Author: Dune

Translation: Felix, PANews

This article is an extended analysis based on a speech by Fredrik Haga, co-founder and CEO of Dune, at EthCC 2026. Here are the details.

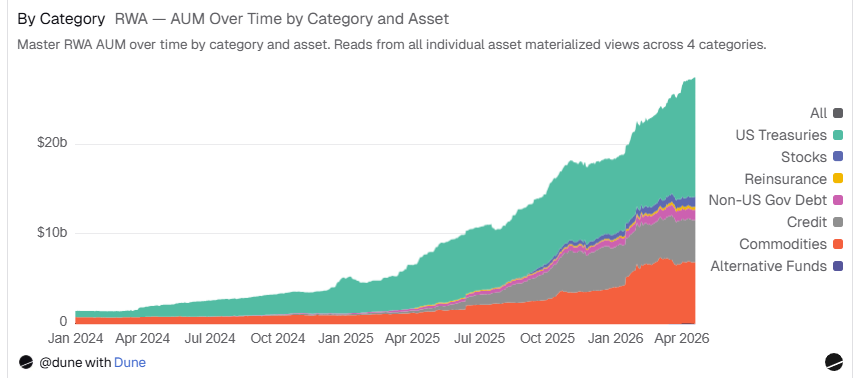

The scale of tokenized RWA has reached $27 billion. However, only about $2.7 billion has been actively deposited into decentralized lending markets as collateral, in vaults, or used for yield strategies. This article will explore the distribution of these funds, the driving forces behind them, and what this suggests for the future.

From Regulatory Clarity to Composable Capital

Three regulatory milestones at the end of 2025 and the beginning of 2026 accelerated the tokenization process. In July 2025, the GENIUS Act established the first comprehensive framework for payment stablecoins in the United States, requiring 1:1 asset backing and clear regulations. In March 2026, the U.S. SEC and CFTC jointly categorized major blockchain tokens as digital commodities rather than securities. A few days later, the SEC approved Nasdaq to trade and settle tokenized stocks and ETFs on its main market.

These milestone events further propelled the tokenization process. As the settlement layer for tokenized assets, the total supply of stablecoins has surpassed $330 billion, growing twelvefold since 2020. During the same period, the number of active stablecoins increased from 31 to 215. Tokenized RWA has also shown a similar developmental trajectory, with its assets under management (AUM) growing twenty-sevenfold over two years to approximately $27 billion, expanding from just a few categories to seven categories tracked in the dashboard (including reinsurance and equities).

Besides the impressive AUM data, a more meaningful question is: how much of this capital is actually used in the DeFi space? Currently, about $2.7 billion of tokenized RWA is actively deposited in DeFi lending markets, accounting for roughly 10% of the $27 billion tokenized AUM. A year ago, this 10% share was nearly nonexistent. Composability can be said to be the most promising advantage of tokenization, allowing tokenized assets to be used as collateral, for lending, and to cycle through different yield strategies across various protocols and chains.

Note: The RWA tokens counted are limited to collateral and vault supplies. Data as of April 16, 2026.

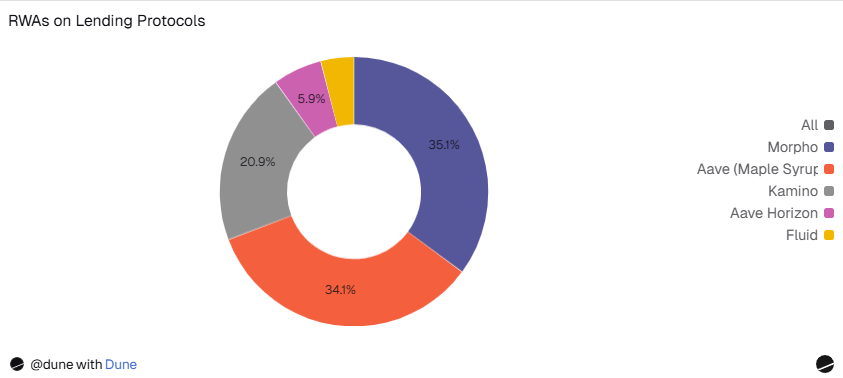

Where is the $2.7 billion stored?

