net income growth contributed by USDC was only $18 million, which marks the eighth consecutive quarter where Coinbase's USDC rewards growth outpaces income growth. This indicates that the decline in interest rates and the increase in marketing expenses are eroding Coinbase's profitability on this golden egg.

For a long time, the genuine use case for stablecoins has been very limited, with Circle relying heavily on Coinbase's traffic to ensure USDC's usage volume. However, as stablecoins have become a hot topic globally, the situation is undergoing subtle changes.

Since the end of 2025, many of Circle's actions have been interpreted as attempts to regain control, including launching its own public chain Arc, and establishing an independent payment network Circle Payments Network (CPN). In December 2025, Circle received conditional approval for a national trust bank license from the OCC, allowing it to directly open a master account with the Federal Reserve for minting and redeeming, no longer relying on Coinbase as a fiat channel.

Coinbase's CFO stated in the earnings call that the USDC distribution contract with Circle will automatically renew every three years and will continue indefinitely. However, still, how this contract will be signed and whether the profit-sharing ratio will change remains uncertain. Facing the pressure from the leading player Tether and numerous emerging stablecoins, Coinbase's meal, which is held in others' hands, is not as appealing as it seems.

Third Aspect: High Costs

In the first quarter, Coinbase's total revenue was approximately $1.413 billion, a decline of over 30% compared to $2.034 billion in the same period of 2025, yet operational costs rose by 8%. Excluding investment income and other factors, this marks the first time since Q4 2023 that Coinbase experienced losses in its main business.

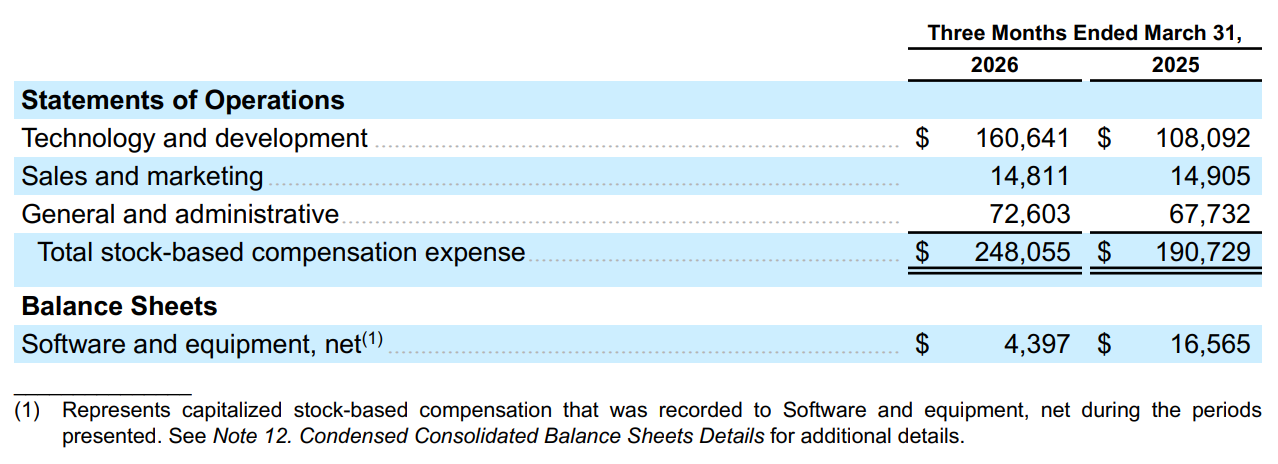

R&D expenses have become the largest drag on performance, and the core reason for this issue lies in Coinbase's acquisitions of Deribit and Echo. Coinbase's acquisition of Deribit for $4.295 billion generated $1.39 billion in intangible assets, which need to be amortized over several years, with an amortization of as much as $35.6 million in Q1 this year alone. This alone could continuously drag down profits in the future.

