Written by: Eli5DeFi

Translated by: AididiaoJP, Foresight News

BlackRock, JPMorgan, Apollo, Société Générale, Banque de France, and many other institutions are currently trying to utilize Ethereum as financial infrastructure.

They are not buying ETH, nor launching crypto products for retail investors, nor issuing press releases discussing any "Web3 strategy".

They are using Ethereum as operational-level financial infrastructure to transfer trillions of dollars. Clearly, 99% of crypto Twitter is still busy debating whether crypto is dead or which coin to speculate on next.

Let me clarify this because it has been almost completely underreported.

First: What exactly is a Repo?

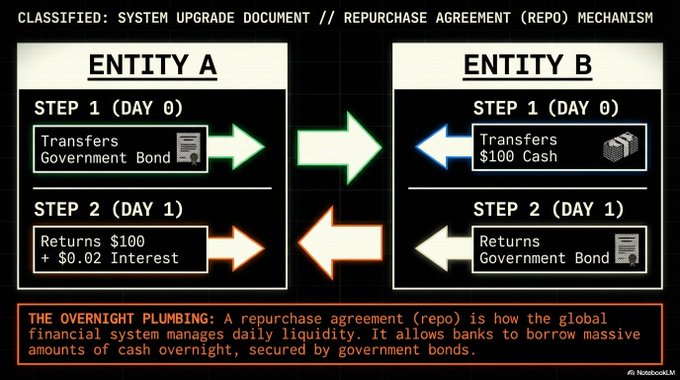

The repo agreement is actually one of the simplest transactions in finance.

Suppose you need $100 cash tonight and you have a $100 government bond. You go to a bank and say, "Today, you buy my bond for $100. Tomorrow, I will buy it back for $100.02." The bank agrees. You get the cash. They make $0.02. Tomorrow, the bond goes back to you, and the cash goes back to them.

That's a repo. The term "repo" refers to the agreement to buy back the bond, and the $0.02 difference is the interest. The government bond serves as the collateral that makes the transaction secure.

Now, scale this type of transaction to the size of the entire financial system.

Every day, banks, hedge funds, money market funds, and brokerages are running variations of this transaction to manage liquidity. A bank that just received a large deposit on Tuesday and needs cash on Wednesday will do a repo. A hedge fund requiring overnight financing for its bond position will do a repo. A money market fund with surplus cash wanting to earn some risk-free return will act as the other side of the repo.

The repo market is the overnight pipeline system of the financial system.

It is how banks maintain liquidity day in and day out. It determines how much it costs to borrow money using government bonds as collateral, and this cost subsequently affects nearly all other interest rates you encounter.

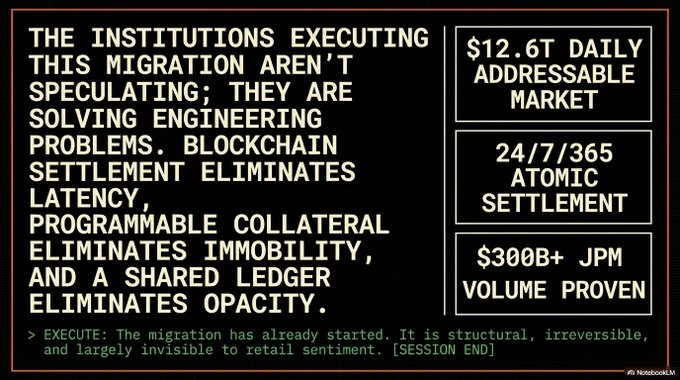

At the same time, as of the third quarter of 2025, just in the United States, this is a market with a daily trading volume of $12.6 trillion. Together with €10.9 trillion in Europe, you are looking at about $25 trillion in daily transaction volume.

For reference: In April 2026, the total market capitalization of the entire crypto market was about $2.7 trillion. The turnover of the repo market per day is almost ten times the total market capitalization of all crypto assets.

Most people who have held ETH since the inception of Ethereum have never even heard of this.

The Day the Global Financial System Nearly Collapsed

To understand why institutions are willing to spend hundreds of millions of dollars to move repos to Ethereum, you need to grasp what happened on September 17, 2019.

