Technology has won, the platform has profited, venture capital has exited, and only you, the holder of tokens, remain at the bottom of the K-shaped divergence.

Written by: Vaidik Mandloi

Translated by: Saoirse, Foresight News

A well-known influencer in the crypto circle called ThreadGuy. In 2021, he became famous for teaching people how to trade NFTs. Now he lives in an apartment in New York, with a barrel of crude oil next to his desk, regularly trading pharmaceutical stocks and commodities on the Hyperliquid platform. A few weeks ago, he invited Cobie to join a live stream.

Cobie, a veteran in the crypto space since 2012, previously sold the project Echo to Coinbase for $375 million and is now working full-time at Coinbase. When ThreadGuy inquired about the current state of the crypto industry, he presented a K-shaped divergence in the industry.

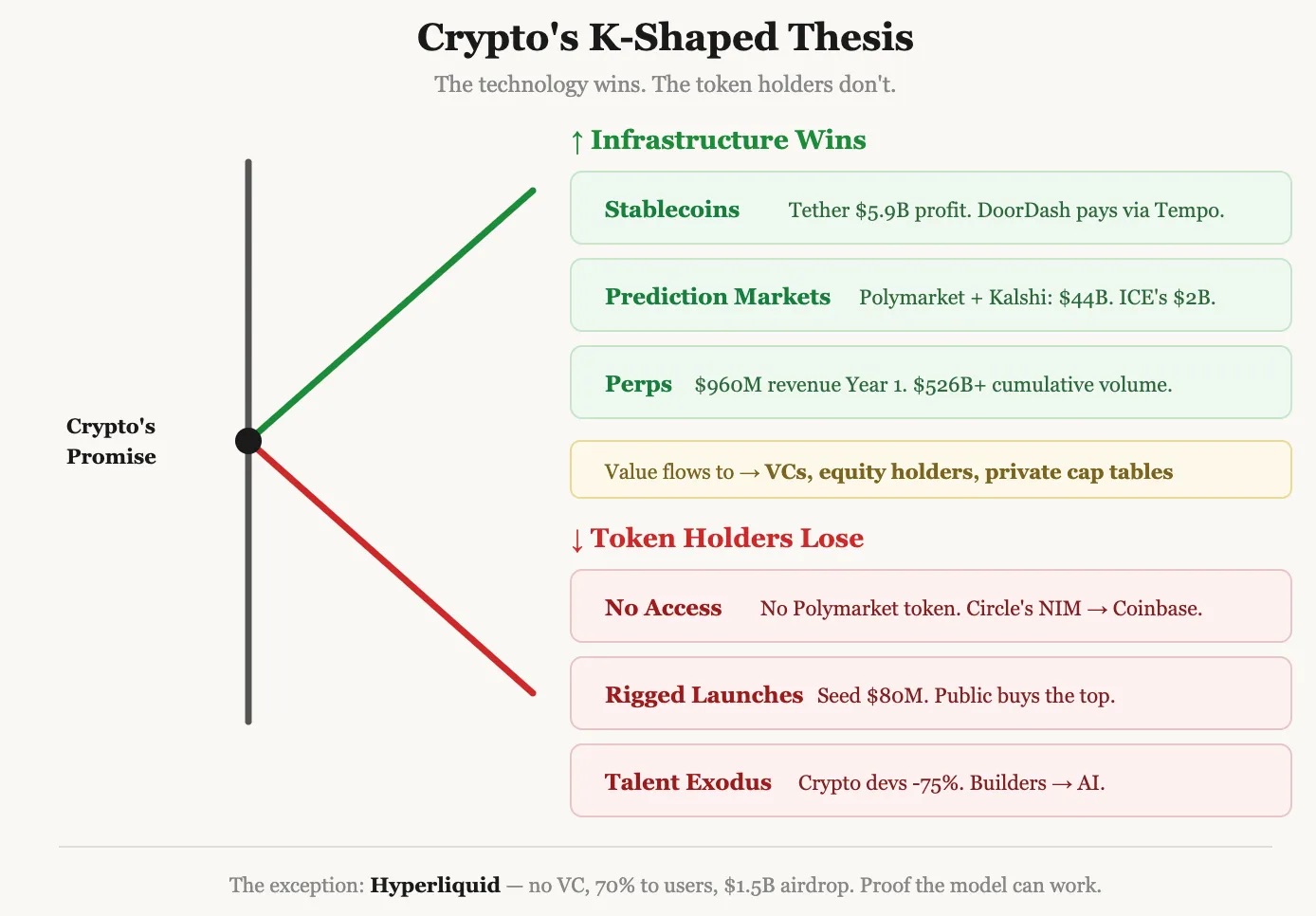

He said: "The crypto world is experiencing a strange K-shaped divergence. There are unprecedented success stories emerging in the industry, far exceeding previous years, but these achievements are not reflected in the prices of crypto assets available to ordinary investors."

