Original Title: "The Singularity of Mechanisms, The Starting Point of the Bull Market: Short Selling Rights are the Puzzle to Ignite the Next Round of Altcoin Bull Markets"

Original Author: danny, Crypto Analyst

In the three hundred years of financial markets, there is a repeatedly validated law: Bull markets are never ignited by a narrative, but by upgrades in trading mechanisms. Whether it's ICOs, perpetual contracts, AMM, DeFi, NFT... all are mechanisms driving games and gaming pulls capital into circulation. It is the upgrade of mechanisms that brings prosperity.

Looking back at the starting point of each major market, you will find that their commonality is not that "a good story emerged," but that "market participants suddenly gained a new way of playing."

What has sparked the next round of prosperity is never narrative, but the evolution of trading mechanisms each time.

This law has held true from Wall Street to Binance, from spot to contracts, from DeFi summer to Hyperliquid, never failing.

You can short it, you can short sell - aka equal rights to short selling is the opportunity for the next round of altcoin bull markets.

1. In 1609, a Dutch Merchant Changed Financial History

In 1609, Amsterdam.

The Dutch East India Company (VOC) was the largest publicly traded company in the world at that time, monopolizing the Asian spice trade with stock prices that only rose and never fell. Everyone was buying in, and everyone was making money. The market had only one direction - upwards.

Then a merchant named Isaac le Maire did something that everyone thought was insane at the time: he borrowed shares of VOC, sold them, and bet that they would fall.

This was the first recorded short sale in human history.

The Dutch government was furious. Parliament considered it a malicious attack on the national pillar company and legislated to ban short selling. Le Maire was publicly condemned. But the story did not end there—despite repeated bans, short selling never truly disappeared in Amsterdam. Because market participants discovered an undeniable fact that could not be denied by legislation: with short selling, prices became more real. Those overvalued stocks could no longer maintain false prosperity endlessly.

Four hundred years later, the crypto market is replaying the same script. In the market of thousands of altcoins, there is only buying, no short selling. Prices reflect only the optimistic half, and the pessimistic voices are forcibly silenced. Each market cycle is the same: FOMO pushes prices up, the bubble bursts, chaos ensues, waiting for the next narrative to restart.

But history has told us—each time short-selling rights are introduced, it is not the end of the market, but the starting point of the market.

2. Two Hundred Years on Wall Street: How Short Selling Transformed from "Enemy of the State" to "Market Cornerstone"

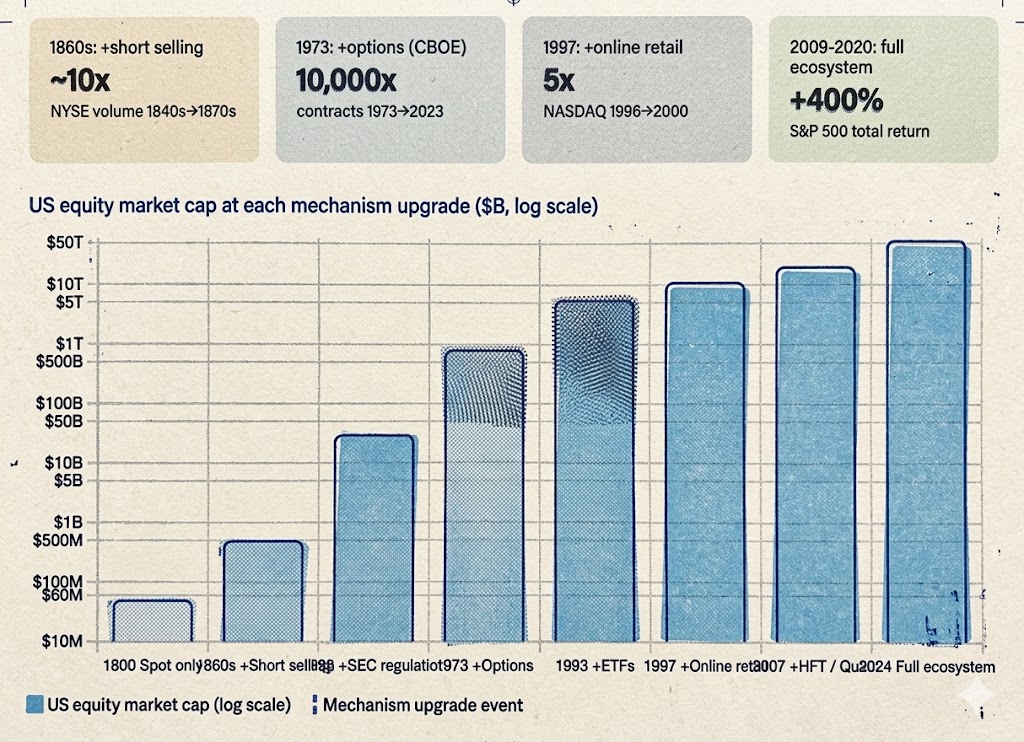

1792-1840s: The Savage Era - A Primitive Market that Could Only Go Long.

