Author: Master Zuo web3

Igniting with Outcomes

History does not repeat itself, but it resonates with the same rhymes. In 2022, mainstream media frantically wrote essays about how high leverage harms both the self and others, while the SEC took the lead in launching regulatory battles against CEXs such as Binance and FTX. The stories within are true; the contracts indeed thrive on the success built on the bones of many. However, the goal of the U.S. is not to eliminate leverage but to participate in the profit-sharing. By 2026, WSJ and Bloomberg once again directed their focus towards "prediction markets." The collective intelligence of Polymarket seems ineffective, with 3% of traders guessing most answers correctly while 0.1% of accounts taking home 67% of the profit.

It's another tale of "the wolf is coming." Coinbase advocates for recognition of prediction markets, and Hyperliquid officially launched HIP-4 to enable the Outcome market. If we all know that legalization is imminent, the question becomes who can predict the winners. Yes: The "events" represented by Polymarket will drive self-fulfilling prophecies; No: The "market-making" represented by Hyperliquid will turn predictions into financial engineering.

Truth has no market

"The success of the narrative surrounding prediction markets is built on a rebellion against the democratic political concept represented by polling."

Since Trump's first election in 2016, the entire Western world needed to answer why he could penetrate layers of barriers, reaching the very center of the secular West, akin to a heretic becoming a pope. The theorists cast spells of "populist politics", while the quantifiers provided data for "prediction markets". The Iowa Electronic Markets (IEM) performed best in 2016, predicting Trump's winning rate at about 28%, exceeding other mainstream platforms.

The problem still exists, but keen observers saw opportunities; there exists a chance for prediction markets to overtake competition, with their accuracy potentially improving further. In 2020, FTX officially launched binary options for TRUMP VS BIDEN, successfully predicting outcomes and achieving a peak daily trading volume of $8M. As the rhymes synchronously aligned, the founders of Polymarket and Hyperliquid, Jeff, attempted to predict the market during this period. The 2024 presidential elections completely transformed prediction markets into super products following CEXs and DeFi. Even from daily data, sports betting > politics > crypto > long tail (culture, entertainment), but predicting presidential candidates truly possesses an entertaining effect, and public opinion bears immense leverage. A president cannot be elected daily; prediction markets must find a route for daily scenarios, with the desire for liquidity becoming an extreme ambition across all platforms. The most typical example is early Polymarket, which charges no fees and clearly does not bet against users, making every effort to maintain the platform's fairness.

To date, theoretically, one cannot say Polymarket is fraudulent, but practically, as mentioned earlier, only 3% of experts can guess the answers correctly. Regarding trading fairness, Polymarket not only began charging fees but also continually shifts standards and values between Bots, market makers, and ordinary retail investors. This is the double-lock of prediction markets: First lock: To have liquidity, Bots and market makers must remain; however, once they stay, "collective intelligence" effectively becomes the intelligence of 3% experts + Bots, with retail investors merely serving as liquidity providers, causing the narrative to collapse from within. Second lock: If Bots and market makers are expelled to "restore collective intelligence," liquidity immediately vanishes, and worse, retail traders trading alone will not approach truth but cause market failure. The claim that "collective intelligence can approach truth" is ultimately self-refuting.

Bots are both the oxygen of prediction markets and the poison of its narrative. Although Polymarket does not play the role of a bookmaker, the combination of Bots + experts has already become a new bookmaker organization, essentially siphoning liquidity from the entire market for their profit. With no extraction fees, the protocol has no income, making the $POLY price unsustainable. Liquidity is a demon that requires a soul for exchange. However, from another perspective, precisely because of this deadlock, its liquidity structure has been anchored—where experts are, where Bots are, where retail investors stand, with each role’s capital volume, behavior patterns, and entry-exit rhythms repeatedly validated by the market. This is a vividly depicted, stable pool of participants, a paradox internally, yet externally a ready sample.

Since Polymarket cannot resolve this internally, the industry has naturally seen several alternative routes. Kalshi pursued a "change of subject"—focusing on sports betting. The results are objective, and settlements are clean, eliminating the need to debate whether "collective intelligence can approach truth," as there is fundamentally no "truth" to approach, only scores. With regulatory license support, Kalshi outvalued Polymarket at $22B in the capital market, relying not on more accurate predictions but on lighter questions.

