Author: Zuo Ye Web3

Aave's "Triangle Debt", Stani Pretends to be a Coordinator

The shockwave caused by Kelp DAO to Aave is gradually reducing, and everything seems to be returning to normal.

DeFi protocols can claim that the DAO mechanism is effective, and the LST/LRT protocols avoid collective collapse, many retail investors also fantasize that DeFi United will provide airdrops.

However, DeFi United is still a subset of "socializing losses", but different from direct relief through DAO/tresury and resembling traditional financial debt restructuring.

Using this as an example, let’s discuss how DeFi can become a more efficient financial system, offering us some comfort in these increasingly dull times.

In past security incidents, it was either a direct shutdown like Balancer or full compensation like Tribe DAO, but the outcome was highly similar; the protocol itself could not continue, leading to insolvency.

In view of this, the scope of discussion in this article is established: only protocols with cash flow operations, like Aave/Curve, are likely to attempt new crisis management paradigms, and the reason is not complicated—maintaining protocol operation is profitable for all parties involved.

Protocol Stakeholders: Who is Responsible, Who is Acting

“The Exit Moment of Old DeFi”

As Aave was breached, the relics of DeFi Summer 2020 were almost completely destroyed, and the security of DeFi is no longer a theoretical optimum, but faces numerous real-world tests.

All of this happened while DeFi had not yet reached the mainstream market; Sky accepted Aave's risk-hedging funds, which was merely an internal game.

External institutions can only increase fear; if the token economics are overtaken by AI and DAO governance is effectively taken over by project parties, then DeFi or blockchain has no narrative subjectivity.

Yet amidst the crisis, there is opportunity; the Aave incident gives us confidence to reconstruct the narrative of DeFi, and after the Kelp DAO explosion, five narratives emerged in the market:

Bad debt distribution: EF, LayerZero/Kelp/Aave Umbrella/Aave DAO, Arbitrum

Responsibility allocation: LlamaRisk (Chaos Labs escaped timely), Kelp, LayerZero, Aave DAO

Liquidity: moving to Sky/Spark and many small lending protocols, the impact on DeFi in terms of capital is limited, but significantly large in terms of confidence

Technical design: monolithic vs modular (Aave vs Morpho), single token ($USDS) vs multiple tokens

Industry self-rescue: Aave founder Stani collaborated with various protocols vs CZ & Binance after FTX vs Morgan & various government crises

The discussion about the first four narratives is prolific, but for how the industry can rescue itself, most still remain in the binary opposition of socializing losses and bailouts. However, in my view, Aave's debt restructuring and Curve's attempt at "debt tokenization" are more interesting.

