Written by: danny

This article aims to inform all project parties that it is not only high control (control over 96%+) that can attract and bring liquidity; a serious builder can carve out their own path in the crypto bear market as long as they make good use of the inertia of mechanisms. Trading is not done just to chase scores? For a little airdrop? It is done for profit. Some use chip structure (control over chips), some engage in narrative manipulation, some seek VC endorsements, some find market makers, and this article tells you:

Using Mechanisms

Every year, $300 million to $800 million flows from project parties to market makers in the crypto space, hiding in a contract called token loan + call option. This article breaks down the financial principles behind that money, demonstrating how the funding generated by the structurally bullish perp market flows back to token holders through bidirectional lending agreements, and provides a specific self-rescue checklist for bear market project parties.

To begin with:

I am building a protocol that implements this set of mechanisms in the article (youcanshortit.com), which is already running. This piece is written by me as a builder to similarly anxious project parties—if you do not care about my stance, you can read the article as industry commentary; if you do care, you can directly skip to section six for the practical checklist.

1. What Project Parties Experience in a Bear Market

If you are a project party still seriously working in a bear market, your desktop probably looks like this:

The protocol is still generating revenue every day—perhaps accumulating $500,000 over 30 days, an 18% year-on-year increase; the fundamentals are good.

But the token price has been stagnant for 60 days, trading volume has dropped 70% from the TGE peak, and the order book’s ±2% depth is left with only a few tens of thousands of dollars.

Every few weeks, the exchange operations will always send a message: "Your token's 24h trading volume and depth have been continuously below the listing maintenance standard. It is recommended to supplement the market-making budget or change the market-making plan; otherwise, it will be delisted." (As a project party, I receive collection notifications for "protection fees" from exchanges regularly.)

You ask the market maker—that market maker to whom you lent 3% of the total token supply and signed a 12-24 month contract—his response is: "We are placing orders according to the contract. The market environment is not good; there’s nothing we can do. The stipulated depth in the contract may also be unsustainable. Please forgive us."

At 3 a.m., you stare at the dashboard, and only four sentences remain in your mind:

The protocol is clearly advancing. The coin price just doesn’t move. The exchange is chasing again. Can we only spend money to inflate volume?

In fact, there is not just one way out. But to see other paths, you must first clarify which path you are currently on.

2. The MM Contract You Are Signing Is Actually a Derivative

The instinctive action of project parties in a bear market is "to sign another market maker." This is a very costly action that most project parties are completely unaware of.

The most common structure of market-making contracts in the crypto space is called the Loan + Call Option Model—you "lend" 1-5% of the total supply of tokens to the market maker for a period of 12-24 months, with a call option clause in the contract: they can buy these tokens at an agreed exercise price at expiration.

Sounds good? You don’t have to pay a monthly fee; the coins are only "loaned" out. But this contract is, in financial terms, an extremely unfavorable derivative trade for you.

Assuming a TGE price of $1, lending out 10 million tokens (about 1% of the supply), an exercise price of $1.50, and a term of 12 months. The implied volatility of altcoins is usually 100-200%. Substituting into Black-Scholes, the present value of that call option is 30-50% of the nominal value of the underlying.

You unintentionally gave away a financial instrument worth $3 million to $5 million.

Worse, this figure is opaque and undisclosed; you don’t even know what the market maker is doing with your tokens? For small and medium projects in the entire crypto market, the total amount paid to that small circle of market makers through this mechanism is conservatively estimated to be in the range of $300 million to $800 million every year.

The more dangerous aspect in a bear market is—you have paid this hidden cost, yet the market maker may still shift blame during the contract period. "The market environment is not good," "the stipulated depth in the contract cannot be maintained," "please forgive us"—these responses you’ve probably heard. You paid $3 million to $5 million in exchange for a "please forgive us."

To break free from this structure, you must first understand what those scattered energies are.

3. Within the Perpetual Contract Structure Lies Money You Haven't Seen

Everyone in the crypto space has heard of perpetual contracts, but very few realize—there exists a structurally stable amount of money in the altcoin market that no one can continuously withdraw.

Perpetual contracts maintain anchoring with spot through the funding rate. Settlement occurs every 8 hours: when the perp price is higher than the spot, longs pay shorts, and vice versa. The theoretical baseline is 0.01% every 8 hours, annualizing to 10.95%—this is the level when perp is completely anchored.