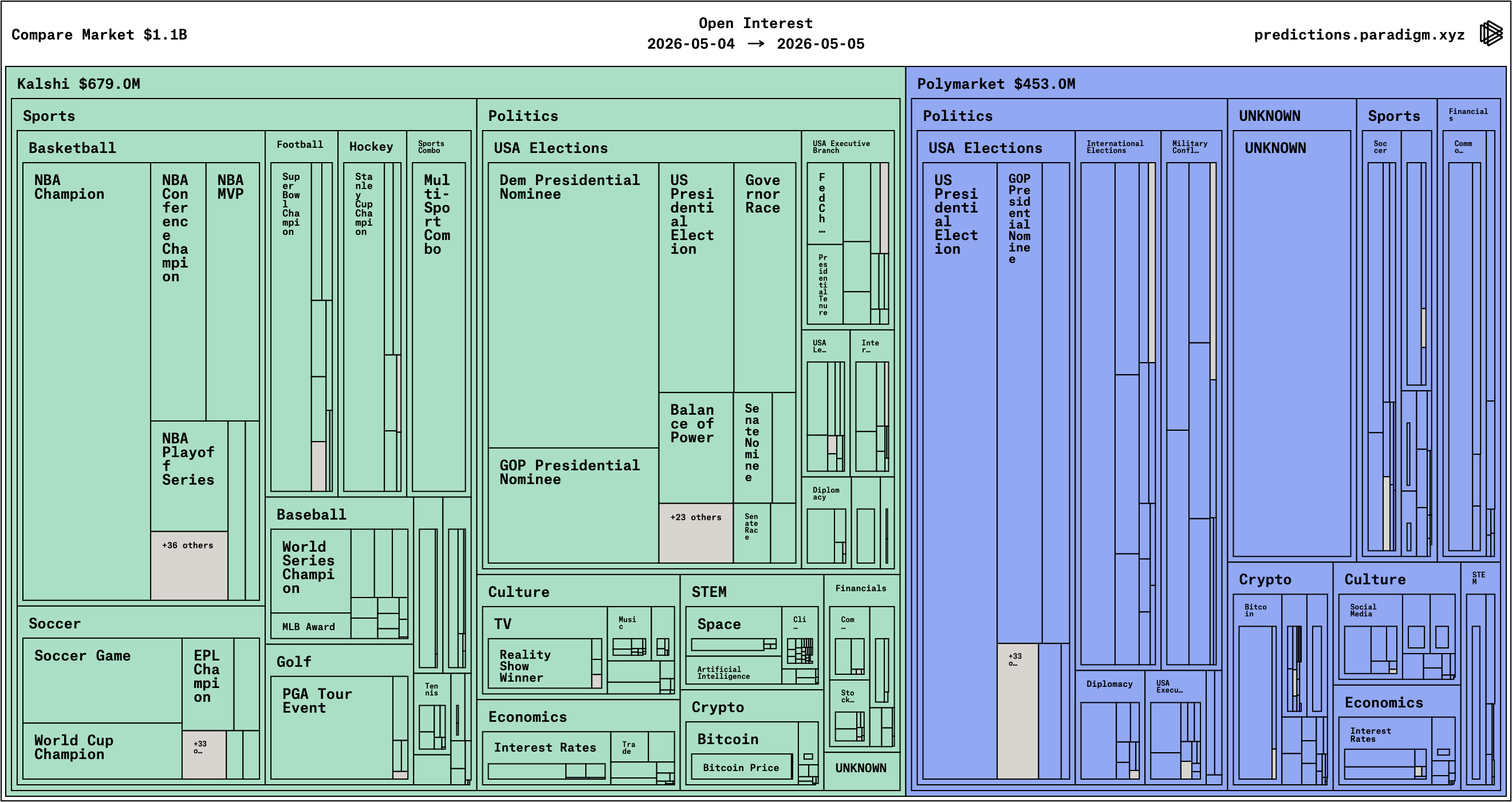

Image description: Comparison between PL and Kalshi OI. Image source: @notnotstorm. Paradigm took the route of "changing categories"—besides betting on Kalshi, it also supports attention markets, decision markets, opportunity markets, and other long-tail products, turning the step functions of 1/0 into continuous "fat tail" distributions to avoid the most fatal mechanical issues of prediction markets. Hyperliquid adopted the approach of "changing frameworks"—it does not intend to prove whether collective intelligence is valid. It degrades prediction markets to a component of derivatives hedging, leveraging the pool's liquidity to create a new market.