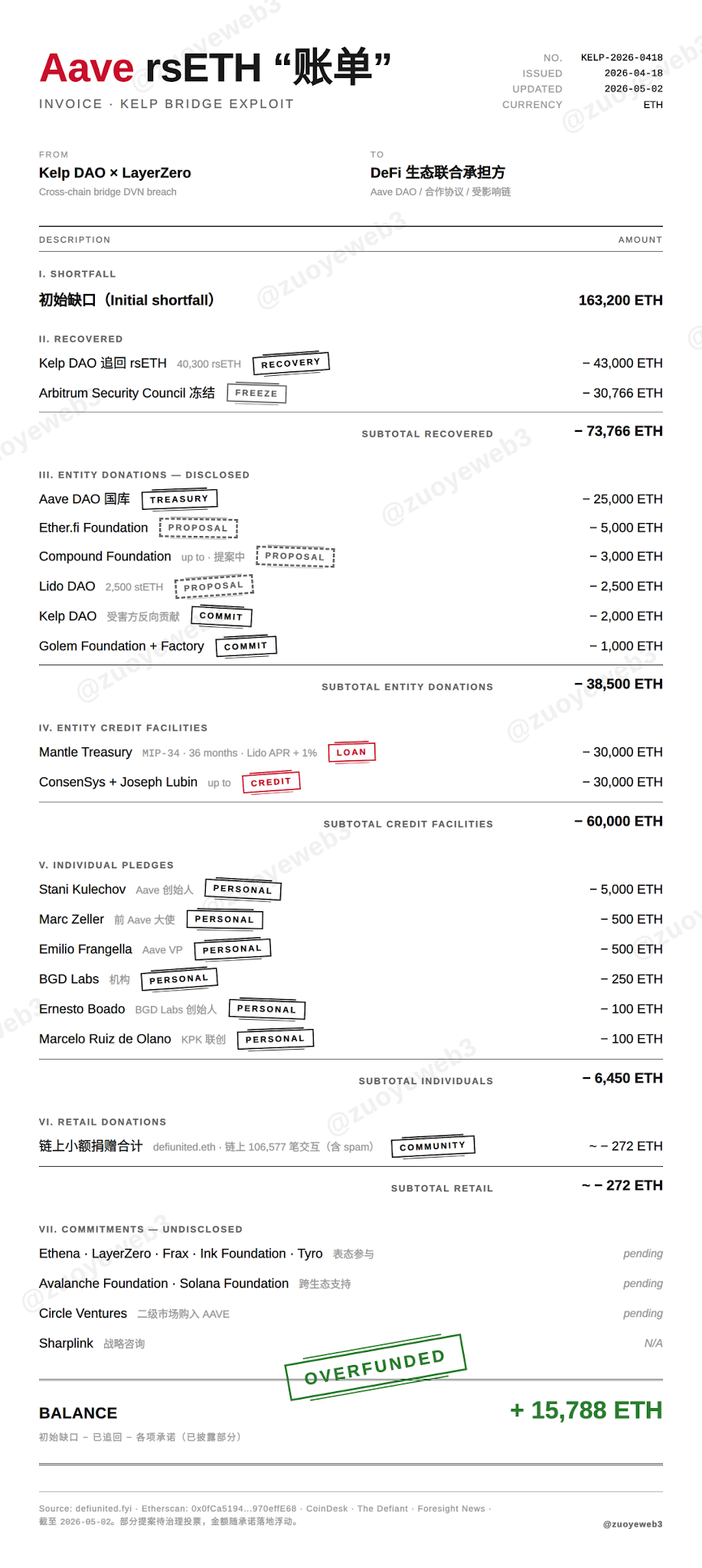

Image description: Aave debt restructuring

Image source: @zuoyeweb3

If we look at the responders to Aave DeFi United, they can mainly be divided into three categories: stakeholders of the Aave protocol, stakeholders in the LRT industry, and those related to ETH overall.

In terms of absolute amounts, retail donations are relatively small in proportion; the various protocols' recognition of donations and liabilities “reviving” the Aave market is not surprising, as Aave is in an absolute core position in the Ethereum ecosystem, and if the LRT protocol stands by, a drop in ETH prices would also threaten its own security.

US debt is not a debt, it’s a tax on the world; Aave's bad debts being "externalized" is draining the industry, leveraging its own industry position, posing potential threats to $ETH and LRT protocols.

But more importantly, this crisis only affects the protocol layer, not the retail side, nor does it impact the fundamental of $ETH, which hasn't affected the price of $AAVE either.

All the panic will reflect on prices; it can be said that Aave users have already separated from the retail image, and it’s purely the game of large holders.

This is Aave's core advantage of linking protocols; as long as a few large holders do not flee, and external protocols do not impact it, Aave's fundamentals are merely the daily changes in TVL, if the comparison is not obvious, one can think of how Binance magnified the crisis for Hyperliquid, the most typical case being $JELLYJELLY.

In Aave, with its industry position posing as JPMorgan, Stani is indeed "coercing" the industry to provide Aave with a lifeline; however, under the silence of Vitalik and the proactive selling of tokens by EF, Stani has already done enough.

He even set an example for the industry; the real crisis isn't about technology, but about liquidity among various protocols, which indeed reflects the scarcity of on-chain retail investors while providing a reference for the industry.

Prior to this, protocols could only shut down, and tokens must go to zero, allowing creditors of the protocol some hope, keeping the interests of creditors and token holders aligned.

For instance, Mantle issued a loan of up to 30,000 ETH to Aave, which Aave used its own tokens valued at 11 million dollars as collateral, and Mantle would also receive Aave's protocol income for repayment while locking in returns with a Lido staking rate +1% premium.

In this small "triangle debt", the interests of $AAVE holders, Aave DAO, Mantle DAO, and $MNT holders are re-bound, and Mantle increases its influence within the Aave system.

Since Friedman proposed the principle of "maximizing shareholder interests" in the 1970s, coupled with the Reagan administration allowing stock buybacks, tokens are seen as the secret to aligning interests between protocols and holders.

This secret is still effective today. Sky really distributes 100% of national debt yields to $sUSDS holders; this secret has turned against its own, with Stani and Curve founders profiting by selling tokens and distributing DAO income.

However, as the protocol grows to a sufficient scale, this token constraint brings new vitality. The new projects in Curve's ecosystem are not being accepted by the market; after Stani left Aave and remained idle, he ultimately chose to regain control.

