Author: Claude, Deep Tide TechFlow

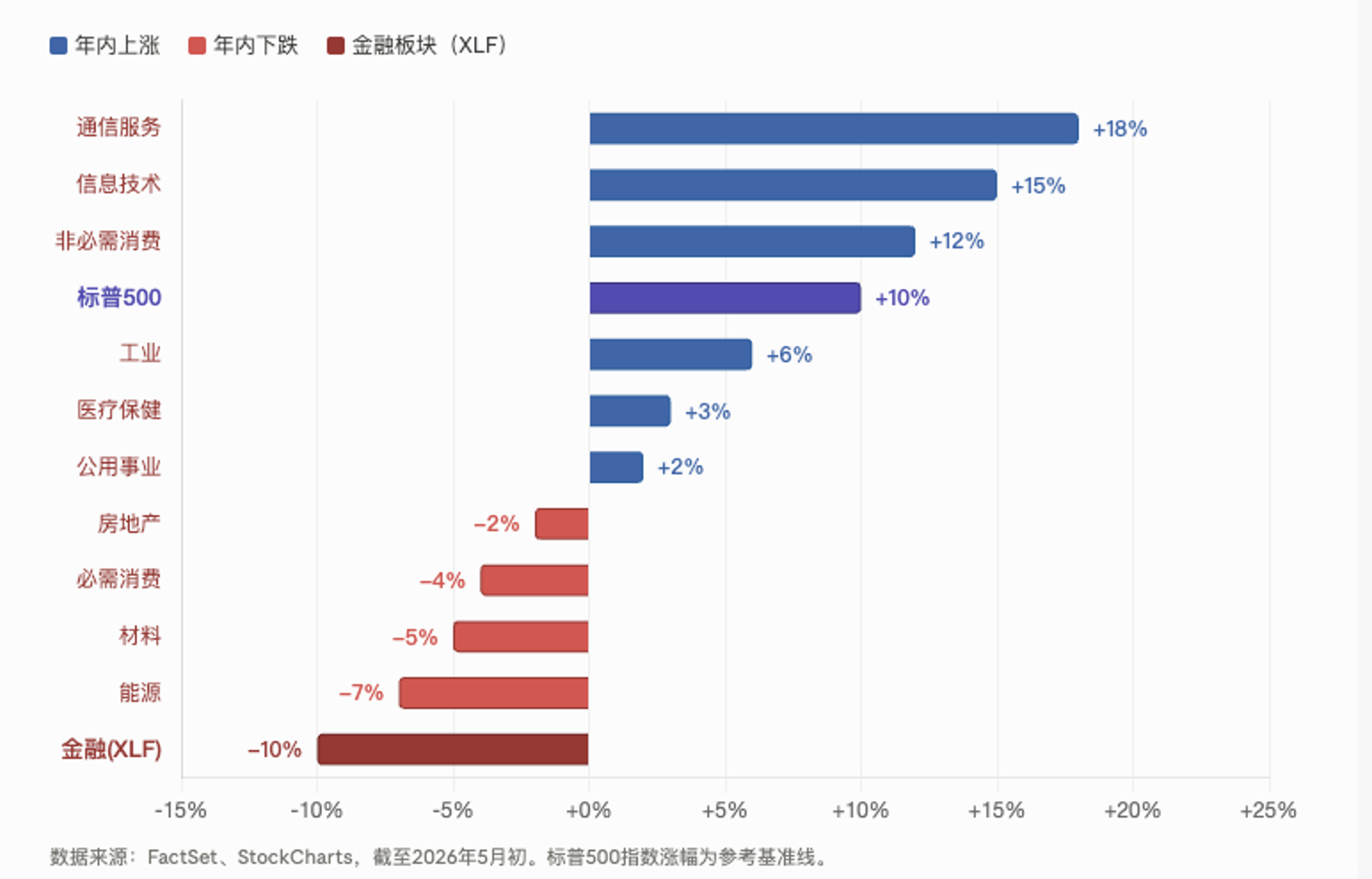

Deep Tide Overview: While the S&P 500 continues to set historical highs and Q1 earnings growth reaches 27.1%, the financial sector has surprisingly become the worst performer, dropping over 6% this year among the 11 sectors. The XLF has fallen to its lowest relative level since 1998 compared to the overall market, weaker than both the financial crisis and the COVID-19 period. The underlying driver is the accelerated exposure of cracks in the $20 trillion private credit market, Blackstone's flagship fund faced a $3.7 billion wave of redemptions, and the FSB issued a systemic risk warning two days ago.

The S&P 500 index closed at a historical high of 7209 points in April, with Q1 earnings growth hitting 27.1%, the highest since Q4 2021, and 84% of the component stocks exceeded expectations. On the surface, U.S. stocks have never appeared so healthy.

However, the financial sector is sending a completely different signal. The XLF ETF tracking this sector has plummeted over 6% this year, making it the worst-performing sector among all 11 industries in the S&P 500. The severity of this divergence has surpassed the levels seen during the 2008 financial crisis and the 2020 COVID-19 shock. According to FactSet and MarketWatch data, the XLF's relative performance against the S&P 500 has fallen to the lowest historical level since its inception in 1998.

Scott Brown, founder of Brown Technical Insights, bluntly stated: The U.S. stock market cannot function without the support of the financial sector, and currently, financial stocks are not even participating in the upward market.

Bank Profits Reach New Heights, Yet the Sector Hits New Lows

The current softness in the financial sector is particularly counterintuitive.