Funding Rate (F) = P + clamp(I - P, max_rate, min_rate)

I (interest rate), generally 0.01%.

But actual funding is determined by market sentiment. Generally, the altcoin market is overall bullish (however, currently the market environment is predominantly bearish all day), with the funding rate typically above the baseline— a typical medium altcoin maintains a steady state annualized funding of 10-50%, with bullish sentiment pushing it to 80%+, and popular assets or major events temporarily spiking to 200%+ (for example, $alpaca).

After layering the altcoin market sentiment with the perp anchoring mechanism, the shorts can continuously extract funding from the longs at a rate superior to BTC and ETH by one or two orders of magnitude each year.

This is a structurally existing pot of money. The question is—who can take it?

Theoretically, anyone can arbitrage to obtain it through cash-and-carry (holding spot + opening short perp). Ethena’s sUSDe reached a peak of nearly $5 billion in TVL on BTC/ETH, which essentially executed this arb at scale. However, almost no one does this with altcoins—the spot depth is shallow, slippage is large, and there is a lack of complete prime brokerage services.

The key to unlocking this: enabling holders to become short themselves.

There already exists a large number of spot holders in altcoins—project treasuries, foundations, early investors, DAO treasuries, long-term holders. They hold a large amount of spot (delta = +1) and only need to open short positions in perp (delta = -1) to achieve delta neutrality and earn funding.

But opening a short position in perp requires USDT collateral, while they only hold tokens. Unless they sell coins for USDT—but selling would mean losing directional exposure, and they are unwilling to do so.

This is the specific problem the design needs to solve: allowing holders to open short positions in perp without selling their coins.

