Author: Jae, PANews

On May 6, Strategy released its Q1 2026 financial report.

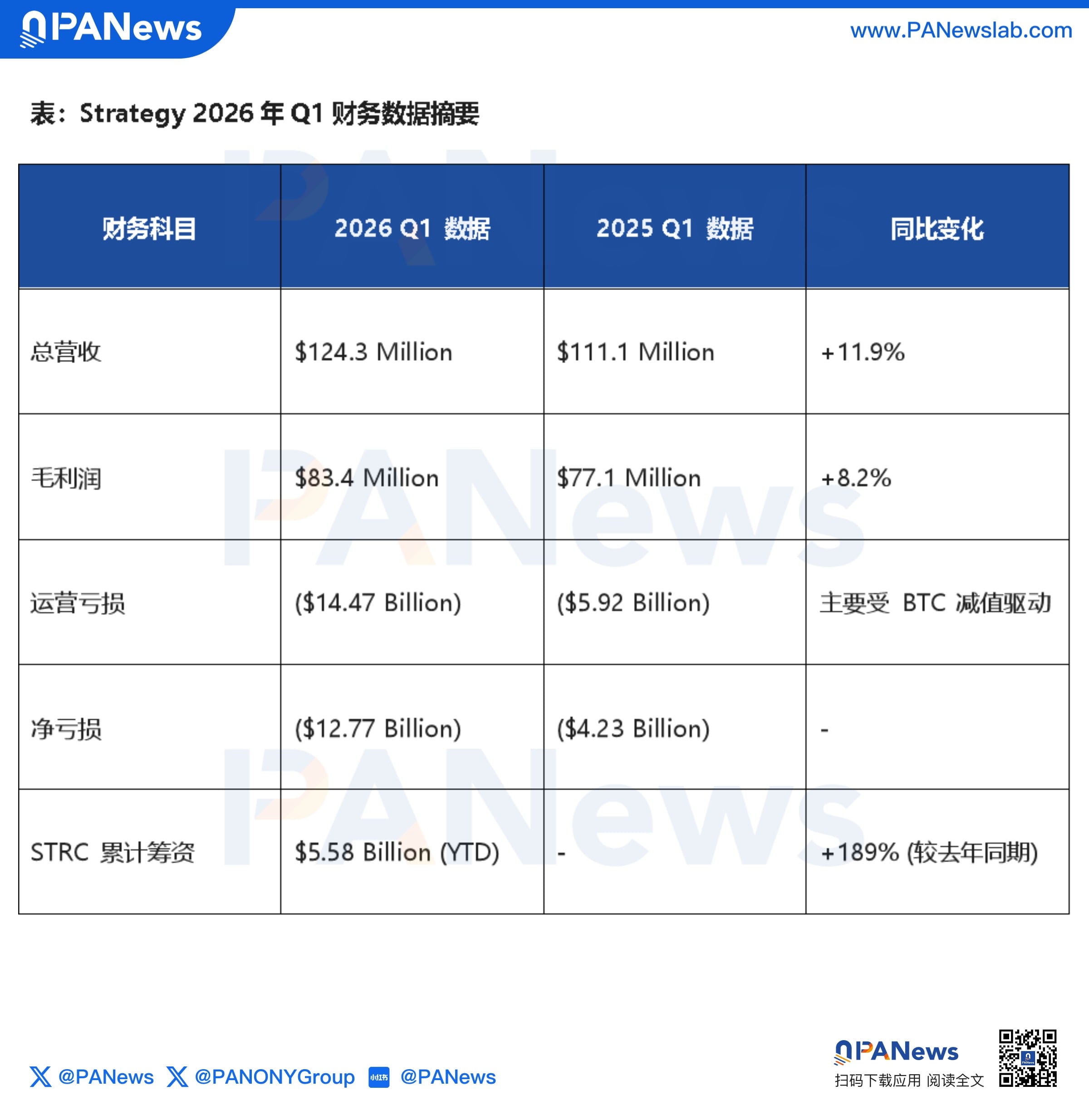

The numbers were not good: a net loss of $12.54 billion, mainly due to the fair value changes of its Bitcoin holdings. CEO Michael Saylor hinted during the conference call that "some Bitcoin might be sold to pay dividends."

As soon as the news came out, Strategy's stock price dropped over 4% in after-hours trading, and Bitcoin briefly fell below $81,000.

However, while traditional markets were voting with their feet, Strategy's product was being sought after in another market. Its perpetual preferred stock STRC is becoming the "new favorite" in the DeFi space.

Three major DeFi protocols - Saturn, Apyx, and Pendle - have built a "BTC on-chain yield structure" around STRC, initiating a financial experiment to explore the ultimate capital efficiency of Bitcoin.

11.5% high interest temptation, STRC drives DeFi integration

In July 2025, Strategy launched perpetual preferred stock STRC on Nasdaq, with no maturity date, no need to repay principal, and only monthly dividend payments, becoming a financing tool for Saylor to buy Bitcoin.

