Author: Connor King, Founder of Novora

Compiled by: Hu Tao, ChainCatcher

Last month, we published our report "Is Investor Relations Important in the Cryptocurrency Space?" This is a follow-up report. Based on the initial dataset of 53 protocols, we expanded to over 150 protocols, covering all major tracks: DEX, lending, perpetual contracts, liquid staking, L1, L2, bridges, DePIN, AI, stablecoins, infrastructure, and CEX tokens. The fully diluted valuation (FDV) of the protocols ranges from $40 million to $45 billion.

We examined 15 bi-directional, verifiable metrics for each protocol: Does the protocol disclose this information? Yes/No. Each data point was cross-verified through public sources: Artemis, Tokenterminal, Blockworks, Dune, DefiLlama.

We found the following:

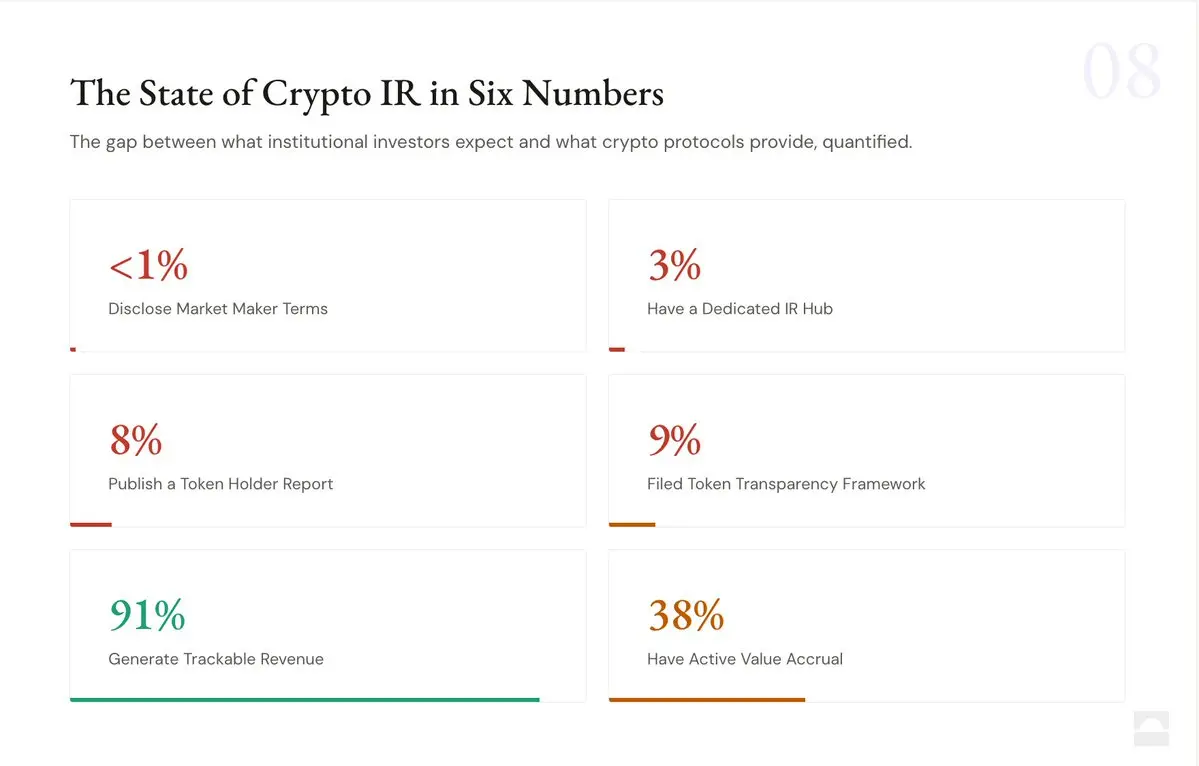

Fewer than 1% disclose market maker terms.

50 protocols. Daily trading volume amounts to billions of dollars. But only one protocol publicly disclosed its market-making arrangements.

