Author: Godot

After the market closed yesterday, Arm announced its fourth quarter financial report for fiscal year 2026. With the official announcement of the AGI CUP, Arm has shifted from previously not manufacturing chips and only providing instruction set architecture to becoming an AI CPU provider, changing its business model from IP licensing to custom Silicon and computing subsystem supplier.

However, there are divergences on Wall Street regarding Arm's future. One side bets that agentic AI will completely rewrite the landscape of CPUs.

The other side is concerned about issues such as memory costs and TSMC's capacity limitations, fearing that the current extremely high valuation multiple for $ARM seriously overdraws the expectations of perfect execution in the future.

1) Firstly on the data aspect

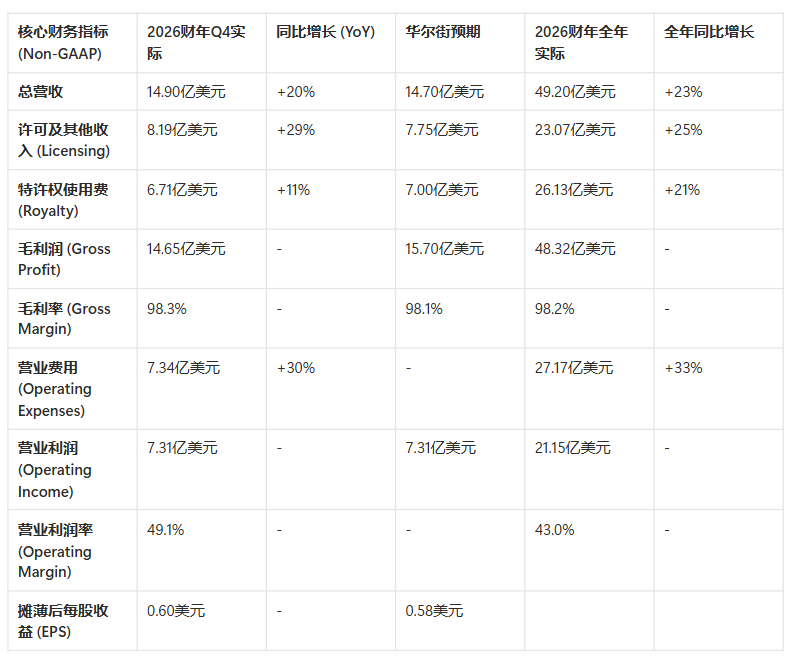

In the fourth quarter of fiscal year 2026, total revenue reached $1.49 billion, a year-on-year increase of 20%, exceeding Wall Street's previous consensus expectation of $1.47 billion.

Total annual revenue reached a record $4.92 billion, a year-on-year increase of 23%.

Among these, there was a significant divergence between licensing revenue and royalties.

Licensing and other revenue increased by 29% year-on-year to $819 million, as chip design companies accelerated obtaining next-generation architecture licenses from Arm to seize the AI opportunity.

The leading indicator for assessing the long-term health of the licensing business, the Annual Contract Value (ACV), increased by 22% year-on-year, exceeding the management's medium to high single-digit long-term target.

Royalty income reached $671 million, which is a year-on-year increase of 11%, below the market's previous expectation of $700 million.

The strong demand for front-end licensing and weak back-end royalties indicates that the recovery in downstream consumption is not optimistic.

In terms of cost and expense control, Arm continues to increase its R&D investment in AGI CPUs, computing subsystems, and complete chip solutions.

In the fourth quarter, Non-GAAP operating expenses reached $734 million, a year-on-year increase of 30%. Annual operating expenses soared by 33% year-on-year to $2.717 billion.

Fortunately, the IP licensing model inherently has high gross margins, with the Non-GAAP operating profit margin in the fourth quarter at 49.1%, maintaining at 43.0% for the entire year.

In terms of cash flow and balance sheet, net cash flow from operating activities was $1.524 billion, with Non-GAAP free cash flow at $882 million.

At the end of the period, cash, cash equivalents, and short-term investments totaled $3.601 billion, reserving ample ammunition for subsequent advanced wafer and packaging capacity allocation at TSMC.

2) Bullish narrative: Agentic AI pushes CPU back to the center

Beginning this year, AI is entering the agentic AI phase represented by Openclaw.

