Author: Four Pillars

Translated by: Felix, PANews

Stablecoins are the most important product category in the crypto space. Earlier this year, the supply surpassed $32 billion, doubling from $15 billion in 18 months. By 2025, the trading volume reached $33 trillion, exceeding the adjusted throughput of the U.S. Automated Clearing House (ACH) network. B2B stablecoin payments are expected to grow from less than $100 million per month in 2023 to $6 billion per month by 2025. All areas related to the U.S. dollar are migrating on-chain, and this process is happening faster than the most optimistic predictions from two years ago.

However, of this $32 billion, less than 10% can earn native yields. USDT and USDC holders cannot earn any yield directly from the issuers, while Tether and Circle collected over $7 billion in interest income last year. Among this, Circle allocated 50% of the reserve interest to Coinbase, which then returned part of it to Coinbase One subscribers paying $4.99 per month at an APY of 3.5%. There are indeed earnings in the stablecoin economy, but these must pass through layers of extraction by issuers, distribution partners, custodial relationships, and payment walls.

The arbitrage opportunity between the potential yield of stablecoin capital and its actual yield remains one of the largest gaps in the crypto space, and this opportunity persists because existing participants are structurally unable to fill this gap. The GENIUS Act prohibits stablecoin issuers from directly paying yields to token holders. U.S. remittance licenses and banking relationships also do not allow direct yield payments.

For those globally seeking yields, USDe is a product designed to bridge this price gap. It is a synthetic dollar supported by delta-neutral positions (long spot cryptocurrencies, short equivalent perpetual assets) that can earn funding rate differences and pass them on to sUSDe holders. This mechanism is not novel (basis trading has existed in traditional finance and crypto for decades). Ethena’s innovation lies in its packaging: tokenizing the trade, institutionalizing the custodianship, embedding it within the DeFi ecosystem, and making the product itself a distribution channel.

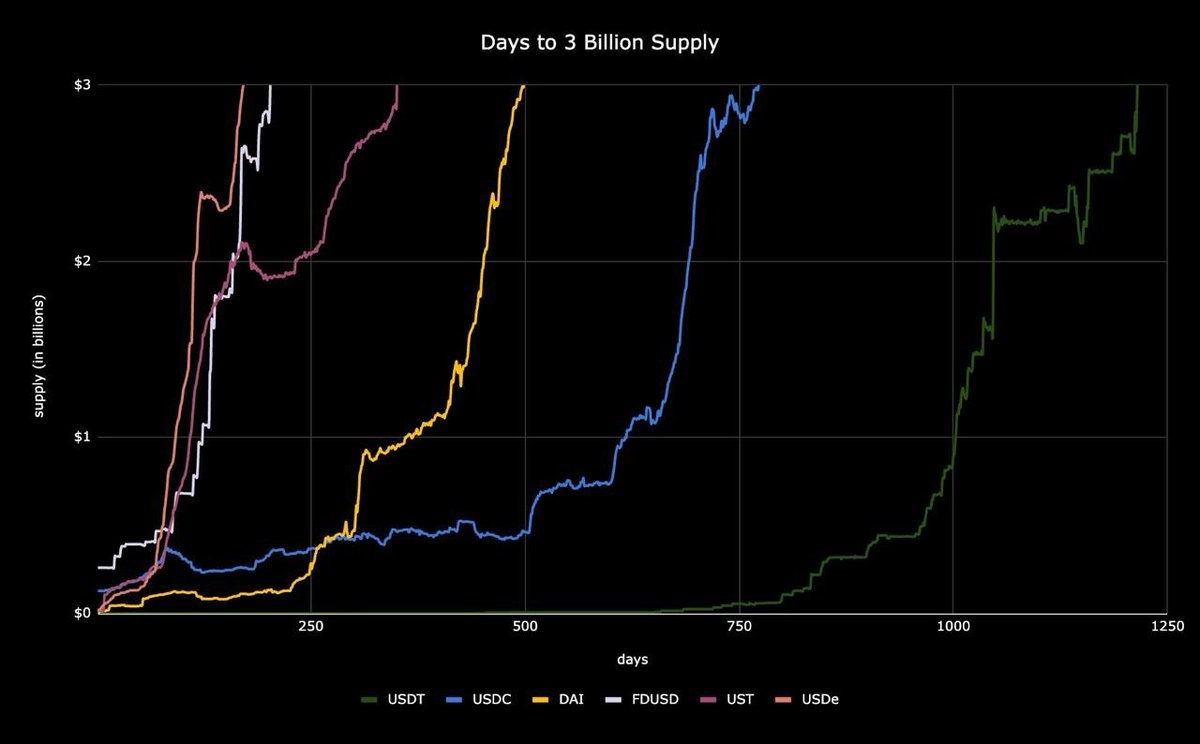

USDe reached a supply of $1 billion within three to four weeks of launch. USDT took over three years to reach the same milestone. USDC took 21 months. USDe reached $2 billion in seven weeks and $6 billion in 10 months. This indicates that before the emergence of USDe, the market’s demand for interest-earning stablecoins was largely underestimated.

Source: X

Architecture

The story of Ethena begins with Guy Young. Before founding Ethena, Young worked at Cerberus Capital Management, a firm managing $55 billion in distressed credit, specializing in decisions that could lead to fund losses if mismanaged. Young has publicly stated that USDe "has the potential to become a $100 billion product," positioning Ethena as the "yield version of Tether." If Tether today reaches a size of $186 billion while providing zero yield to holders, the question becomes: "As the version that pays you yield, how large can USDe grow?"