When STRC's market price is below its $100 par value, the board will raise the dividend rate to attract buyers; conversely, it will lower the dividend rate if above par. As of May 2026, STRC's annualized dividend rate has risen to 11.5%, far higher than the approximately 3.7% yield of U.S. Treasuries, making it highly appealing to a large number of retail investors.

Related reading: STRC drops below $100, Strategy's Bitcoin buying machine slows down

This mechanism has created a financing flywheel for Strategy. The company will only issue new shares at par value to raise funds when STRC's price is at least $100, and, after deducting dividends reserves, the funds will be used to purchase Bitcoin.

Saylor referred to this model as "smart leverage": for every $1 of financing through STRC, Strategy issues $2 of common stock MSTR, maintaining approximately a 33% leverage ratio. This means that $1 of STRC will be converted into $3 of Bitcoin buying.

Today, STRC's issuance scale has reached $8.5 billion, ranking among the largest preferred stocks worldwide. Even though Strategy recorded a net loss of $12.8 billion in Q1 due to Bitcoin impairment, STRC still boasts a Sharpe ratio of 2.53 and maintains relatively ample liquidity.

The performance of STRC has also laid the groundwork for DeFi protocols to bring it on-chain.

Saturn takes the lead, bringing STRC dividend yields on-chain

Saturn is the first protocol to take the initiative. It secured $800,000 in seed funding from Yzi Labs and Sora Ventures to convert STRC's dividend yields into on-chain stablecoin cash flow, co-founder Kevin Li described the protocol as the "Tether of digital credit."

Saturn employs a dual-token model similar to Ethena, separating liquidity and yield:

USDat: The base stablecoin, 100% collateralized by tokenized U.S. Treasuries, serving as the protocol's liquidity layer, primarily used for payments, settlements, and DeFi collateral;

sUSDat: Staked version of USDat, when users deposit USDat into a staking contract, Saturn will switch the underlying reserve asset from Treasuries to STRC, and the yield of sUSDat directly comes from STRC's monthly dividends.

Currently, Saturn's total holding of STRC has increased to approximately $50 million. Since STRC pays in cash, Saturn will enable sUSDat to appreciate relative to USDat through cash reinvestment or exchange rate adjustments. As of May 7, sUSDat's yield has reached 9.51%.

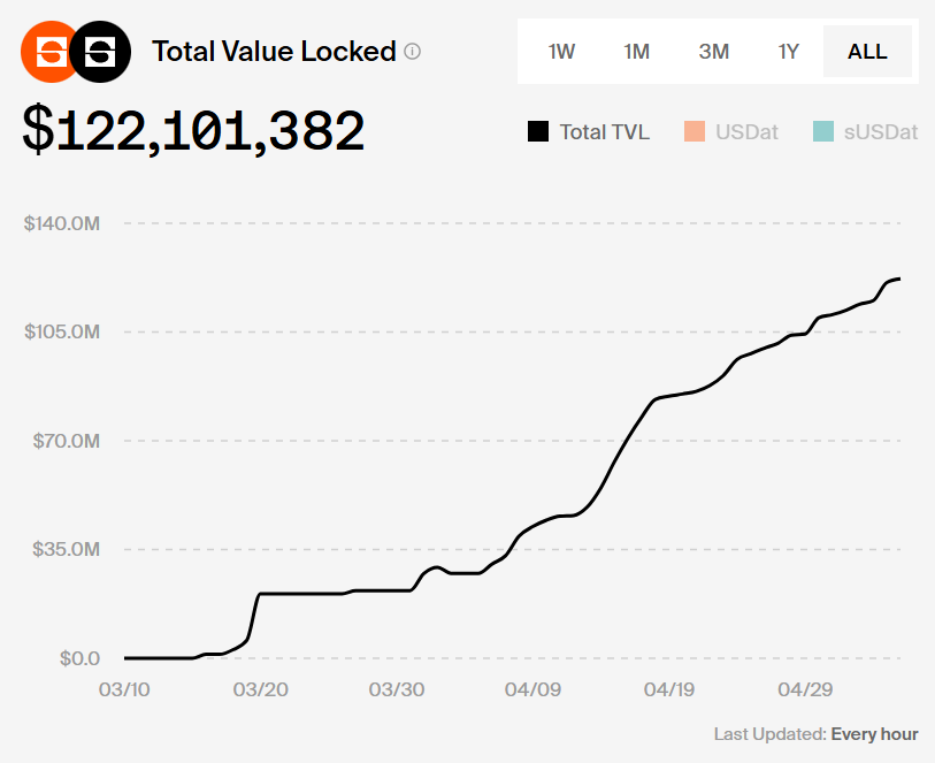

To attract early users, Saturn launched the "Gravity Points" reward program, offering up to 18 to 20 times the points for providing liquidity on the USDC/USDat and USDC/sUSDat trading pairs on Curve, rapidly establishing initial liquidity depth. Within just one month after going live on the mainnet, Saturn's TVL surged from $40 million during the beta phase to $122 million, an increase of over 3 times.

$130 million heavily invested in STRC, Apyx focuses on yield enhancement

If Saturn is building the basic currency, Apyx is enhancing credit yields. As the largest external holder of STRC on-chain, its holding value is close to $130 million, relying on "yield aggregation" to roll basic dividends into excess returns.