The funds are distributed among four major platforms across Ethereum, Solana, and multiple L2s:

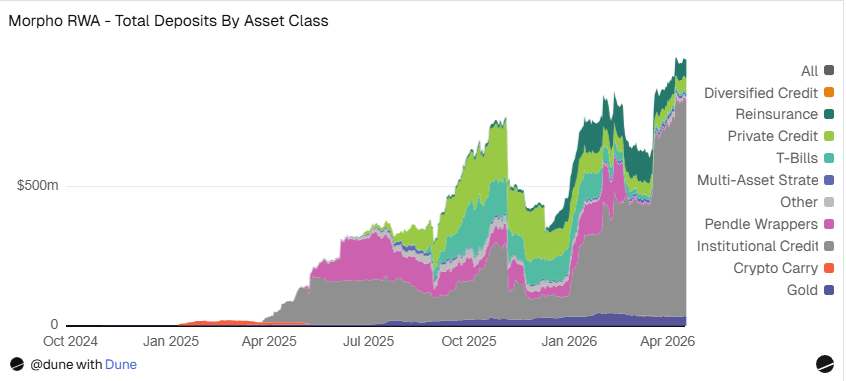

- Morpho ($957 million): Permissionless, listed 41 types of RWA assets across 10 chains. Professionals like Gauntlet and Steakhouse manage vaults, allocating funds to these markets and building structured leverage strategies based on tokenized RWA.

- Aave ($929 million): Maple's syrup tokens are deposited on Plasma, Base, and Ethereum. Institutional credit flows permissionlessly to the most economically efficient lending.

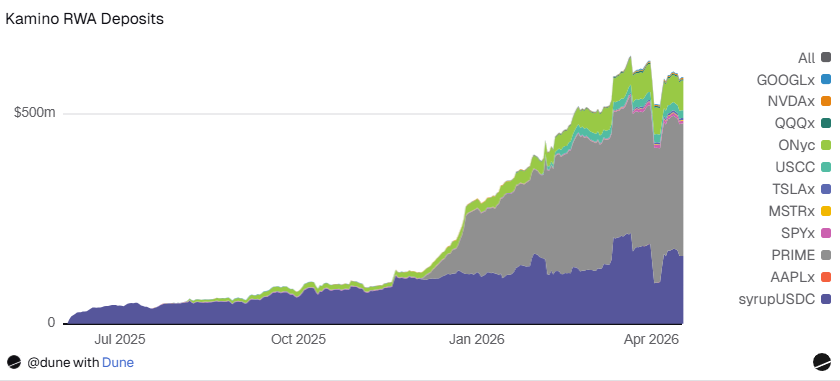

- Kamino ($587 million): The largest lending protocol and RWA platform on Solana. Among them, PRIME accounts for $315 million (HELOC lending yield), syrupUSDC for $161 million, ONyc for $71 million (reinsurance), USCC for $18 million, plus the xStocks market (covering seven types of tokenized stocks, totaling $21 million).

