The potential of Hook goes far beyond the current meme token experiment.

Written by: Maher, Foresight News

UNI surged recently from 3.3 USD to 4.17 USD, which may be attributed to the renewed market interest in Uniswap following the on-chain frenzy.

sato broke through a market value of 40 million USD in just a few days, and uPEG rocketed from zero to over 30 million USD in market value within two weeks using the name “Unipeg,” which had been discarded by Hayden Adams eight years ago; Slonks incorporated AI-generated models into smart contracts, achieving hundreds of ETH in sales within six days, with daily trading volume temporarily surpassing CryptoPunks. Their common tag is not meme, not NFT, but Uniswap V4 Hook.

While the market is still using "new narratives" to explain this wave, a more fundamental fact has been overlooked: Hook is not a marketing gimmick of a certain project, but rather a reconstruction of the entire DeFi protocol architecture since going live.

From Exchange Counter to Programmable Market

Before V4, Uniswap was essentially an automated exchange counter. You exchanged ETH for USDC, the price followed x*y=k, the trade completed, and the story ended. V3 introduced concentrated liquidity, allowing LPs to customize price ranges, but the core logic of the protocol remained rigid.

The Hook mechanism of V4 completely breaks this rigidity. It allows developers to insert custom code during the lifecycle of the liquidity pools—before and after trading, when adding liquidity, and when removing liquidity. This means that on the same Uniswap infrastructure, traditional AMM pools can operate alongside issuing protocols with Bonding Curves, dynamic fee models, on-chain limit orders, and even built-in MEV protection modules.

More critically, there is a change at the architectural level. V4 adopts a Singleton design, with all pools no longer being independent smart contracts but coexisting within a unified contract, leading to a significant reduction in Gas costs.

According to on-chain data, the Gas optimization of V4 has greatly lowered the barrier for complex Hook interactions, which is the technical prerequisite for Hook projects to explode densely this year.

What are sato and others doing

To understand the Hook frenzy, one must first understand which capabilities of V4 these projects are utilizing.

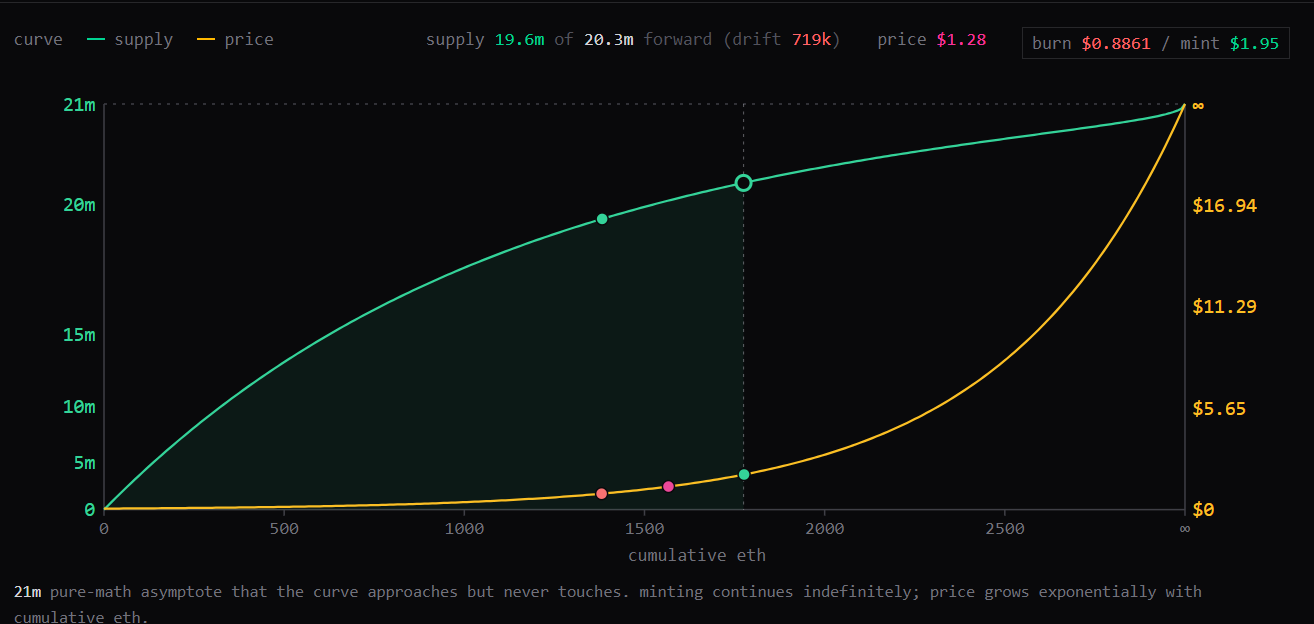

The design of sato is the most typical example of Hook native token economics. It has no pre-mining, no team allocation, no admin rights, and the entire system operates automatically based on a Hook contract. Users send ETH to the contract, and Hook automatically mints sato according to an exponential Bonding Curve; when selling, the contract automatically burns the tokens and returns ETH. When the total supply reaches 99% of the theoretical limit of 21 million (i.e., 20.79 million), minting stops permanently, and the Curve turns into an on-chain automated buyback pool. All trading fees of 0.3% are permanently locked in the Hook contract and cannot be withdrawn by anyone.

