Author: Claude, Deep Tide TechFlow

Deep Tide Introduction: The CAPE ratio of the S&P 500 has reached 39, the highest level since the internet bubble of 2000; the "Buffett Indicator" has surpassed 230%, setting a record high; the top ten constituent stocks account for over 35% of the index weight, achieving the highest concentration in modern market history. Multiple valuation metrics are simultaneously signaling overheating, but there is a significant divergence in Wall Street's judgment: one side believes that AI earnings growth supports a premium, while the other side considers this to be a classic characteristic of a bubble peak.

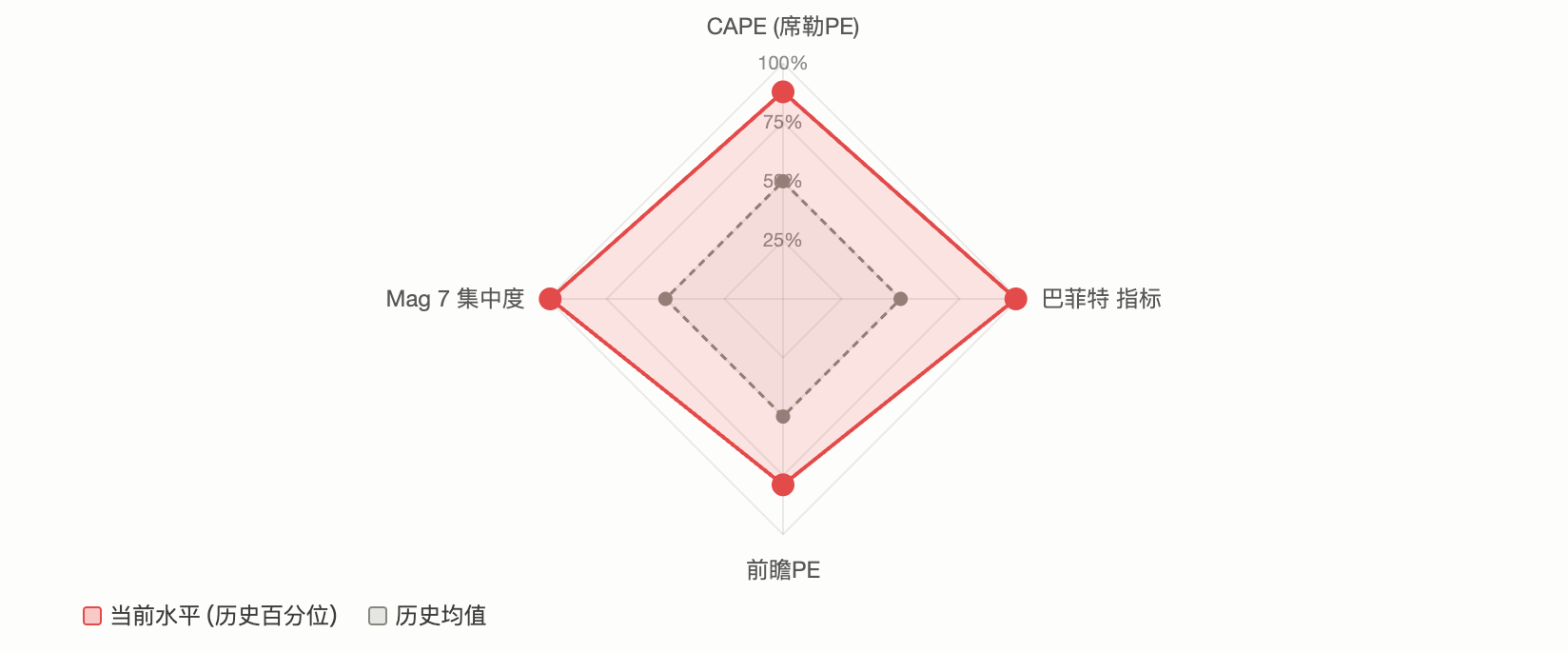

The S&P 500 is in a rare state: almost all mainstream valuation metrics are flashing red simultaneously.