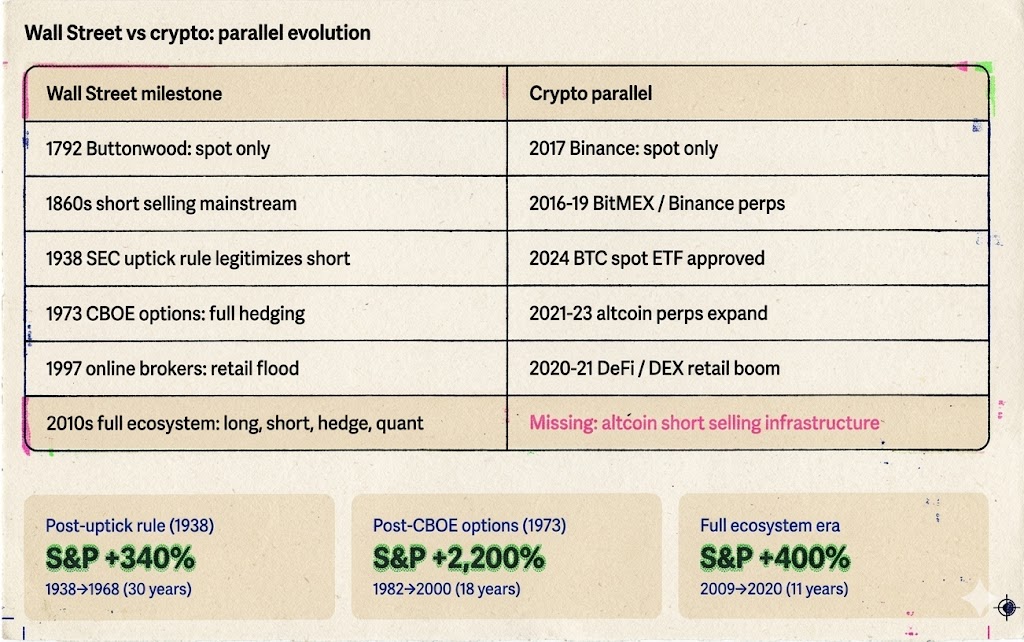

On May 17, 1792, 24 brokers signed the "Buttonwood Agreement" under a sycamore tree on Wall Street, agreeing to trade stocks with each other. This was the precursor to the New York Stock Exchange (NYSE).

The market at that time was similar to today’s altcoin market: you could only buy, hold, wait for dividends, and wait for the New Year. No leverage, no short selling, no standardized settlement process. Daily trading volume may have been less than $500,000, with only a few dozen participants. The market was tiny because there was too little to do.

Price fluctuations were entirely driven by bullish sentiment. News comes, everyone buys, and prices soar. News turns bad, everyone wants to sell, but due to the shallow market, they can't sell, and the price crashes. There are no shorts buying to cover the drop, so the market lacks natural support, and the bottom completely depends on when the last bull gives in.

Does this resemble the 2024-2025 meme, high FDV, low float altcoin market?

1850-1860s: Short Selling Takes Center Stage - Fear and Prosperity Arrive Simultaneously.

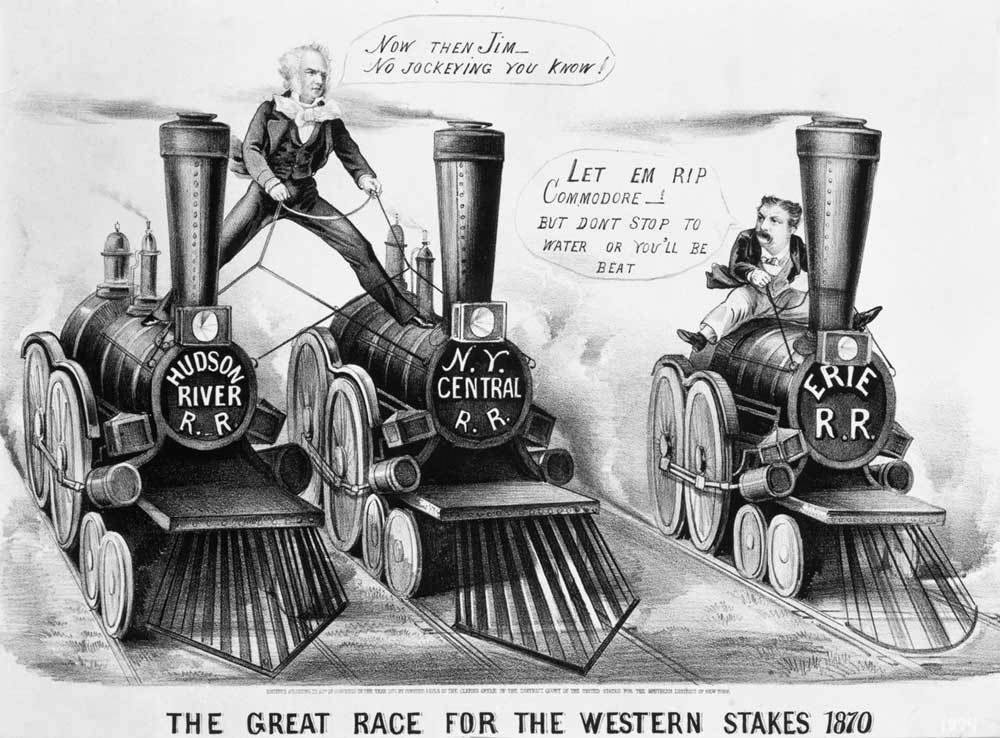

In the 1830-1840s, a trader named Jacob Little made a fortune by short selling and was dubbed "Wall Street's first great bear." But short selling truly became a mainstream weapon in the decade before and after the Civil War.

Daniel Drew, Jay Gould, Cornelius Vanderbilt—these names defined Wall Street during that era. They engaged in a series of epic battles around railroad stocks: Drew shorted Erie Railroad, and Gould and Fisk joined forces to target Vanderbilt's long positions. These battles were brutal, chaotic, and full of fraud, but the objective result was—short selling transformed from a secret weapon of the few to a standard tool of Wall Street.

The societal response mirrored that of Holland in 1609. Congressional representatives decried short sellers as "enemies of the state," and newspapers described them as profiting from others' misfortune. Public fear of short selling has hardly changed over the past four hundred years.

But the market's response has also been the same as four hundred years ago, vigorous and enthusiastic:

Every short sale creates a sell order while also creating a future buy order that will inevitably occur (short covering). Trading volume increased, spreads narrowed, and more people were willing to participate. Wall Street began transforming from a small circle of dozens into a true capital market.