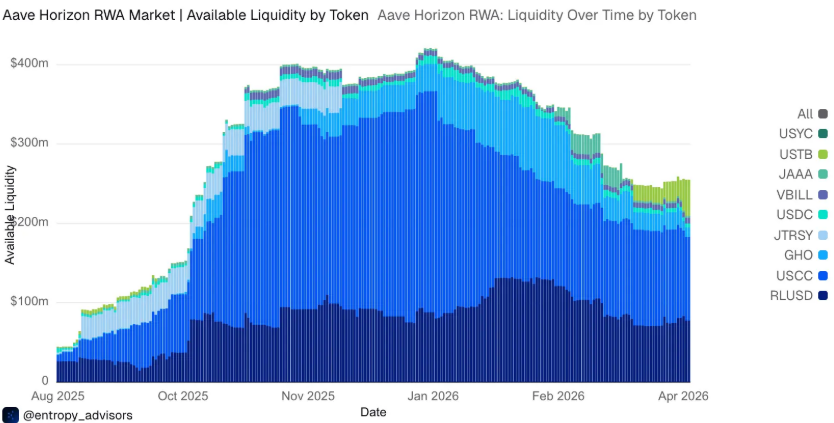

- Aave Horizon ($161 million): A permissioned RWA market focused on institutions on Aave. There are 256 addresses with an average holding of $1.5 million. Among them, USCC is $105 million, USTB is $46 million, VBILL is $7 million, and JAAA is $3 million. The total amount of actively lent stablecoins reaches $124 million, with a utilization rate of 77%.

- Fluid ($109 million): reUSD is $94 million (reinsurance), gold is $12 million, and syrup is $2 million. Notably, it supports using the Re Protocol's reUSD as collateral, which other platforms do not offer.

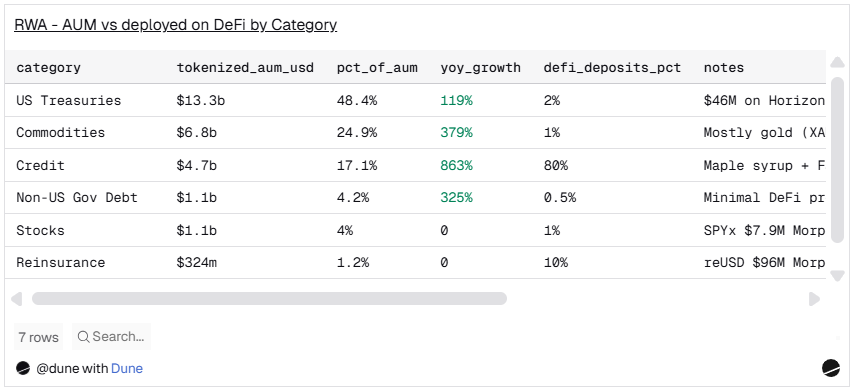

The tokenized assets do not align with the assets actually used

There is a significant disparity between the assets that dominate tokenized AUM and those that are actually deposited into lending protocols as collateral. These two rankings are nearly completely reversed.

Source: Dune

U.S. Treasury bonds account for 48.5% of the tokenized AUM ($13.2 billion), but only 2% of DeFi deposits. Credit assets account for 17% of AUM but occupy about 80% of deposits. Commodities account for 25.2% of AUM but account for nearly less than 1% of DeFi deposits.

The dominance of credit assets is due to their earning models. Maple's syrupUSDC yields about 6% while Treasury bonds (T-Bills) yield about 3.5%. When your collateral can earn 6% while you can borrow stablecoins at 3%, you achieve positive returns. Curators like Gauntlet build clear cyclical strategies on this basis: deposit RWA as collateral, borrow funds, and then buy more. This is designed and risk-managed leverage. This also explains why credit assets appear on every major lending platform: $957 million on Morpho, $929 million on Aave, and $476 million on Kamino.

Source: Dune

Reinsurance is gradually becoming a genuinely new type of composable asset class. The Re Protocol's reUSD appears on multiple platforms: $96 million on Morpho (including $50 million of Pendle PT-reUSD), $94 million on Fluid, and ONyc in Kamino also occupies $71 million. Overall, the tokenized AUM of reinsurance reaches $324 million (accounting for 1.2% of the total), with DeFi deposits of about $261 million (accounting for 10% of the total), of which about 80% of the tokenized reinsurance funds are active in lending protocols, with a deposit ratio far higher than any other asset class.

Tokenized stocks have also appeared in DeFi: SPYx ($7.9 million on Morpho), xStocks on Kamino (covering SPYx, TSLAx, QQQx, NVDAx, GOOGLx, MSTRx, AAPLx totaling $21 million), and deSPXA ($3.6 million). Although the amounts are small, the infrastructure is already in place, and borrowing activities secured by stocks are occurring.