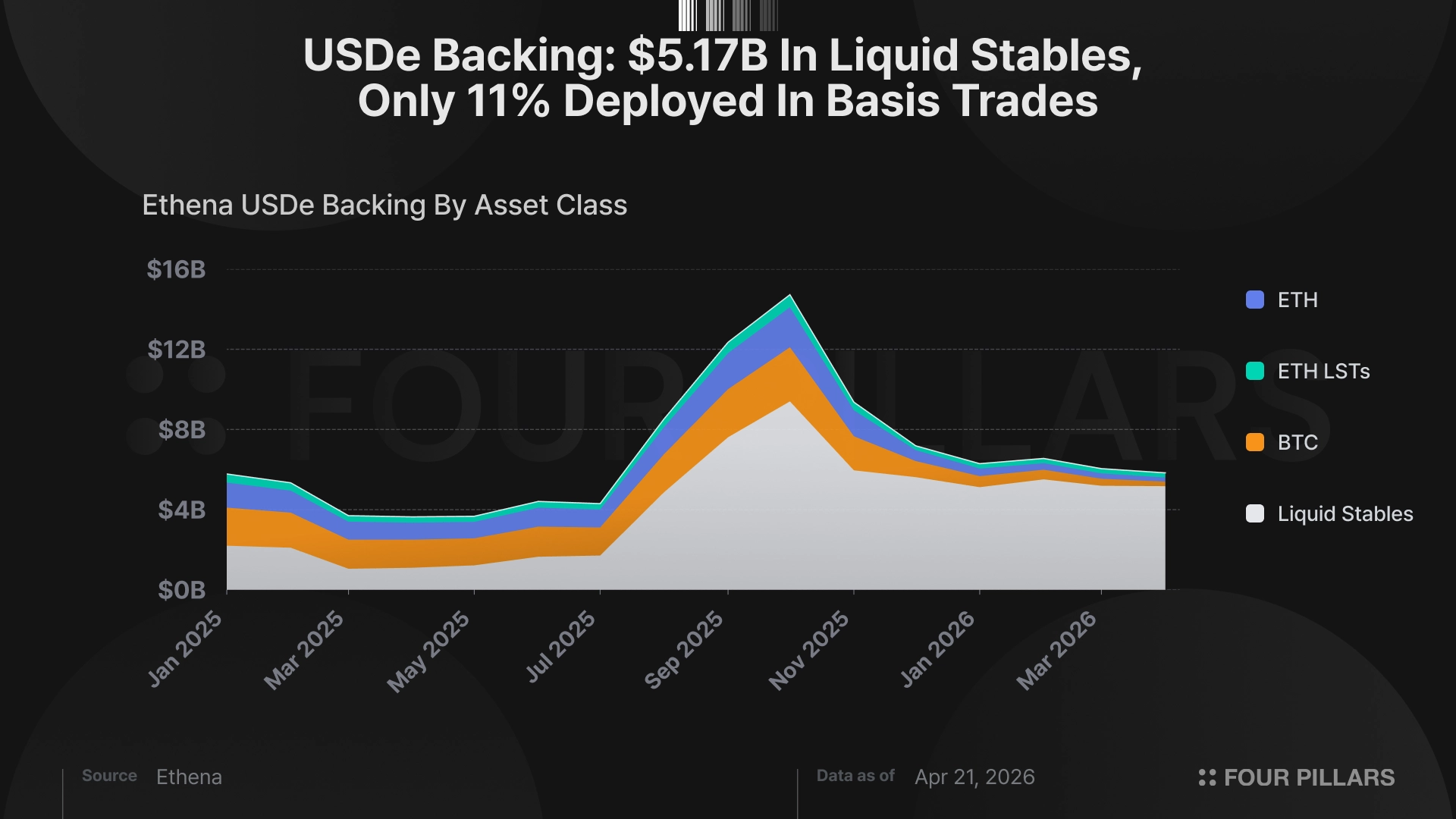

Currently, USDe has a supply of $5.83 billion. Of this, 89% ($5.19 billion) is held as liquidity stablecoins by regulated custodians (Copper, Ceffu, Cobo) and is subject to regular audits. Only 11% ($223 million BTC, $423 million ETH) is currently in delta-neutral perpetual contract positions, actively generating basis income. About half of the supply is staked (48.6%), with sUSDe yielding 3.75%.

From this data, we can conclude that first, Ethena deploys only 11% of its AUM into yield strategies but can generate $270 million in annual total fees. Second, the remaining 89% is idle capital. On April 6, Ethena announced a plan to redeploy $5.1 billion into yield strategies: through institutional lending via Anchorage Digital (an OCC-chartered institution), Maple Institutional, and Coinbase Asset Management; structured credit; and performing HyENA basis trading on the Hyperliquid platform. USDtb (a $937 million product backed by BlackRock BUIDL) has already launched. The other projects have been announced but not yet executed.

If this $5.1 billion is deployed at a mixed rate of 4-5%, under the current staking ratio, the yield for sUSDe is expected to rise from 3.75% to 8-10%.