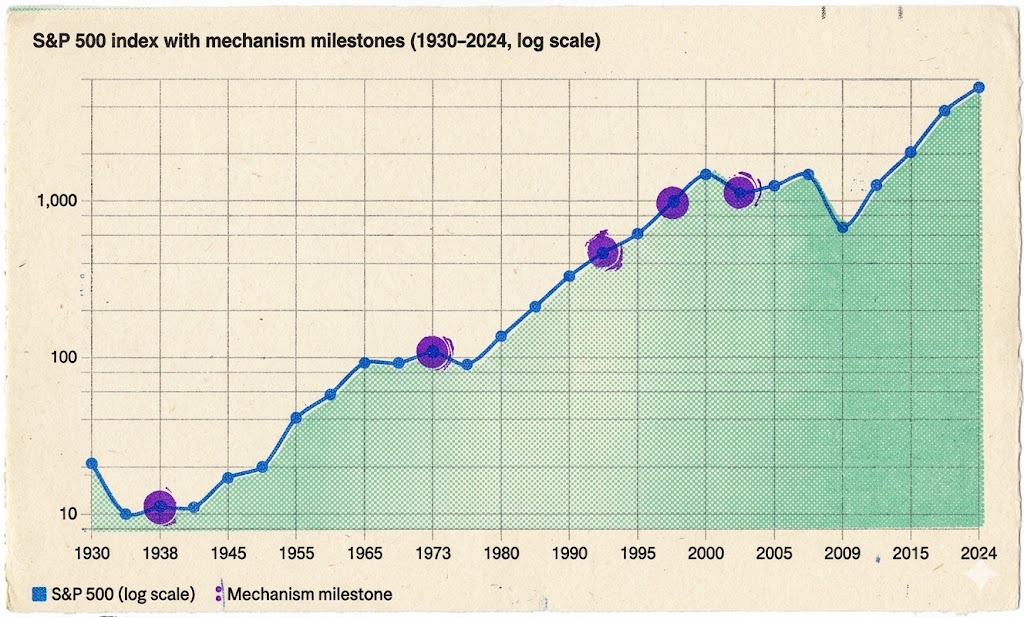

The Great Crash of 1929 → Uptick Rule of 1938: The Pinnacle of Fear and the Turning Point.

In October 1929, Wall Street crashed. The Dow Jones Index fell by nearly 90% within two years. Public outrage needed an outlet, and shorts became the most convenient target—even though the real culprits were the insane leverage bubbles and systemic failures in the banking system.

In 1934, the Securities and Exchange Commission (SEC) was established. Short selling once again faced the danger of being entirely banned. But the SEC made a historic choice: in 1938, instead of banning short selling, it introduced the "uptick rule" (Rule 10a-1) — allowing short selling only when stock prices were on the rise to prevent bears from hammering prices down consecutively.

The significance of this choice cannot be overstated. It established a principle that continues to this day: short selling should not be destroyed, but regulated. Regulations are not the enemy of short selling; they are the premise for its legitimacy.

With regulations, short selling was no longer a gray area. Institutional funds, which had previously been wary of short selling, now dared to participate on a large scale with the protection of legal frameworks. Regulation did not kill short selling; it made short selling safer and more credible, attracting more capital into the market.

This lesson has yet to be genuinely learned by the crypto market today.

1973: Standardization of Options - Turning from One Direction to Four Directions.

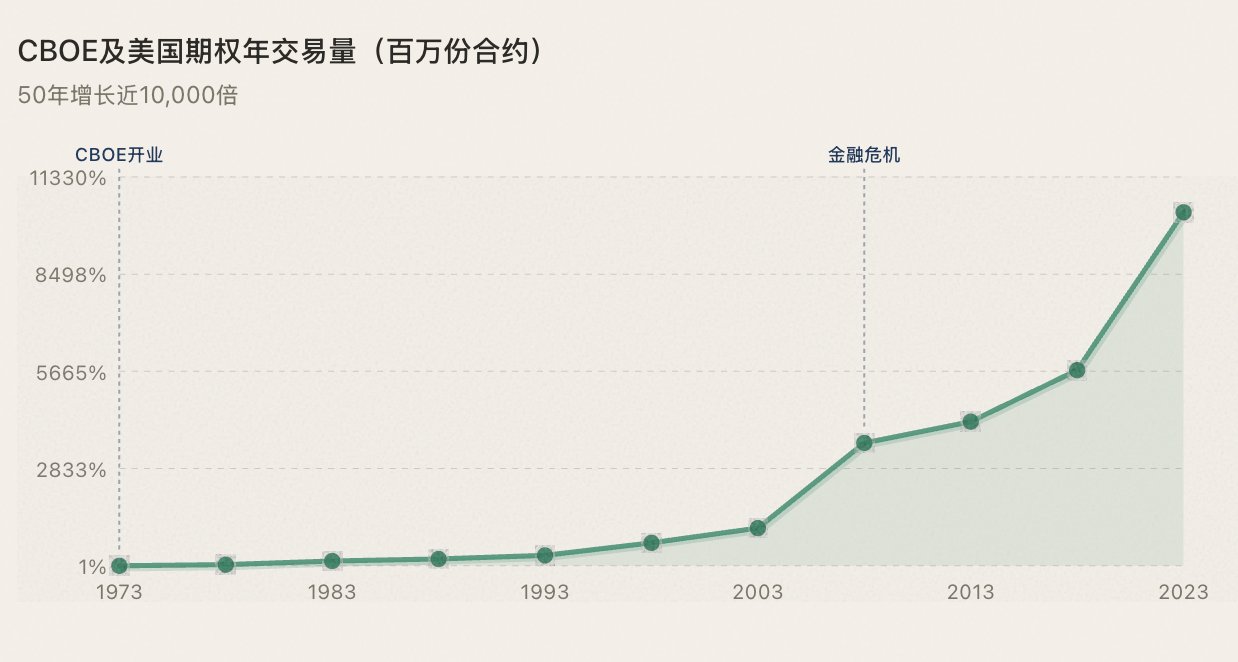

On April 26, 1973, the Chicago Board Options Exchange (CBOE) opened. On the first day, only call options on 16 stocks were tradable. Put options were added in 1977. In the same year, Fischer Black and Myron Scholes published the Black-Scholes option pricing model, which changed financial history, providing a mathematical foundation for options trading.

The significance of options lies in: it expanded the dimensionality of market games from two (buy/sell) to four (buy up/buy down/sell up/sell down). For the first time, investors could express their judgments about the market in a very precise way—not just "go up or go down," but "when, at what speed, by how much up or down."

More critically, options provided institutional investors with a complete arsenal for hedging. The great bull market of the 1980s (the S&P 500 rose over 2200% between 1982-2000) was directly ignited by Volcker controlling inflation, Reagan's tax cuts, and deregulation, but options provided the risk management infrastructure that made institutions brave enough to increase their positions. When they could hedge, they dared to go long; as more people went long, more capital flowed in, and the bull market arrived.

For the wealthy and institutional investors, controlling drawdown is more important than how much they can earn—uncontrollable risks mean large funds cannot enter.