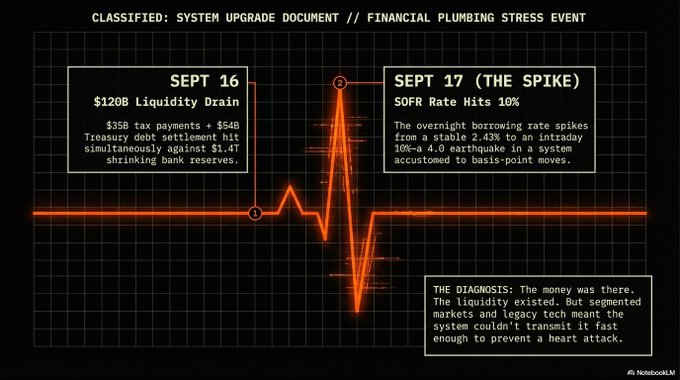

On September 16, two routine events collided:

- Corporate quarterly taxes were due. Corporates withdrew around $35 billion from money market funds to pay their taxes.

- At the same time, $54 billion of newly issued government bonds was settled, hitting the main underwriters' balance sheets all at once. These underwriters needed overnight financing for this inventory through the repo market.

These two events combined siphoned $120 billion in liquidity from the banking system in less than 48 hours.

At this point, the system's vulnerability was exposed. The Federal Reserve had been reducing its balance sheet for the previous two years, leading to a continuous reduction in reserve levels in the banking system.

By September 2019, reserves had fallen below $1.4 trillion. Withdrawing $120 billion from $1.4 trillion sounds manageable. In reality, it was not, because the money was not evenly distributed.

Some banks had plenty of money, while others had none. Moreover, at that time, there was no efficient mechanism to enable funds to flow from surplus banks to those in need.

Thus, the repo rate SOFR shot up from 2.43% on September 16 to 5.25% on September 17, spiking to 10% intraday. For a market that typically fluctuates in basis points, this was like experiencing a major earthquake in a building you thought was secure.

That's right, it was chaotic at that time.

The Federal Reserve had to urgently inject $75 billion on September 17. Daily liquidity operations continued until June 2020.

The official post-mortem concluded that two things greatly exacerbated the spike in rates: one was limited transparency (prices were not shared in real time across different segments of the repo market), and the other was market fragmentation (funds could not flow efficiently between different corners of the system).

In other words, the money existed, the liquidity was there. However, the system could not deliver it quickly enough, at the right time, to the right place.

And this particular failure point is something that on-chain settlement could inherently fix, because no other centralized infrastructure could achieve it.

Ethereum's Arrival (Quietly, without a Press Conference)

No one has officially announced, "The repo market is moving to Ethereum."

Institutional finance doesn't work that way. Instead, a series of decisions were made by almost infallible institutions, spanning 2024, 2025, and into 2026:

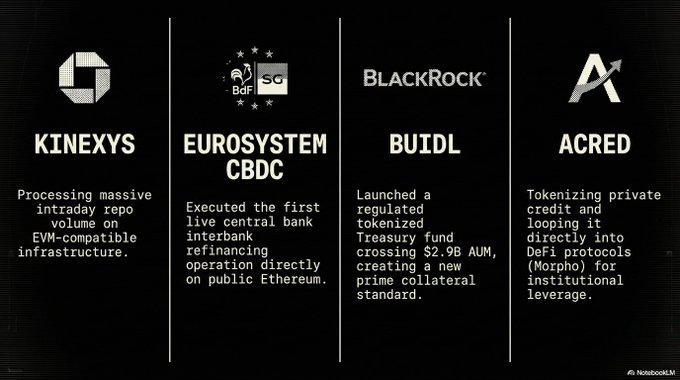

JPMorgan: Over $300 Billion in Blockchain Repo (Completed)

JPMorgan has been building blockchain-based intraday repos since 2019, back when their platform was still called Onyx (now renamed Kinexys).

The operational mechanism is this: institutions deposit tokenized collateral on Kinexys to borrow intraday funds and return cash before the close of business.