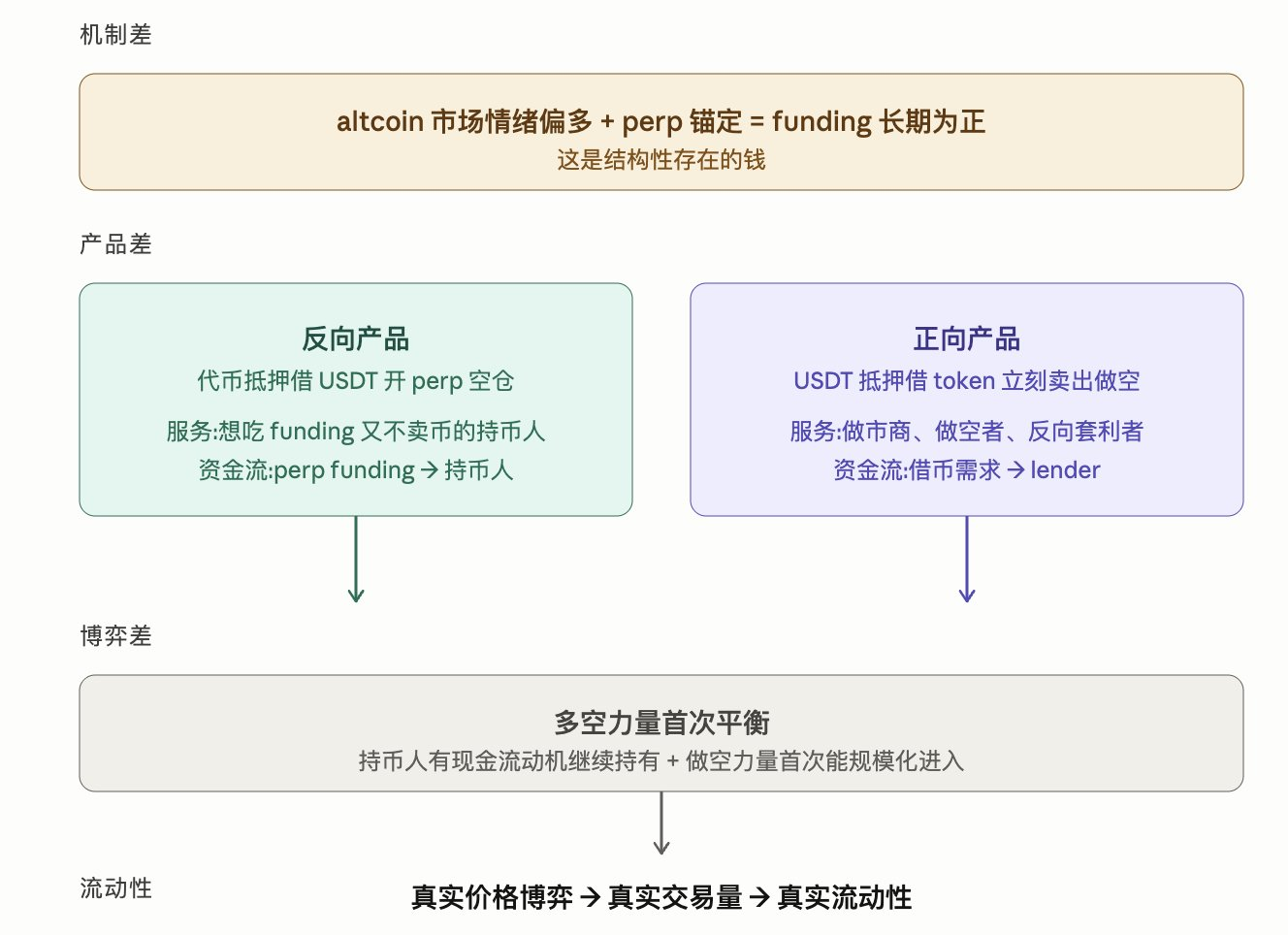

Reverse product: use tokens as collateral to borrow USDT to open short positions in perp (aka hedging operation).

Holders pledge tokens to the protocol → borrow USDT → use USDT to open short positions in perp.

The goal of this mechanism is (approaching) delta neutrality. Let’s calculate:

- Pledged tokens (still owned by holders): delta = +1.

- Borrowed USDT and liabilities: delta neutral.

- Short positions in perp: delta = -1.

- Net delta: to achieve 0, the nominal value of the short position in perp must equal the value of the pledged tokens.