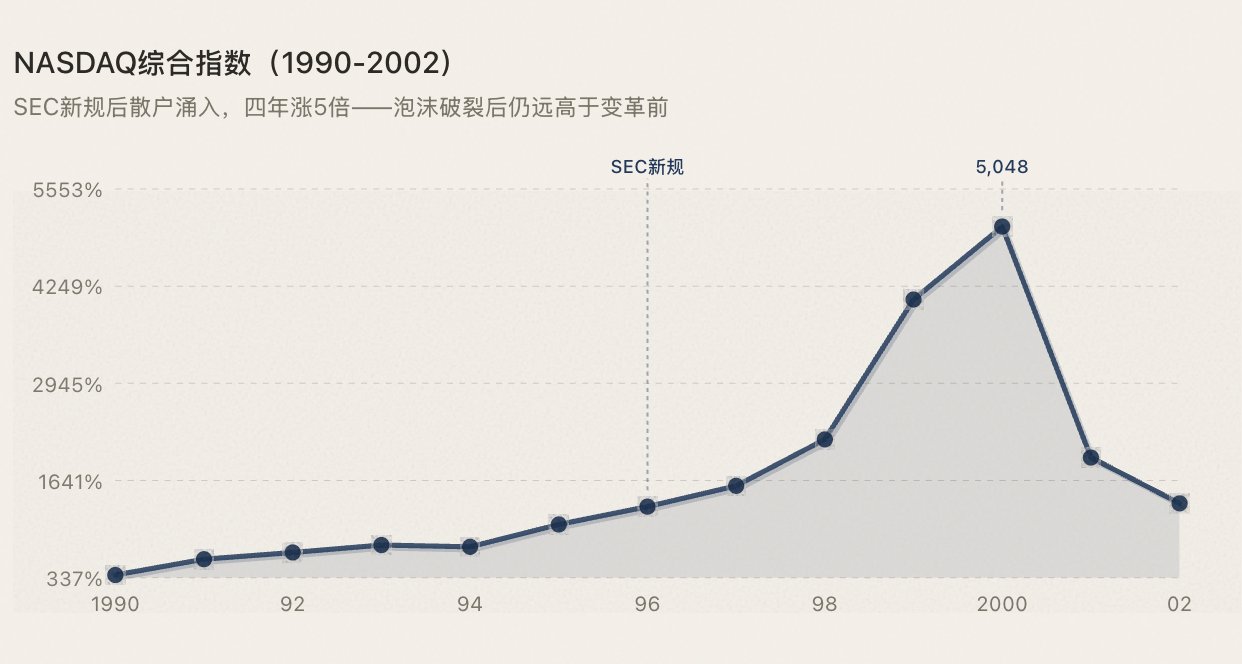

1996-1997: Retail Investors Break In.

NASDAQ has been an electronic trading platform since its establishment in 1971—the first in human history. The real transformation that occurred in 1996-1997 involved two things: SEC's Order Handling Rules broke the market makers' monopoly on quotes; and online brokers (E*Trade, Ameritrade) pushed trading commissions down from $50-100 to below $10.

The bubble eventually burst, but NASDAQ's market value still remained much higher after the bubble than it was before the transformation—because the increase in participants due to infrastructure upgrades is irreversible.

1993-2010s: Maturity of a Complete Ecosystem.

Many people think ETFs are a product of the past decade, but the first ETF—SPY (tracking the S&P 500)—was listed on US stock exchanges in 1993. In 2001, the SEC mandated decimalization of quotes, reducing the bid-ask spread from $0.125 to $0.01, significantly lowering trading costs. Between 2005 and 2010, high-frequency trading (HFT) surged, accounting for over 60% of US stock market daily volume at one point. Quantitative strategies, ETF arbitrage, long-short hedging—all strategy types had standardized tool support.

By this point, the toolset for games in the US stock market was fully matured. Long, short, hedged, arbitraged—each type of strategy could find suitable entry methods for funds. The result:

In fact, the law is clear: whenever a new trading mechanism allows more people to participate in more ways, prosperity follows. (As shown in the figure below)

3. Eight Years in the Crypto Market: Two Hundred Years of Evolution Completed in Eight Years

The mechanism upgrades completed by Wall Street in two hundred years took less than eight years from Binance's launch in 2017 to the maturity of perpetual contracts. But when it comes to the layer of altcoins, it got stuck.

2017 - The Sycamore Tree Moment

Binance was launched, but only spot trading was available. What could be done was the same as the brokers in 1792: buying, holding, waiting for prices to rise.

The ICO bubble reflected this best. Everyone was buying, and prices could only rise. Then the buying dried up—in a market without shorts, there is no natural support without short covering, and prices free fall; the bottom depends on when the last bull gives up. Altcoins completely crashed. This was exactly the market characteristic of the sycamore tree era in 1792.

2016-2019 - Short Selling Tools Debut.

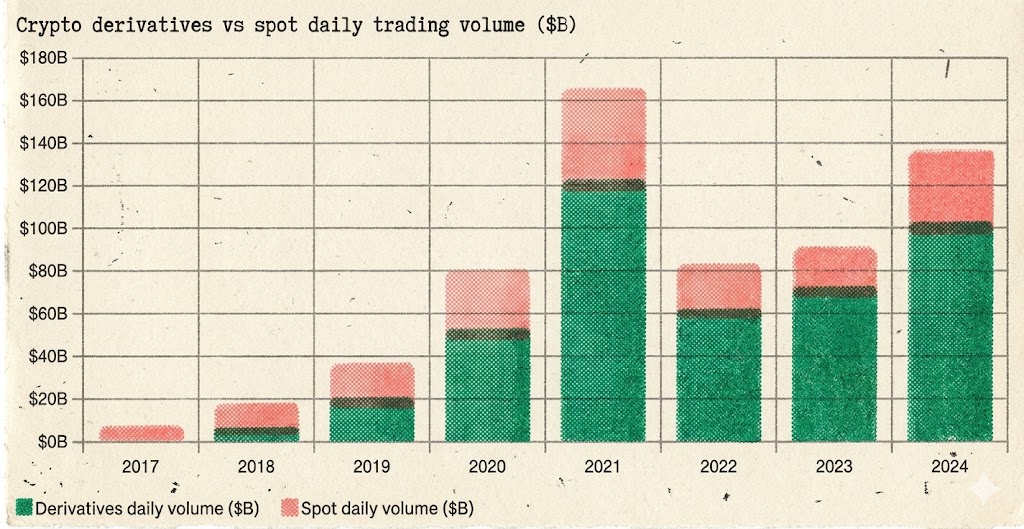

In May 2016, BitMEX launched the XBTUSD perpetual contract—the first short selling tool in the crypto market. In September 2019, Binance launched the BTC/USDT perpetual contract, mainstreaming short selling.

