Abstract

The on-chain lending market is transitioning from the fringes of DeFi to become a core infrastructure. By early 2026, the total value locked (TVL) in on-chain lending protocols has reached $64.3 billion, accounting for 53.54% of the total TVL across the entire DeFi sector, establishing itself as the largest and most mature sub-field in the decentralized finance ecosystem. Aave dominates the lending space with approximately $32.9 billion in TVL, making its market leadership difficult to shake in the foreseeable future. However, on-chain lending is not without its challenges—liquidation waterfalls leading to cascading failures, systemic risks from credit defaults, and security issues with cross-chain bridges pose significant threats hanging over the industry. Meanwhile, a deeper transformation is taking place: on-chain lending is evolving from a "leverage tool for crypto natives" into a "compliance channel for traditional financial institutions." The lending scale of real-world assets (RWA) has exceeded $18.5 billion, with U.S. Treasury bonds and government securities becoming core collateral in on-chain lending, as institutional capital redefines the user structure and risk appetite in this space. This report systematically outlines the evolution of the definition, competitive landscape, core risks, and future trends of the on-chain lending market, providing panoramic industry insights for investors and practitioners. The research finds that the "one dominant player and many strong players" market structure will not change in the short term, but fixed-rate lending, compliance asset collateralization, and institutional credit assessments will become the core battleground for the next generation of on-chain lending protocols. For investors focusing on DeFi infrastructure, the Aave ecosystem (Morpho, Spark), RWA lending (Ondo, Maple), and fixed-rate innovations (Notional, Pendle) constitute three key value clues worth paying close attention to.

1. Definition Evolution: From Crypto Leverage Tool to Mainstream Financial Infrastructure

On-chain lending is not a novel concept. In 2020, Compound launched a liquidity mining mechanism that extended DeFi from the geek sphere into the public eye, marking the beginning of the "DeFi summer." At that time, on-chain lending was essentially a high-leverage tool native to crypto—users over-collateralized their crypto assets to obtain liquidity, then deployed this liquidity into yield aggregators or liquidity provision, chasing annual returns multiple times higher than traditional finance. This model operated smoothly in a bullish market; however, the 2022 collapse of Terra/Luna and the bankruptcy of FTX exposed the vulnerabilities of ultra-high collateralization and cascading liquidations. After two years of bear market reshuffling, on-chain lending has completed a critical transformation from a "leverage tool" to a "configurable infrastructure." This transformation was driven by three factors: first, improvements in the regulatory environment—the MiCA framework taking effect in the EU and the SEC's gradual acceptance of ETFs have cleared some compliance barriers for traditional funds entering the on-chain world; second, the wave of real-world asset (RWA) tokenization—real assets such as U.S. Treasury bonds, tokenized corporate bonds, and real estate rights began to serve as core collateral in on-chain lending, transforming the asset structure and user profiles of on-chain lending; third, explorations in interest rate liberalization—from initially pure floating rates to fixed-rate agreements (such as Notional and Yield Protocol) and then to hybrid interest rate systems (Pendle), on-chain interest rate pricing mechanisms have matured and begun to align with traditional financial markets.

By early 2026, the asset classification in the on-chain lending market has formed a clear three-tier structure: the bottom layer consists of stablecoin lending represented by USDC, DAI, and USDT, which is the largest and most controllable risk area, with typical LTVs reaching 80%-90%; the middle layer involves lending against volatile assets with collateral such as ETH and BTC, with LTV generally controlled at 50%-70% to cope with the liquidation risks posed by severe price fluctuations; the top layer comprises RWA collateralized lending, including tokenized U.S. Treasury bonds (Ondo Finance’s OUSG), corporate credit (Maple Finance’s private debt), and real estate rights, which are becoming a new growth engine for on-chain lending, especially favored by institutional investors seeking compliant capital entry. From a regional distribution perspective, the user structure of on-chain lending is undergoing profound changes: the Asian market is predominantly made up of individual investors and arbitrageurs, who prefer high leverage and complex strategies; the European and American markets exhibit a clear trend toward institutionalization, with higher demands for compliant custodianship, KYC verification, and audit transparency. This differentiation in user structure directly influences the functional design priorities of protocols across different regions.