Three Bullish Arguments

1. Ethena is the yield layer of the dollar economy.

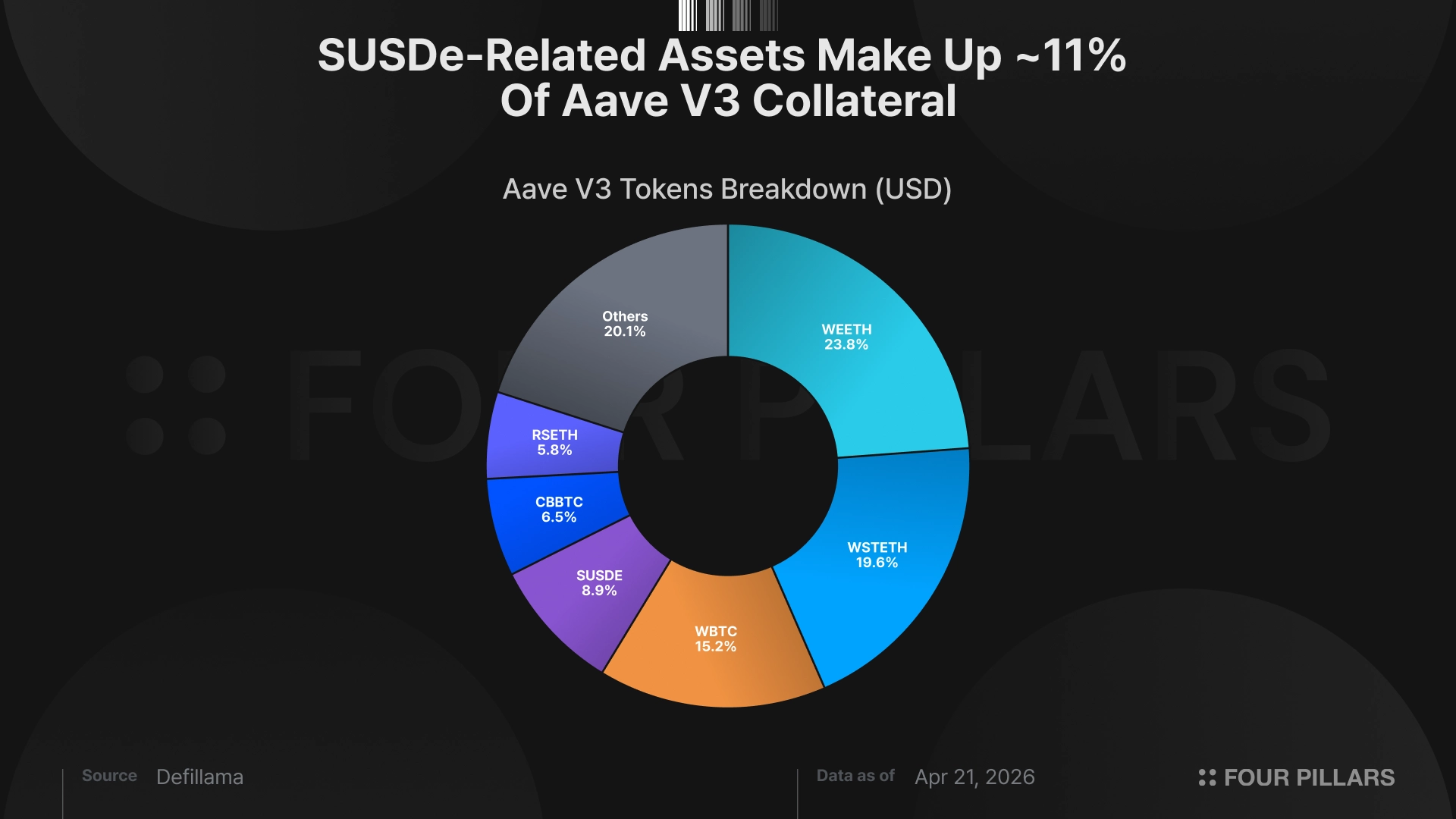

In terms of composability, USDe's related exposure is diversified throughout the DeFi ecosystem. As of April 19, approximately $2.9 billion of sUSDe (about 50% of the total supply) is stored as leveraged looping collateral on the Aave platform, around $750 million is stored in Pendle's fixed-rate market, and roughly $250 million is stored in Morpho's vault.

Deposit sUSDe, borrow USDC, buy more USDe, stake, then repeat; or utilize Pendle PT fixed income, then re-collateralize. Every dollar of USDe in the loop creates 2-3 times the effective protocol demand. This multiplier demand exists because sUSDe has already been accepted by Aave as blue-chip collateral, tokenized as principal and yield components on Pendle, supported in Morpho's gated vault, and recognized by Sky.

These integrations took two years to complete. Listing sUSDe on Aave required approval from the risk committee, oracle design, liquidation parameter calibration, and real on-chain testing through multiple volatility events. Pendle had to build a dedicated PT market with sufficient liquidity to support the re-collateralization loop. Morpho's gated vault architecture needed specific risk parameterization for sUSDe.

This composability also has a self-reinforcing effect. More sUSDe accepted as collateral → potentially more loops → increased demand for USDe → enhanced liquidity → more protocols willing to accept sUSDe as collateral → a cyclical and iterative process. Currently, most of the supply is in circulation, indicating that the flywheel has begun to turn.

Regarding cyclical considerations, there is a subtle but important point, which is also the biggest bearish argument since Ethena's inception. Critics argue that Ethena's yield relies on perpetual contract funding rates, which in turn depend on speculative leverage, and leverage fluctuates with cycles; thus, USDe is a cyclical trade that will never become a permanent allocation, indicating a structural ceiling on USDe.