This statement has lingered in my mind because he is absolutely right.

Polymarket and Kalshi, the two major prediction markets, have formed a duopoly in the industry with a scale of up to $440 billion; stablecoins are widely used for payment of wages to gig workers, and DoorDash now pays drivers through the Tempo platform; Hyperliquid has built its own underlying public chain, with on-chain trading volume surpassing most centralized exchanges; Trade XYZ can even predict the opening price of US stocks on Monday with an error rate of within 50 basis points.

The original vision of cryptocurrency was to achieve the flow of funds without banks, market making without brokers, allowing anyone to trade any asset anytime and anywhere. By the standards of all the skeptics back then, the crypto industry has now fully achieved all of this.

However, ordinary investors who initially believed in crypto and held various tokens have hardly reaped any dividends from it.

Ordinary investors cannot buy shares in Polymarket or Tempo; although Circle has gone public, half of the net interest margin generated by USDC must first be given to Coinbase as channel distribution revenue, with shareholders only able to share in the remaining profits.

The platforms have made substantial profits, but token holders repeatedly find themselves at a loss.

This is the K-shaped divergence in the crypto industry. After further research, I found that this has long ceased to be an issue unique to the crypto circle.

Where has the value really flowed?

Let's start with stablecoins, which are the true pathway for the crypto industry to successfully match product markets.

It is estimated that Tether's profits will reach $10 billion in 2025, with only about 100 employees, achieving per capita profitability that exceeds most companies worldwide. Circle has successfully gone public, with a market capitalization of $230 billion as of April 28.

In recent years, the total supply of stablecoins has skyrocketed one hundredfold, jumping from $6.8 billion in 2020 to over $315 billion today. The U.S. Treasury even predicts that the stablecoin market will exceed $2 trillion by 2028.

On the crypto infrastructure, a true global financial system is being built. But for ordinary token holders, they have no economic connection to this trillion-level dividend.

Tether's profits go to corporate shareholders, while Circle’s earnings flow to its shareholders and Coinbase; DoorDash pays drivers through Tempo, and the trading value is divided among the platform, businesses, and workers, entirely unrelated to the token holdings of ordinary people.

The same script applies to prediction markets.

Polymarket has transitioned from an obscure crypto experiment to a permanent reference data source for CNN, and The Wall Street Journal has included its data in news reports; Substack has directly integrated Polymarket’s functionality, allowing creators to embed real-time odds in their articles, turning every piece of information into a real-time data terminal.

The Intercontinental Exchange behind the New York Stock Exchange invested $2 billion at an $80 billion valuation; Kalshi won a legal battle against the U.S. Commodity Futures Trading Commission, expanding its business into fields such as economics, sports, and scientific research. By 2025, the total trading volume of the two platforms will reach $440 billion, with the highest monthly trading volume exceeding $100 billion.

This enormous value increase has not fallen into the hands of token holders at all.

Early venture capital firms, founding funds, and investors in Polymarket hold huge unrealized book profits. As a benchmark success project in the crypto circle, built upon crypto infrastructure and by insiders, it ultimately adopts a traditional equity structure, with all appreciation earnings snatched up by venture capital.

Some might say: Polymarket hasn’t issued a token yet.

Indeed, it may issue a token in the future. But even if it does, private capital has already set an $80 billion valuation for it. The window for ordinary early users to share in industry dividends closed imperceptibly while everyone was unaware.

If it never issues tokens, then the prediction market revolution touted by the crypto community for years, claiming to reshape the global information landscape, will have all its value entirely monopolized by the traditional equity system: venture capital funds the incubation, ultimately sold to institutions, with ordinary users having no on-chain ownership whatsoever.

Even in the decentralized finance (DeFi) field, it cannot escape this pattern.

The crypto industry has spent nearly a decade building DeFi infrastructure: lending protocols, automated market makers, perpetual contract exchanges, and stablecoin payment networks have all been perfected. The entire process was mostly open-source construction, relying on tokens to operate, all while facing regulatory crackdowns and restrictions.

Project builders faced extremely high entrepreneurial risks; early users, during an era where smart contract vulnerabilities could wipe out assets at any time, took great risks in actively providing liquidity and testing protocols.