2. Competitive Landscape: One Dominant Player and Many Strong Competitors with Diverging Technical Routes

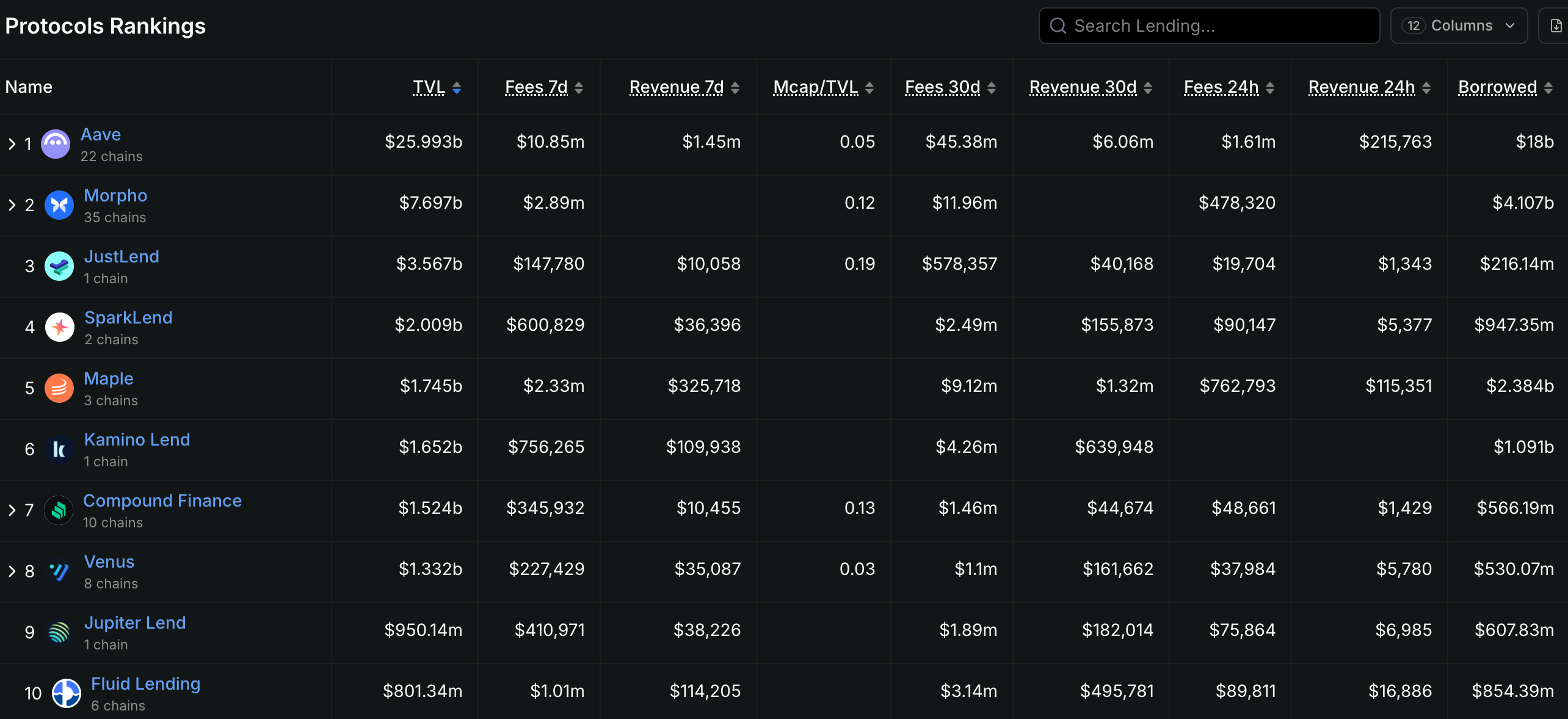

The competitive landscape of the on-chain lending market displays a typical "one dominant player and many strong competitors" characteristic. Aave, with about $32.9 billion in TVL, holds an absolute dominant position, a figure that is not only more than ten times ahead of the second-place Compound (with approximately $2.6 billion TVL) but accounts for over 50% of the total TVL in the lending sector. However, Aave’s moat does not derive from network effects or brand recognition—these are nearly irrelevant in the world of open-source protocols—but rather from its continuous technological iterations and ecosystem expansion capabilities. From Aave V1's floating interest rate model, to the introduction of credit delegation and flash loans in V2, and then to the portal cross-chain liquidity and isolation mode in V3, Aave has precisely hit market pain points with each product iteration. The V4 version is expected to launch in mid-2026, further enhancing cross-chain liquidation capabilities and an institutional-level compliance framework. In Aave’s shadow, a number of differentiated protocols are seeking their own space for survival. Morpho Labs has followed a unique evolutionary path—initially serving as an optimization layer for AAVE and Compound (enhancing capital efficiency through P2P matching), it has gradually developed independent products such as Morpho Blue (oracle-free, no-governance lending) and Morpho Vaults (yield strategies managed by professional risk planners), transitioning from an "optimization layer" to an "independent protocol." Spark Finance, leveraging MakerDAO's DSR (DAI Savings Rate) ecosystem, has established a solid user base in the stablecoin lending space, with its technological synergy with Aave V3 making it an important channel for institutional entry.

From a technical route perspective, on-chain lending protocols are diverging along three paths. The first path is the "liquidity aggregation" route (P2Pool), represented by protocols including Aave, Compound, and Kamino Finance, whose core philosophy is to pool lender funds into a shared pool, dynamically adjusting interest rates algorithmically based on utilization rates, achieving efficient capital allocation. The advantage of this route lies in ample liquidity and a simple user experience, while the disadvantage is relatively lower capital efficiency (lenders cannot directly negotiate terms with borrowers). The second path is the "peer-to-peer matching" route (P2P), represented by protocols such as Notional Finance and Myso Finance, which aims to directly match lenders and borrowers for a fixed-term, fixed-rate lending experience. This route has advantages in interest rate stability but relatively less liquidity, making it suitable for borrowers with clearly defined funding plans. The third path is the "permissionless pools" route, represented by protocols like Euler Finance (V2) and Ajna Finance, whose core philosophy is to leave risk management entirely to the market—no oracle price feeds, no governance votes, borrowers and lenders set parameters themselves, assuming risks. While this route offers a higher degree of decentralization, it also faces higher user education costs and potential smart contract risks.

3. Core Risks: The Triple Dilemmas of Liquidation, Credit, and Cross-Chain

The risk landscape of on-chain lending is far more complex than traditional finance. Unlike banking systems, on-chain protocols lack deposit insurance, final lenders from central banks, and regulatory guidance—when crises strike, the liquidation mechanism becomes the only price discovery method, and this "relentless mechanization" often amplifies drops during market panic. Liquidation waterfalls are the most typical systemic risk in on-chain lending. On March 12, 2020, known as "Black Thursday," Ethereum’s price plummeted 37% in a single day, triggering a large-scale liquidation in MakerDAO; due to a lack of liquidity, extreme instances of zero-price transactions occurred during liquidation auctions, with the actual liquidation price of ETH collateral being only 50%-60% of the market price. Similar events played out again during the May 2022 UST/LUNA collapse, with multiple high-leverage positions in Aave and Compound being forcibly liquidated, further exacerbating market selling pressure. To respond to liquidation waterfall risks, various protocols have adopted different strategies: Aave V3 introduced "Efficiency Mode," allowing borrowers to optimize collateral efficiency for specific assets; Isolation Mode places high-risk assets into independent pools to prevent the risk of a single asset spreading to the entire protocol; Ajna Finance completely abandoned oracles, using the supply and demand relationship between collateral and debt for automatic pricing, putting the responsibility for price discovery entirely in the market's hands.