Aside from this "objective factor" of acquisitions, Q1 saw a 23% year-on-year increase in Coinbase's staff count, reaching 5,500 employees, while the stock-based compensation for employees also grew by 30% year-on-year to $248 million. As a result, while incentives were generously distributed, the per capita output plummeted by 43.5% from $454,000 a year ago to $257,000.

Thus, Coinbase's layoffs are not without reason. While publicly citing AI as a reason, it is essentially aimed at cutting costs. Coinbase states that this round of layoffs could incur a one-time cost of $50 million to $60 million, but is expected to save $500 million in annual operational costs. Management indicated in the Q2 guidance that the technology + management expenses for the second quarter are expected to be between $820 million and $870 million, down from $902 million in Q1; marketing expenses might remain flat or slightly decrease compared to Q1.

From the stark contrast between the sharp decline in revenue and rising costs, we can also faintly see the issues mentioned in the first part. Coinbase has been attempting to broaden its revenue sources as much as possible, from introducing options products with the acquisition of Deribit to various other derivatives and prediction markets. However, the trading volume and income brought in by these new products currently still lag significantly behind the spot market, while the increased costs are visibly manifested.

DaiDai remarked, "The key to whether Coinbase can emerge from this predicament lies in the future performance of its derivatives." Coinbase is already supplementing its offerings in derivatives, prediction markets, DEX, Base, and other new businesses. It refers to its direction as Everything Exchange, no longer relying solely on spot trading.

In the long run, Coinbase is moving towards "crypto financial infrastructure"; in the short term, it is still a company reliant on trading cycles.

Fourth Aspect: Cyclicality

Unlike Circle, Coinbase is still affected by the cyclicality of the cryptocurrency market itself.

The price trends of Coinbase's stock since its listing clearly show a strong correlation between its stock price and the trends in the cryptocurrency market. To this day, aside from stablecoin revenues, trading, subscription, and service revenues are all affected by market dynamics. Coinbase has introduced a series of derivatives, including tokenized stocks, bulk assets, and prediction markets.

My impression is that Coinbase has "spread itself too thin" on the battlefield. Cryptocurrency, tokenized assets, derivatives, prediction markets—aside from having a considerable advantage in the options market, other areas are continually being squeezed. As previously mentioned, the trading of cryptocurrencies is being encroached upon by traditional financial giants and brokerages like Robinhood, derivatives struggle to compete with DEX in terms of cost-effectiveness, and prediction markets can only serve as a means of customer acquisition.

Of course, Coinbase is also actively investing in the crypto-native fields like L2 Base and stablecoin payments. From my perspective, instead of seeking to become an "Everything Exchange," it would be more effective for Coinbase to delve deeper into crypto-native areas, establishing more moats, rather than spreading its limited resources thinly to contend with strong competition across every field.

If Coinbase continues to stubbornly pursue "trading," it may well find itself relegated to being merely a subsidiary of the broader cryptocurrency market.

Structural Issues in the Crypto Market

The unsatisfactory report from Coinbase may signal the beginning of revealing the predicaments faced by cryptocurrency exchanges in the data.

The cryptocurrency market is currently undergoing a rapid differentiation. On one hand, trading mainstream assets like Bitcoin, Ethereum, and SOL no longer necessarily needs to take place on cryptocurrency exchanges, as long-tail memes and similar assets have mature on-chain products; high-quality altcoins may now be one of the few segments that cryptocurrency exchanges can control. However, this portion of high-quality income sources is also being encroached upon by brokerages, and the number of altcoins performing well but not large enough to capture the attention of financial giants is rapidly dwindling, while capital and liquidity are constantly congregating towards the top.

If the cryptocurrency market cannot recreate the situation from 2021 where "all coins soared together," the survival environment for cryptocurrency exchanges is likely to continue deteriorating. In recent years, exchanges including Binance have undertaken large financing, and looking back now, those two years may have marked the peak valuation period for cryptocurrency exchanges.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。