What happened? The same thing that happened in Wall Street when short selling was introduced in the 1860s: liquidity surged, price discovery became bidirectional, and volatility structurally decreased.

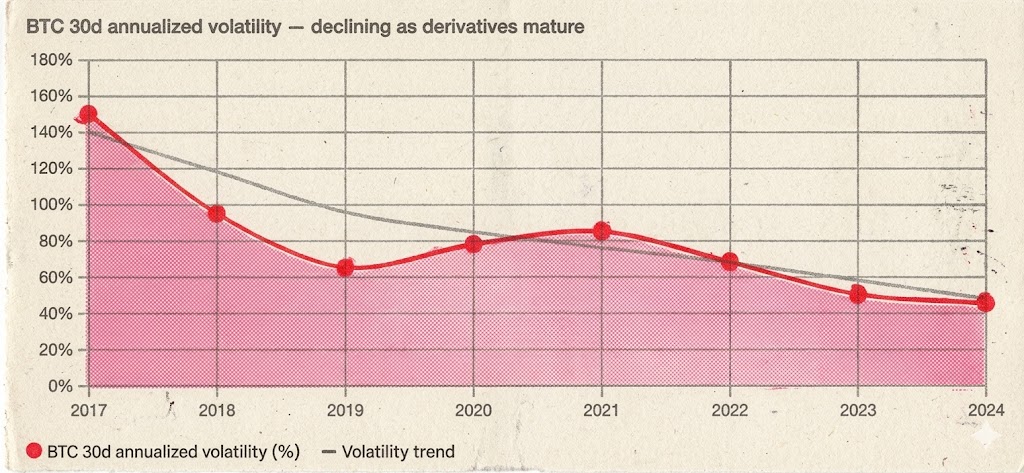

The 30-day annualized volatility of BTC dropped from over 150% during the 2017 bull market to 60-90% during the 2020-2021 bull market—prices surged more, but the volatility became more orderly. While there were still spikes and dips, instances of "three months of descending on low volume" significantly decreased, because shorts would cover at certain price levels, forming natural support.

More importantly, the amount of capital underwent a leap. With hedging tools, institutional capital was willing to enter on a large scale. You cannot expect a fund manager managing several billion dollars to throw money into a market that can only go long and cannot hedge. Perpetual contracts not only provided retail investors the rights to short sell; they furnished the entire market with infrastructure that allowed institutions to come in.

The proportion of derivatives in total trading volume rose from less than 10% in 2017 to about 90% in March 2026—derivatives have completely dominated the pricing power in the crypto market:

Short selling did not kill BTC. Short selling transformed BTC from a $10 billion speculative asset into a $2 trillion asset class.

2020-2021 - DeFi Summer: Not Just a Narrative, It's Mechanism Evolution Itself.

The options market for BTC and ETH rapidly matured in 2020-2021 (mainly Deribit). This was the crypto market's "CBOE moment of 1973"—institutions not only could short sell but also hedge accurately and construct structured positions. The dimensions of strategies expanded from two-dimensional to higher dimensions.

Moreover, many people classify DeFi Summer as a "narrative"—like the NFT boom or the metaverse concept, just another wave of hype. However, this is a fundamental misunderstanding. The essence of DeFi Summer is not narrative; it is a structural leap in trading mechanism.

AMMs (Automated Market Makers) rewrote the underlying logic of trading. Before Uniswap, trading required order books, market makers, and centralized matching. AMMs overturned all that—anyone could create a liquidity pool with two tokens, and anyone could trade instantly without needing counterpart orders or any permission. This is not a narrative; it is a paradigm shift in trading infrastructure. It allowed thousands of previously impossible long-tail tokens to finally gain liquidity.

Lending protocols created on-chain leverage and circular strategies. Aave and Compound allowed users to collateralize assets to borrow another asset—this is essentially on-chain margin trading. More critically, it birthed "circular loans": collateralizing ETH to borrow stablecoins, using the stablecoins to buy more ETH, then collateralizing again... This strategy is what traditional finance calls leveraged long, while in DeFi it was packaged as "yield farming," but the underlying logic is exactly the same—it is a new way of playing that enabled participants to engage in the market with more-dimensional strategies.

Composability allowed mechanism innovations to accumulate exponentially. AMM + lending + liquidity mining + cross-protocol arbitrage—these combinations of "money Legos" created strategic spaces that never existed in traditional finance. Each new combination represents a new form of participation, and every new form of participation brings in new capital and new users.

Thus, the super bull market of 2020-2021 was not the result of adding two factors together, but three: BTC and ETH's perpetual contracts/options provided institutions with an entry and exit channel, DeFi's AMMs and lending protocols brought about a qualitative change in on-chain trading mechanisms, and narrative was merely the surface wrapping of these two layers of mechanism evolution.

Again validating the same law: every evolution of trading mechanisms spawns the next round of prosperity.