Market makers set the terms for token trading. These protocols often include token lending, option structures, and performance incentives, all of which directly affect price discovery. In traditional markets, such important agreements are disclosed. But in the cryptocurrency market, every market participant trades under conditions of information opacity.

Meteora is the only protocol that disclosed its market-making arrangement information through its annual report for token holders in 2025. Only one among over 150 protocols.

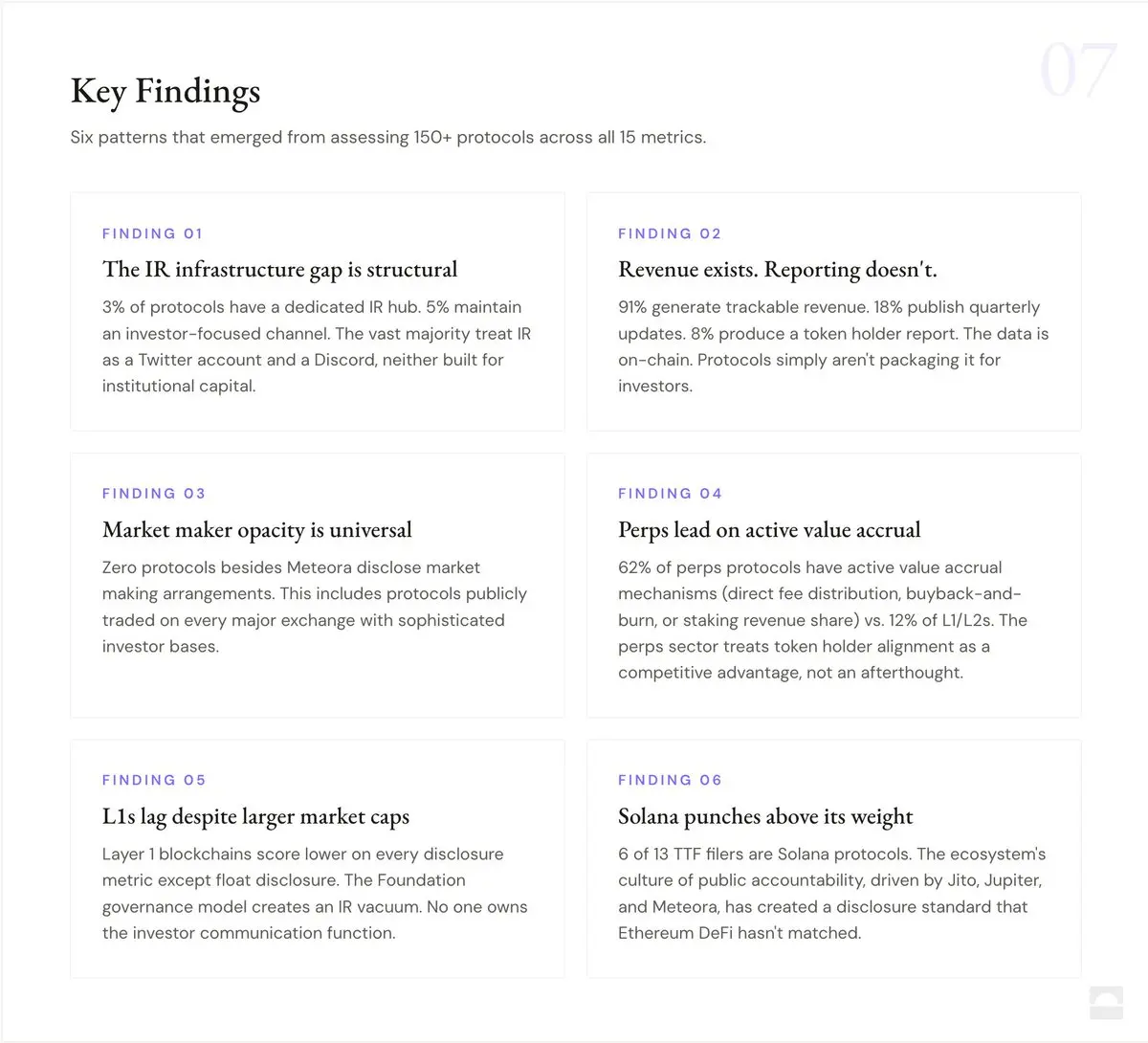

This represents the most significant transparency gap in the industry.