Credit default risk is the second dilemma of on-chain lending. Unlike the "machine execution" model of over-collateralization, on-chain credit lending without or under-collaterization inherently faces assessment challenges. Goldfinch and Maple Finance use a hybrid model of off-chain KYC verification + on-chain settlement, scoring borrowers through real-world credit assessment agencies (such as Blackstone Credit Partners, Van Eck, etc.), addressing the issue of information asymmetry in on-chain contexts, but this "centralized endorsement" fundamentally contradicts the permissionless spirit of DeFi. In November 2022, the crypto trading firm Orthogonal Trading declared default, leaving approximately $36 million in bad debt on the Maple Finance platform, exposing the vulnerabilities of on-chain credit lending—when borrowers are institutions rather than individuals, their asset allocation and risk management capabilities can vary significantly, casting doubt on the reliability of "credit assessments." A deeper contradiction lies in the attempt of on-chain credit lending to replicate traditional finance's credit assessment system in a decentralized world, but this pathway encounters intrinsic tensions between regulatory compliance (GDPR, KYC/AML) and on-chain anonymity. Establishing an effective credit assessment mechanism while protecting user privacy will be a core issue for the long-term development of on-chain credit lending.

Cross-chain security represents the third dilemma. Aave's Portal functionality, Morpho's cross-chain deployment, and Ajna's multi-chain expansion—the cross-chain layouts of leading protocols are shifting on-chain lending boundaries from a single chain to a multi-chain ecosystem. However, the complexities introduced by cross-chain expansion exponentially magnify security risks. The 2022 Ronin Bridge attack (with losses of $625 million) and Harmony Horizon Bridge attack (with losses of $100 million) illustrate how security vulnerabilities in cross-chain bridging can impact the DeFi ecosystem. When Aave's V3 protocol brings assets from BNB Chain, Avalanche, Arbitrum, and other chains into its lending pools, these assets generally require cross-chain transfers via cross-chain bridges, whose security is often weaker than that of the chains themselves. Compounding the issue is the reliance on price oracles for cross-chain assets—if an oracle on a specific chain experiences anomalies or delays, the positions collateralized with that asset on that chain may face risks of not being liquidated in a timely manner. This "barrel effect" means that the overall security of on-chain lending protocols depends on the weakest link among all the chains to which they expand. For investors, closely monitoring protocols' cross-chain expansion strategies and bridging security is a key dimension for assessing long-term risks of protocols.

4. Innovation Trends: Fixed Rates, RWA, and Institutional Wave

Despite numerous risks, the innovation engine of on-chain lending has never stopped. Between 2024 and 2026, three forces are reshaping the game rules of this sector. The first force is breakthroughs in fixed-rate lending. The traditional P2Pool model is essentially a floating rate—interest rates dynamically adjust with the utilization of the liquidity pool, and borrowers may face surging interest costs when market rates rise rapidly. This uncertainty is unacceptable for companies and institutions seeking stable financing costs. Notional Finance was the first to launch fixed-term, fixed-rate lending products, allowing borrowers to lock in interest rates for the next 12 months or even longer at the time of loan creation, while lenders achieve term matching by purchasing corresponding yield-bearing tokens (fCash). Pendle Finance takes a different approach by tokenizing yield rights—separating future yield into "principal tokens" (PT) and "yield tokens" (YT), enabling lenders to secure certain yields by purchasing PT, while transferring interest rate risk to YT holders willing to speculate. These two routes jointly propel the process of market-based pricing for on-chain interest rates.

