Entering the perpetual contract market is much more difficult than a perpetual contract platform entering the prediction market.

Written by: Prathik Desai

Translated by: Luffy, Foresight News

The perpetual contract sector has already become an undeniable force in the industry. It allows participants to price trades as events approach, offering high leverage, round-the-clock access, and deep liquidity. Traditional exchanges are limited by fixed trading hours and cannot provide similar services.

A team of just 11 people has seized the pain point of 24/7 uninterrupted trading, making Hyperliquid the fastest-growing cryptocurrency exchange, with an annual revenue close to $1 billion.

In 2025, the average daily trading volume of perpetual contracts reached 7 times that of spot trading, seemingly becoming a gold sector with a long-term sustainable business model. Thus, following the trend to enter the market has become inevitable for the industry.

Just last week, the two major global prediction market platforms, Polymarket and Kalshi, announced the launch of perpetual contracts and cryptocurrency trading within hours of each other. Just months earlier, Hyperliquid had officially announced plans to launch event contracts.

The integration of perpetual contracts and prediction markets is an undeniable trend. Each platform aims to create a comprehensive exchange for all types of trading, aggregating traffic, funds, and leverage trading demands in one stop.

Saurabh recently stated on the X platform that Hyperliquid's entry into the prediction market could help it dominate the entire financial trading sector. But does the reverse logic hold true? Can Polymarket and Kalshi, entering the perpetual contracts space, replicate the same success?

Why are perpetual contracts important for prediction markets?

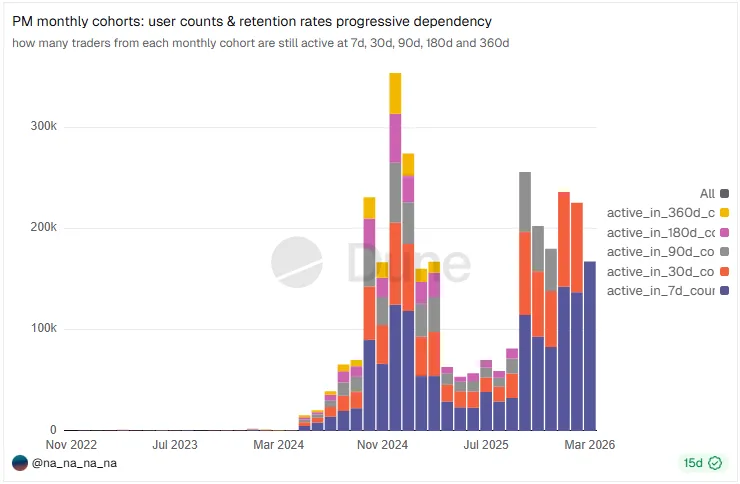

Prediction markets generally face the problem of low user retention, with business showing significant seasonality: trading volumes peak only during major events, such as the U.S. elections, the Super Bowl, and Federal Reserve meetings.

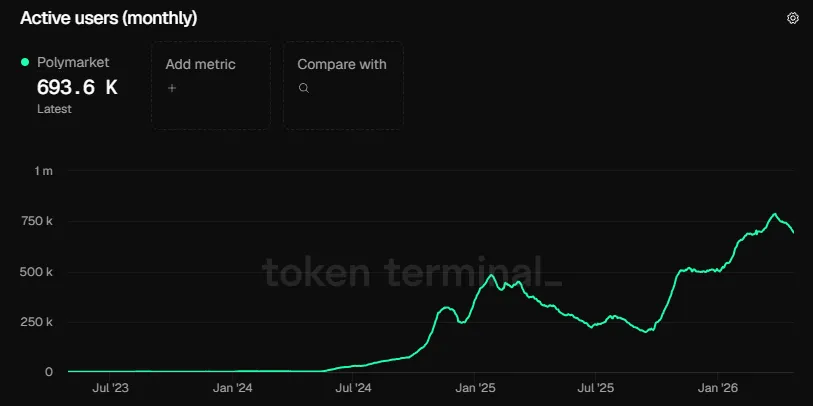

During the 2024 U.S. elections, Polymarket’s monthly active users peaked at 321,500; just three weeks later, the number plummeted by 25% to 245,000.