2021-2023 - Perpetual Expansion of Altcoins

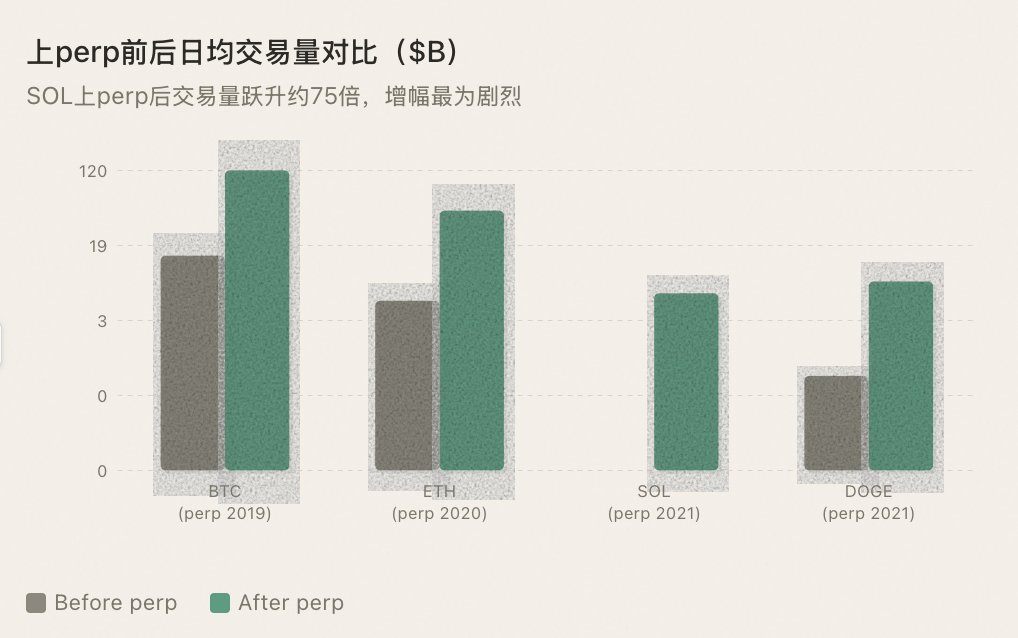

Binance began offering perpetual contracts for an increasing number of altcoins. For every new coin listed as a perp, trading volume would experience a step increase—not because "listing as perp" is good news, but because the introduction of short selling tools allowed funds of more strategy types to participate.

Quant funds could make markets, hedge funds could arbitrage, trend traders could short. The diversity of participants directly equals the depth of liquidity.

The pattern continues to hold: when BTC has a perp, it welcomes a big bull market; ETH does too; SOL does too; every altcoin that added perp experienced a liquidity leap.

2023-2025 - The Moment When the Law Fails

Then, if there are no surprises, there will be surprises; turning a corner and encountering "obstruction," just a hindrance.

In the second half of 2023 to Q3 2025, Binance will provide perpetual contracts for altcoins at an unprecedented speed. Almost every week, new perp trading pairs will be launched—from mainstream public chain tokens to AI concept coins, from GameFi to memes, even some projects with only a few million in market capitalization have obtained perpetual contracts.

On the surface, this appears to be a continuation of historical laws: providing more assets with short selling tools creates more liquidity, attracting more participants. Furthermore, objectively speaking, these perps do indeed create liquidity out of thin air—projects with tens of billions of FDV but actual circulating market caps of only a few million can't support decent trading depth solely relying on the spot market. Perpetual contract market makers provide two-sided quotes with stablecoins, effectively injecting a layer of synthetic liquidity into these paper-thin markets.

But this time, the law does not work.

The issue lies in the disconnection between "liquidity" and "confidence." The premise of creating liquidity is that someone is willing to engage in the game. However, the reality of 2024-2025 is that—everyone is afraid. The current market sees listing as perp as the endpoint, as an exit signal, as news trading.

Retail investors are scared. After experiencing FTX's explosion, Luna's crash, and countless rug pulls, retail trust in altcoins has plummeted.

More critically, many newly added perp projects have deformed token economics: tens of billions of FDV paired with extremely low circulation means a massive amount of tokens are waiting to unlock and crash the price. Retail investors are not fools—if you give me short selling tools, but the underlying itself is a designed chronic bloodletting machine, why should I participate? Whether going long or short, I don't want to touch it.

Market makers are scared. This is the most crucial point.

Providing perpetual contracts for a project with daily spot trading volume of only a few hundred thousand dollars carries high risk. Liquidity is too thin, prices are easily manipulable, and market makers' inventory risk is challenging to hedge. When extreme conditions arise, market makers cannot offload the orders they receive. After a few missteps, market makers began to tighten quotes, widen spreads, reduce depth, and even exit entirely. Without market makers willing to engage in a perp, liquidity is just a shell.

Worse still, the altcoin perpetual contracts that are still operational have become private casinos for the major players.

With small circulating caps and concentrated chips, major players can nearly do as they please in the perp market. Pumping does not require too much capital—manipulating the spot market raises prices while simultaneously harvesting a wave of short liquidations on perp. Dumping is just as convenient—open a short on perp first, then dump the spot, allowing the shorts to profit. Repeating this back and forth, the high leverage of perp has become a tool for major players to amplify returns, rather than a weapon for retail investors to hedge risks.

This kind of gameplay is far more destructive than control on the spot market. In the spot market, the major players deceive retail investors taking the positions; on perp, they are harvesting both sides of bulls and bears—regardless of whether you go long or short, as long as you stand opposite the major player, your margin becomes their profit. Experienced traders dare not touch these altcoin perps, while inexperienced traders coming in will leave after being harvested repeatedly.

Originally, short selling tools should serve to constrain major players. But in the altcoin perp market, the relationship has reversed: short selling tools have become another knife in the hands of major players. The destruction is not limited to a single coin's ecology, but rather the trust of the entire crypto market. Every trader who has been hit in the altcoin perp market is one user permanently lost to the cryptocurrency market.

A paradox has appeared: Binance is listing more and more perps, but trading volume and activity in the altcoin market are shrinking instead.

What does this indicate? The mechanism upgrade of perpetual contracts for altcoins has hit a ceiling. Perps require market makers, oracles, funding rates, and centralized approvals to function. BTC and ETH can afford to support this machine, but thousands of long-tail altcoins cannot—machines may be running, but they have run out of fuel. And those that barely keep running have instead become cash cows for major players.

4. Why Perpetual Contracts are Destined to Fail for Altcoins

The experiment from 2023-2025 has already provided results; here’s an explanation from a mechanism perspective as to why.

The death spiral of liquidity. Perps require market makers to provide dual-sided quotes with stablecoins. Who would want to make a market for an unknown project with daily trading volume of a few hundred thousand? Without market makers, there is no liquidity; without liquidity, there are no traders; without traders, market makers won't come back. Spot leverage short selling doesn’t need to construct a derivatives market from scratch—just borrow the tokens and sell them in existing DEX pools. Lending protocols provide supply, AMMs provide execution, and the two are decoupled.

