Author: Zhao Ying, Wall Street Journal

At 10 PM Beijing time on Tuesday, the U.S. Senate Banking Committee will hold a hearing on Kevin Warsh's nomination as Chairman of the Federal Reserve. This marks Warsh's first formal occasion on Capitol Hill to systematically elaborate on his monetary policy views. Notably, Warsh has long been critical of the massive scale of the Fed's balance sheet, and this hearing may become a significant platform for expressing his related views.

In fact, since the end of 2025, the direction of the Federal Reserve's balance sheet has always been a core topic of high concern in global financial markets. Against this backdrop, Fed Governor Stephen Milan, along with three Fed economists, recently published a working paper titled "A Guide to Reducing the Federal Reserve's Balance Sheet," and on March 26, 2026, during a themed speech at the Miami Economic Club, he systematically explained the strategic logic and potential pathways for the Fed's balance sheet reduction.

The core value of this paper lies in breaking the market's conventional understanding. In the past, the market generally believed that "the ceiling for the Fed's balance sheet reduction is the exhaustion of reserves." However, the paper points out that the demand for reserves can itself be shaped by policy—through a series of regulatory and operational framework adjustments, the Fed can potentially achieve significant downsizing of its balance sheet while maintaining a framework of "ample reserves."

In response, the research team at CITIC Securities subsequently conducted an in-depth interpretation. Their judgement is that relaxing LCR standards, reforming SRP, and upgrading Fedwire have certain practical feasibility; however, schemes like reserve tiering, TGA reform, and foreign reverse repo pool reforms are relatively idealistic. Overall, the process of balance sheet reduction is unlikely to alter the underlying logic of global central bank gold purchases, and CITIC Securities still maintains its judgment that the Fed will lower interest rates by 25 basis points in the second half of this year.

Reasons for Reducing the Balance Sheet: Milan's List of Reasons

In his speech in Miami, Milan straightforwardly presented multiple reasons for reducing the Federal Reserve's balance sheet.

First, to reduce market distortions. The excessive scale of the Fed's balance sheet imposes unnecessary interventions on the money market, exacerbating the disintermediation problem of financial intermediaries. Minimizing the Fed's "footprint" in the market is a basic requirement for maintaining the function of price discovery.

Second, to control financial risks. Large asset holdings imply greater exposure to market value losses, while also leading to increased volatility in treasury revenue (remittances). In recent years, the Fed has been under pressure from unrealized losses due to holding a significant amount of long-duration securities, a problem that can no longer be ignored.

Third, to safeguard the boundary between monetary and fiscal policy. A large balance sheet objectively leads to the Fed intervening in the allocation of credit resources, blurring the lines between monetary and fiscal policy. Additionally, paying large amounts of interest on reserves to banks has been viewed by some Congress members as a hidden subsidy to financial institutions.

Fourth, to preserve policy ammunition. If the next zero lower bound crisis occurs, the Fed will need to expand its balance sheet to provide easing space. Compressing the balance sheet to a reasonable scale now reserves necessary room for future policy maneuvers.

Milan admitted that the external perception is that significant balance sheet reduction is "absolutely impossible." However, his judgement is distinctly different: "Reducing the balance sheet is a challenge that can be addressed; those who categorically deny it simply lack imagination."

Key Diagnosis: The Constraint on Balance Sheet Reduction is "Demand" not "Supply"

To understand this discussion, it is first necessary to clarify a long-misunderstood logical structure.

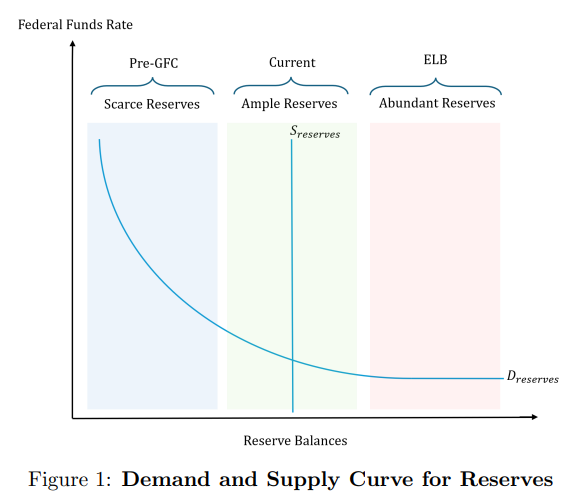

The traditional framework holds that the constraint on the Fed's balance sheet reduction comes from the "reserve supply reaching the steep portion of the demand curve"—once the supply tightens to the critical point, overnight rates will go out of control. Therefore, the Fed can only passively stop reducing the balance sheet once reserves are in a "scarce" state. The "repo market earthquake" in September 2019 was a real-world illustration of this logic.