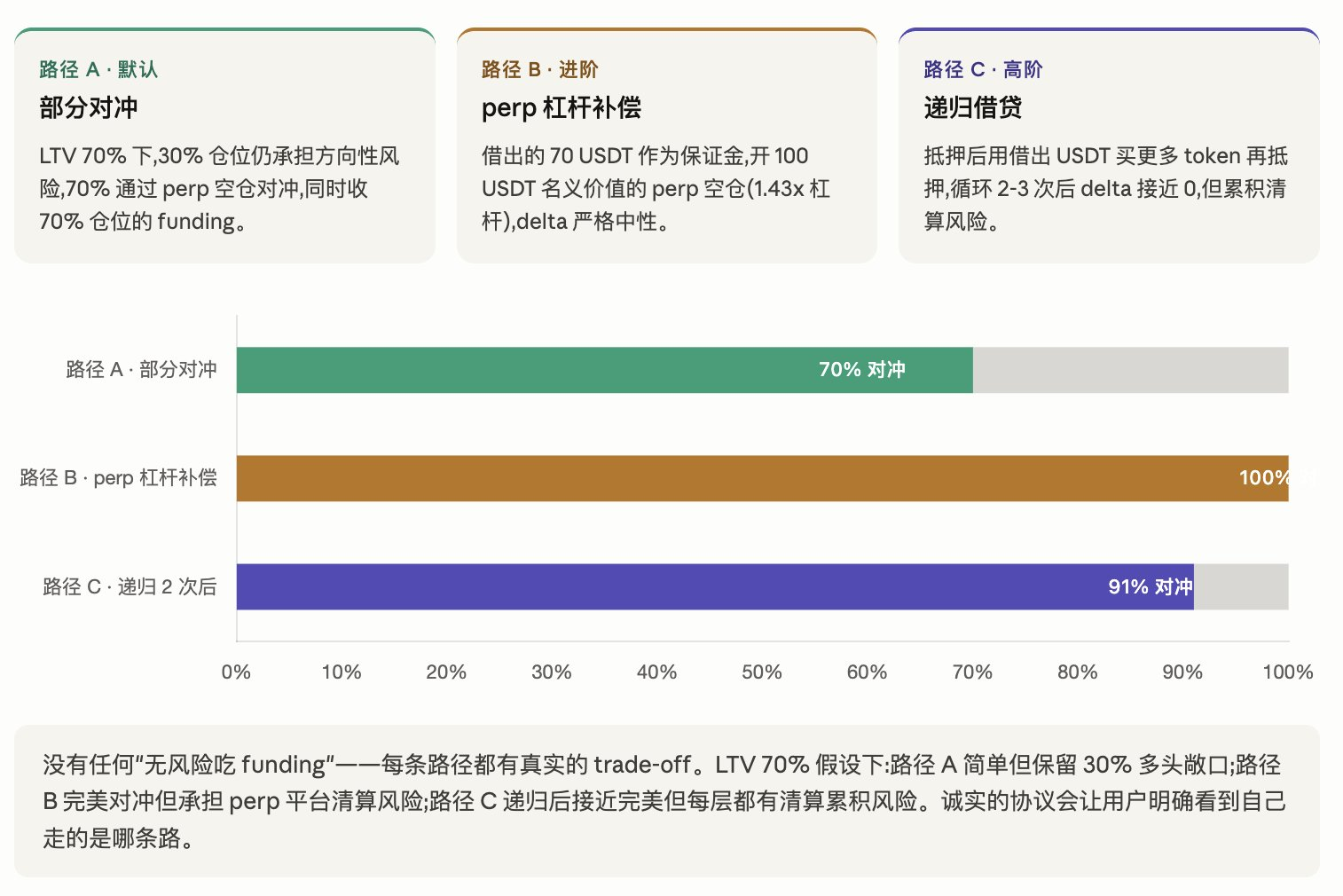

There is an engineering constraint: the collateral lending agreement cannot use 100% LTV (there's no liquidation buffer). A typical LTV of 60-80% means that pledging $100 in USDT equivalent tokens can only borrow $60-$80 in USDT. The direct result is—under single pledge conditions, holders will preserve 20-40% of directional exposure.

To approach true delta neutrality, there are three engineering pathways:

There is no such thing as "risk-free earning funding"—every pathway has genuine trade-offs.

No matter which path you take, the core financial phenomenon remains—altcoin holders can for the first time generate cash flow without selling coins.

Reversing is only one side; there must also be a forward aspect.

The reverse product solves "holders earning funding." But the structural counterpart in the altcoin market is the absence of shorting power—there are only two paths for shorting altcoins (opening short positions in perp and facing funding losses, using CEX lending platforms that are closed to retail), resulting in a naturally insufficient shorting capacity.

Design of the forward product:

USDT collateral → borrow tokens → immediately sell (establish a short position in spot).

This serves three types of clients:

- Market makers hedge their perp long inventory (passively accumulated). Market makers cannot hedge their perp long positions with short positions (funding becomes self-circulating); they must go short in spot, hence they must borrow tokens to sell.

- Directional shorters borrow tokens to sell, betting on a price drop.

- Reverse cash-and-carry arbitrageurs borrow tokens to sell + open perp long positions to earn negative funding (when funding is below zero).

Case study:https://x.com/agintender/status/2050125087320490227?s=20

The commonality among these three types of clients is "borrow and sell immediately"—this is entirely different from "borrow and hold." Lenders in the token borrowing market earn borrowing interest from lending tokens, driven by the genuine borrowing demand from these three types of clients.

Bidirectional Product: Closing the Financial Mechanism Loop for Altcoins

Combining both sides—

Poor mechanism: altcoin bullish sentiment + perp anchoring = funding remains positive long-term.Poor product: bidirectional agreements allow for two types of delta arbitrage to execute at scale for altcoins for the first time—reversely allowing holders to earn funding, and positively bringing in shorting power.Poor gaming: the entry of shorts + the cash flow motivation for holders to continue holding = balanced long and short forces for the first time.Liquidity: balance between longs and shorts → real price gaming → real liquidity.

Every interest payment has a clearly defined financial source—funding from the reverse product comes from the funding rates between perp longs and shorts, while interest from borrowing tokens in the forward product comes from borrowing demand premiums. These two product funds are independent, but both are driven by the same force: the bullish sentiment in the altcoin market.

The most desperate moment for project parties in a bear market occurs when protocols are profitable, the coin price remains still, the order book is empty, and market makers are perfunctory. The root of this despair is not that the market dislikes your project, but rather that there is no mechanism to aggregate the scattered financial energies in the market to your token.