Two prices, two worlds. Perps and spot are two separate pools; when they are thin, a single trade can pull the spread to absurd levels. You think you're shorting this project, but you're gambling in a parallel universe disconnected from spot. Spot leverage always operates in a single market, there is no disconnection.

Funding rates are manipulated. Major players inflate perp prices to create extreme funding rates, causing shorts to be liquidated every few hours; even when their direction is correct, they can be ground down to nothing. What's worse is that major players simultaneously operate both spot and perp—pumping the spot, then harvesting shorts' liquidations on perp. Spot leverage only has borrow rates determined by supply and demand, not distorted by the long-short ratio.

Synthetic positions do not create real selling pressure. This is the most critical point. When shorting on perp, there will be no sell orders in the spot market. Major players can juggle positions from left hand to right hand in the spot, leaving perp shorts with zero threat. Spot leverage short selling involves borrowing real tokens to sell in the spot—real selling pressure directly influences prices, and major players must shell out real money to maintain high prices.

Approval + Oracles. Perps require trading platform approvals and reliable oracles, both of which smaller coins lack. On-chain lending for short selling does not require approvals, and liquidation prices depend on AMM real-time prices.

Perpetual contracts are heavyweight infrastructure, and their operation costs exceed the value they can create for long-tail assets. What altcoins need is the lightest way to short—borrow tokens, sell them, buy them back when they drop. That is the spot leverage borrowing short selling.

5. Fear of Shorting, or Fear of No Price Discovery?

From Amsterdam in 1609 to Wall Street in the 1860s to Crypto Twitter in 2024, people's fear of short selling has never changed. "Short selling crashes markets." "Short selling is a malicious attack." "Short selling drives markets to collapse."—for four hundred years, the wording has remained almost unchanged.

But four hundred years of history has also repeatedly proved the same fact: the cost of fearing short selling is far greater than short selling itself.

When criticism is not allowed, praise becomes meaningless. When short selling is not allowed, going long will also lose meaning.

Because in a market that can only buy, prices reflect only half of the optimism. The pessimistic half of information—doubts, negatives, fraud—has been forcibly silenced. Everyone can only "like," and no one can "dislike."

Such prices are distorted, fragile, and unsustainable. They are not price discovery; they are price illusions.

The ability to both go long and short is the most basic respect for price discovery.

And with real price discovery, markets have a chance for durability. Institutions are willing to participate because prices are credible; market makers are willing to participate because both sides can trade; long-term investors are willing to participate because current prices have undergone the scrutiny of shorts, not lines drawn by operators.

Conversely, markets without price discovery can only rely on narratives to survive. Every heat cycle that passes results in chaos, and then awaits the next narrative to draw another wave of people in to fill the void. It is eternally this cycle, and it can never accumulate.

The greatest tragedy of the altcoin market is not that "there are too many major players," but that it lacks the basic conditions for price discovery. Without real prices, how can there be long-term value?

6. Short Selling is Not a Tool for Bearish Sentiment, but a Catalyst for Bull Markets

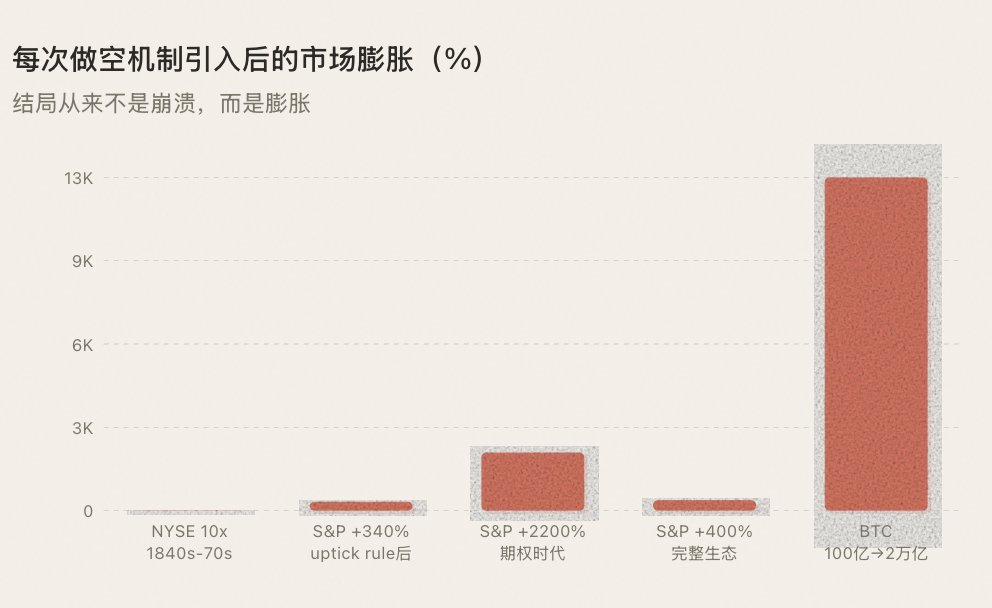

The most counterintuitive law in history: Every introduction of short selling mechanisms, in the long run, does not drive prices down, but lifts them up.