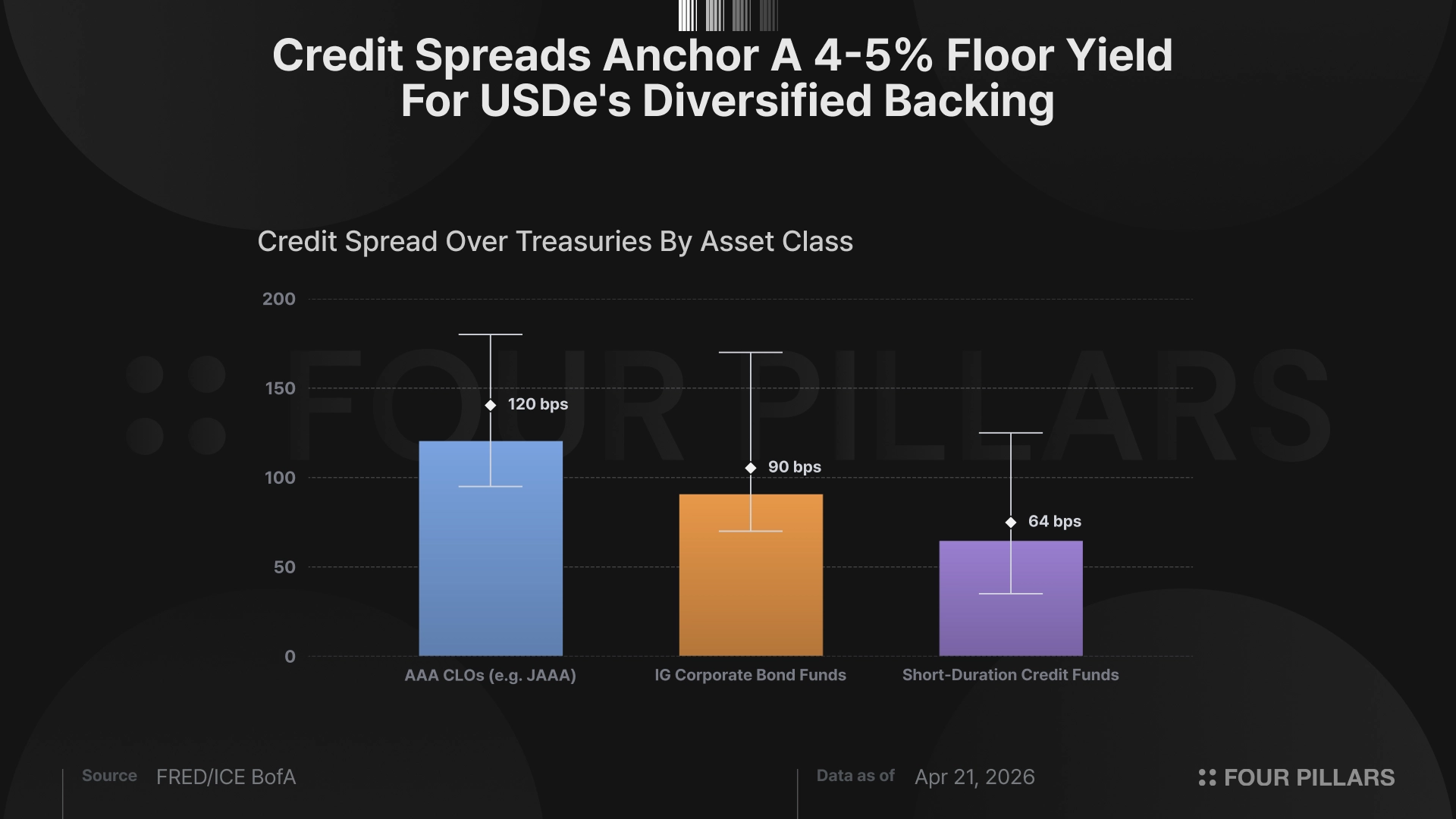

The diversification plan eliminates this criticism. By redeploying $5.1 billion into institutional loans, Ethena adds a yield of 4-5% in credit exposure, which performs well in high-interest-rate times: that is to say, precisely when basis trading is compressed. High rates benefit the diversified loan portfolio. Low rates favor basis trading (lowering rates stimulates speculation, which stimulates leverage demand, leading to higher perpetual contract funding rates).

The practical result is that USDe can generate competitive yields in both interest rate environments. This transforms USDe from a cyclical capital rotation product into a permanent asset allocation for capital rotation. Permanent asset allocation can grow through compounding, while cyclical trading cannot. This distinction determines whether USDe remains perpetually limited to $5-6 billion or exceeds $25 billion.

2. At the intersection of two major trends.

Ethena is the only protocol connecting the stablecoin economy and the perpetual economy through a single mechanism, capable of converting perpetual funding rates into stablecoin yields. Both markets are accelerating in development, and this dual growth simultaneously expands Ethena's potential market.

The stablecoin aspect has been discussed: its size reached $32 billion and continues to grow, with less than 10% earning yields, indicating a significant demand. The GENIUS Act is the more complex part. According to this act's 1:1 high-quality liquid asset (HQLA) reserve requirement, USDe does not qualify as a payment stablecoin and is, in fact, illegal to issue in the U.S. USDe is currently unavailable in the U.S., with its capital inflow primarily coming from overseas. Ethena's solution is USDtb, which is a payment stablecoin that complies with the GENIUS Act, issued through infrastructure provided by Anchorage Digital, which is OCC-chartered. Together, they form a dual-track system: USDtb is used for payments under U.S. regulation, while USDe is for global yield trading.

