The same Ethereum is being redefined by two almost different language systems.

Written by: imToken

In April 2026, Hong Kong is telling two stories about Ethereum at the same time.

At the 2026 Hong Kong Web3 Carnival, Vitalik Buterin continues to discuss security, decentralization, verifiability, post-quantum resistance, and long-term sustainability, attempting to answer the question "What should Ethereum look like in the next five years"; while on the other hand, institutional investors and asset management giants, from BitMine to BlackRock, are increasingly inclined to view ETH as an underlying asset that can enter balance sheets, generate staking yields, and be packaged into ETFs and traditional account systems.

In other words, while Vitalik is still discussing the "world computer," institutions have begun to regard ETH as "cash flow assets." Interestingly, both descriptions refer to the same Ethereum.

This creates an interesting and noteworthy sense of division.

The Ethereum in Vitalik's eyes and the Ethereum in the eyes of institutions seem to be turning into two different things. One belongs to protocol design, cryptography, security boundaries, and long-termism, while the other pertains to asset allocation, staking yields, ETF packaging, and balance sheet management.

But the issue is not about who is right or wrong; rather, when these two perspectives begin to emerge simultaneously, has the narrative focus of ETH quietly shifted? Further, what does this change mean for the majority of ordinary Ethereum users who are neither institutions nor writing protocol code?