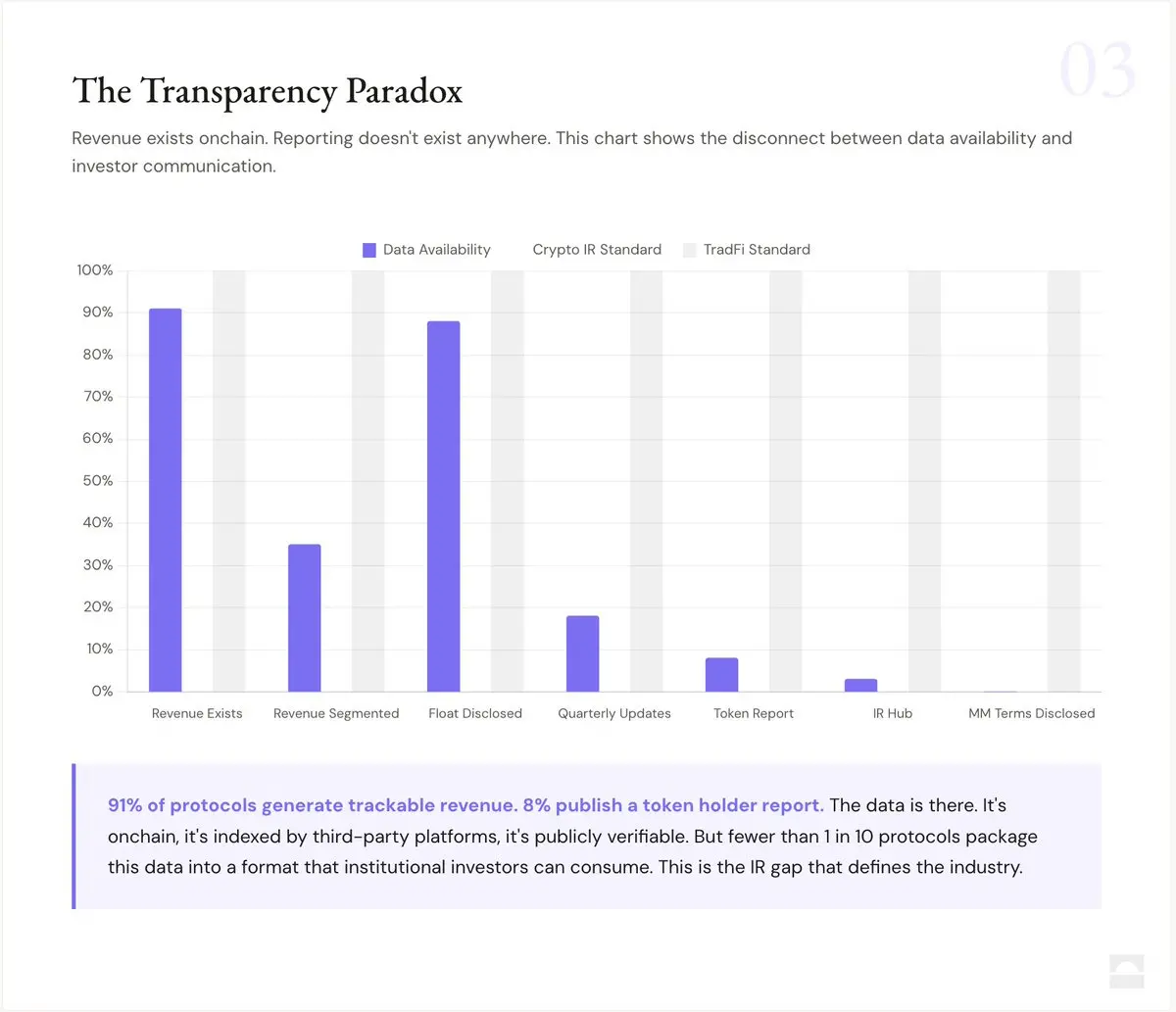

91% of companies have revenue data. 3% of companies have investor relations centers.