The breakthrough of the paper lies in shifting the perspective from the "supply side" to the "demand side." The paper indicates that reserve demand is not an external constraint "naturally determined" by payment settlement activities but is artificially elevated by regulatory rules, supervisory execution criteria, and the Fed's own operational framework—Milan describes this phenomenon in the paper as "regulatory dominance" over the Fed's balance sheet.

Specifically, three mechanisms together raised the baseline demand for reserves:

1. Interest rate spreads turned reserves into "easy-income assets." Since the Fed began paying interest on reserves in 2008, reserves have transformed from purely settlement necessities to assets that can compete with Treasury securities. Historically, there have been periods when the interest rate on reserves (IORB) exceeded the yields on 1-month/3-month Treasury bills, leading banks to prefer accumulating reserves from a risk-return perspective.

2. Overlapping multiple liquidity regulations created a "ratchet effect." Rules like the LCR (Liquidity Coverage Ratio), ILST (Internal Liquidity Stress Test), Resolution Liquidity Assumptions (RLEN), NSFR (Net Stable Funding Ratio), and SLR (Supplementary Leverage Ratio) intertwine, creating a dilemma of "borrowing from Peter to pay Paul"—changing just one rule immediately lets another take its place as a new binding constraint.

3. Long-term "stigmatization" of the discount window. The discount window interest rates are relatively high, historically associated with "problem banks," and using it faces risks of information disclosure and regulatory scrutiny, which leads banks to prefer holding large amounts of reserves over using policy tools during liquidity stress periods. The same stigmatization logic has also spread to the Standing Repo Facility (SRP).

This diagnosis implies a fundamental policy path: there is no need to wait for reserves to return to a scarce state, but instead by lowering the "scarcity-ample" dividing line, allowing the ample reserves framework to operate normally under a smaller balance sheet size.

How Much Can Be Reduced: Quantitative Estimates of $1.2 trillion to $2.1 trillion

The paper uses data from the Fed's H.4.1 report dated March 11, 2026, as a baseline, at that time, the Fed's total assets were approximately $6.646 trillion. The breakdown of the liabilities side is as follows: reserves approximately $3.073 trillion, currency in circulation $2.390 trillion, Treasury General Account (TGA) approximately $806 billion, foreign reverse repo pool approximately $325 billion.

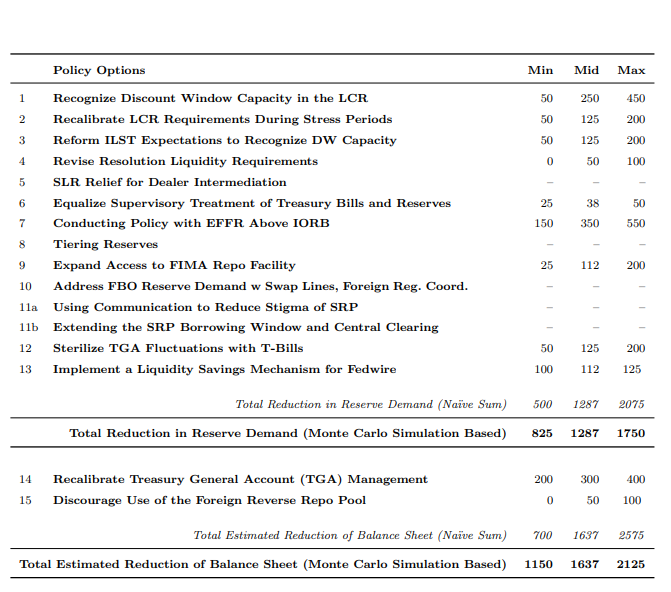

The paper performs quantitative estimates around two major directions, totaling 15 policy options, but the most critical point is that it rejects simple summation. Due to the correlations and substitutability between different policies, the paper employs the Monte Carlo aggregation method under the OMB A-4 framework, leading to the following confidence intervals:

| Dimension | 95% Confidence Interval | Median |

|---|---|---|

| Possible reduction in reserve demand | $825 billion - $1.75 trillion | Approximately $1.287 trillion |

| Total balance sheet possible reduction | $1.15 trillion - $2.125 trillion | Approximately $1.637 trillion |

Milan compared the above intervals with historical reference points in his speech:

- 15% of GDP: The level of the balance sheet after the first round of QE ended in 2009, when the banking system could still operate normally;

- 18% of GDP (2012 or 2019 levels): Reflecting the real liquidity demand of the banking system after the Basel reforms and the Dodd-Frank Act requirements became clearer.