1. Vitalik is still answering "Why does Ethereum exist?"

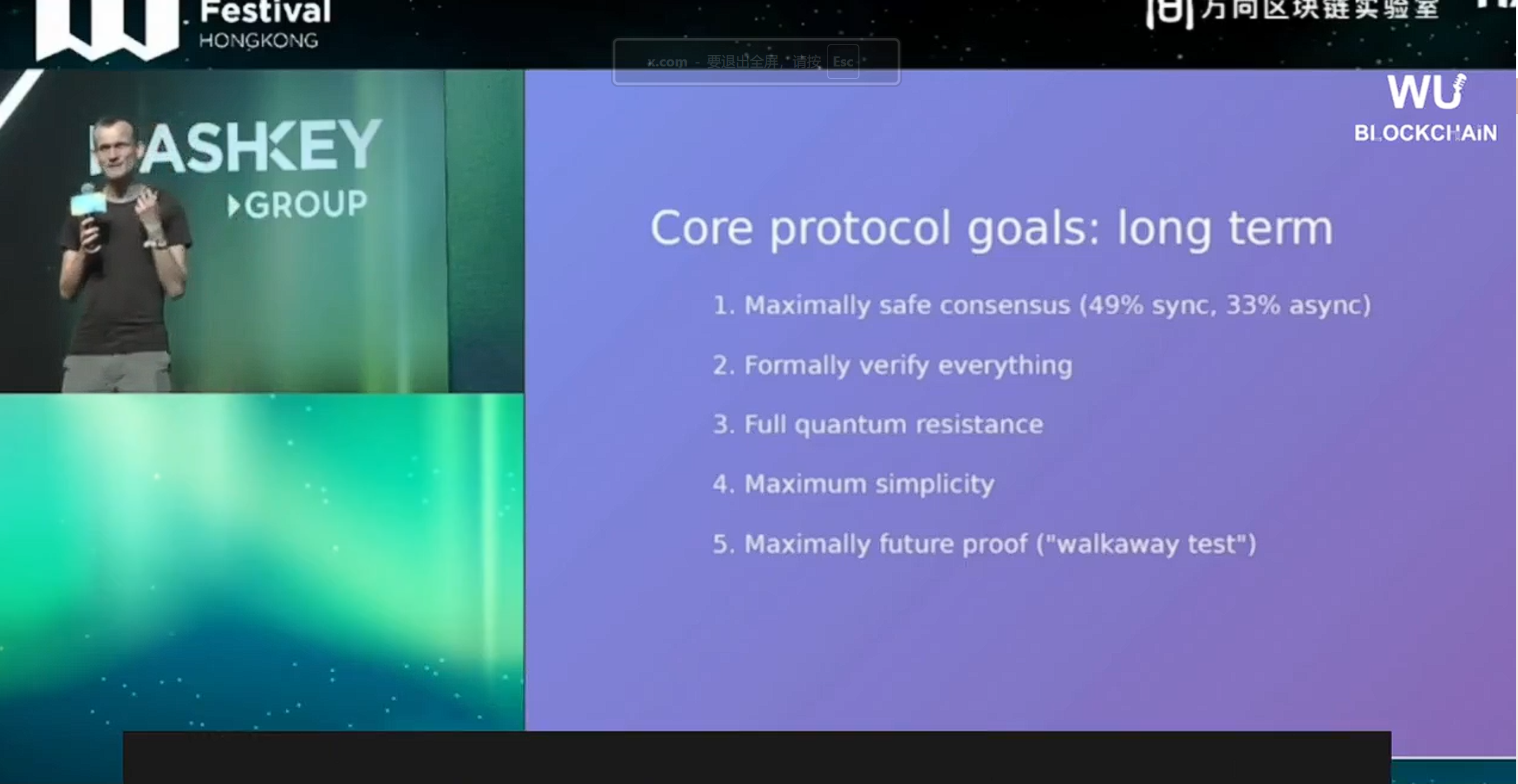

This time, Vitalik's public statement in Hong Kong nearly reorganized all the key directions in Ethereum's roadmap for the foreseeable future.

Looking at each keyword individually, they are very technical, such as scalability, account abstraction, post-quantum, ZK-EVM, Lean Consensus, formal verification, and state layer optimization. However, placing these contents back into the same question reveals that he is doing something very unified—designing a long-term architecture for Ethereum that can continue to operate securely even without any specific team.

He defined two core functions for Ethereum very succinctly:

One is the public bulletin board. Applications post messages here, and everyone can see the content and order of these messages; these messages can be transactions, hashes, encrypted data, or even more complex on-chain commitments. The important thing is not what these messages themselves are, but that "they are seen by everyone simultaneously, and the order can be validated," which provides public credibility (see further reading "From 'Global Computer / Settlement Layer' to 'Bulletin Board': What Ethereum and Vitalik Want to Achieve?");

Two is shared computing. This means providing a layer of shared digital objects controlled by code, where tokens, NFTs, ENS, identity, DAO control rights, and on-chain organizational rules may appear to be different applications, but from a protocol perspective, they are actually different expressions of the same layer of abstraction: they all require an open, verifiable, and hard-to-tamper execution environment;

Around these two functions, Vitalik is also very clear about the value prioritization of Ethereum: self-sovereignty, verifiability, and fair participation must come before pure efficiency. In other words, speed is important, scalability is also important, but they cannot become reasons for Ethereum to sacrifice its foundational principles; that is, Ethereum is not meant to become the fastest chain, but rather to be the most reliable chain.

This prioritization also determines the technical trade-offs in the roadmap for the next five years.

In the short term, Ethereum needs to continue scalability while also improving account abstraction, the block creation process, node synchronization, and privacy support. For example, continuing to raise the gas limit, achieving better parallel verification through block-level access lists, allowing validators to perform more thorough checks on blocks via ePBS, and further optimizing node state synchronization.

In the medium term, the real challenge is not scalability at the execution layer but at the state layer. After all, computation can be optimized, made parallel, and advanced through hardware and engineering means, but state must be stored, synchronized, and verified. If handled poorly, it could gradually squeeze ordinary nodes and lightweight validators out of the network. This is also why Vitalik repeatedly emphasizes the state layer problem. If the verification threshold keeps rising, Ethereum will unknowingly lose its most precious decentralized foundation.

Post-quantum resistance is another medium to long-term main line. Vitalik used a very vivid metaphor: imagine a country that has never experienced rain, where all houses were not designed to withstand rain. When rain finally comes, only 5% of the houses might leak, but the residents will initially not panic because they have never seen rain, until one day they are told that in five years or ten years, rain will really come.

At this point, the entire society must relearn how to repair houses, schools, and offices. Quantum computing for Ethereum is like that rain that has not yet fallen but must be prepared for in advance.

Quantum-resistant signature algorithms are not new per se; the real difficulty lies in efficiency. Hash-based signatures may reach 2–3 KB, while common signatures today are only a few dozen bytes. The gas cost of on-chain verification for quantum-resistant signatures could far exceed that of existing solutions. If every transaction were simply replaced with a quantum-resistant signature, Ethereum's efficiency would be directly compromised.

Therefore, the solution is not to have every transaction bear the heavy costs individually but to shift the pressure from "individual signatures" to "entire blocks being packaged." This also means that only after ZK tools mature can the migration to quantum resistance truly have a feasible engineering path.

Looking further ahead, Vitalik's roadmap nearly describes a terminal state of Ethereum: Lean Consensus, ZK-EVM, formal verification, and walkaway tests.

In fact, if we look at these technological items in sequence, what Vitalik truly wants to resolve is how to ensure Ethereum's security does not depend on any specific team, specific client, specific hardware assumptions, or any generation of cryptographic tools' continuous existence. In essence, it is about ensuring that Ethereum maintains its positions of decentralization, security, and trusted neutrality—positions that "others do not do well but it must carry out," while efficiency, experience, and vertical demands can be left to L2 and the application layer.