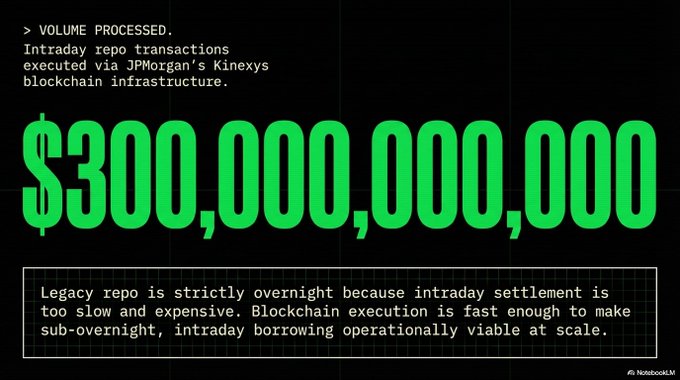

Why emphasize "intraday"? Because traditional repos are mostly overnight.

In traditional finance, intraday repos are costly and fraught with friction, so most institutions are reluctant to engage in them. However, on a blockchain, you can execute, settle, and reverse within the same trading day without significant cost burdens.

The result is:

Since its launch, Kinexys has handled over $300 billion in intraday repo transactions.

The entire platform (including repos, cross-border payments, and foreign exchange) has processed over $1.5 trillion in total transactions, with an average daily processing volume of $2 billion.

Clients include Siemens, BlackRock, and Ant International.

In December 2025, JPMorgan further doubled down, launching the tokenized money market fund My OnChain Net Yield Fund (MONY) on the Ethereum mainnet, with an initial investment of $100 million, redeemable in USDC.

JPMorgan currently has $46 trillion in assets and is the first globally systemically important bank to operate tokenized funds on a public blockchain.

Société Générale + Banque de France: The First Central Bank Repo on the Ethereum Public Blockchain (2024)

In December 2024, SG-FORGE, the digital asset subsidiary of Société Générale, executed the first blockchain repo transaction with a central bank of the Eurozone. The transaction structure was as follows:

SG-FORGE deposited bonds issued in 2020 on the Ethereum public blockchain as collateral.

Banque de France (the French central bank) issued a wholesale central bank digital currency in exchange.

The end-to-end repo took place on-chain in real-time.

Banque de France described this as proving the "technical feasibility of conducting interbank refinancing operations directly on the blockchain." In layman's terms, that means, "We tested it, it works, and we are considering using it more often."

The overnight repo market in Europe is sized at €10.9 trillion. The Eurozone is not only a participant but also a regulator in this market. The French central bank conducting real-time repos on the Ethereum public blockchain sends a policy signal, not a hackathon project.

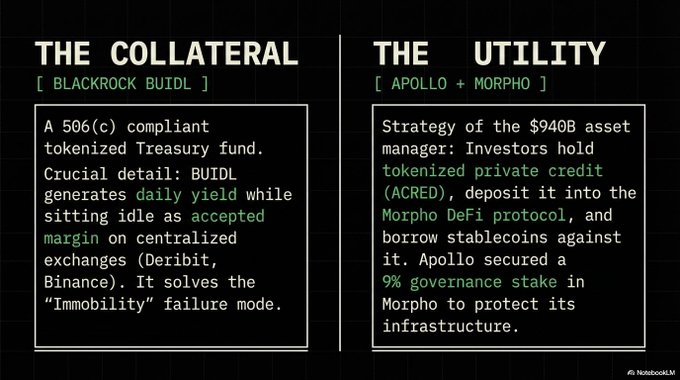

BlackRock BUIDL: Tokenized Government Bonds Are Becoming the New Collateral Standard

In March 2024, BlackRock launched its dollar institutional digital liquidity fund on the Ethereum public blockchain.

BUIDL holds short-term U.S. government bonds and cash equivalents, directly paying interest to crypto wallets daily, with nearly instant settlement. By mid-2025, its assets under management peaked at nearly $2.9 billion, capturing 42% of the tokenized government bond market.