The token loan + call option model promised to do this but failed—market makers received $3 million to $5 million in hidden options, yet they had no incentive to activate the market during a bear phase.

The new mechanism requires no intermediaries—it directly leverages the perp algorithm, altcoin sentiment, market maker demand, shorters' motives, and holders' yield desire, allowing the five driving forces to converge naturally through bidirectional products.

4. What This Means for Project Parties

Specifically in terms of profit—

Forward pool deposits: self-driven period lender annualized 3-8%, cold start period including token incentives 15-25%.

Inverted product collateral: typical steady state 10-30% (depending on funding level, LTV, USDT borrowing cost, engineering path), peak funding 40%+.

A project with a $100 million FDV activates 10% of its inventory ($10 million worth of tokens) through a combination approach, potentially generating $300,000 to $1.5 million in "passive cash flow" each year. Over three years, this amounts to a round of strategic financing.

To be honest—this yield is not entirely comparable to stETH. StETH comes from PoS staking, providing stable returns at the infrastructure level; the yield from the reverse product depends on market sentiment, which is volatile and could approach zero in deep bear markets.This is a tool that transforms token holders from "fully naked longs" to "hedging to reduce volatility + earning funding," not a risk-free yield.

This is also beneficial for market makers (especially wild MM and arbitrage traders)—they no longer need to use token loan + call option channels to claim tokens; they can directly borrow tokens from the forward pool and pay at market rates. But there’s a trade-off: in the traditional model, market makers did not need to lock USDT as collateral; under the new mechanism, a 60% LTV collateral is required (hedging $1 million in perp long inventory requires $1.67 million in USDT collateral). The transition will be gradual, weighing according to funding structures—this article does not assume all market makers will switch overnight.

The most important aspect is that through multi-party gaming, liquidity and trading activity can be stimulated, and this liquidity and trading opportunity are organic, driven by underlying logic and interests, rather than relying on subsidies and incentives.

The entire market logic has been turned on its head: previously, project parties paid to have market makers "use" their inventory; now, demand parties in the market are paying to "borrow" project parties' inventory.

5. Cold Start Requires Real Money

Informed project parties will ask—since this mechanism is so good, why has it not been realized in the past decade?