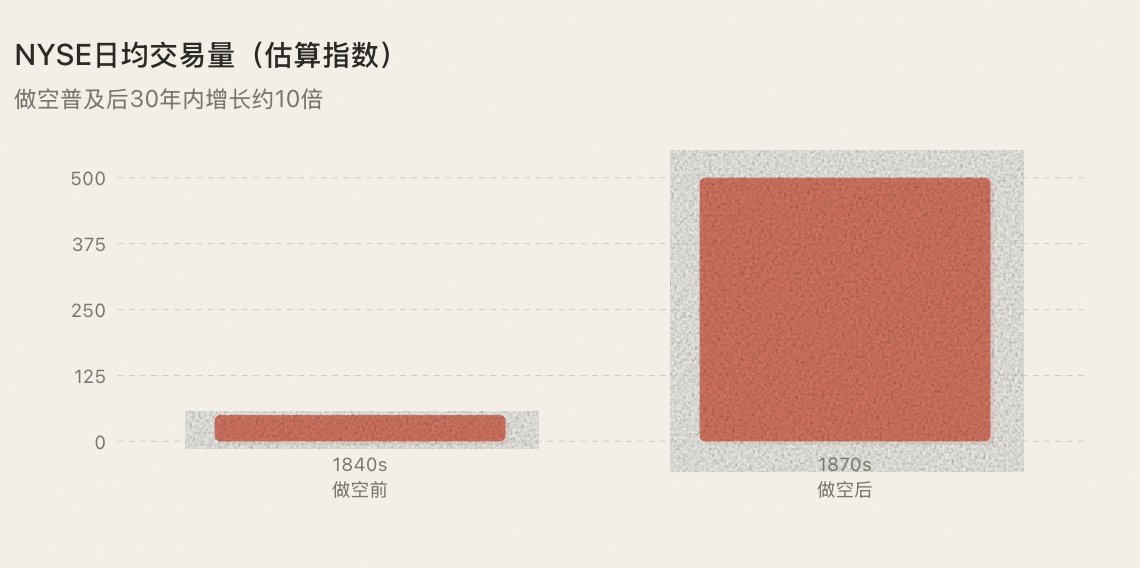

After the popularization of short selling in the 1860s, NYSE trading volume grew tenfold in ten years, transforming Wall Street from a small circle into a real capital market. After the 1938 uptick rule legalized short selling, institutional capital flowed into the market on a large scale, and the S&P 500 rose 340% over the following 30 years. After CBOE options were born in 1973, options trading volume increased 10000 times over 50 years, ushering in decades of sustained expansion in the US stock market. After the launch of BTC perpetual contracts in 2019, BTC volatility dropped from 150% to 50%, but market capitalization swelled from $10 billion to $2 trillion.

Every time, the outcome has not been market collapse, but market expansion. The reasons are three:

1. Short selling creates liquidity—every short order is both a sell order + a future inevitable buy order (covering); the more active short selling is, the deeper the liquidity.

2. Short selling attracts new participants—market makers, quant funds, hedge funds, arbitragers do not come to crash markets, but to provide liquidity, and liquidity is the oxygen of a bull market.

3. Short selling establishes trust—the prices that have survived the scrutiny of shorts are credible prices; credible prices attract real capital, and real capital pushes for real increase.

The complete toolset for gaming does not destroy confidence; it builds confidence.

7. The Path to the Next Bull Market

From Amsterdam in 1609 to the crypto market in 2025, four hundred years of financial history repeatedly validate the same law: first comes the evolution of mechanisms, then comes prosperity. This order cannot be reversed.

The current altcoin market is trapped in a death spiral: only going long → single mode → fewer and fewer people making money → fewer and fewer people trading → liquidity dries up → the market withers. Even gambling can bet on highs and lows, why must altcoins only buy and not short?

Perpetual contracts do not solve this problem—the experiments from 2023-2025 have already proven this. Perps are heavyweight infrastructure; long-tail altcoins cannot afford to support them. "Listing as perp" has become another narrative trigger, like "listing spot" or "listing Alpha," turning into a reason for news trading, detached from trading and gaming itself. Trading tools that were originally meant to serve trading have now become objects of trading themselves—in the case of long-tail assets, perps are structurally the wrong tool.

The correct path is on-chain "native spot leverage shorting"—borrowing real tokens through excessive collateralized loans and selling them in the spot market to produce real selling pressure, participating in genuine price discovery. There is no need for market makers to build the market from scratch, no need for oracles to maintain anchoring, no need for funding rates to flatten spreads, no need for anyone's approval.

This aligns perfectly with the paths of every introduction of short selling mechanisms in history. Le Maire’s short in 1609 was not approved by the Amsterdam trading platform. The margin short selling on Wall Street in the 1850s was not designed by the NYSE. They were all spontaneously created by market participants—tools came first, then rules. The SEC in 1938 did not invent short selling but established a regulatory framework for a practice that had been operating for nearly a century.

On-chain short selling protocols follow the same path.

When this happens—when an altcoin is no longer just a one-way game of "buy it, wait for it to rise," but a genuine confrontation of both bulls and bears in the spot market with real money—the quality of the market will fundamentally transform. Liquidity will return, participants will return, and capital will return. Not because there is a new story to tell but because there are new ways to play.

If historical laws continue to hold—and we have no reason to believe they won't—then the inflection point for the next altcoin bull market will not be some new narrative, a celebrity's endorsement, or a halving.

It will be an upgrade of infrastructure: allowing thousands of long-tail altcoins to gain on-chain native spot leverage shorting tools—this is where true pricing power in the crypto space lies.

This time, it won’t just be BTC liquidity overflowing into altcoins, but the other way around.

8. Conclusion

In 1609, the Dutch government banned short selling, and le Maire was publicly condemned. In the 1860s, the US Congress called short sellers enemies of the state. After the crash of 1929, the public demanded the complete elimination of short selling. In 2024, in the crypto community, "short selling" is still a dirty word.

For four hundred years, the fear of short selling has never changed.

But four hundred years of history has also repeatedly proven the same thing: every time this fear is overcome, and short selling rights are introduced into the market, the market does not collapse— it expands.

Amsterdam became the global financial center. Wall Street evolved from a sycamore tree to a trillion-dollar capital market. BTC rose from $10 billion to $2 trillion.

Now, thousands of altcoins are locked in a cage of "can only go long." Without short selling, there is no price discovery; without price discovery, there is no trust; without trust, there is no lasting prosperity. The entire market has devolved into a single game of betting on "expected outcomes"—fewer and fewer people make money, fewer and fewer people participate, and it grows increasingly quiet.

Meanwhile, those altcoins that have barely launched perpetual contracts see their short selling tools becoming new tools for major players to harvest, accelerating the loss of market trust.

When criticism is not allowed, praise will lose all meaning. When short selling is not allowed—or when short selling is just a privilege of major players—the prices will never be real.

More terrifying than the fear of short selling is a market without price discovery.

Bull markets are never waited for; they are birthed from the evolution of mechanisms. And at the core of every mechanism evolution, from 1609 to today, remains the same thing—

Returning short selling rights to the market.

Who is willing to walk with us and shout "no matter how you feel about it, you can short it" you can short it. (inspired by @heyibinance)

Original Link

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。