Due to various seasonal events, platform monthly active users fluctuate significantly. In January 2025, monthly active users surged to 500,000, but by September that same year, it fell below 200,000. This sufficiently reflects Polymarket's user retention shortcomings.

Dune data shows that since 2024, only 8% to 11% of the user base continues trading a year later, while about 75% of users will drop off within 90 days. Users only return during significant events and do not develop long-term dependency on the platform.

This is just part of the problem.

Another pain point for prediction markets: funds are locked until event settlement. In contrast, perpetual contracts fluctuate constantly in price, attracting user attention over the long term and maintaining continuous trading activity. From a business perspective, perpetual contract trading volumes are larger, and the proportion of fee income is also higher.

In 2025, the global nominal trading volume of perpetual contracts surpassed $60 trillion, while prediction markets were only at $28 billion.

Therefore, the extension of prediction markets into perpetual contracts is a natural evolutionary business logic. Any platform that can support a type of speculation demand usually extends to the next kind of similar demand, either by developing functions in-house or acquiring entities with relevant capabilities. Such cases are numerous: Robinhood expanded from stocks to options, cryptocurrency assets, and then entered the prediction market; Coinbase spent $2.9 billion to acquire Deribit to lay out the derivatives sector; Binance started with spot trading, extended to contract businesses, and then built its own blockchain ecosystem.

The traditional financial industry follows the same principle. Companies broaden service boundaries and cross-sell new products to existing users, bringing two core values: increasing revenue per user while hedging industry cycle risks through a diverse income structure.

In the early 1970s, as revenue from commodity futures at the Chicago Board of Trade (CBOT) continued to decline, it utilized a 4,000-square-foot lounge from its parent company to establish the Chicago Board Options Exchange (now Cboe). The two types of products could develop synergistically, relying on the same underlying infrastructure: risk management, clearing and settlement, and a network of professionals proficient in derivatives pricing.

However, there is still a long way to go to operate a perpetual contract platform successfully.