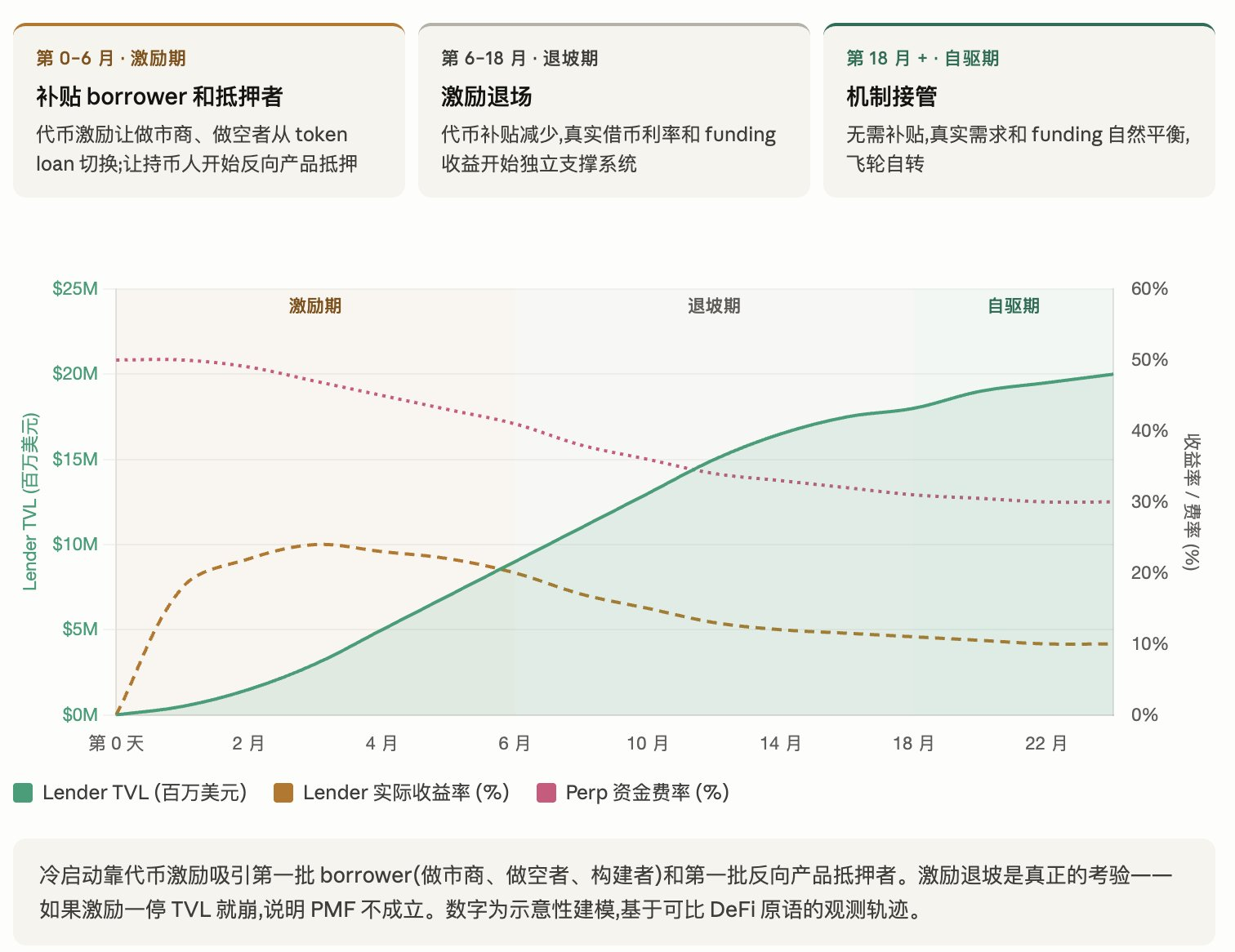

The answer is that cold starts are too difficult. Any lending protocol faces the chicken-and-egg problem: lenders won’t come first (utilization 0, earnings 0), and borrowers won’t come first either (no tokens in the pool). Compound relies on COMP, Aave on AAVE, Curve on CRV—every successful lending market starts with real early-stage subsidies.

However, cold starting this market has a special path: while lenders and traders do not need subsidies, the first batch of borrowers and first batch of pledgers do require subsidies.

Dear project parties, you are the first batch of pledgers.

The forward pool attracts early borrowers by allowing token incentives to leverage borrowing rates significantly below market levels, enticing market makers, arbitrage traders (giving them incentives to switch), and shorters (to establish positions at lower rates), as well as builders (to develop products based on the pool).

The reverse pool incentivizes altcoin holders via protocol tokens to be willing to take on liquidation risks and open short positions in perp to earn funding.

Once the first batch of borrowers and pledgers enters the pool, the forward pool’s utilization rises, boosting lender earnings, while the reverse pool generates real funding earning data. Only at this step will "holders see yield and naturally flock in" truly happen—because the yield is no longer a promise, but a fact proven by real demand and real funding.

The entire cold start logic:

Token incentives attract the first batch of borrowers + pledgers → real demand and funding boost lender earnings → lender yield brings retail capital in → funding pool scales up, incentives taper off → the market enters a self-driving state.

This path has been traversed by Compound, Curve, GMX, and Hyperliquid—it essentially dilutes early tokens for later protocol scale. If after incentive tapering the flywheel can be maintained, PMF is established; if the incentive ceases and TVL collapses, it indicates that market demand was insufficient from the start, which is not what this mechanism aims to do.

The significance for project parties is: you cannot wait for a "perfect protocol" to emerge. What you can do is participate in the early cold start phase and enjoy the complete yield curve from cold start to self-driving period. Early effective yield is far higher than in the self-driving phase—this is the "original bonus" of the cold start period. Additionally, do not subsidize trades; instead, subsidize the mechanism.

6. Specific Action Checklist for Project Parties

Checklist 1: Review Your Existing Market-Making Contracts

Open the contract signed with the market maker: how many tokens did you lend out (usually 1-5%)? What is the exercise price? What is the duration? Calculate the embedded option value using Black-Scholes (assume implied volatility of 100-200%)? How has the market maker performed in a bear market?

If you have already incurred $3 million to $5 million in hidden costs but received a "please forgive us"—you need to reassess the actual returns from this collaboration.