Currently, the Fed's balance sheet is approximately 21% of GDP. According to the median estimated in the paper, if reforms proceed smoothly, the balance sheet could return to levels close to those of 2012 or 2019. As for whether it can drop below 10% of GDP before the crisis—Milan clearly stated: "Unrealistic and unnecessary."

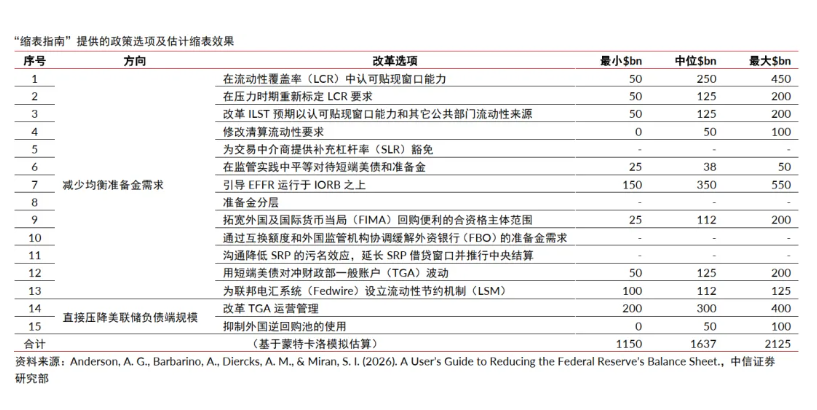

How to Reduce: "Menu-style" Analysis of 15 Options

The paper divides the 15 policy tools into two major categories, providing effect range estimates and execution prerequisites for each.

First Category: Reducing Equilibrium Reserve Demand

(1) Regulatory Reform Level

LCR Reform (Liquidity Coverage Ratio): The core measure is allowing banks to count the financing capacity corresponding to non-HQLA loans pre-collateralized at the discount window as HQLA, subject to a cap. The estimated impact range on reserve demand is $50 billion to $450 billion. The paper also warns that if only the LCR is modified, the NSFR may immediately become the new binding constraint and requires comprehensive consideration.

ILST and Resolution Liquidity Assumptions (RLEN): If regulators accept the discount window capacity and short-term liquidity sources, ILST reform could lead to a decrease in reserve demand by $50 billion to $200 billion; extending the time window assumptions of the discount window could yield an estimated range of $0 to $100 billion.

(2) Supervisory Standards Level

If banks excessively hold reserves to align with examiner preferences (i.e., T-bills and reserves are not "equal" on the supervisory level), the estimated adjustment magnitude is $25 billion to $50 billion. This is a reform that does not require regulatory amendments and can be achieved through a shift in supervisory culture, but the progress difficulty should not be underestimated.

(3) Reducing Returns on Reserves Holdings

Allowing the effective federal funds rate (EFFR) to exceed IORB, thus breaking the current state where EFFR long remains below IORB. The paper quotes the framework from Lopez-Salido and Vissing-Jorgensen (2025), estimating that if "EFFR-IORB = +2bp" (which is close to the pressure level in September 2019), the corresponding decrease in reserve demand would be in the range of $150 billion to $550 billion.

However, this path has evident costs: the volatility of overnight rates and repo rates will significantly increase, and if the market raises precautionary accumulation as a result, the reduction in demand may be partly offset. Following this route must be supported by mechanisms like SRP and Temporary Open Market Operations (TOMO).

(4) Enhancing the Attractiveness of Alternative Assets

This includes upgrading the Fedwire system, enhancing Treasury market liquidity, and promoting central clearing, with the aim of making Treasury securities and other alternative assets more attractive to banks, closer to reserves. These measures also help improve the private sector's capacity to absorb the securities released during the Fed's balance sheet reduction process.

(5) De-stigmatizing Fed Liquidity Tools

By alleviating concerns over the use of the discount window, standing repo facilities, and day loans, banks' precautionary reserve demand can be reduced. This requires systematic coordination from the Fed in terms of transparency, pricing mechanisms, and regulatory communication.

Second Category: Directly Reducing Non-Reserve Liabilities

(1) TGA Management Recalibration

Reducing the cash buffer in the Treasury's account at the Fed from "about 5 days of operational funds" to "about 2 days," returning the excess to the commercial banking system (similar to historical TT&L arrangements). The estimated reduction to the Fed's balance sheet from this measure is $200 billion to $400 billion. The paper also acknowledges that the corresponding increase in deposits returning to banks will raise their demand for reserves, leading to a net effect that is not one-to-one.

(2) Reducing Foreign Reverse Repo Pool Attractiveness

By lowering interest payments and setting size caps, guide foreign central banks and sovereign funds to move funds from the Fed's reverse repo pool to the U.S. Treasury market. The estimated range is $0 to $100 billion, with relatively limited effects, dependent on the willingness of external institutions to cooperate.