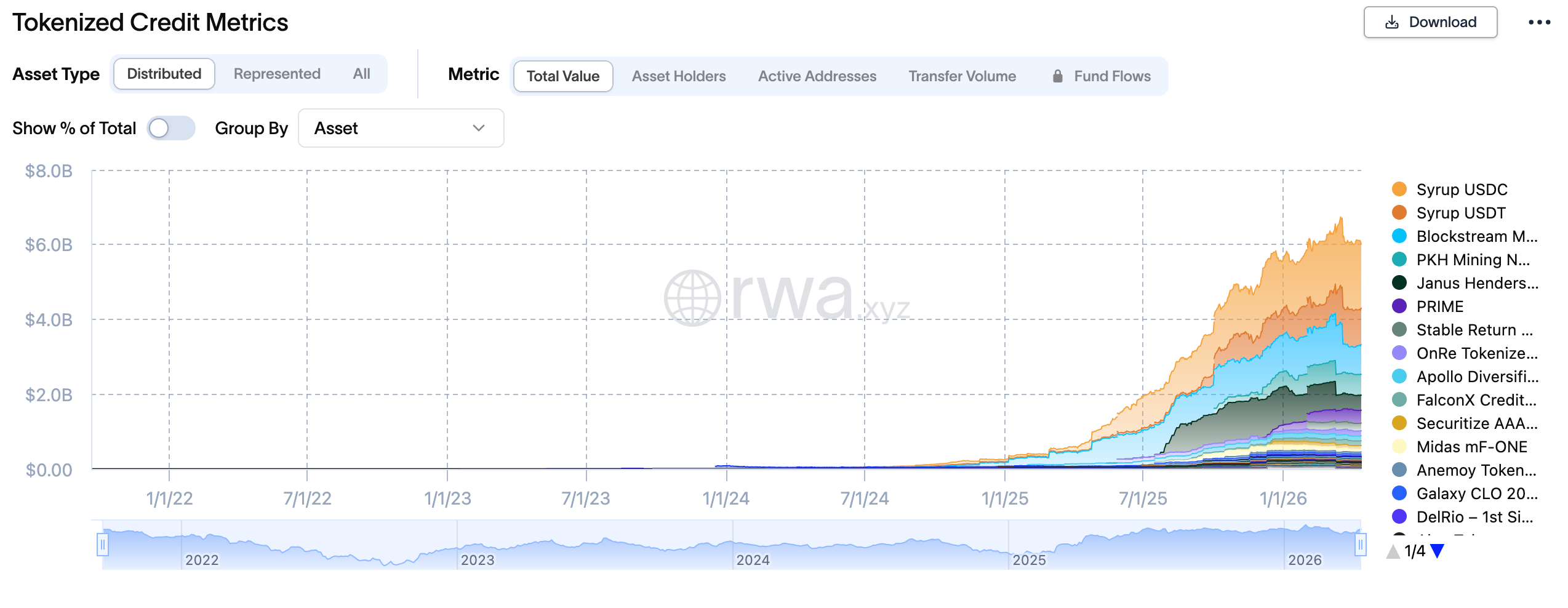

The second force is explosive growth in RWA lending. At the beginning of 2024, BlackRock's tokenized fund BUIDL surpassed $5 billion in size, and Ondo Finance's OUSG (U.S. Treasury yield token) exceeded $1 billion—these compliant assets are beginning to be introduced into on-chain lending protocols as core collateral. Compared to the extreme volatility of crypto assets like ETH and BTC, U.S. Treasury bonds have three advantages: low volatility, strong liquidity, and regulatory compliance, making them the "green channel" for institutional capital to enter on-chain lending. Protocols such as Maple Finance, Pendle, and Flux Finance have begun to support borrowing against tokenized U.S. Treasury bonds as collateral, allowing users to obtain liquidity with treasury positions while retaining treasury yields. Aave has specifically designed an "Institutional Market" for RWA assets in its V4 version, providing on-chain lending services to compliant borrowers registered under the SEC framework. By early 2026, the scale of on-chain RWA lending will have exceeded $18.5 billion, with projections to surpass $50 billion by 2027.

The third force is the accelerated wave of institutionalization. Unlike the anonymity, permissionlessness, and complex strategies preferred by DeFi natives, institutional capital demands compliance, auditability, and controllable risks. Platforms like Centrifuge and RWA.xyz have specially designed product frameworks to meet institutional needs: KYC/AML verification, off-chain credit assessments, custodial settlement, and regulatory reporting—these traditional financial infrastructures are being "transplanted" to the blockchain. A deeper transformation is that institutional entry is changing the competitive dynamics of on-chain lending. Traditional DeFi players often exploit leverage, flash loans, and arbitrage strategies to extract value from protocols, while institutional capital tends to favor a more conservative "hold-lend-hold again" strategy. This strategy difference will lead to fundamental changes in the funding structure and interest rate curves of lending protocols—more long-term locked capital, more stable interest rate levels, and lower speculative liquidations. For protocols, balancing the service of institutional users while not losing retail liquidity will be a long-term challenge.