The CAPE (Shiller Price Earnings Ratio) approaches 40, the highest level since the internet bubble; the "Buffett Indicator" (market capitalization/GDP ratio) has surpassed 230%, setting a new historical high; the top ten constituent stocks account for over 35% of the index weight, with market concentration at an unprecedented level in modern financial history. A post on the Reddit community r/stocks has characterized the current market as "the most overextended state in history," garnering over 2100 likes and 640 comments, with the discussion focusing on a core question:

Is this a signal of a bull market peak, or is it the beginning of an AI-driven "new paradigm"?

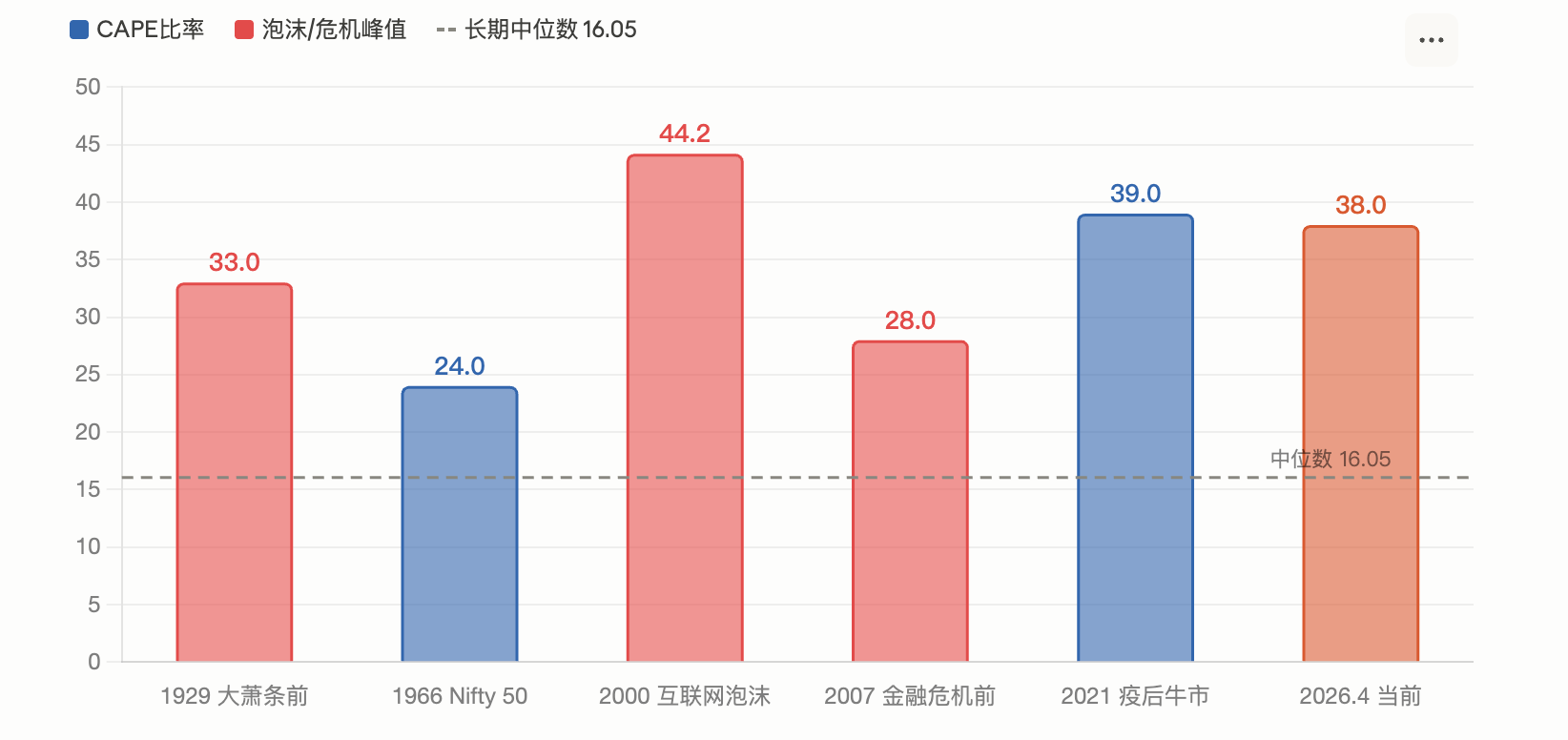

CAPE ratio reaches 39, second only to the peak of the 2000 internet bubble

The Shiller Price Earnings Ratio (CAPE) is a valuation metric developed by Nobel laureate Robert Shiller, which calculates the price-to-earnings ratio using inflation-adjusted average earnings over the past 10 years, aiming to eliminate disturbances from short-term economic cycles.

According to Motley Fool's March report, the S&P 500's CAPE ratio reached 39.2 in February. According to GuruFocus data as of April 1, the metric stood at 38.66. Both readings are at the second-highest historical level, just below the 44.2 seen at the peak of the 2000 internet bubble, while the long-term median is only 16.05.

Historically, CAPE has reached similar high levels twice: at the end of the 1920s (followed by the Great Depression) and in 2000 (after the internet bubble burst, the S&P 500 fell 49% over the next two and a half years). According to Shiller's research model, the current level of CAPE corresponds to a future annualized return of only about 2%.

The analysis from Motley Fool pointed out that Shiller himself expressed concern whenever CAPE exceeded 25, noting that there have only been three periods since 1881 where it has surpassed this level: 1929, 1999, and around 2007.

However, a report from IndexBox also acknowledges that a high CAPE does not automatically indicate an impending crash, as the metric rose over 40% after exceeding 30 at the end of 2023.

"Buffett Indicator" surpasses 230%, setting a record high in half a century