A person cannot replicate their successes, even if they were once incredibly glorious.

The Rise of a Third Way

“We tend to overestimate the short-term effects of a technology, while underestimating its long-term effects.”

Stani is not accountable to $AAVE (maximization of shareholder equity), nor to Aave DAO (public governance system), but to the Aave brand and "capital value", which is harsh, but that is the future, and even one with Sky's dual face, the token is just a parameter adjuster.

This does not contradict what was previously mentioned; traditional relief or socialization cannot simply correspond to Aave. Essentially, Aave uses its expected cash flows to replace the current protocol liquidity.

Through the token mechanism, with reference to the Mantle case, various protocols will ultimately let holders profit; programmatically, proposals through the DAO mechanism also provide legitimacy.

In traditional finance, socialized losses come with privatized profits, with end users bearing the consequences, yet having no hope of sharing gains.

Image description: DeFi Debt Tokenization Methods

Image source: @zuoyeweb3

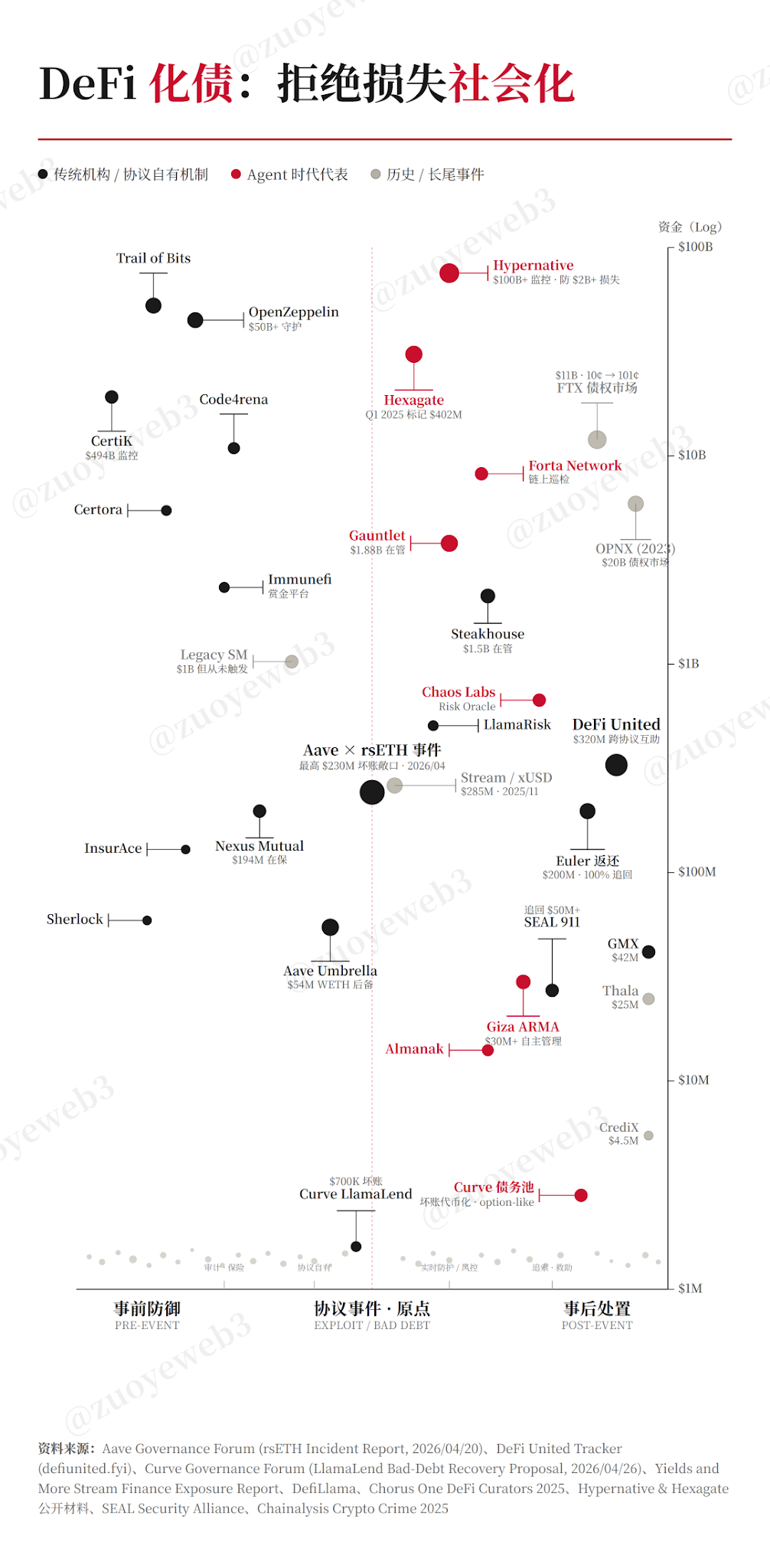

If we look at the management of bad debts in the entire DeFi domain, it is part of the post-event process, starting with the operation of the protocol, with prior auditing, security measures, etc., and post-recovery, restructuring, and other steps.