5. Participation Strategies: Three Value Clues and Risk Reminders

For investors and practitioners focused on the on-chain lending sector, the current market provides three clear lines of value participation. The first clue is the extended investment in the Aave ecosystem. In addition to directly holding AAVE tokens, paying attention to Morpho Labs (as an independent protocol optimizing Aave, its Morpho Blue is establishing a new paradigm of oracle-free lending), Spark Finance (a stablecoin lending protocol deeply integrated with MakerDAO, benefiting from DSR ecosystem expansion), and the new features brought by Aave V4 upgrades (such as the institutional market and cross-chain liquidation) presents more risk-adjusted returns. Historical data shows that whenever Aave releases significant version upgrades or reaches historical highs in TVL, AAVE tokens often enjoy substantial excess returns.

The second clue is beta opportunities in the RWA lending sector. Ondo Finance (OUSG), Maple Finance (institutional credit), and Centrifuge (real asset financing) represent three different entry pathways into RWA. Ondo's advantage lies in its deep integration with BlackRock's BUIDL fund and the stable yield source from compliant U.S. Treasury bonds; Maple's advantage is established credit profiles from real-world institutional borrowers (such as Coinbase Ventures and Framework Ventures); Centrifuge's advantage lies in genuine demand for real asset financing with relatively low default rates. For investors seeking exposure to RWA sectors, a diversified allocation strategy is recommended to avoid the black swan risks of any single protocol.

The third clue is structural opportunities with fixed-rate innovation protocols. Pendle Finance and Notional Finance represent two different fixed-rate paths: Pendle achieves "yield separation" via yield tokenization, suitable for advanced users who understand DeFi Lego logic; Notional implements "interest rate locking" through traditional fixed-term loans, more suited to institutional users seeking stability. Notably, Pendle's TVL saw a tenfold increase in 2024, expanding from under $100 million to over $1 billion, with the high volatility of its YT token offering space for arbitrage and speculative strategies.

While chasing opportunities, three types of risks need to be closely monitored. The first is smart contract risk— the scale of TVL in lending protocols makes them high-value targets for hackers; the 2023 attack on Euler Finance, resulting in a loss of $197 million, warns us that even top protocols may have undiscovered contract vulnerabilities. The second is liquidity concentration risk—when a particular collateral (such as stETH or Lido's staked ETH) occupies too high a proportion of a protocol's TVL, extreme fluctuations of that collateral may trigger systemic liquidations. The third is regulatory policy risk—the "permissionless lending" feature of on-chain lending protocols may be deemed by regulators as an unregistered securities offering or illegal fundraising, particularly under the MiCA framework in the U.S. and EU, leading to significantly increased compliance costs. For exposure allocation, it is recommended that on-chain lending exposure be controlled at 20%-30% of overall DeFi allocations, prioritizing mature protocols that have undergone multiple audits, boast robust TVL, and possess transparent team backgrounds.

6. Conclusion: The Value of Infrastructure and Investment Clock

On-chain lending is the sector in DeFi that most closely adheres to the definition of "infrastructure." It does not seek extreme leverage ratios like perpetual contracts, relies on token incentives for false prosperity like liquidity mining, or face cyclical asset crashes like the NFT market—its value is rooted in genuine financing needs, stable interest income, and gradually established institutional trust. The $64.3 billion TVL reflects countless individuals and institutions engaged in financing, deposits, and risk management behaviors; this "grassroots finance" scale effect is DeFi's most basic yet powerful value proposition. Looking ahead, the investment clock for on-chain lending is shifting from the "proof of concept phase" to the "institutional acceptance phase." The influx of RWA assets, establishment of institutional markets, and improvement of compliance frameworks are all propelling this sector from a playground for crypto natives to an extension battlefield of traditional finance. During this transformation, finding the balance between "DeFi-native innovation" and "institutional compliance needs" will be the key determinant of each protocol's rise and fall. For long-term investors, the on-chain lending sector warrants strategic allocation, with core positions focusing on key assets within the Aave ecosystem, while satellite positions can moderately participate in alpha opportunities in RWA and fixed-rate innovations, all while maintaining respect for smart contract risks and discipline in position management.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。