2. From "World Computer" to "Yield-Generating Asset," institutions are reevaluating ETH

In contrast to Vitalik's protocol perspective, institutions have a much more straightforward understanding of ETH.

They may not first discuss Lean Consensus, state tree optimization, or quantum resistance migration and may not describe Ethereum using the term "public bulletin board." Instead, their concerns are usually more direct: Can ETH be held securely? Can it generate yields? Can it enter balance sheets? Can it be packaged into compliant products? Can it accommodate larger-scale funds?

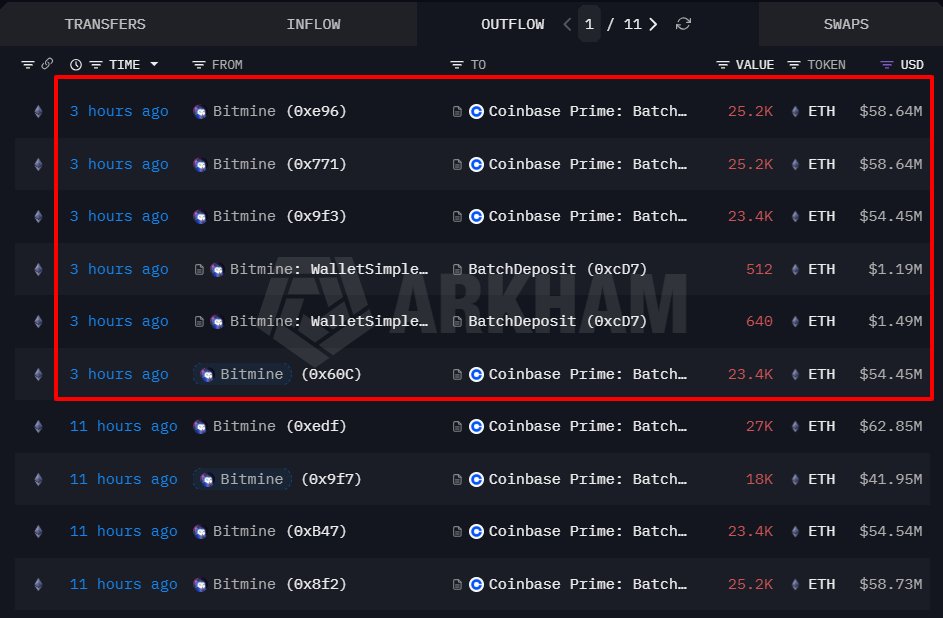

BitMine's actions are a concentrated reflection of this institutional language.

As of April 24, BitMine holds 4,976,485 ETH, accounting for approximately 4.12% of the total ETH supply, of which 3,471,000 ETH is staked, making up 70% of its total ETH holdings.

It is visibly clear that Tom Lee and BitMine are accelerating the staking progress of their held ETH, transforming their ETH from merely a crypto asset waiting for appreciation into a layer of foundational asset with inherent yield potential.

This is the largest difference between ETH and most crypto assets. Many asset values still heavily rely on narratives, liquidity, and risk appetite, but the asset properties of ETH are becoming more complex. It has usage demand, staking mechanisms, burning mechanisms, on-chain economic activities, and potential for being repackaged by traditional financial products.

BlackRock's ETHB represents another path.

As a Staked Ethereum product under iShares, it integrates ETH's price exposure with staking yield distribution into a traditional asset management framework, emphasizing that investors can gain exposure to ETH-related assets through traditional brokerage accounts without having to directly manage private keys, operate nodes, or handle on-chain staking processes (see further reading "When Wall Street's ETH Begins to 'Generate Yields': From BlackRock's ETHB, Observing the Shift in Ethereum's Asset Properties").

This is essentially a translation that encapsulates the complexity of self-custody, staking, validators, slashing, gas, and other technical terms in the Ethereum world, translating them back into custody, monthly/annual yields, and other more easily understandable concepts. While this may not resonate with crypto-native users, for traditional funds, it is precisely the interface they need to enter a new asset class.

Interestingly, the Ethereum Foundation itself has also begun to more proactively use the yield-generating attributes of ETH. On February 24, the Ethereum Foundation announced the launch of the Treasury Staking Initiative, pledging approximately 70,000 ETH for staking, with staking yields directed back into the foundation's treasury to support long-term operations and ecological development. The foundation emphasized that this process will minimize reliance on proprietary software, reduce client centralization, and control risks through multi-regional and multi-operator configurations.