Warsh's Signal: From Technical Paper to Policy Expectations

Understanding this paper cannot divorce it from the personnel background of the Fed. The market generally expects Warsh to take over as Chair of the Fed. Warsh has long been critical of the Fed's balance sheet expansion policies since QE and has repeatedly expressed a policy preference for reducing the balance sheet.

This working paper led by Milan has been viewed externally as a forward-looking signal of the Fed's policy direction during the anticipated "Warsh era." The CITIC Securities research team points out that given Warsh's stance and the potential space revealed in this paper, there does exist a possibility for a gradual exploration of restarting balance sheet reduction during the "Warsh era."

However, both the paper and the speech repeatedly emphasize that speed and rhythm are the most important constraints in execution. Milan clearly stated in his speech: "Once the preparations for reform are initiated, following the usual pace of government through the Administrative Procedure Act (APA), it could take more than a year, or even several years." He referenced the SLR (Supplementary Leverage Ratio) reform, which took nearly six years from temporary relaxation to formal regulatory enactment.

This means that the Fed is unlikely to immediately restart balance sheet reduction due to the release of this paper; a more likely path is to begin advancing research from options that face less controversy and are technically feasible, while simultaneously providing the market with forward guidance on how new mechanisms will operate.

CITIC Interpretation: Which Options are Feasible and Which are Idealistic

The CITIC Securities research team conducted a systematic assessment of the 15 policy options from a perspective of practical feasibility, resulting in the following core judgments:

Options with Practical Feasibility:

- Relaxing LCR standards: A technical regulatory reform, with relatively controllable variables and large reform initiative from the Fed;

- Reforming the Standing Repo Facility (SRP): The work on de-stigmatization is more direct and does not involve external legislation;

- Upgrading payment systems such as Fedwire: This represents long-term improvements at the infrastructure level with a clear direction;

- Adjusting ILST supervisory standards: Some reforms do not require legislative amendments and can be promoted through changes in supervisory culture.

Options that are Aggressive or Require External Cooperation:

- Tiered interest on reserves: This may trigger non-linear reactions in the banking system, making operations complex;

- TGA management reform: This involves coordination mechanisms between the Treasury and the Fed and requires political consensus;

- Reducing the attractiveness of the foreign reverse repo pool: Highly dependent on the willingness of external institutions to cooperate, making effects difficult to guarantee.

Overall, CITIC Securities considers this "a reform menu worth referencing and relatively pragmatic," but the actual implementation progress will be far slower than the potential upper limits described in the paper and should be seen as directional guidance rather than a near-term policy commitment.

Market Impact: Increased Volatility, but No Change in Rate Cut Logic

Regarding the impact on the bond market, the essence of the Fed's balance sheet reduction is to decrease the injection of base money, which will inevitably increase the amount of U.S. debt that the private sector needs to absorb. CITIC Securities believes this will amplify market volatility and lead to increased tail risks—despite some deregulation measures (such as SLR easing) helping to expand dealers' capacity to absorb.

In terms of pacing arrangements, the paper clearly opposes accelerating balance sheet reduction through direct sales of securities; a more feasible method is to let maturing securities roll off naturally while providing dealers and the repo market with higher capacity reserves. This objectively limits the intensity of short-term shocks from balance sheet reduction.

CITIC Securities judges that U.S. debt is currently better suited for trading opportunities, with short-term bonds likely outperforming long-term ones.

For the stock market, the contraction effects from balance sheet reduction will impact the real economy through both money supply and portfolio balance effects, but can be offset by lowering the federal funds rate. CITIC Securities believes that if balance sheet reform proceeds, the necessity for corresponding adjustments to the interest rate path will increase, but this has limited direct connection to the current pace of monetary policy. U.S. stocks may wait for a correction window to find a thicker safety margin.

Regarding the gold market, balance sheet reform is unlikely to fundamentally change the strategic logic for global central banks to increase their gold holdings, which is driven more by geopolitical restructuring and the trend of diversification of dollar reserves. Gold still retains medium- to long-term allocation value.

Milan clearly pointed out in his speech that the contraction effects generated by reducing the balance sheet can be offset by lowering interest rates, and that "the reduction of the balance sheet may expand the relative decline of the federal funds rate compared to the baseline scenario." CITIC Securities expects that the U.S. CPI year-on-year will fluctuate in the range of 3.0% to 3.5% this year, and still maintains its judgment that the Fed will lower interest rates by 25bps in the second half of this year, as there is no direct binding relationship between the balance sheet reform and the interest rate decision.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。