According to FactSet data from May 1, the S&P 500's Q1 earnings growth reached 27.1%, the highest since Q4 2021, with the financial sector's revenue growth also ranking in the top four. Major banks like JPMorgan Chase, Bank of America, and Wells Fargo reported strong quarterly earnings in April.

However, the market is trading not on the seasonal profit reports but on the unseen risk exposures within balance sheets.

The root of the problem points to private credit. This market, estimated at about $1.5 to $2 trillion, has rapidly expanded in the gap left by banks retracting lending after the 2008 financial crisis, and is now deeply entangled with banks, insurance companies, and asset management institutions. When credit deterioration occurs, the chain of transmission is far longer than what is visible on the surface.

$20 Trillion Private Credit: From "Cockroaches" to Systemic Warnings

JPMorgan Chase CEO Jamie Dimon previously likened the emerging problems in the private credit space to "cockroaches," suggesting that seeing one may mean there are many more behind it. This metaphor is increasingly supported by data.

On May 6, the Financial Stability Board (FSB) released a strongly worded report on private credit risk, warning that the complexity, high leverage, and deep interconnection with the banking system of this market could amplify pressures in adverse scenarios, posing risks to broader financial stability. The FSB specifically noted that the high leverage in private credit is concentrated in technology, healthcare, and services, and has never been tested through an extended economic downturn.

The report also singled out an ominous signal: an increasing number of private credit borrowers have begun to rely on payment-in-kind loans, which are typically viewed as a sign of deteriorating credit conditions.

Two days ago, Bank of England Deputy Governor Sarah Breeden publicly expressed concerns over the quality of private credit assets, valuation discipline, and liquidity issues. The European Central Bank has also recently issued similar warnings. Barclays disclosed a $20 billion exposure to private credit, while Deutsche Bank reported about $30 billion.

Blackstone’s Flagship Fund Faces $3.7 Billion Redemptions, Clear Signal of Retail Investor Exodus

Beyond macro-level warnings, the turmoil at the funding level is more direct.

According to a Reuters report on March 3, Blackstone's $82 billion flagship private credit fund, BCRED, faced $3.7 billion in redemption requests in Q1, with redemption amounts reaching 7.9% of fund assets, setting a record since the fund's inception. JPMorgan analysts characterized this as the first net outflow in BCRED’s history, labeling it a "significant expression of investor sentiment sharply worsening towards direct lending." Blackstone was forced to raise its usual 5% redemption cap to 7% and contribute $400 million from the company and executives to meet all redemption requests.

The day after the announcement, Blackstone’s stock price plummeted by 8% to a two-year low.

Another private credit giant, Blue Owl Capital, finds itself in an even more precarious position. Its flagship fund, OCIC, saw redemption requests soar to 21.9% in Q1, but the company only made proportional payments up to the 5% cap, meaning about three-quarters of redemption requests were denied. Its technology-focused fund, OTIC, previously had redemption requests as high as 17% in the prior quarter.

Investment bank RA Stanger provides a striking assessment, suggesting that alternative assets are entering a "sharp turn" phase, with capital withdrawing from private credit, and forecasts that BDC (Business Development Company) capital formation will decline by approximately 40% year-on-year by 2026.

According to PitchBook's survey of around 100 credit institutions, 35% of respondents believe negative perceptions in the private credit sector pose the biggest headwind for the industry, with market sentiment significantly deteriorating compared to six months ago. Morgan Stanley predicts that the private credit default rate will rise to 8%, with about 20% of loans directed towards software companies, particularly concerning given the impact of AI on these assets.

Technical Signals: 90% Historical Probability Points to a Correction

Returning to the technical aspects of the financial sector itself, the signals are similarly bleak.

Scott Brown pointed out that the XLF has not only continued to decline during the S&P 500's new highs but has also consistently operated below the 200-day moving average. Historical data shows that in the previous 32 instances where the S&P 500 reached new highs while the XLF was below the 200-day moving average, the S&P 500 dropped in 29 of those instances one month later, averaging a decline of 3.3%. The win rate six months later is closer to fifty-fifty, but the maximum drawdown in the downside scenario could reach 41.5%, indicating a disproportionately large tail risk.

Among all 11 SPDR sector ETFs of the S&P 500, the XLF is currently the only sector where the price is below both the 50-day and 200-day moving averages, indicating that both short-term and long-term trends are weak.

Historically, the financial sector has given early warnings twice before major market tops. In April 1999, the XLF began to weaken relative to the S&P 500 approximately 11 months prior to the final peak of the S&P 500; in February 2007, the XLF again issued early warning signals, leading the market peak by about 8 months.

Expectations of "Trump Dividend" at the Beginning of the Year Have Completely Fallen Through

The financial sector was highly anticipated at the beginning of the year. The market widely expected that a second term for Trump would bring lower interest rates and looser regulations, creating a favorable environment for banks, insurance, and asset management institutions.

However, according to an early April report by Investing.com, the result has been exactly the opposite. Over a year into Trump's second term, the financial sector has become the worst-performing sector in the S&P 500. Expectations of interest rate cuts have fallen through, private credit landmines have surfaced, and conflicts in the Middle East have pushed up oil prices and inflation expectations, with multiple headwinds compounding.

Melissa Brown, global investment decision-making research director at SimCorp, pointed out that the financial system is highly interconnected, and the associated risks in the private credit field could spread more widely than currently anticipated.

Scott Brown's advice is to be cautious rather than aggressive, noting that judging a top in the current market is not easy, but investors should consider gradually reducing holdings instead of continuing to chase after rises, and should refrain from injecting new capital into the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。