Almost all protocols in this audit publicly provided revenue data through third-party platforms or their own dashboards. The raw data exists.

But only 3% of companies established specialized investor relations centers that integrate this data into investor-facing experiences. Exception protocols include Meteora, Jito, Jupiter, Raydium, MetaDAO. All other protocols scatter information across blogs, governance forums, X threads, and third-party platforms. There is no centralized, institutional-level investor experience. The gap lies not in whether the data is available, but in the communication infrastructure.

9% submitted Blockworks TTF

The Blockworks Token Transparency Framework (TTF) was submitted to the SEC in June 2025, covering a total of 18 disclosure standards regarding supply, allocation, finances, and market structure, supported by Pantera, L1D, and Theia. Among the over 150 protocols audited, only 13 submitted the framework: Jito, Jupiter, Raydium, Morpho, Aerodrome, MetaDAO, Maple, dYdX, Euler, Marinade, EtherFi, Gains Network, and Meteora.

This marks substantial progress from zero submissions. However, the submission rate has declined from 25% when the initial 53 protocols were sampled to 9% among 150+. The original dataset favored early-adopting DeFi protocols for the TTF. After expanding the sample, the situation became clearer: The vast majority of protocols in the market did not choose to join. Zero L1, zero L2, and zero infrastructure protocols submitted the framework. The framework already exists, and more protocols should utilize it.

38% have active value capture, 62% return nothing

We define "active value capture" broadly: Does the protocol have at least one active mechanism that directs economic value directly to token holders (excluding governance rights)? Among over 150 protocols, we identified six different models:

- Direct fee allocation (JUP, DYDX, GMX)

- Buyback and burn (HYPE, RAY, MET)

- Staking income sharing (PENDLE, AAVE, ETHFI)

- Conditional buybacks (LDO)

- ve model cyclical allocation (AERO)

- Governance only, no economic rights (MORPHO, LINK, ARB)