Barriers to the underlying infrastructure of perpetual contracts

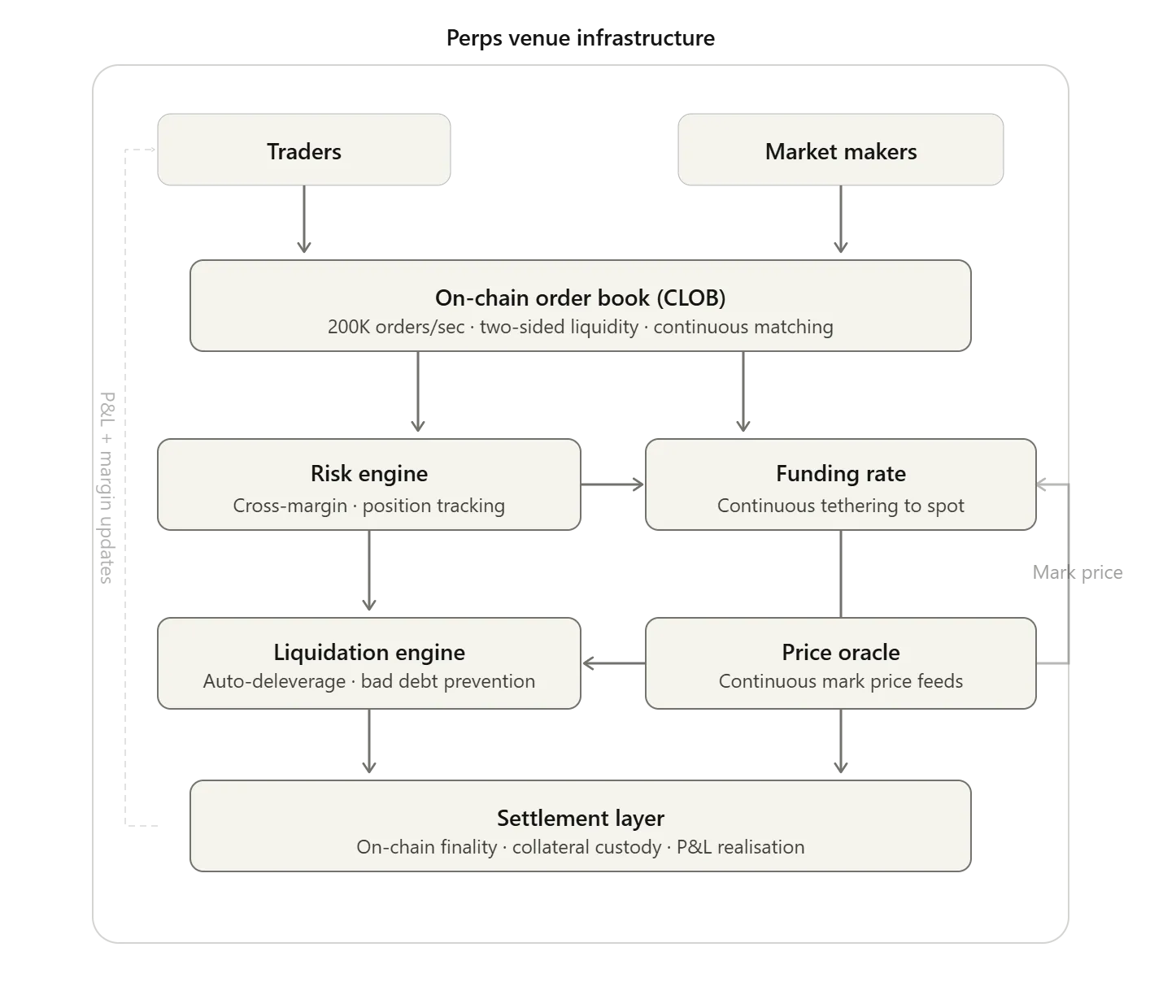

Running a perpetual contract exchange involves extremely complex systems, starting with liquidity.

Hyperliquid, leveraging its on-chain order book, can process over 200,000 orders per second; relying on a dual-sided market maker mechanism, its average daily clearing trading volume reaches $6-7 billion. If liquidity is insufficient, it will trigger significant price fluctuations, increase bid-ask spreads, escalate trading slippage, and make it easy for whales to manipulate prices.

Next is the risk engine, which is the core lifeline of all derivatives platforms. It tracks all positions in real-time and verifies margin rules for each order. In October 2025, as the market cap of cryptocurrency saw a sudden clearance of $19 billion overnight, Hyperliquid smoothly handled billions of dollars in clearing operations without downtime.

Furthermore, there is the funding rate mechanism, which anchors the perpetual contract price to that of the spot underlying asset. The system automatically settles small funding fees between long and short positions every few hours to maintain fair pricing.

Building the entire underlying infrastructure is not the biggest challenge for prediction market platforms, as they likely have what it takes to implement it. The real barrier lies in pressure testing and practical validation.

After completing the entire infrastructure setup, Hyperliquid underwent extreme practical pressure tests during events like the 10·10 cryptocurrency market clearance wave and the Israel-Palestine conflict, confirming system robustness before proposing event contracts through HIP-4.

On the other hand, Kalshi and Polymarket are taking a completely opposite path: originally operating prediction markets, they do not need the complex underlying architecture of perpetual contracts. Now they must face the already mature Hyperliquid, while their own systems have never experienced the practical pressure tests of high-frequency trading and extreme market scenarios.

Moreover, there are multiple adverse factors that make it much more challenging for prediction markets to reverse-enter perpetual contracts than for perpetual platforms to advance into prediction markets.

Hedging Synergy Effects

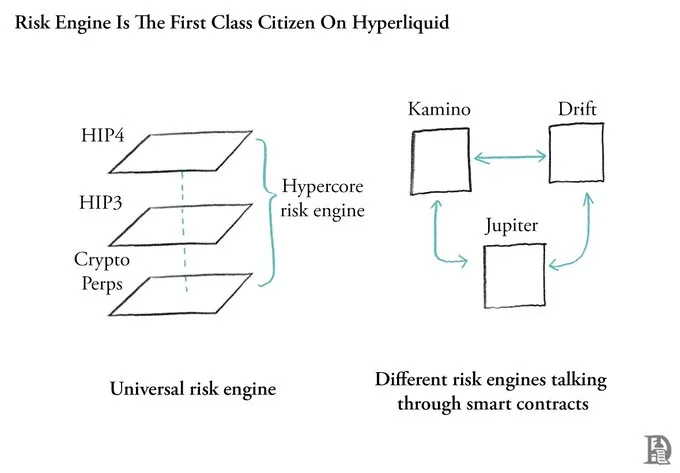

Within the Hyperliquid platform, the risk engine can uniformly identify users' positions across perpetual contracts, spot, and the soon-to-be-launched event contracts. Saurabh had previously provided detailed explanations while interpreting the HIP-4 proposal.