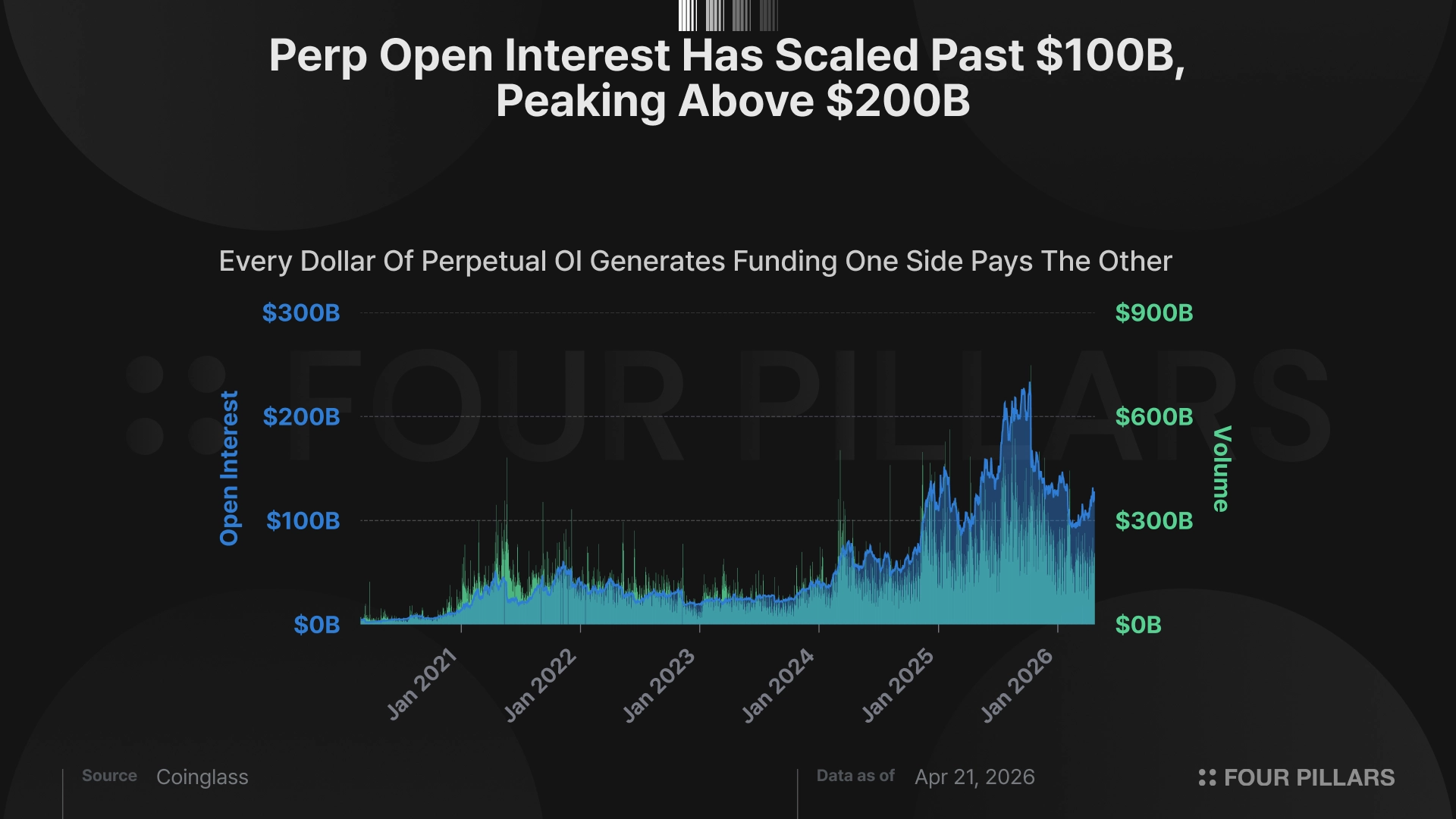

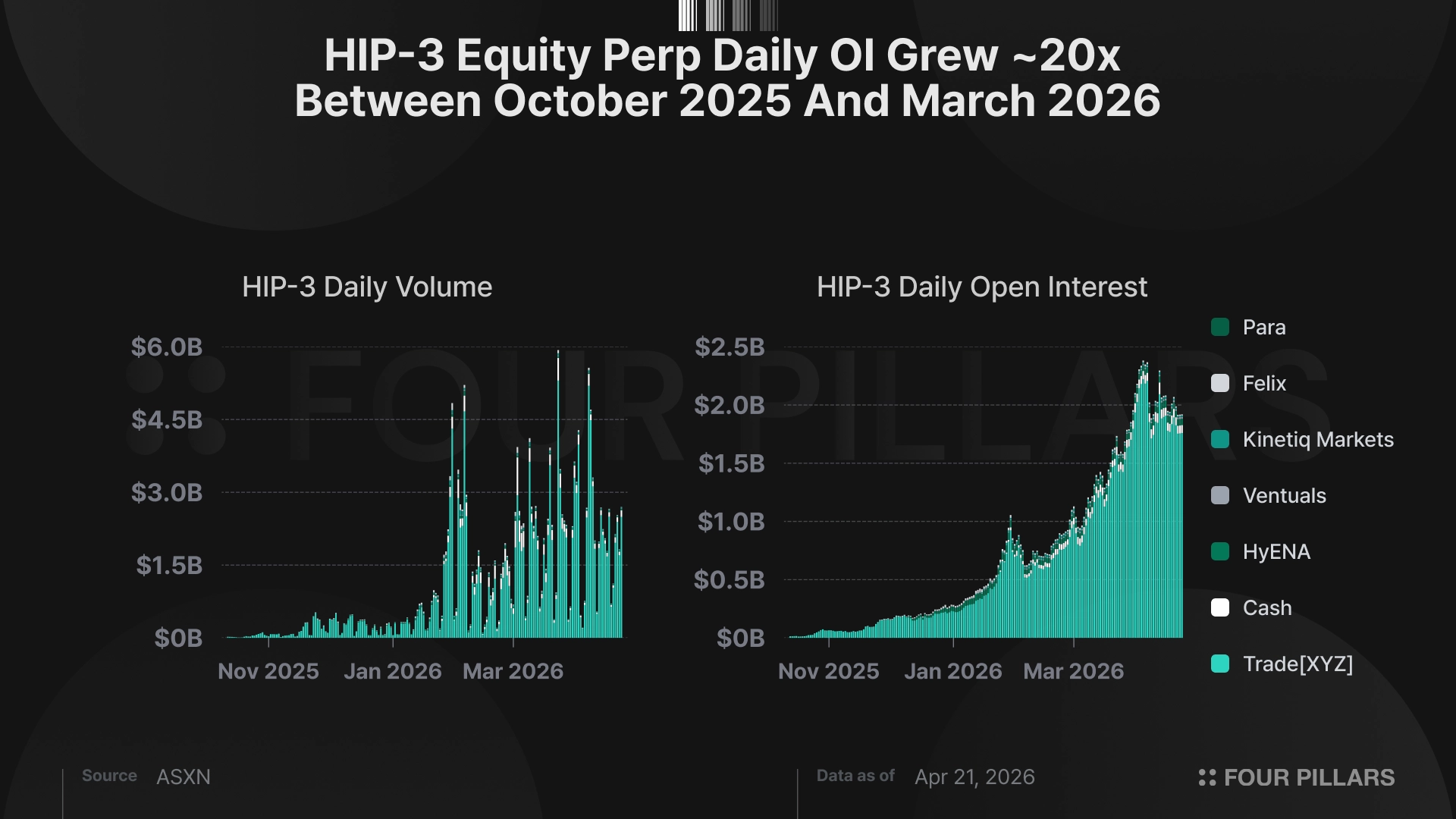

The growth in perpetual contract trading volumes has been particularly significant. By 2025, trading volume for DEX perpetual contracts is expected to reach $77 trillion, a year-on-year increase of 346%. Following that, stock perpetual contracts will arrive. Binance launched Tesla perpetual contracts in January 2026. Coinbase then introduced stock perpetual contracts in March. S&P Dow Jones has licensed the S&P 500 index to TradeXYZ on Hyperliquid. The HIP-3 stock perpetual contracts on Hyperliquid surged from $525 million per week to $30.7 billion per week in the first quarter, a quarterly increase of 5,757%, rising as a proportion of Hyperliquid's total activity from 21.5% to 45% (peak). A brand new asset class was essentially created last quarter.

Each dollar of open interest (OI) in perpetual contracts generates a funding fee that one side pays to the other. These funds are the source of USDe's yields. As perpetual contracts expand into stocks, commodities, and (eventually) foreign exchange, Ethena's sources of income will multiply and diversify. During the period of heightened tension in Iran in 2025, when traditional financial markets were closed, crude oil trading on Hyperliquid exceeded $1 billion in weekend volume. This is a source of yield that did not exist twelve months ago.

The traditional limitations of basis trading strategies lie in trading capacity. As the AUM deployed into trades expands, the funding rates earned will decrease, causing yield to drop. For single-asset basis strategies, scaling up can be counterproductive . Ethena's solution is to expand the number of markets that can be deployed. As the size increases, the production cost of unit yield will decrease. Each new perpetual contract market will create basis trading capacity that previously did not exist. If the open interest in stock perpetual contracts reaches 1% of the open interest in the S&P 500 futures (about $750 billion), Ethena alone will add $7.5 billion in revenue-generating capacity.

Source: ASXN

The synchronized growth of both is its structural characteristic. Increased demand for stablecoins drives more yield-seeking funds into USDe. The depth of the perpetual market expands, creating more competitive yields for these funds. The two mutually reinforce each other. MakerDAO generates stablecoin yields by holding government bonds. Hyperliquid facilitates perpetual trading. However, neither has transformed one market's returns into another. Ethena is the only protocol that accomplishes this, and as the scales of the two markets expand, this advantage will generate compounding effects.