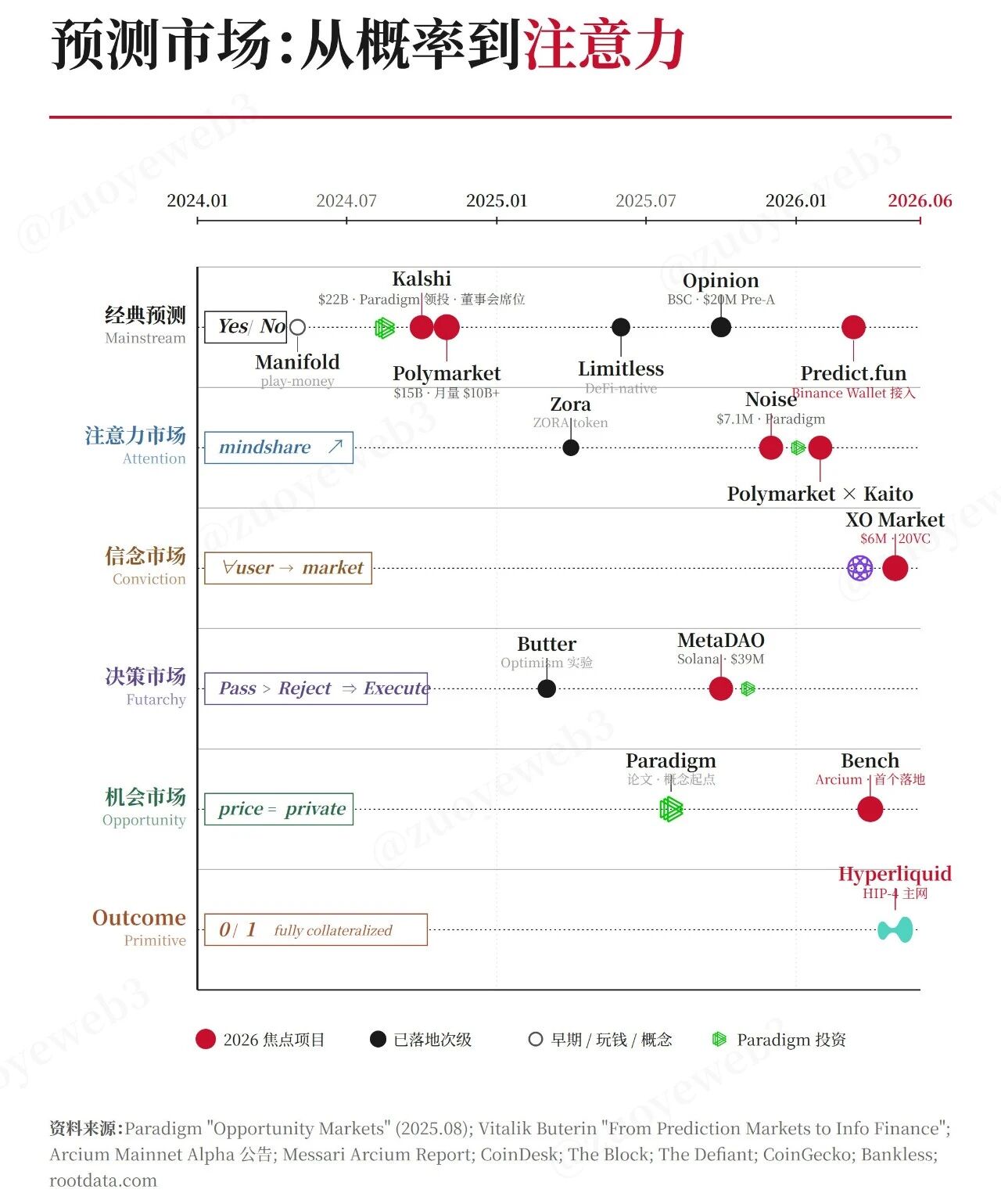

Image description: Classification of prediction markets. Image source: @zuoyeweb3

The Engineering of Liquidity

"The uniqueness of humanity may lie in the ability to recognize which direction deserves a lifetime of effort even without feedback signals."