This disparity is quite enlightening. Tokenization emphasizes security and familiarity. U.S. Treasury bonds are easy to understand, well-regulated, highly transparent (frequent net value updates and convenient oracle pricing), and highly attractive for institutional balance sheets. Composability, on the other hand, values different things: yield spread and leverage economics.

Collateral structure is evolving in real-time

The dominance of high-yield credit may be partly due to timing factors. Aave Horizon provides the clearest evidence.

When Horizon launched in August 2025, Superstate's crypto arbitrage fund USCC provided an annualized yield (APY) of about 15% through basis trading in crypto futures. This yield made it account for 93% of all RWA collateral. While Treasury products were also introduced, no one showed interest.

Subsequently, as the basis narrowed, the yield of USCC was compressed to about 4%, aligning with the 3% to 4% yield of Treasuries. The result: the collateral share of USCC dropped from 93% to about 67%, while USTB skyrocketed from less than $1 million to $45.6 million within 30 days, a growth of 570%. As the yield spread narrows, the market is moving toward diversification.

Source: Dune

This is significant not only for Horizon. If credit yields compress across the entire market (as often happens in mature markets), then the collateral structures on all platforms may become more diversified. Assets that dominated the first wave (high-yield credit) may not dominate the next wave. Factors like risk appetite, regulatory environment, and settlement mechanisms will become more important.

Pendle adds a new dimension to this evolution. Its principal tokens (PTs) have occupied $58 million in deposits on Morpho (allowing users to lock in fixed yields from RWA products). Pendle also offers direct RWA markets for thBILL and mTBILL, bringing yield curve trading into the composability stack. As more RWA products go live on Pendle, fixed-rate strategies will become another channel for RWA distribution.

Permissionless access drives distribution

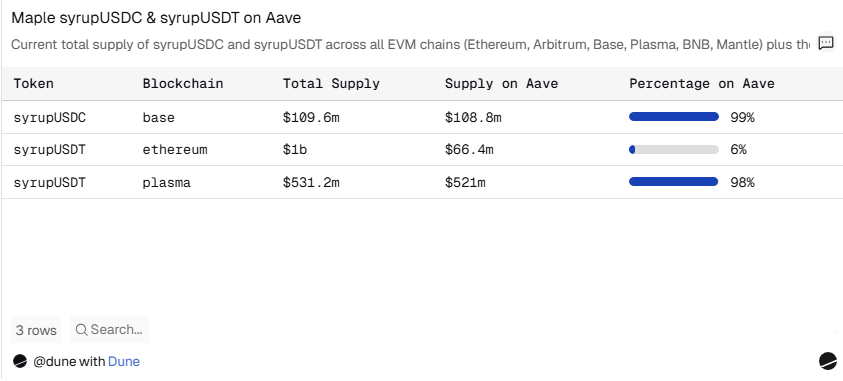

Maple Syrup is the clearest case. syrupUSDC and syrupUSDT are permissionless ERC-20 tokens. Technically, they are a hybrid between stablecoins and RWA since they are pegged 1:1 to USDC/USDT but earn yields from institutional credit. They are classified as RWA because their underlying exposure is real-world lending. Anyone can mint, trade, or deposit them into any lending protocol. No KYC is required, no whitelisting, and no partnerships need to be established.

The result: 98% of syrupUSDT on Plasma and 99% of syrupUSDC on Base are actively deployed on Aave. Curators like Gauntlet independently built leveraged vaults around Syrup without needing to coordinate with Maple. The scale of syrupUSDC on Kamino (Solana) also reached $161 million.

Source: Dune

Every integration increases utility, which attracts capital, and capital drives more integrations. It is this flywheel effect that has led to $929 million being organically distributed across three chains.