Buffett described the market capitalization/GDP ratio as "the best single measure of valuation" in a 2001 interview with Fortune magazine. He suggested that a range of 75%-90% is reasonable, and exceeding 120% signifies overvaluation.

According to Advisor Perspectives data, by early 2026, this indicator briefly reached 230.3%, the highest level on record, exceeding the trend line by approximately 2.09 standard deviations, defined as "seriously overvalued." The latest reading in March dropped to 227.5%, still the second-highest in history. GuruFocus estimates that the future annualized return of U.S. stocks over the next 8 years is around -0.3% based on this ratio.

As of April 14 according to GuruFocus data, the ratio was 219.5%. Critics argue that this metric fails to adequately consider two structural changes: first, the substantial rise in U.S. corporate profit margins compared to historical averages, and second, the increasing share of revenues of large U.S. companies coming from overseas (which inflates market capitalization but is not reflected in domestic GDP). However, supporters contend that even after detrending, the current reading remains at historical extreme levels.

Market concentration at an all-time high, Mag 7 accounts for over 30%

Valuation is just one dimension of the issue. The structural risks in the market are equally unsettling.

According to AhaSignals data from April 13, the top ten constituents of the S&P 500 account for 35.59% of the index weight, with the top five accounting for 25.97%, and the "Magnificent 7" making up 30.44%. The comprehensive concentration risk index (ACRI) compiled by this agency has a reading of 81/100, reaching a "critical" level. According to Motley Fool's April data, the weighting of Mag 7 in the S&P 500 has increased from 12.5% in 2016 to the current 33.7%.

CNBC reported in December 2025, citing warnings from Kathmere Capital Chief Investment Officer Nick Ryder: investors remain overly concentrated in Mag 7, and he suggests a more diversified allocation outside of U.S. large-cap growth stocks. Ed Yardeni, president of Yardeni Research, concurrently advised investors to underweight Mag 7 and overweight "the other 493" (Impressive 493).