For overnight repos, the important point is that BUIDL is now accepted as collateral by Deribit, Crypto.com, and Binance. It is also a reserve asset for the Frax stablecoin. It has been used as margin for derivatives trading. JPMorgan launched a direct competitor MONY in December 2025.

What is really happening here is that tokenized money market funds are becoming a new type of repo collateral. And they are better than traditional repo collateral because they can generate returns while being idle as collateral.

In traditional finance, if you pledge a government bond as collateral, that bond just sits at the clearinghouse without bringing in any additional returns. But with BUIDL or MONY, the returns continue to accumulate while the assets serve as collateral.

Apollo + Morpho: Private Credit Enters the DeFi Lending Stack

Apollo Global Management manages $940 billion in assets. At the beginning of 2025, they tokenized their Apollo Diversified Credit Securitized Fund through Securitize, using it as collateral deployed on the DeFi lending protocol Morpho.

This created a loop:

- Investors hold tokenized ACRED (private credit fund shares).

- They deposit ACRED into Morpho as collateral.

- They borrow stablecoins.

- They redeploy the borrowed liquidity into other chain strategies.

- They earn the spread between ACRED returns and borrowing costs.

This is a "loop" strategy. In traditional finance, to achieve this, you need to have a prime brokerage relationship and deal with a mountain of paperwork. On-chain, it’s just a matter of a few interactions with smart contracts.

This is the first time private credit funds have been used for on-chain structured products. Apollo’s own statement is, "Tokenization has realized accessibility, while on-chain financial infrastructure has created new utility."

In February 2026, Apollo deepened that commitment: reaching a partnership agreement to acquire up to 90 million MORPHO tokens (9% of the total supply) over 48 months. These tokens hold governance rights over Morpho's protocol parameters and fee structure. Apollo is not just using DeFi infrastructure; they are becoming a stakeholder in it.

Morpho currently holds over $10 billion in deposits across major EVM chains (according to Messari data). The Coinbase crypto mortgage product supported by Morpho has accumulated $1.7 billion in collateral (mainly ETH and BTC) and $960 million in active loans since its launch.

Bitwise opened a USDC yield vault on Morpho in January 2026. This is becoming infrastructure, not just a niche DeFi application.

What On-Chain Overnight Repos Solve

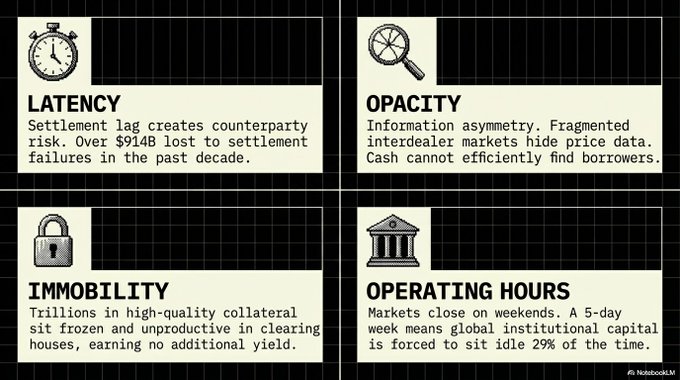

Traditional overnight repos face four structural issues:

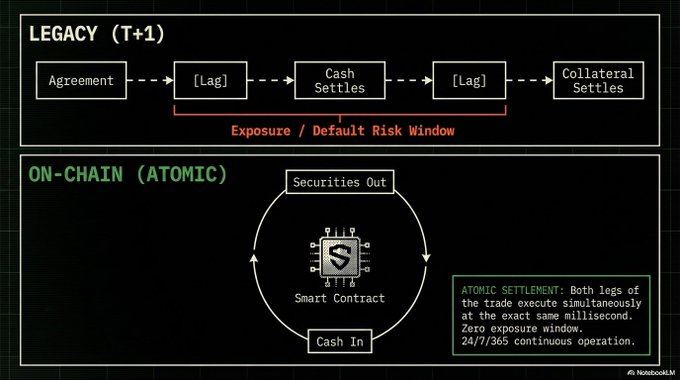

Issue One: Settlement Delays Create Counterparty Risk

In traditional overnight repos, you complete a transaction today, but the actual movement of securities and cash takes time. During this window of time, the counterparty may default, and you have nothing in hand. According to JPMorgan data, settlement failures over the past decade have cost market participants over $914 billion.