Checklist 2: Evaluate the Yield Potential of Your Inventory

Treasuries, vesting pools, DAO treasuries, early investor shares—add these numbers together. You will likely find that you hold a large amount of tokens that have been idly generating zero returns for a long time. These can be activated in two ways: depositing into the forward pool to earn borrowing interest (self-driving period 3-8%, cold start period 15-25%), or pledging them in reverse products to earn funding (steady state 10-30%, peak 40%+).

Checklist 3: Identify Truly Usable Protocols

- Do they offer bidirectional products (forward token borrowing pool + reverse token pledge borrowing USDT to open short positions in perp)? Just having the forward pool is incomplete, as it cannot allow perp funding to flow to holders; just having the reverse is also incomplete, as it cannot bring shorting power into the market.

- How is delta neutrality achieved in the reverse product?? Is it purely partial hedging, or does it use perp leverage to achieve perfect hedging? Honest protocols will clearly communicate their engineering paths, rather than vaguely promising "risk-free earning funding."

- Are borrowing rates and liquidation lines linked to perp funding and token volatility?

Checklist 4: Assess Entry Strategy for the Cold Start Phase

What is the FDV of my token? How much does activating 1-3% of the inventory amount to in dollars? Tokens borrowed from the forward pool to be sold for shorting vs. pledging in the reverse pool to open short positions in perp—what are my respective psychological expectations for these two states? Early yield might be high, but it carries early protocol risk—am I comfortable with this risk-reward?

Checklist 5: Renegotiate with Your Market Makers

Regardless of whether you eventually participate in the open market, you should renegotiate the contract. New leverage:

- "Your hedging no longer relies on my tokens."

- "Our contract should be retainer + performance bonus, not token loan + call option."

Just having this alternative option greatly strengthens your negotiating position. This is a minimal-cost step for self-rescue during a bear market—merely changing the contractual structure could save millions of dollars in hidden costs annually.

7. After the Bear Market

The bear market will eventually pass. The question is, in what posture will your project enter the next cycle?

By the old path—continue signing token loan + call option, continually sending hidden options to market makers, continue receiving "please forgive us" during bear markets, and continue to be harvested for the upward dividends in bull markets.

By the new path—your token inventory generates cash flow independently, with market depth supported by genuine shorting forces and arbitrage demand instead of being maintained by paid services. When the next bull market with soaring funding arrives, the tokens pledged in your reverse products earn significantly increased funding, while the activity of market makers and shorters in your forward pool rises synchronously—your tokens will enter a positive cycle: poor mechanisms drive poor products, poor products drive poor gaming, poor gaming drives liquidity, liquidity drives a new wave of holders entering.

One of the deepest lessons from the crypto industry over the past decade is—all financial businesses driven by personal relationships will ultimately be replaced by open, mechanism-driven protocols. Uniswap replaced some market makers, Aave replaced some lending platforms, Hyperliquid replaced some centralized perps. Each time a substitution occurs, the industry proclaims "institutions have real value." Each time, institutions ultimately have to adjust their positions.

Token loan + call option is the last bastion of such institutional privilege. It has existed for ten years because no one has earnestly filled in the two foundational infrastructures of "open borrowing + reverse product." Once filled, market-making capability will be decentralized from ten institutions to anyone holding tokens.

But the true significance of this goes beyond "breaking market makers." It transforms the largest class of idle assets in the crypto market—long tail altcoin inventories—into yield-bearing assets. It allows "holding" for the first time to generate cash flow. It turns the treasuries of projects, the reserves of foundations, the shares of early investors, the treasuries of DAOs, and the wallets of long-term holders from silent book value into active productive capital.

Self-rescue for project parties in a bear market is essentially not about cutting costs—it is about opening up sources. Retrieving the money you previously sent away, activating the previously idle assets, allowing the funding generated by the structurally bullish perp market to flow to your token holders through reverse products, and letting the genuine shorting and hedging demand in the market pay for your token inventory through the forward pool.

At 3:47 a.m., the project party staring at the dashboard should know—that the protocol making money should inherently enable the tokens to make money as well.

Only over the past decade has no one turned this switch on.

Ultimately, it is not only high control (control over 99%) that can attract and bring liquidity; serious builders can also utilize mechanisms' inertia to carve out their own paths.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。