In the past, large models were static, waiting for user input prompts. Agentic AI is automatic, requiring CPUs to handle control and orchestration tasks.

Internal data from Arm indicates that in complex agentic workflows, as much as 50% to 90% of system latency is actually caused by insufficient CPU scheduling capabilities.

As a result, hardware configurations have been forced to adjust. In the past, the ratio of CPUs to GPUs in AI training clusters was often 1:8 or even lower.

But this ratio is changing to 1:4, and in the future, it may even approach 1:1.

Arm conservatively estimates that the demand for CPU core density in data centers will surge from the current deployment of 30 million cores per gigawatt to 120 million cores, a nearly certain quadrupling of physical expansion.

At the same time, each concurrent agent needs to maintain a large KV Cache and complex contextual states, and the CPU platform also has to take on massive memory management tasks.

UBS estimates that the total potential market size for server CPUs will soar from approximately $30 billion in 2025 to $170 billion in 2030, approaching a fivefold expansion.

Moreover, as supercomputing centers will prioritize power efficiency and high-density scalability in the agentic AI era, Arm's streamlined instruction set architecture, with its low power consumption advantages, is expected to capture a significant portion of the new market share.

By 2030, Arm's market share in the server CPU field is expected to rise from approximately 15% in 2025 to 40% to 45%.

This is the core basis for institutions such as Evercore ISI being optimistic about Arm's long-term explosive growth potential.

On the product level, only six weeks after the release of Arm's AGI CPU, the clear demand orders from clients for fiscal years 2027 and 2028 have already doubled from the initially expected $1 billion to over $2 billion.

Aside from Meta, European AI cloud provider Verda has clearly stated that it will deploy AGI CPUs on a large scale in the next-generation infrastructure, coordinating with NVIDIA's GB300 and Vera Rubin systems for agentic computing power orchestration.

Cerebras, OpenAI, as well as ODM manufacturers like Lenovo, Quanta, Supermicro, and ASRock have also launched complete server solutions based on this chip.

3) Concerns are TSMC's packaging and HBM capacity

However, Arm expects that substantial sales revenue from the first batch of silicon chips will not be confirmed until the fourth quarter of fiscal year 2027, and large-scale production will have to wait until fiscal year 2028. There is a mismatch period of over a year between demand and financial realization.

The Arm AGI CPU architecture integrates a large amount of HBM, with TSMC's exclusive CoWoS packaging being the only mature and reliable interconnect solution currently.

Compared to NVIDIA and AMD, Arm, as a new entrant, is at a disadvantage in TSMC's priority sequence. HBM supply is also tight.

In the next 12 to 18 months, Arm's core competitiveness will shift from architectural design capability to supply chain capacity acquisition capability.

4) Bearish perspective: Valuation has been overdrawn

Therefore, the cautious faction, represented by Vivek Arya of BofA Securities, has downgraded Arm's rating to neutral, reducing the target price range to $120 to $135.

Its core short-selling logic includes two points.

Firstly, consumer smartphones are facing severe headwinds from rising memory costs, and Arm's traditional royalty revenue growth is nearing its peak. The royalty growth rate falling to 11% this quarter has confirmed this pressure.

Secondly, the company's recent rapid growth in licensing revenue is heavily reliant on internal fund circulation from its parent company SoftBank, with this related party transaction accounting for nearly 30% of total licensing revenue, raising market concerns about circular financing and revenue quality.

BofA states that Arm's current valuation multiple is severely overdrawn against expectations for future perfect execution.

The $2 billion AGI CPU nominal orders, constrained by a global shortage of packaging capacity, will be unable to convert into substantive cash flow to support financial statements before fiscal year 2028.

This is the fundamental reason for the divergence on Wall Street.

In conclusion,

Arm stands at a crossroads defined by architectural dividends and capacity bottlenecks. Agentic AI offers the most imaginative entry ticket for the next five years, but to realize this ticket, one needs to pass through TSMC's packaging workshop, the HBM supply list, and more.

Bulls see a $170 billion market in 2030, while bears see a cash flow vacuum before 2027. Both perspectives seem correct, just differing in pace.

Attached report link: https://tradingview.com/symbols/NASDAQ-ARM/documents/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。