HIP-1 opened the spot market, HIP-2 opened "non-manual" instant liquidity, and HyperCore provided initial order placement capabilities on-chain, addressing the "cold start" issue from a technical perspective. In other words, Hyperliquid views liquidity as an engineering problem, not a trading willingness problem. Of course, Hyperliquid's spot market cannot be said to be successful, and HIP-2 is not a third-party volume-boosting Bot, but the attitude conveyed is quite intriguing; Hyperliquid welcomes all Bots that increase liquidity.

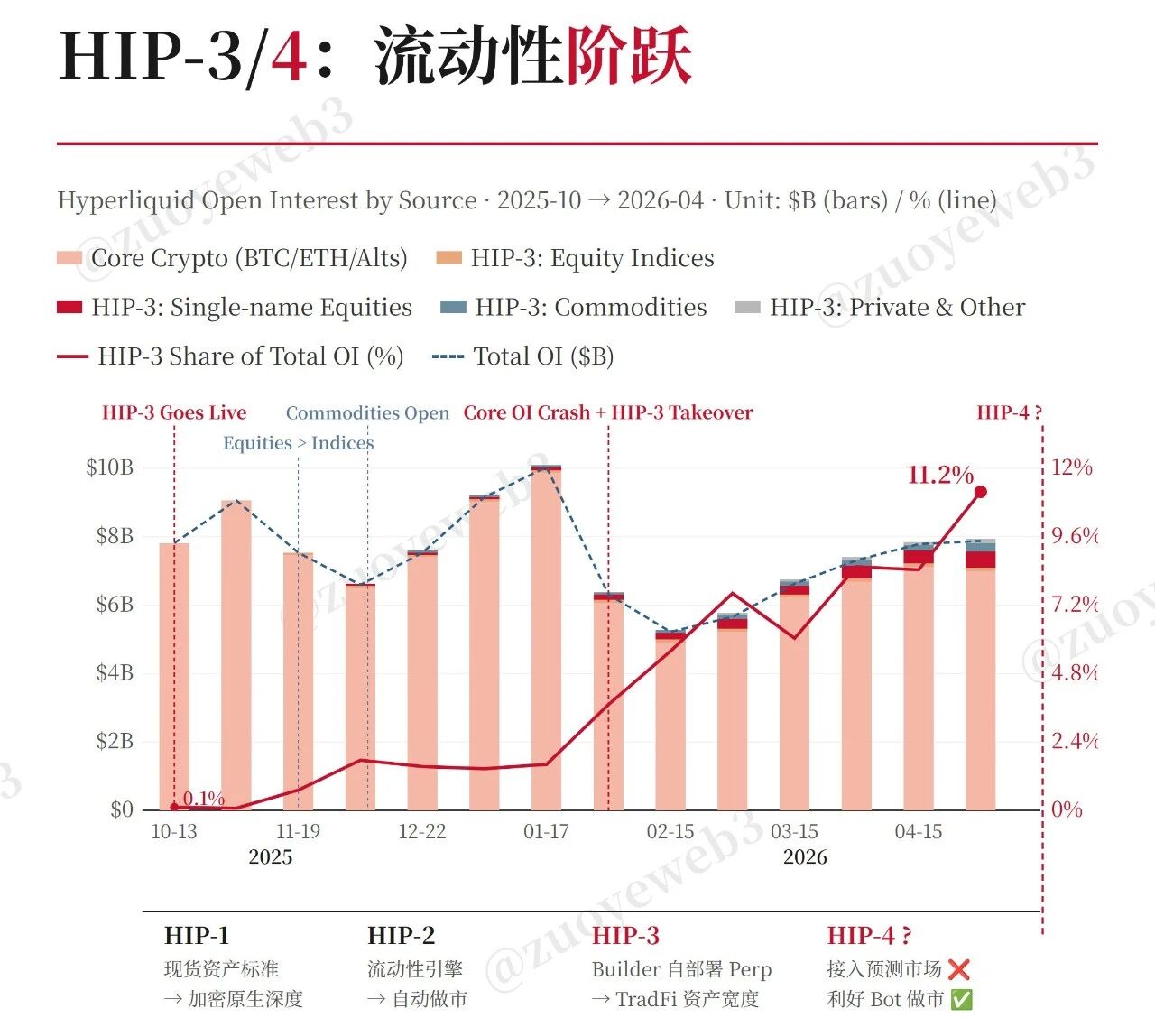

Image description: HIP-3 liquidity. Data source: @21shares. Hyperliquid's spot trading is highly concentrated in a few currencies like BTC/ETH/HYPE; the auction-based spot mechanism for listing assets has not made breakthroughs, but the TradFi targets introduced in HIP-3 have indeed brought incremental benefits to HyperCore Perp. Trade[xyz] has effectively become a mainstream player in the on-chain RWA Perp, bringing Hyperliquid one step closer to becoming the AWS of liquidity, especially as Trade[xyz] begins entering the Pre-IPO market, which is essentially an event contract with the market speculating on its IPO price.

Whether it’s Trade[xyz] or HyperCore, the vast majority of the trading volume comes from Bots enhancing volume; this is not fraud but the real source of liquidity. HIP-3 is a prototypical paradigm; it is not adding SKUs for itself but packaging existing liquidity of RWAs into HyperCore. Looking towards HIP-4, the question is not "will it create another category of prediction market," but "how will it take over the liquidity of prediction markets."