This is crucial because distribution is universally acknowledged as the biggest challenge in the industry. Centrifuge's "2026 Tokenization Outlook" report noted that 86% of operators stated that scaling distribution of existing products is more important than launching new products. The case of Maple on Aave shows that permissionless composability itself is a distribution channel.

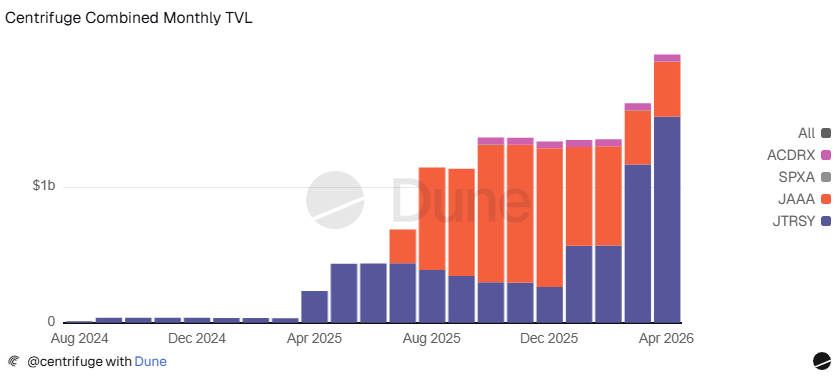

$1.85 billion tokenized, only $13 million composable

Centrifuge's report showcases both the opportunities of RWA and the gaps it faces. It is one of the largest tokenization platforms, with its institutional products having an AUM exceeding $1.85 billion: JTRSY (tokenized U.S. Treasury fund) has a scale of $1.52 billion, JAAA (tokenized AAA-rated CLO fund) has a scale of $403 million, ACRDX (Apollo diversified credit fund) has a scale of $52 million, and the recently launched SPXA (the first tokenized S&P 500 index fund) has a scale of $3.7 million. However, only about $13 million of this is composable in DeFi: mainly achieved through deRWA wrapped tokens and JAAA on Horizon.

Source: Dune

This gap ultimately stems from timing and design. deRWA wrapped tokens went live in September 2025. The permissioned design slowed the integration speed and the liquidity was insufficient.

However, integrations are accelerating. Resolv has committed to deploying $100 million of JAAA on Horizon. Falcon Finance added JAAA and JTRSY as collateral for USDf. Grove is deploying $250 million on Avalanche. LayerZero has enabled distribution across over 165 networks. Meanwhile, deSPXA (the DeFi wrapped version of Centrifuge's S&P 500 fund) has reached a total TVL of $3.6 million, with DEX trading volume hitting $7.9 million, showcasing early organic activity and the potential of the deRWA model: permissionless wrapped tokens running in parallel with permissioned institutional products.

Three Key Points

The growth rate is more important than the current scale. There are $2.7 billion of RWA deposits across major DeFi lending markets, accounting for about 10% of the $27 billion tokenized AUM. However, this $2.7 billion was nearly nonexistent a year ago. The absolute figure is still small, but what truly matters is its growth rate.

The tokenized assets are not equivalent to the assets actually used. Treasury bonds account for 48.5% of tokenized AUM but only 2% of DeFi deposits. Credit accounts for 17% of AUM but represents 80% of deposits. Higher yields can provide positive returns, thereby supporting leverage cycles. Credit yields above 6% are feasible, while the 3.5% yield of Treasury bonds is not. However, as the macro environment changes and yield spreads across different asset classes shift, the composition of collateral will also adjust to fit different assets and emerging categories, such as reinsurance.

Permissionless access drives distribution. Maple's syrup tokens (a hybrid between RWA and stablecoins) have reached a scale of over $1 billion on Aave and Kamino across four chains. These tokens are designed to be composable, therefore the market has composed them. Assets that can be easily accessed tend to be adopted more readily. In contrast, assets that require whitelisting are also catching up but at a much slower pace.

Related Reading: Going On-Chain is Not Liquidity: RWA is Still One Leap Away

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。