On-chain solution: Atomic settlement. In blockchain transactions, the two legs of a transaction (securities out, cash in) are settled simultaneously. They either both happen or they don’t happen at all. There is no exposure window. JPMorgan has collaborated with Chainlink and Ondo Finance to test cross-chain transactions in real-time, settling tokenized U.S. government bonds against dollar deposits across two different blockchain networks.

Issue Two: Information Cannot Flow Between Different Market Segments

The intensification of the September 2019 crisis was partly due to the fact that different segments of the repo market (triparty repos, bilateral cleared repos, inter-dealer markets) do not share price information in real time. Banks sitting on excess liquidity did not know where to place their money. Borrowers could not find cheap cash. The pipeline was clogged.

On-chain solution: A shared transparent ledger. Every transaction, every interest rate, and every collateral position is visible in real time on-chain. Market participants can read the same world state at the same time. The kind of information asymmetry that exacerbated the September 2019 crisis is structurally weakened.

Issue Three: Collateral is Frozen and Not Generating Returns

When you pledge a government bond as repo collateral, that bond is locked at the clearinghouse and offers you no other utility. In a $12.6 trillion daily transaction market, the opportunity cost of this collateral being frozen is huge.

On-chain solution: Programmable, composable collateral. A tokenized bond on Ethereum knows who it belongs to, can transfer itself when certain conditions are met, generates returns while being pledged, and can be used across multiple protocols under defined rules. BUIDL, which is used as collateral on Binance, can still generate daily returns from the underlying government bonds it holds. This was not possible before.

Issue Four: Market Has Operating Time Limitations

Traditional overnight repo markets close on weekends. Banks compress their balance sheets to beautify their quarterly reports (they will recall loans to clean up their accounts), creating predictable pressure events every 90 days. The market operates only five days a week, meaning capital is idle for 29% of the time.

On-chain solution: 24/7 around-the-clock settlement; Ethereum has no operating hours. JPMorgan explicitly promotes its blockchain deposit account as "24/7 same-day settlement". The viability of intraday repos on Kinexys exists precisely because blockchain settlement is fast enough to make borrowing shorter than overnight operationally feasible.

What This Means for ETH Assets (Three Demand Vectors)

ETH remains highly influenced by macro factors. It dropped from $2,200 to around $1,700 at the beginning of 2026 due to tariff pressures, a decrease of 23%, and trades as a risk asset under most market conditions.

This migration of institutional overnight repos will not supersede short-term price dynamics.

However, it does create structural long-term demand, which will not be reflected in funding rates or retail sentiment. There are three specific mechanisms:

Demand for Block Space

Every on-chain overnight repo transaction, each time BUIDL is deposited as collateral, and every time stablecoins are borrowed against ACRED on Morpho consumes Ethereum block space. EIP-1559 burns a portion of every transaction fee. Increased institutional-level block space demand means more fee burns, equating to a reduced supply over time. JPMorgan processes $2 billion in transactions daily on Kinexys (primarily on EVM-compatible infrastructure), representing a baseline for institutional-level block space consumption that did not exist three years ago.

ETH as High-Quality Collateral

Standard Chartered reported in early 2026 that since June 2025, corporate treasury companies and ETH spot ETFs have cumulatively acquired about 3.8% of the circulating ETH supply. Just the treasury companies alone purchased around 2.3 million ETH in about two months, almost double the pace of accumulation comparable to Bitcoin stages. In the integration of Coinbase with Morpho, there is $1.7 billion worth of collateral (primarily ETH) actively supporting real-time loans. ETH is serving as high-quality collateral in institutional credit businesses.

Staking Yields Becoming On-Chain Reference Rates

As more institutional activities settle on Ethereum, and institutional idle liquidity resides in ETH-denominated yield instruments, ETH staking yields (about 3.8% for independent stakers) are becoming related on-chain risk-free rates. This is a structural demand anchor for staking ETH, with its scale set to grow proportionally with on-chain institutional settlement volumes.