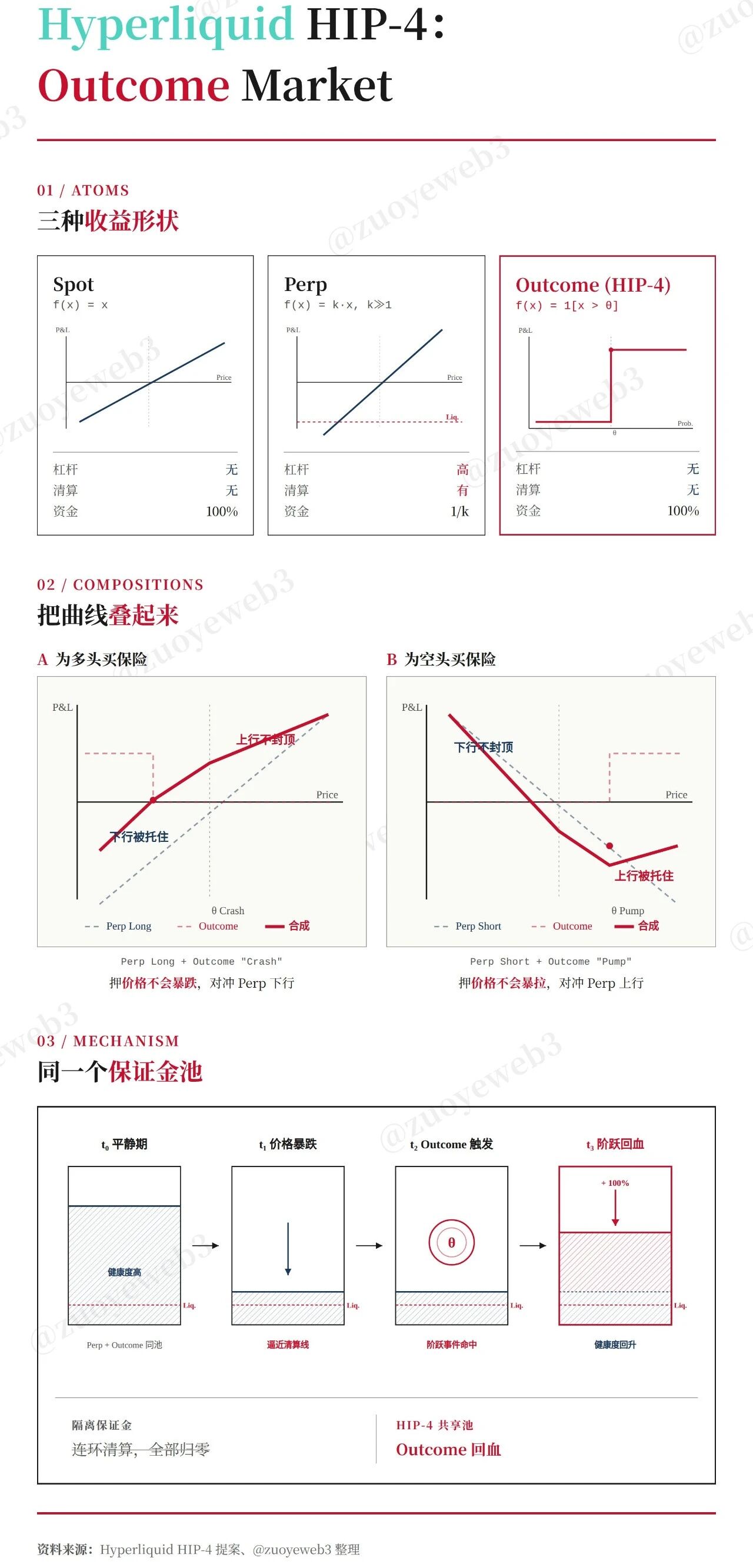

In reality, the leverage issue in prediction markets originates from their step-functions, which can flip from 1 to 0 instantaneously; you have no chance to resist trends with margin collateral—not a speed issue but a mechanical one.

Image description: Adding leverage to insurance. Image source: @zuoyeweb3. The significance of HIP-4 lies in its organic integration of Perp and Outcome, where margin is unified and can be combined inversely. Prediction requires small full capital input without leverage, while contracts allow for infinite leverage from small funds, effectively adding leverage to the contracts.

When opening long on contracts, buy inverse bearish predictions; if the price rises at expiry, only the prediction margin is lost, and overall profits are made;

When opening long on contracts, buy inverse bearish predictions; if the price falls at expiry, the prediction market profits while the contract incurs significant losses.

Insurance is effective when prices rise but becomes ineffective when they fall. However, the insurance mechanism of HIP-4 is "inadequate insurance," making it difficult to design a mechanism that fully offsets Perp losses. It has positive significance in mitigating cascading liquidations and avoiding wild surges akin to 10·11; however, theoretically, Perp leverage is infinite and, combined with spot mechanisms and more sophisticated financial engineering, the entire system circulates and nests, ultimately leading to systemic crises. The only certain benefit is that connected margins can increase liquidity for the current Perp, slowing down liquidations. A more practical hidden danger lies in fairness: HIP-4 currently concentrates on "price guessing" products; a short-term deviation of BTC from its target price is not impossible, as there were already signs on the first day. Small coins rely on off-chain oracles, introducing greater contention.

HIP-4's own scale might not be larger than HIP-3; viewing solely from the "price guessing" products, it may even stop at a moderate category. However, the value of HIP-4 is not in size but in paradigm; it simultaneously executes "leveraging existing market liquidity + hedging mechanisms + margin interchange," so a new derivative's cold start does not have to begin from scratch.

Conclusion

HIP-1/2 solved "how to initiate oneself", HIP-3 solved "how to get others to initiate TradFi with me", and HIP-4 addresses "how to take over liquidity from other markets". This is a progressive engineering route; the House of All Finance is not just a slogan but the natural endpoint of this route.

Any new derivative's cold start does not necessitate educating users from scratch or buying liquidity from zero; rather, it seeks to find an existing market where liquidity has already been validated, designing a set of hedging mechanisms so that the liquidity of existing markets will naturally flow into the new products. Polymarket gathers liquidity using the narrative of collective intelligence, treating liquidity as a faith; Hyperliquid reallocates liquidity through engineering, treating liquidity as a component. The former struggles with the tension between fairness and extraction, while the latter sidesteps this issue entirely. Whether you make money or not is unimportant; what matters is whether your position serves as a hedge against the other side's position.

The primary driving force of liquidity comes not from marketing but from market structure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。