Now that technology has matured, with stablecoins, on-chain trading, and asset tokenization all worked out, those coming to reap the dividends are no longer the builders and users who initially took risks to pioneer.

Replaced by established companies adhering to traditional equity structures: Stripe is planning stablecoin payments, PayPal is issuing its own stablecoin, and major banks are promoting asset tokenization on private chains.

These companies once merely watched the explorations of the crypto industry with a cold eye, waiting until the commercial model was validated before replicating and building their own closed ecosystems, with all economic gains going only to their own shareholders.

Industry dividends are being privatized. Tokens were originally meant to counterbalance this situation, allowing early participants to share in the value they created.

But the reality is: the truly successful projects either do not issue tokens at all, or the timing of token issuance is severely lagging and the valuations are inflated, with ordinary retail investors coming in only to become exit cash-out funds for early internal investors.

The Common Malady of K-shaped Capitalism

The K-shaped divergence theory of the crypto industry

This is no longer a problem unique to the crypto industry but a common pattern in global wealth creation today; crypto has merely replicated the social ailments it originally aimed to cure.

SpaceX started from scratch, with a private valuation skyrocketing to $1.75 trillion; OpenAI is valued at $852 billion, and Anthropic has also reached the $800 billion level. These three companies alone have created trillions of dollars in value increment.

In the 1970s or early 2000s, ordinary people only needed to invest in companies of the era like Apple, Amazon, or Google to share in the wealth dividends from corporate growth by directly buying stocks.

Believing in the future and gaining returns was meant to be the most fundamental social contract of capitalism, yet it has completely failed today.

These epoch-making giant companies maintained their private status throughout the phase of their fastest value growth, restricting entry qualifications to top-tier circles: Silicon Valley networks, fund-of-funds, and institutional funders contributing at least $50 million.

By the time SpaceX and OpenAI eventually go public, the stock prices will have already exhausted a decade of private compounded returns, leaving ordinary retail investors with no opportunity for early dividends.

The number of publicly traded companies in the U.S. has sharply decreased by 46% since 1997, from around 7,500 to 4,000. There are now over 1,400 unicorn companies incubated by venture capital, with a combined valuation of $5 trillion, all choosing to remain private for the long term.

In the past, companies went public to raise funds; now, giants can complete billion-dollar private financings through closed capital circles, granting them infinite extensions. By the time they finally IPO, the value pricing has already taken place in exclusive circles inaccessible to ordinary people.

Data also supports that this is not a baseless guess: from 1970 to 1990, the average annual return rate for IPOs was only 5%, far lower than that of mature publicly traded companies of the same scale.

Low float IPOs like SpaceX and OpenAI have a historical failure rate of up to 90%. Since 1980, among eleven low float IPO companies, the degree of underperformance compared to the market within three years exceeded 50%.

What remains for ordinary people is only one outcome: when the company's valuation is in the millions, you are not allowed to invest, but when it is valued at $1.5 trillion and goes public with fanfare, you are left to buy in at a high price, completing the cash-out exit for internal investors.

This is K-shaped economics: the upward dividends are monopolized by closed circles, while the downward losses are borne by society as a whole—sky-high IPOs, passively entering high-price index funds, soaring inflation, stagnant wages, with all the costs distributed to every ordinary person.

This is also the core reason for the continuous outflow of crypto talent.

Since early 2025, the amount of crypto code submissions has plummeted by 75%, dropping from 850,000 per week to 210,000; the number of active developers has fallen by 56%, leaving around 4,600. A large number of talents have shifted to the AI field: GitHub currently has 4.3 million AI-related code repositories, with the import volume of code related to large models increasing by 178% within a year.

From the perspective of K-shaped divergence, this trend can be fully understood: each round of wealth creation in the crypto industry—2013's altcoins, 2017's ICOs, 2021's DeFi and NFTs, and later meme coins—shares a common point where ordinary people can quickly make money.

Now, this atmosphere of wealth generation has shifted to the AI domain. Independent developer Peter Steinberger developed OpenClaw alone, eventually being acquired by OpenAI for billions of dollars. This is the wealth-generating allure that the crypto industry once possessed.

If you are a 22-year-old like me, planning your career for the next five years, the answer is obvious:

The crypto industry offers governance tokens starting at a valuation of $16 billion, which subsequently continue to decline; the AI track offers opportunities for teams of three to five people to develop intelligent agents that can hatch billion-dollar projects within just a year.

The root of talent exodus lies in the crypto industry gradually no longer distributing the dividends it creates. K-shaped divergence concentrates profits upward toward venture capital and equity holders, ultimately devolving into the very elite circles it originally intended to disrupt.