This design was nearly impossible to achieve in the V3 era. Developers needed to fork the Uniswap code, deploy an independent AMM contract, and handle complex permission management. However, in V4, all it takes is to write a Hook contract to embed the issuing, pricing, buyback, and burning of the token within Uniswap's liquidity infrastructure.

The gameplay of uPEG showcases the narrative explosiveness of Hook. Its name “Unipeg” originates from a blog post by Hayden Adams in 2019: he initially wanted to name the protocol a combination of Unicorn and PeGasus but abandoned it after Vitalik joked that it sounded more like Uniswap. Eight years later, an anonymous developer @unipegv4 revived this name, redefining it as “Uni + JPEG.” This narrative connects the founder's anecdotes, Vitalik's comments, NFT community slang, and the new mechanism of V4, naturally possessing viral attributes.

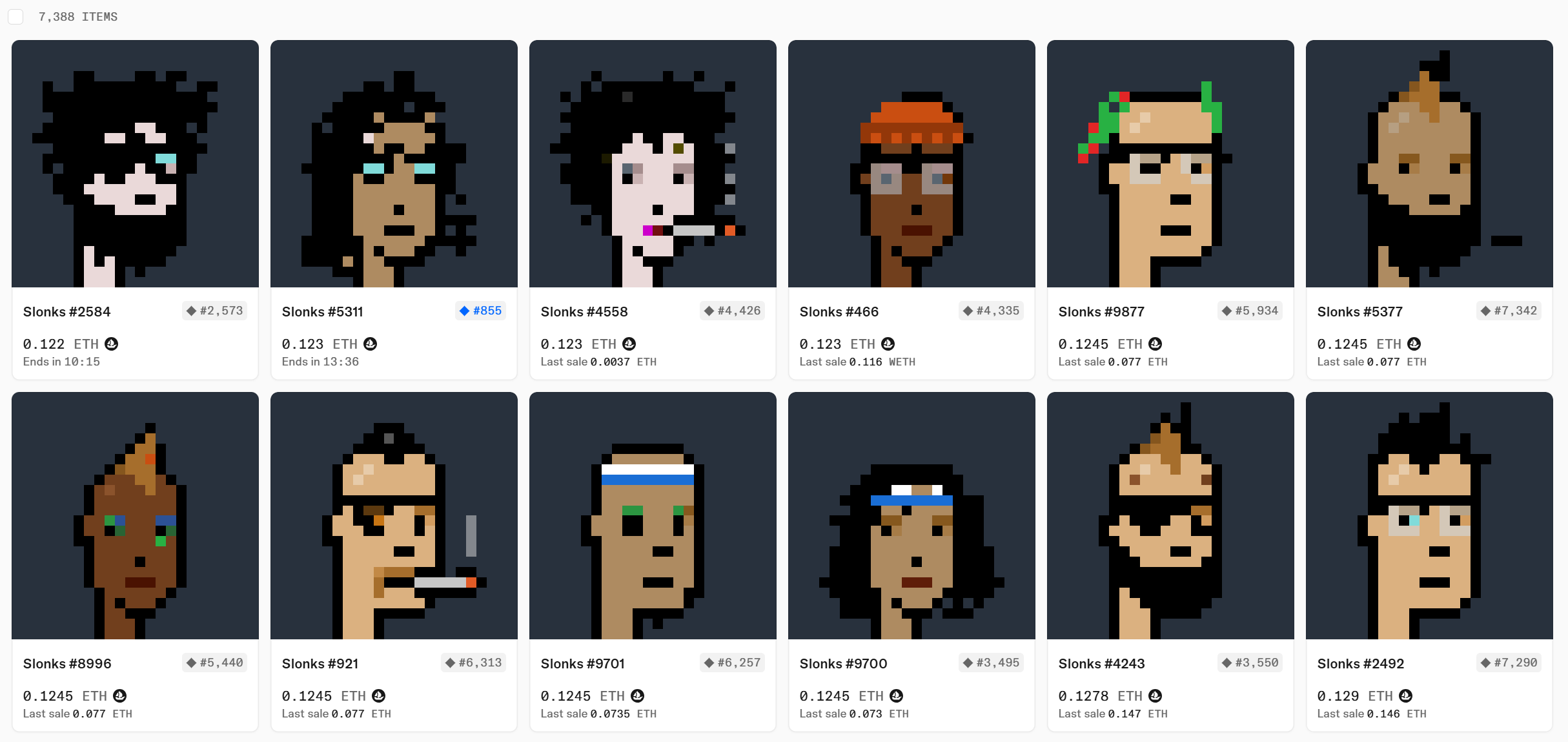

Slonks has gone further by combining AI-generated CryptoPunks replica images with the Hook mechanism, minting at a cost lower than 0.004 ETH, with the floor price rising to 0.123 ETH within six days, representing a 60-fold increase. As of May 11, OpenSea data shows that the transaction volume has exceeded 1200 ETH.

Why now

The Hook mechanism was launched with the V4 mainnet in January 2025, but market attention did not arrive until May 2026. The 15 months in between were precisely the silent construction period of the V4 ecosystem.

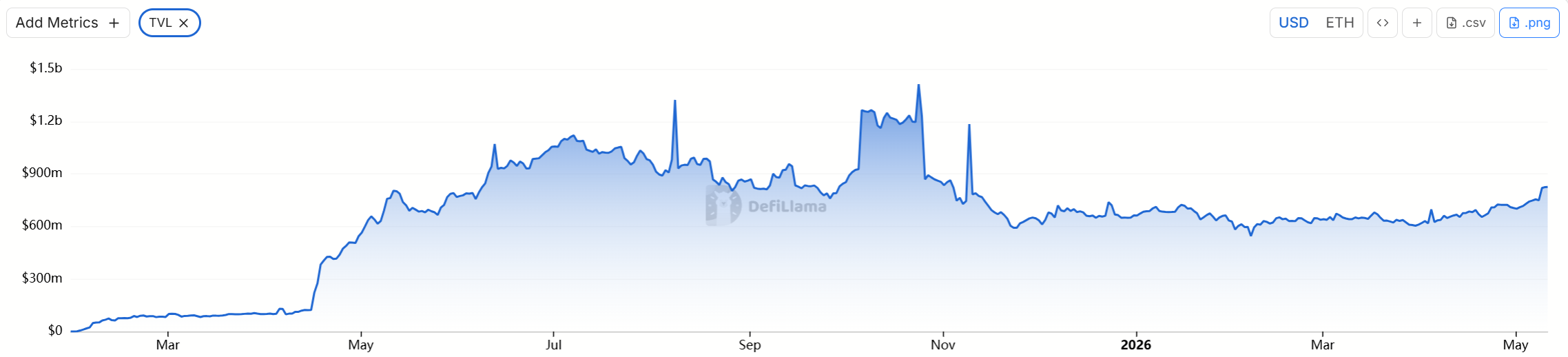

According to DefiLlama data, after V4 launched, the TVL peaked at over 1.4 billion USD but then dropped to 650 million USD, and it has currently recovered to 800 million USD. This indicates that V4 was initially viewed more as a “technical upgrade” rather than a “liquidity migration.”