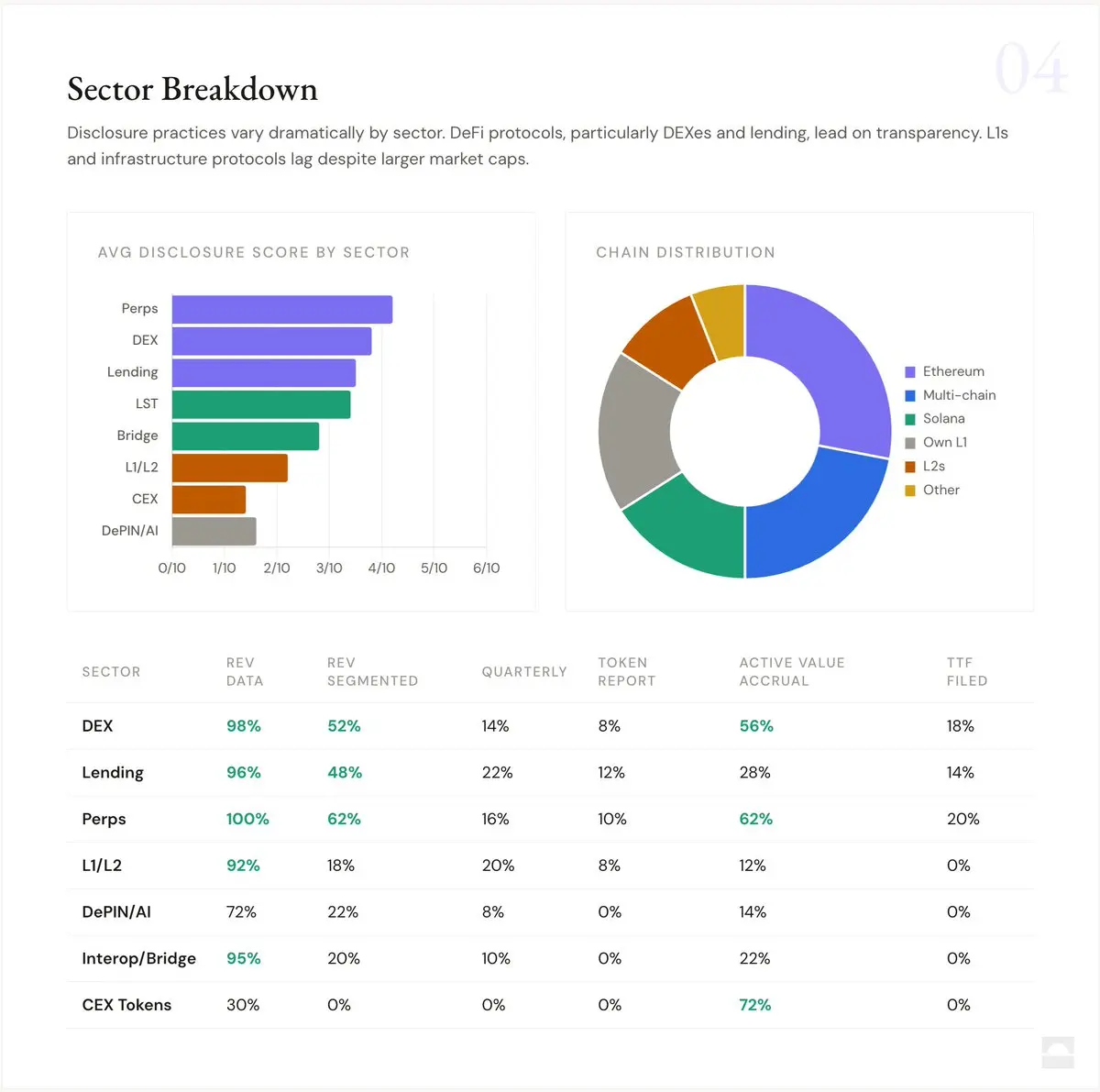

62% of the protocols fall into the last category—governance only, with no value capture tokens, including some of the largest market cap projects in the industry. The track differences are very apparent: 62% of perpetual contract protocols have active value capture, while only 12% among L1/L2 tokens. Perpetual contract tracks view aligning token holder interests as a competitive advantage, whereas L1 foundations have not yet achieved this. In-depth analysis on which models genuinely work will be released next week.

Data layer is built, communication layer is not

We reviewed five major third-party platforms: Token Terminal, Dune Analytics, Artemis, DefiLlama, and Blockworks Research. The first four platforms together cover 85-95% of the dataset. 72% of protocols appear on 4 or more platforms simultaneously. Each protocol in the audit appears at least on one platform. The raw data infrastructure aimed at institutional analysis is largely established. What is missing is the interpretation, packaging, and communication layer that converts data into investable narratives.