The system does not differentiate between categories; it unifies the accounting of all positions. The final decision on the liquidation line is based on the overall leverage level of the user and the cross-category margin-sharing ratio. All positions in spot, perpetual, prediction markets, etc., are combined to determine the required margin size.

Some may ask: don't general-purpose public chains like Ethereum and Solana have combinability? They do have combinability, but each application on a general-purpose public chain operates independently under its own smart contract risk engine, unable to communicate atomically with each other's position statuses. For instance, Kamino cannot perceive Pacifica’s positions, and Aave cannot synchronize Lighter’s risk control data. Each application fights its own battle, and establishing a unified risk control framework and a global risk engine would require massive multi-party collaboration and is extremely challenging to implement.

Hyperliquid's unified risk engine has a core advantage: the same capital can be flexibly reused across multiple trades on the platform, optimizing capital efficiency.

For example: a trader goes long on ETH with 5x leverage while being concerned about a potential change in Federal Reserve policy next week, so they buy an event contract for "Federal Reserve maintaining interest rates." The cost is $0.65. With a unified margin account, both positions share the same margin. If the Federal Reserve unexpectedly lowers interest rates, ETH surges, resulting in profits from the perpetual contract, while the event contract only incurs a loss of the principal; if the Federal Reserve maintains interest rates, the prediction contract profits, partially hedging the losses from the perpetual contract's withdrawal.

This also means that neither prediction markets nor perpetual contracts can only exist as simple add-on features. This inherent hedging value is the core significance of Hyperliquid's HIP-4 proposal. Ordinary traders will treat prediction market positions as risk insurance tools for their perpetual contract holdings.

In contrast, currently, with Polymarket and Kalshi, user funds are fully locked until event settlement. Unless the two major platforms establish cross-category margin-sharing between perpetual contracts and prediction markets, they will lose the key advantage of retaining traders. Currently, neither has announced related functions.

From the perspective of category structure and user profiles, there are additional hidden concerns about prediction markets entering perpetual contracts.

Over 80% of Kalshi’s monthly trading volume comes from sports events; in 2025, sports events accounted for over 40% of Polymarket's volume as well. Such sports events are challenging to adapt to the continuous pricing mechanism required for perpetual contracts, indicating that a significant portion of existing users on the platform does not overlap with the target audience for perpetual contracts.

Additionally, Kalshi's typical users are often retail investors who have never interacted with cryptocurrency assets, depositing via bank ACH transfers. Even if the platform introduces cross-margin functionality in the future, these regular retail clients will likely lack the professional trading knowledge to use perpetual contracts for hedging their prediction positions.

Opportunities for Prediction Market Platforms to Break Through

Only one scenario exists for a potential breakthrough: if Kalshi and Polymarket officially launch the cross-category margin-sharing function, leveraging partnerships with top-tier brokers and clearing institutions, it could attract high-net-worth funds and high-frequency trading users to participate simultaneously in event contracts and perpetual contracts.

Institutional trading departments could incorporate prediction markets into their overall risk management toolset.

Both platforms possess quality institutional collaboration resources: Kalshi has data partnerships with FIS and Tradeweb; Polymarket has teamed up with the Intercontinental Exchange (ICE). These collaborations can help retain institutional clients that value "hedging and value preservation on the same platform, optimizing capital allocation."

However, this breakthrough path remains filled with uncertainties and depends on multiple conditions being met simultaneously: building an underlying infrastructure that has undergone extreme market pressure tests, deepening institutional collaborations, and proving to clients that the platform offers capital optimization and risk management value.

In the fiercely competitive industry, these are essential conditions for survival. Hyperliquid has firmly occupied traffic and first-mover advantages, leaving Kalshi and Polymarket with no choice but to strive for breakthrough opportunities across other dimensions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。