Transparent Risk Exposure

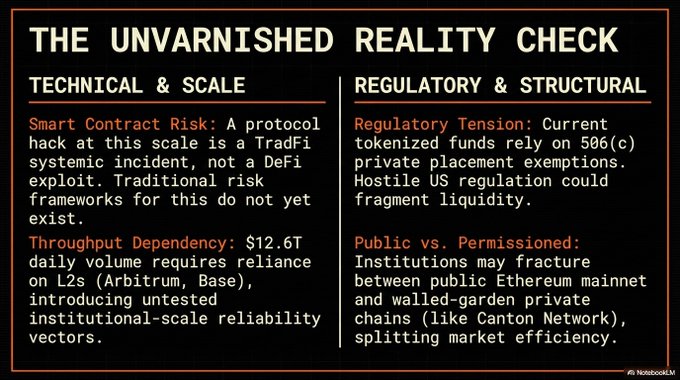

Institutional-level smart contract risk. Morpho holds over $10 billion in deposits. Apollo has governance risk exposure to a protocol. If there is a serious vulnerability, it will not be just a DeFi news headline but a traditional financial event. Currently, there are no risk management frameworks in traditional finance for such risk exposures.

Regulatory uncertainty still exists. BUIDL and MONY operate under the 506(c) private placement exemption, carefully designed workaround for the not fully bridged regulatory gap. An adverse regulatory action against the on-chain money market fund structure in the U.S. could force institutional activities back to permissioned private chains, fragmenting the ecosystem.

Tensions Between Public Chains and Permissioned Chains. JPMorgan's main Kinexys infrastructure remains a permissioned chain. Canton Network is a public chain but purpose-built for institutional use with privacy controls. Not every institution will choose the Ethereum mainnet. Part of the migration may ultimately land on purpose-built institutional chains rather than the public Ethereum chain.

Scale-Level Oracle Dependency. Programmable collateral needs reliable price feeds. Chainlink currently bears this in institutional pilots. A failure or manipulation of an oracle at repo scale has fundamentally different risk levels from DeFi liquidation cascades.

Throughput. The current Ethereum mainnet cannot handle the daily settlement volume of $12.6 trillion. Nor does it need to. L2 Rollup (like Base, Arbitrum) handles the transaction load while Ethereum mainnet provides settlement finality and data availability. However, the reliability of institutional-level L2s has not been tested at such scale, and as we know, the Ethereum roadmap still has a long way to go.

The Global Picture

Step back and consider what is actually happening:

The overnight repo market has a known failure mode, publicly proven in September 2019. The reasons are specific: settlement delays during liquidity crunch periods, market fragmentation, and information asymmetries. These are engineering problems with corresponding engineering solutions.

Blockchain settlement eliminates settlement delays. A shared on-chain ledger eliminates information asymmetries. Programmable collateral solves the frozen collateral issue. 24/7 operation eliminates calendar-driven pressure events.

The institutions executing this migration are not speculating in cryptocurrency; they are solving operational problems with operational tools:

JPMorgan processes $15 trillion in blockchain transactions not because someone in their digital asset team is bullish on ETH. They do this because it is more effective than the alternatives.

Apollo acquiring 9% governance rights in the DeFi protocol is not for yield farming. They do this because, in 2025, they raised $228 billion in new capital and needed infrastructure that could handle institutional credit sizes globally on customizable terms.

Banque de France executing real-time overnight repos on the Ethereum public blockchain is not a PR stunt. They do this because the European repo market is sized at €10.9 trillion, and they are assessing whether central bank digital currencies can improve collateral liquidity within it.

None of this guarantees ETH's price. Markets are irrational, macro conditions are harsh, and institutional adoption can coexist with ongoing multi-month pullbacks (as seen with every ETF issuance in history).

However, the structural demand being built at the protocol level—from those institutions whose infrastructure decisions have a decade-long impact—is real, growing, and largely invisible to retail sentiment.

This migration has already begun.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。