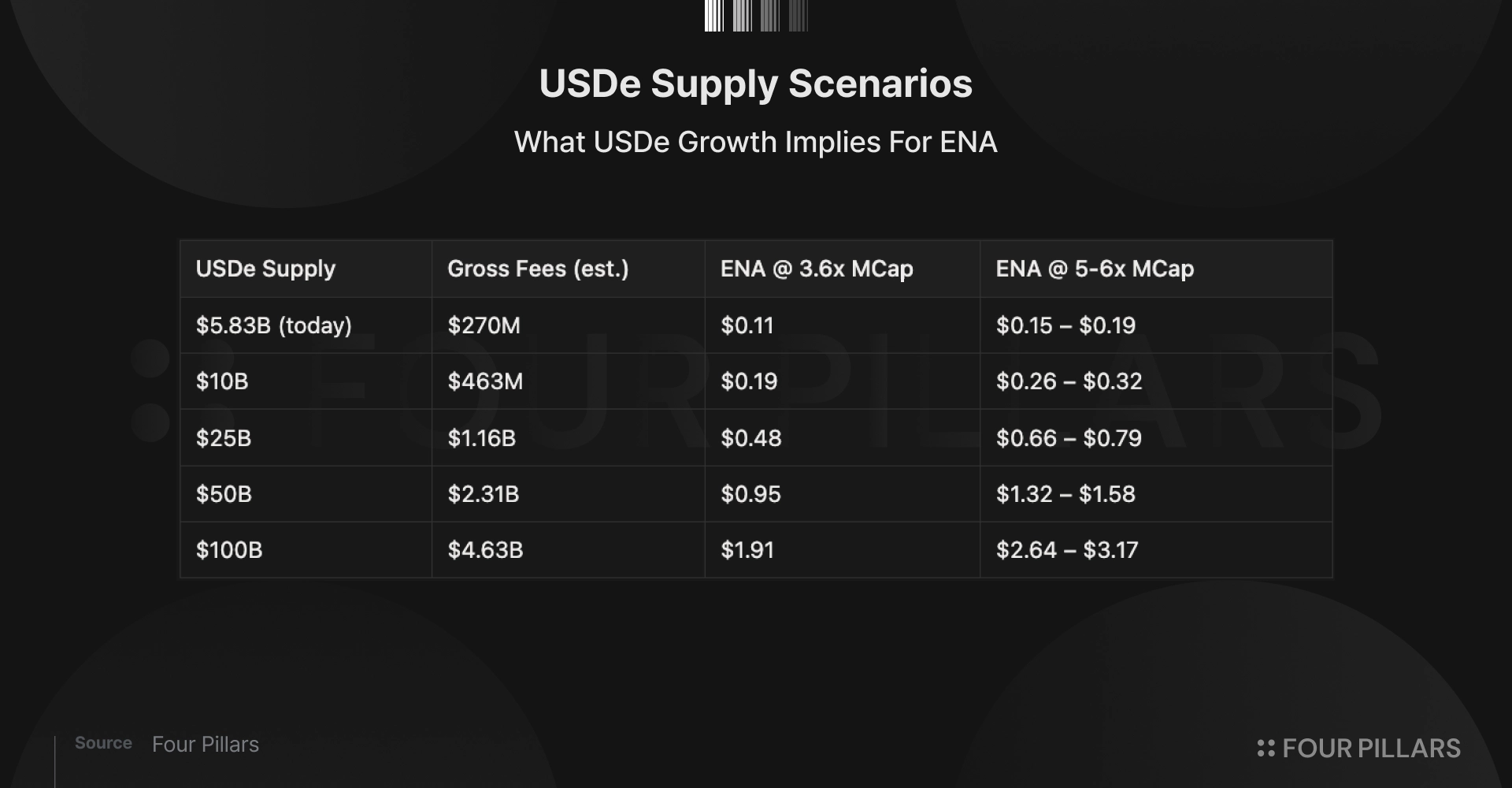

3. ENA's pricing exists at a deviation in a total fee multiple of 3.6 and value accumulation of zero. There is asymmetry in any reasonable growth scenario (including scenarios far below management's set targets).

Currently, ENA's trading price is approximately $0.11. Considering its $270 million in annual total fee income, this equates to a price-to-earnings ratio of 3.6 times that of top DeFi income protocols (with no active value accumulation).

The vast majority of fees flow through a treasury that complies with the ERC-4626 standard to sUSDe holders, a portion of which is allocated to a $62 million reserve fund to address periods of negative yield. The specific allocation ratio has not been publicly disclosed, but the current capital adequacy of this reserve fund is approximately nine times its conservative tail risk requirements, and the governance committee suggested in March 2026 to allocate more interest to sUSDe holders.

Guy Young proposed a goal of $100 billion for USDe. Supporting this goal are reference points including Tether's market cap of $186 billion, USDC's market cap of $78 billion, and the current total supply of yield-generating stablecoins being less than 10%. Assuming that the share of yield-generating stablecoins doubles to $500 billion, capturing 20% of the stablecoin market (a conservative assumption considering the favorable regulatory and interest rate factors), then the total market cap of this category would reach $100 billion, of which Ethena would be the largest and most widely distributed protocol.

Here are the calculations at different supply levels, using current fee earnings per dollar of assets under management:

At $25 billion (5% of a $500 billion stablecoin market), Ethena generates over $1 billion in total fees annually, and depending on the multiple, ENA's value ranges from $0.48 to $0.79. This means there is a further upside potential of 4-7 times on this basis, without needing to activate the fee switch. The issue of the fee switch has attracted excessive attention from analysts, but it is essentially just a scale issue.

At the scale of $5.83 billion and a yield of 3.75%, activating it would be counterproductive. Competitive yield products (for example, the Aave USDC deposit yield is about 3%, and Sky's sDAI yield is about 3.75%) have yields comparable to sUSDe under simpler risk structures. If a 10% commission is charged, the yield on sUSDe would fall from 3.75% to approximately 3.4%.

Capital is unfeeling; it will flow to projects with higher yields. The supply of USDe will decrease, and the capital base used to pay fees will also shrink. Mechanisms intended to create value could diminish the product's competitiveness instead.

When the yield is sufficiently high to allow for some fees without losing competitiveness, this trap will be broken at larger scales. Assuming sUSDe's asset scale reaches $25 billion, supported by diversified capital, with 25-30% of AUM allocated to basis trading generating 6-10% yield (from perpetual funding rates) and 55-60% allocated to institutional loans generating 4-5% yield, the blended protocol yield would be around 4-5%. At an approximate staking rate of 50%, this translates to sUSDe yields of about 8-10%. This is a more conservative estimate. Under even more conservative assumptions (basis funding rates compressing to 5%, institutional loans at 4%), sUSDe's yield could still reach around 7%, significantly higher than alternatives like government bonds, and sufficient to absorb moderate fees.

The mechanism designed by the risk committee has already addressed the "counterproductive at small scales" issue; it simply needs to scale up to make a substantive impact. As USDe grows, this problem will naturally be resolved. The fee switch debate is essentially a microcosm of the AUM dispute; if the AUM issue is resolved, the fee switch debate will also be resolved.

The dilution rate is an annualized 14.6%, equating to about $30 million per month at current prices. By December 2026, the circulating supply is expected to reach approximately 73% of fully diluted, compared to the current 58.4%. This is the cost of holding that position and must be acknowledged. In the above scenario, a potential return of $0.11 is sufficient to offset several times the dilution cost. However, dilution is also the reason this strategy is asymmetrical and not infinite. To participate in this trade, you would pay a time premium of about 15% annually.

Risks

“Risk means that more things can happen than will happen.” — Elroy Dimson

This article does not imply that Ethena will certainly succeed, but rather that the asymmetry in its architecture is sufficient to make betting profitable. Surface risks have been priced in. The real risks worth discussing are internal to Ethena's mechanism.