Compared to the lengthy processes and high fees in traditional finance, like the handling of FTX debts, DeFi is now effectively practicing at various stages.

April 2026 saw frequent crises, from Drift at the beginning of the month to Kelp at the end, but the purely code-level bug cases are becoming fewer, with more being "targeted human" social engineering attacks, at least partially validating the effectiveness of code audits.

However, insurance mechanisms have not become mainstream choices; Nexus Mutual's coverage amounts to only about 200 million dollars, which is negligible compared to DeFi TVL.

In dynamic protocol protection, AI/Agent has already been applied, with Hexagate, acquired by Chainalysis, marking 75 addresses of high-risk assets on-chain worth 400 million dollars back in Q1 2025, and can provide 18 hours advance warning when Venus Protocol is attacked.

However, the operations of Curators like Re7 are noteworthy; before the $xUSD incident, it had already noted abnormal risk control indicators, but under the incentive of “raising APY”, ultimately chose to approve continuously until the incident occurred. This is similar to social engineering attacks; human factors remain the most unstable element of the entire process.

As of now, "human + model" has become the mainstream in the industry, with modeling capabilities increasing daily, while human factors could tip the balance.

Before the concept of agents (Agent) became popular, in 2022, Gauntlet built Agent-Based Simulations, modeling different roles, such as borrowers, liquidators, LPs as Agents, to simulate performances under different environments, starting as a technical service provider for protocols like Aave / Compound, and expanding into standard Vaults in the Morpho era.

A skilled warrior does not boast great achievements; today’s risk control has already entered real-time status.

In the era of AI Agents, Chaos Labs, which fled from Aave, is another typical representative; through training on historical crypto data, it simulates security events under more realistic environments and has launched multiple Agent workflow projects.

Each Agent is responsible for a single parameter, such as supply limits, and ultimately combines into a modular product, complemented by an optimistic execution mechanism, allowing humans to retain control over it.

Image description: Agentic Finance Framework

Image source: @chaoslabs

Its latest development proposes a five-layer Agentic Finance framework, deepening Agent capabilities layer by layer from data reading → analysis assistant → restricted operation → decision execution → self-management, with security and risk control embedded within.

In the AI era, we need to rewrite the DeFi security mechanism; on the economic front, Curve provides another attempt—debt tokenization.

In the 10·11 event, Curve's LlamaLend accumulated 700,000 dollars in bad debts, which is not a large absolute amount, but its team proposed a "debt tokenization" mechanism. Lenders can exit bad debts at market prices, selling at a discount to obtain liquidity, while buyers receive current "loss position" representative tokens; if CRV prices rebound, they earn the price difference; if CRV prices remain unchanged, they lock in current earnings.

However, from the discussions of DAO proposals, user acceptance is limited, primarily due to skepticism about CRV price growth potential and the sources of initial transaction liquidity; referencing the Curve team's past operations on Yield Basis, there’s a high probability they will mint new crvUSD to provide initial liquidity.

But the idea is sound; the debt tokenization market is indeed more profitable than insurance, as long as the basic fundamentals of the protocol are good, maintaining its long-term profitability of operation will be more beneficial than direct shutdown.

As Agents become increasingly powerful, rewriting DeFi is already an ongoing process, with the number of Skills and Agents increasing daily, but the economic models equipped for humans like Tokens and DAOs are still in decline, which is also a technical debt that Agents must face.

Conclusion

“Aave exceeds Binance, but is still far from JPMorgan.”

If you feel guilty about being engaged in DeFi, then consider this: during the Great Depression of 1932, the head of Morgan suggested that the New York working class donate their wages to save the capital giants.

If you don’t believe that on-chain is the future of finance, then Morgan can retain his seat on the NYSE to save transaction fees, yet long-term avoids stock trading to improve capital efficiency.

The essence of finance is intermediation; $AAVE successfully moves towards large holders, retail investors no longer need to worry about Stani playing Aave protocol to death, but should rather consider opportunities for humans in the age of Agent takeover in DeFi.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。