Apyx also adopts a model that separates non-yield stablecoins from yield certificates:

apxUSD: Synthetic USD, backed by over-collateralized preferred shares SATA issued by STRC and Strive. apxUSD does not directly pay yields but is mainly used for liquidity in the lending market.

apyUSD: Yield certificate, users can obtain apyUSD by depositing apxUSD, with the latter appreciating through capturing all dividend flows from the underlying asset portfolio.

Unlike Saturn, Apyx's yields have a "leverage effect." Not all apxUSD holders choose to stake, and all dividends generated by STRC will be distributed to the fewer apyUSD holders. As of May 7, the 30-day average annualized yield of apyUSD was 11.1%, with an expected yield set above 13%.

It is worth mentioning that Apyx's risk management mechanism also carries some aspects of traditional finance.

- Dynamic rebalancing: The asset basket will automatically adjust according to issuer concentration limits, liquidity demands, and over-collateralization requirements;

- 30-day redemption cooling period: ApyUSD's redemptions have a 30-day cooling period to prevent liquidity squeeze risks.

Principal and interest split, Pendle engraves interest rate curves on STRC assets

While Saturn and Apyx brought STRC's dividends on-chain, Pendle infused credit attributes into these assets through yield tokenization.

Pendle splits yield assets sUSDat/apyUSD into two independent tokens:

PT (Principal Token): Principal token, typically trades at a discount, held until the maturity date, allowing users to redeem back the underlying asset on a 1:1 basis, locking in a fixed annualized yield, and thus hedging against interest rate fluctuations of the asset.

For example, suppose a user buys a PT-apyUSD with a term of 1 year and an implied yield of 18.42%, which means that for every 1 apyUSD spent to acquire 1 PT-apyUSD, the user will receive 1.18 apyUSD upon redemption at maturity.

YT (Yield Token): Yield token, YT prices are typically much lower than the underlying asset price, allowing users to gain leveraged exposure to perceived increases in STRC dividends with a smaller capital.

For instance, if the price of 1 YT-sUSDat is 4% of the sUSDat price, this means that by spending 1 sUSDat, the user can purchase 25 YT-sUSDat, and even a small increase in sUSDat (STRC) yield could lead to a 25-fold increase in the user's returns.

In addition, users can also provide liquidity in Pendle's sUSDat and apyUSD pools to earn trading fees and PENDLE token incentives.

Pendle's intervention has brought "implied yield" curves to the Bitcoin credit market for the first time, marking a leap for Bitcoin into credit-type assets. Currently, the TVL of the assets issued by the two major protocols Apyx and Saturn on Pendle has reached $200 million and $55 million, respectively.

DeFi reinforces the resilience of STRC financing, nested leverage creates interlinked liquidation risks

As DeFi protocols successively integrate STRC, it appears to be another upgrade of DeFi gameplay; in essence, it also reversely impacts Strategy's financing capacity and Bitcoin's asset properties.

DeFi protocols serve as major buyers of STRC, objectively enhancing STRC's price resilience in the secondary market. As long as STRC maintains a price above par, Strategy can continue to issue new shares to buy more Bitcoin.

According to Strategy, over $270 million of STRC is circulating in the DeFi market, accounting for about 3% of its total issuance. This model of on-chain liquidity feeding back into off-chain credit will become one of the classic cases in the RWA field.

Through STRC and its DeFi derivatives, Bitcoin has been endowed with "yield" characteristics. For a long time, Bitcoin was regarded as "digital gold," with its primary value based on scarcity, rather than cash flow. Now, investors can achieve above 10% annualized returns by holding stablecoins based on STRC's dividend flow without needing to sell their Bitcoin.

Despite the intricate on-chain yield structure of STRC, its multi-layer nested characteristics also mean that risks and vulnerabilities are magnified.

Some DeFi players are amplifying yields through circular leverage: users deposit assets in Apyx to obtain apxUSD, package it in Pendle to receive PT, then use PT as collateral on Morpho to borrow USDC to purchase more apxUSD. This 5x leveraged circular operation can elevate fundamental yields to 60% or even higher.

However, the assumptions supporting this chain are very fragile: STRC has dividend deferral risks. Preferred stock dividends are not mandatory, and under pressure from unfavorable market conditions, Strategy's board may choose to suspend or defer payments, which could lead to a significant price deviation of STRC from par. If apxUSD gets into an under-collateralization situation, it could trigger a chain reaction of on-chain liquidations.

From STRC on Nasdaq to the three-layer on-chain yield structure, the crypto market is creating a new capital logic: Bitcoin as the underlying asset, Nasdaq responsible for price discovery, and DeFi for distribution and circulation in the digital credit system.

Saturn fortifies the currency layer, Apyx strengthens the yield layer, and Pendle dismantles the interest rate layer, together forming the framework of the digital credit system, as Bitcoin completes its transition from currency to asset and then to credit base.

However, high yields always coexist with high risks, and in the sleepless Bitcoin market, the cost of leverage often comes unexpectedly.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。