The real risk posed by concentration is that when a few stocks dominate the index's movement, their decline can disproportionately drag down the overall market. The first quarter of 2026 has already begun to verify this. According to 24/7 Wall St, Microsoft, Amazon, and Nvidia have fallen approximately 20%, 9%, and 6% year-to-date, respectively, dragging the market-cap-weighted S&P 500 down nearly 4%, while the equal-weighted S&P 500 (RSP) has slightly gained during the same period.

Two camps at odds: "historical repetition" or "this time is different"

In light of this data, Wall Street's judgments have sharply diverged.

Bears base their core argument on mean reversion of valuations. Jeremy Grantham, co-founder of GMO, explicitly characterizes the current market as an AI-driven massive bubble in his latest research. He notes that the actual income from current AI investments is far outstripped by capital expenditures; OpenAI predicts its operational losses will reach $17 billion in 2026, expanding to $35 billion in 2027. GMO believes that classic signs of a bubble peak (the collapse of speculative stocks, substantial outperformance of high-quality stocks) have not fully emerged, but this only indicates that the bubble has not yet peaked, rather than it being non-existent.

IO Fund's cyclical analysis also leans towards caution. Their report points out that 2026 is simultaneously at the intersection of Gann's 60-year long cycle and the 4-year presidential cycle, while each stock in Mag 7 has already peaked between July 2025 and February 2026, and when the index reached its last new high, the core constituent stocks had begun a silent decline, which is a "classic warning signal of the end of a bull market".

Bulls, on the other hand, emphasize fundamental earnings. According to FactSet's April data, the forward 12-month price-to-earnings ratio of the S&P 500 is 20.4 times, which, although higher than the 10-year average of 18.9 times, has decreased from 22 times at the end of 2025. Analysts predict a 17.6% year-on-year earnings growth for the S&P 500 in 2026, and if this expectation is realized, the high valuation could be mitigated to some extent.

Fidelity's Global Macro Research Director Jurrien Timmer presents a relatively mild assessment: since the Iran conflict, the maximum drawdown of the S&P 500 has been less than 10%, a decline that historically occurs on average once a year. Earnings expectations continue to grow at a 17% annualized rate and have not yet been materially impacted by geopolitical headlines.

The Morgan Stanley investment management team also noted in its 2026 outlook that most bull markets last 5 to 7 years, and historically, bull markets entering their fourth year have recorded positive returns. The bank's allocation to non-U.S. equities has risen to a historical high.

BlackRock stated that the rise of technology stocks in 2025 is mainly driven by earnings growth rather than valuation expansion, and the current valuation based on growth expectations is reasonable.

Overlapping geopolitical shocks: Iran war and stagflation risk

Beyond the valuation debate, the macro environment adds extra uncertainty.

The conflict in Iran has pushed oil prices above $100 per barrel, and the S&P 500 briefly fell below the 200-day moving average in March. According to FinancialContent, the Federal Reserve maintained a "hawkish hold" at its March meeting, with the updated dot plot predicting only one more rate cut for the remainder of 2026. UBS described the recent volatility in its March 17 report as "a necessary reset of high valuations" rather than the beginning of a bear market, maintaining a target price of 7700 points by year-end.

Goldman Sachs has raised the probability of a recession over the next 12 months to about 30%. This resonates with warnings from valuation indicators: if an economic downturn coincides with high valuations, the average peak-to-trough decline of the S&P 500 historically has been 32%. However, if earnings continue to grow (with FactSet consensus expecting a 17% increase), significant corrections have historically been limited in magnitude and relatively quick to recover.

For investors, the conflicting signals have become quite clear. Long-term valuation metrics are almost universally flashing red, while short- to medium-term earnings data remains strong. The market stands at the crossroads of "valuation says no" and "earnings say yes". The outcome will depend on whether AI capital expenditures can translate into sustainable profits and whether the geopolitical shocks ultimately lead to a recession.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。