The real turning point occurred recently: when sato achieved a fair launch of a pure on-chain Bonding Curve using Hook, the market suddenly realized—V4 is not just a better AMM but a platform capable of nurturing entirely new asset classes.

This shift in perception has led to rapid capital rotation. Recently, sato temporarily absorbed uPEG liquidity, briefly pushing its market cap over 30 million USD; on the same day, sat1 surged to a market cap of 10 million USD due to enhanced mechanisms. Such a level of on-chain activity is extremely rare in the bear market environment of early 2026.

Cold Reflection Beneath the Carnival

As an infrastructure, the potential of Hook goes far beyond the current meme token experiment.

The developer logs published weekly by the Uniswap Foundation indicate that developers are exploring complex financial tools based on Hook, such as dynamic fees, time-weighted market making, custom oracles, sequential liquidation auctions, and more.

As of early 2026, the V4 ecosystem has seen the emergence of over 2000 dedicated pools. These pools have transformed Uniswap from an exchange into modular financial infrastructure—any scenario requiring liquidity, pricing, and automation can be built on Hook without the need to fork protocols or create independent AMMs.

However, risks also exist, as the modularity of Hook means that each external contract introduces a new attack vector. The V4 code underwent nine independent audits and large-scale security competitions before going live, but the Hook contract itself is written by third-party developers, with varying security standards.

For ordinary investors, the barrier to participate in Hook projects is not only understanding the Bonding Curve but also verifying the permission settings, fund custody logic, and exit mechanisms of the Hook contracts.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。