Where is the ideal of decentralization now?

In the face of dilemmas, where is the way out?

The predicament of the crypto industry is already quite clear: its technical capabilities are impeccable, yet early believers are unable to share in the industry dividends; the privatization of traditional market value has already infected the crypto industry, which was born to disrupt inequity.

Is there still a way to break the deadlock?

Cobie believes there is, and I fully agree. The only solution, which is also the unique weapon of the crypto industry, is—airdropping.

Airdrops can bypass all intermediary links and directly distribute project ownership to real users worldwide, accurately targeting the early stages of highest value. This is the original mission of airdrops.

Unfortunately, in reality, the vast majority of airdrops are mere formalities, devoid of substance. But there is a benchmark case that has proven this model to be entirely feasible and is worth everyone's reference—Hyperliquid.

Founder Jeff Yan led the team to build a bottom-line public chain from scratch, developing a perpetual contract exchange with stable, long-term operations, achieving a cumulative trading volume exceeding $4 trillion to date.

In distributing project ownership, the team allocated 70% of the total token supply to the community, without any venture capital, advisor shares, or exchange allocations.

All benefits were given to genuine traders: loyal users who use the platform long-term, transfer funds across chains, and continuously stress-test the protocol. Ultimately, 94,000 on-chain addresses shared a value of $1.5 billion in airdrops, with many ordinary people becoming millionaires overnight.

What’s most remarkable is that the users who received tokens did not thoughtlessly dump them for cash-out.

Because these HYPE holders are not mere speculative opportunists out to grab airdrops but are the core loyal users of the platform—those who trade most actively, have the largest amounts of capital, and value product experience, leading to long-term retention. They obtained corresponding ownership based on their contributions and chose to hold for the long term, adhering to shared beliefs.

The project team also set an example: in the first two months after token allocation, they only reduced their holdings by 20% (most likely to pay taxes), and the subsequent monthly reduction rate was compressed to 1%. Now, 97% of the protocol's revenue is used for HYPE token buybacks and burns.

Industry analyst Saurabh has thoroughly broken down its valuation logic: In 2025, Hyperliquid's trading volume is projected to approach $30 trillion, with revenue of $960 million, valued at only 10-13 times its revenue.

In comparison, the Chicago Mercantile Exchange has a price-to-earnings ratio of 25 times, the Intercontinental Exchange 23 times, and the Chicago Board Options Exchange 22 times. It approached nearly $1 billion in revenue in its first year of operation, with zero debt and no redundant labor costs; almost all fees are returned to token holders through buyback and destruction.

Hyperliquid has proven with strength: this path is feasible.

Share rights with users rather than capital; let genuine usage behavior determine the growth of value; bind the interests of builders and users to achieve mutual benefit and coexistence.

However, it must be admitted that Hyperliquid is ultimately the exception; the vast majority of airdrops fall far short of this standard.

Most airdrops on the market are merely a well-orchestrated performance: users pretend to use projects they are not interested in just to obtain tokens to unlock and immediately sell; the project parties know this all too well, and users are equally tacitly aware.

Everyone cooperates in this game, simply because once it is acknowledged that airdrops are nothing more than “high-priced tokens exchanged for customer acquisition costs,” there is no longer a way to tell fundraising stories in venture capital roadshows. 90% of tokens in the industry are fundamentally just tools for venture capital to cash out and exit, rather than being used to bind user consensus and distribute value.

Cobie's analytical data further strikes at the pain point: In the past, ordinary people could enter Ethereum's ICO at a valuation of $26 million, reaping returns of 7,500 times; whereas with new projects like Berachain, the seed round valuation is already $40 million, and the public listing occurs at the peak valuation.

Retail investors are immediately trapped, while early seed investors reap returns of 138 times.

Now, the industry faces a core question that is far more important than insiders might imagine: Is Hyperliquid a model that can be replicated across the industry, or merely a rare exception?

If it is a replicable model: More teams can delve into real products, escape the harvesting patterns of venture capital, and distribute ownership to true users. This will become the unique core value of the crypto industry—SpaceX cannot allot equity to onlookers, OpenAI cannot distribute original rights to every user, but crypto can, and there are successful precedents.

If it is merely a rare exception: then Cobie's K-shaped divergence theory will be thoroughly validated. Token holders will continue to be marginalized, top-tier developers will continuously shift to the AI domain, and ordinary people wanting to share in the crypto industry’s dividends will ultimately have only one route left: buying traditional stocks of Coinbase or Circle.

And this, precisely, is the outcome that crypto aimed to completely end from its inception.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。