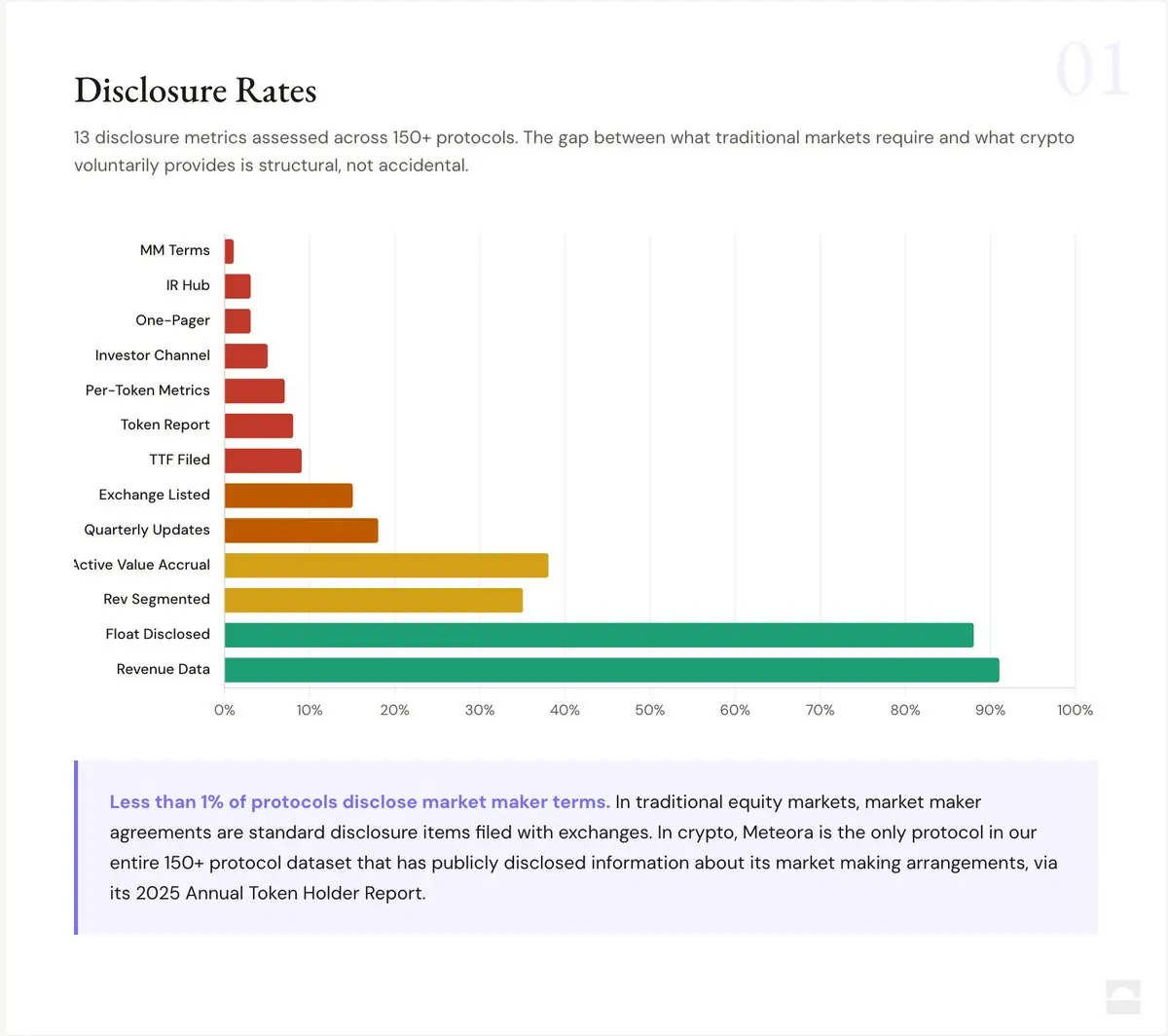

The complete disclosure status of over 150 protocols is as follows:

1% — Disclose market maker terms

3% — Dedicated IR center

3% — Provide a one-pager overview

5% — Dedicated investor channel

7% — Publish single token metrics

8% — Token holder reports

9% — Submit TTF

15% — Disclose exchange listing information

18% — Quarterly updates

35% — Itemized revenue disclosure

38% — Active value capture

88% — Disclose circulation

91% — Revenue data accessible

What this means

The argument in "Is Investor Relations Important in the Crypto Space?" still stands. As the sample size has expanded to over 150, the data becomes even more alarming. Cryptocurrency protocols are not hiding fundamentals; they are simply failing to present them. Raw inputs for fundamental analysis already exist on-chain and on third-party platforms, but the "translation layer" and IR infrastructure that converts data into institutional confidence are almost nonexistent. Only 3% have IR centers, 1% disclose market maker terms, while 91% of the market has not adopted the only available standardized disclosure framework.

The opportunity for protocols is very clear: The cost of building IR infrastructure is negligible compared to the returns from capital markets. Protocols investing in this now will be the first to gain the trust of institutional allocators. A complete interactive report containing all 150+ protocols is now live:

http://novora.co/research/ir-transparency-2026.html

Next week, we will release a comparative report in this series: "Which Token Value Capture Model Works?". This report will detail the six token value capture mechanisms we identified, their empirical performance, and what this means for token classification and institutional adoption.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。