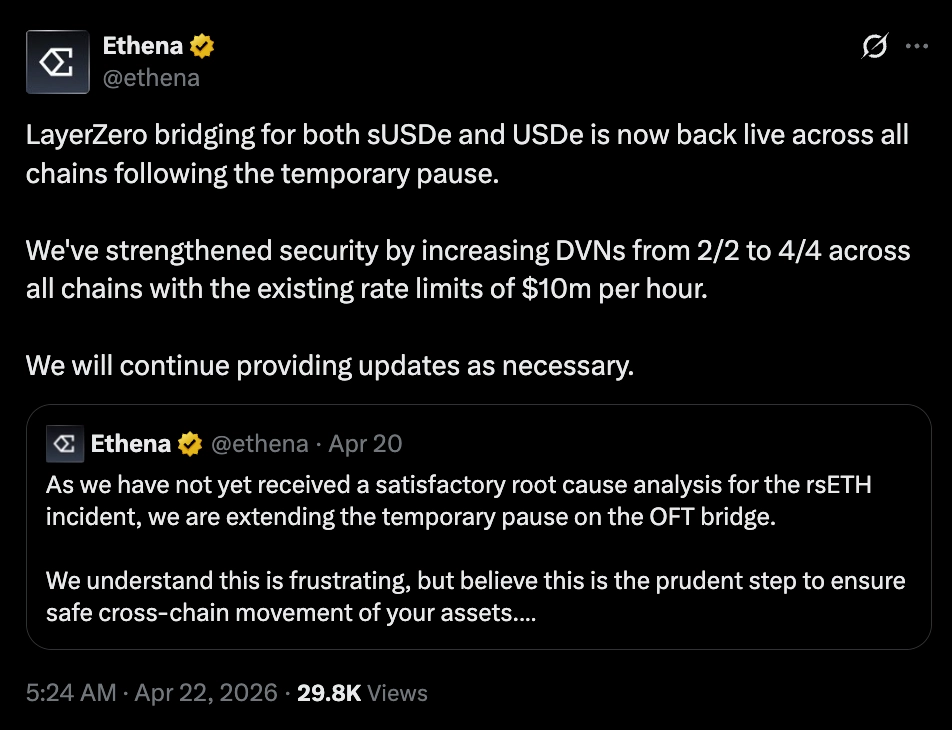

Risk spillover caused by DeFi. The series of hacking incidents in April 2026 was not an isolated case. This is the reverse operation of the composability flywheel. Ethena can be harmed without being hacked. USDe is whitelisted as collateral in Aave, Pendle, Morpho, and Sky; any failure of adjacent assets or cross-chain bridges could trigger cascading liquidations, thereby compressing sUSDe yields and disrupting leverage loops.

Nevertheless, Ethena's response to the Kelp incident (temporarily pausing LayerZero OFT bridging, issuing new reserve proofs as needed, confirming zero exposure to rsETH) was the correct operational behavior and reflects the conduct a credit-trained management team should undertake in a chain event. By April 22, all bridges across chains had been restored, and DVN doubled from 2/2 to 4/4, maintaining a rate limit of $10 million per hour.

Source: X

Basis trading capacity is not as interchangeable across markets as bull market assumptions suggest. The expansion argument is based on Ethena extending the perpetual contract market into stocks, commodities, and foreign exchange markets and deploying to each new basis curve. However, in reality, most new perpetual contract markets do not exist in a perpetual premium state. The funding rate structure for stock perpetual contracts is significantly different from that of cryptocurrency perpetual contracts because stock trading occurs during specific time periods, has a dividend curve, and involves short-term borrowing costs related to clearing mechanisms.

Credit risk. The statement "high rates benefit lending, low rates favor basis trading; therefore, USDe can produce yields across cycles" is clever but quietly transforms Ethena from a market-neutral basis protocol into a balance sheet that bears credit risk. Anchorage, Maple, and Coinbase Asset Management act as intermediaries for real credit exposure. The 4-5% institutional lending in 2026 does not represent risk-free yield. It reflects someone's capital costs, and somewhere downstream, there exists borrower default risk, which sUSDe holders effectively bear.

The "stickiness" of sUSDe depends on leverage, not allocation demand. The bullish perspective argues that the $4.9 billion of sUSDe in Aave loops is evidence of strong demand and a composability moat. Likewise, it also indicates that a majority of USDe holders are leverage yield miners rather than true capital allocators. In any market, leveraged positions are the holders most sensitive to interest rates. If sUSDe's APY falls below the borrowing cost of USDC on Aave, even for just a few weeks, these loops will automatically unwind. The composability flywheel effect is bidirectional.

The fee switch may not be the catalyst the market expects. The design of this mechanism is already highly advanced. The startup criteria from the risk committee includes a real-time competitiveness safeguard intended to maintain the bought-back sUSDE yield at ≥1.075 times the sUSDS level. Analysis conducted by OAK Research in March 2026 shows that the preferred option (a gradual fee rate range with reserves) can maintain the competitiveness of sUSDE 95% of the time. The problem lies in scale. Under the current compression of spreads, even the best-designed scheme has an annual buyback scale of only about $26 million, while ENA's daily trading volume is $74 million, with issuance exceeding $300 million in 2026.

OAK's suggestion is not to activate the fee switch now, as too few dividends would be even more disappointing than not activating at all. The bullish view has portrayed the fee switch as a catalyst for recent price increases. But in reality, unless USDe's assets under management significantly expand (the numerator increases) or the issuance plan concludes early (the denominator decreases), the fee switch may have no impact. In any realistic scenario, neither situation will occur before the end of 2026, meaning the long-anticipated price increase may arrive 12-18 months later than currently expected.

“Crowning”

Gradually, then suddenly.

In 2018, the stablecoin category was virtually nonexistent. In 2020, it was still just a $2 billion novelty. By 2023, its market cap surpassed $150 billion, and it will reach $320 billion by the end of 2025. In financial history, very few product categories have been able to grow this rapidly.

Ethena is doing something unprecedented in finance: converting speculative energy from one market into stable yields in another. Traders pay capital for long positions. Stablecoin holders convert this capital into yield. Two markets, one mechanism, one protocol connecting them.

Moreover, both markets are compounding in growth. The market cap of stablecoins is moving towards being above $500 billion. Perpetual contracts are breaking through their crypto-native limitations, with stock contracts launching in the first quarter, commodity contracts already beginning trading, and foreign exchange contracts on the horizon. Every new perpetual market expands Ethena's yield generation capacity. Every dollar of stablecoin demand expands the capital pool wishing to hold it. The two complement each other and develop together.

Ethena is the first synthetic dollar with scale effects. USDe does not compete with Tether or Circle. They are payment channels. USDe is the capital infrastructure where on-chain dollars can be held and earn yields.

Related reading: After a significant shrinkage of stablecoin USDe, has Ethena decided to trade U.S. stocks and gold?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。