This move is thought-provoking, indicating that from Tom Lee's BitMine to BlackRock and now the Ethereum Foundation, all are placing ETH into a new asset framework. As a result, in the eyes of institutions, ETH begins to present a mixed form standing between "digital commodity," "infrastructure assets," and "yield-generating assets." It possesses attributes of a scarce asset akin to Bitcoin, growth characteristics similar to internet stocks, and also possesses a certain inherent yield feature due to its PoS mechanism.

This change means that ETH's valuation framework no longer relies solely on "Will it rise when a bull market arrives?" but begins to engage in more traditional discussions, such as staking yields, total supply, burn amounts, institutional holding ratios, product scales, net inflow of funds, and whether future on-chain settlement demand will continue to grow.

Of course, this does not mean that ETH has transformed into a low-risk asset; it remains highly volatile and still exposed to regulatory, technological, market cycle, and liquidity risks. However, the difference is that institutions are beginning to reprice these risks within their familiar asset management frameworks rather than simply viewing ETH as a high Beta crypto asset.

3. Two Ethereums, two discounts of the same value

Writing to this point may create an illusion that Vitalik's Ethereum and the institution's Ethereum seem like two different things:

One is a protocol with an evolving technical route, and the other is a yield-generating asset that continuously produces cash flow from a financial perspective; one belongs to developers, while the other belongs to Wall Street; one speaks of long-termism, while the other is about asset returns.

But the reality is precisely the opposite; these two perspectives do not negate one another but are actually complementing each other.

After all, the reason institutions are willing to purchase, "hoard," and stake ETH in large quantities is precisely due to the mid-to-long-term vision of Ethereum that Vitalik promises, which provides a foundation for ETH’s long-term asset properties.

For institutions holding for years, they are truly fearful not of short-term price fluctuations but of the unpredictability of the underlying asset’s rules. If a protocol's signature scheme could suddenly fail in the quantum computing era; if a client bug could lead to repeated network outages; if the chain's finality and consensus security could not withstand extreme environmental challenges; if the roadmap highly depends on a specific team being continuously online, then no matter how attractive the yield models are, they are merely digital games built on quicksand.

Therefore, those terms in Vitalik's roadmap that excite the technical community—quantum resistance, Lean Consensus, ZK-EVM, formal verification, walkaway tests—when translated into the language of institutions, can actually be condensed into four words:

Long-term reliability.

So, while "walkaway tests" is engineering language, its meaning to institutions is very clear: that ETH's stability does not depend on any specific team always being present, does not depend on any cryptographic assumptions always holding true, does not depend on several client teams never encountering issues, which is the necessary condition for Ethereum to be regarded as a long-term asset.

Of course, conversely, institutional funds and large-scale staking also provide economic support for Vitalik's roadmap.

It is well known that after Ethereum transitioned to PoS, security no longer relies solely on cryptography and client engineering but also on the scale, distribution, and penalty mechanisms of staked ETH. The more ETH that is staked, the higher its market cap, and the greater the economic cost attackers must incur to influence consensus. Therefore, each ETH staked by BitMine is not just a slogan at the consensus level; rather, it actively participates in building Ethereum's security budget.

In other words, by promoting quantum resistance, Lean Consensus, and ZK-EVM on the technical level, Vitalik is raising Ethereum's technical lower bound; by economically holding and staking ETH on a large scale, institutions are raising Ethereum's economic lower bound. These two curves push each other upward, simultaneously making Ethereum more reliable.

This is also why the terms "world computer" and "yield-generating cash flow asset" may appear to be two definitions, but in reality, they are not contradictory. They are different definitions, but they converge on the same goal: making Ethereum larger.

A mature global infrastructure requires both perspectives to coexist.

Final Thoughts

Objectively speaking, as of today, Ethereum is no longer a network that can be explained by a single narrative.

It is both the public bulletin board and world computer in Vitalik's words, as well as the yield-generating asset and infrastructure exposure in the eyes of institutions; it is both the protocol engineering advanced by developers and the digital asset being repriced by capital markets; it embodies self-sovereignty, verifiability, and trusted neutrality, while also beginning to be included in ETFs, balance sheets, and yield models.

In the coming years, the market may not price ETH according to Vitalik's language, but the reason institutions are willing to continually buy, stake, and package ETH is precisely because Vitalik's insistence on security, decentralization, verifiability, and long-term robustness is gradually transforming into an "institutional dividend" that can be discounted by capital markets.

This may well be the most significant change for Ethereum by 2026.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。