Written by: Melee

Compiled by: AididiaoJP, Foresight News

In July 2017, Hayden Adams was fired from his job as a mechanical engineer at Siemens. His college roommate, Karl Floersch, was working at the Ethereum Foundation at the time and often talked to him about smart contracts. Adams had previously ignored this. Now unemployed and looking for something to do, he decided to listen in.

The Birth of Automated Market Makers (AMM)

Floersch recommended a blog post by Vitalik Buterin about running on-chain exchanges using mathematical formulas instead of order books. The principle is not to match buyers and sellers but to allow traders to exchange with an asset pool, with prices automatically set according to the proportion of tokens in the pool. At that time, there was no available version in existence. Adams began developing it as a learning project, secured a $65,000 grant from the Ethereum Foundation, and launched Uniswap in November 2018.

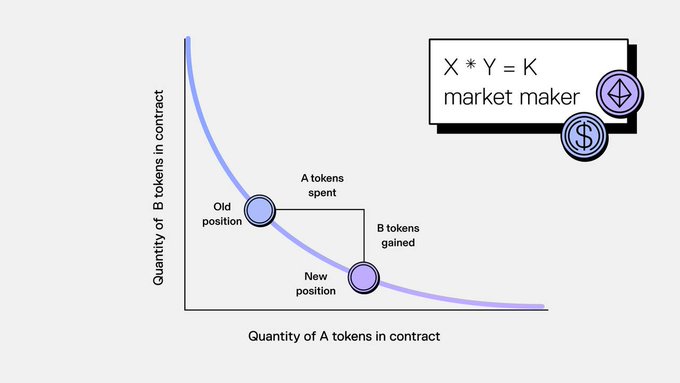

The formula is almost childishly simple: x * y = k.

Two tokens are placed in a pool, and the product of the two remains constant. When someone buys one token, they must deposit the other token, changing the ratio in the pool and adjusting the price accordingly. No order book is needed, no matching engine, and no professional market makers. Anyone can deposit tokens into the pool and earn fees from each transaction.

Automated Market Makers thus became the cornerstone of decentralized finance. Uniswap, Curve, Balancer, and dozens of other protocols have processed billions of dollars in transaction volume. On-chain order books are slow and expensive, while traditional market makers have no intention of showing up for tokens with only two hundred holders. AMMs allow anyone to create liquidity markets for any asset at any time. Before the advent of AMMs, launching a new asset required permission and corresponding infrastructure. After AMMs became available, you only need a liquidity pool.

The benefits are obvious. Therefore, prediction markets naturally also tried to adopt them.

Automated Market Makers and Prediction Markets

Prediction markets and token markets face the same cold start problem. There must be liquidity before anyone is willing to trade, and there must be traders before anyone is willing to provide liquidity. What is little known is that Robin Hanson proposed an automated market-making solution for prediction markets in his 2002 logarithmic market scoring rules several years prior.

He believed he had theoretically solved the cold start problem. However, in practice, the solution encountered the same problem that has faced every subsequent attempt to achieve automated liquidity for prediction markets: the formula cannot distinguish between tokens that forever fluctuate and rights certificates that expire.

The results of prediction markets are binary. They ultimately settle as one or zero. In a token exchange pool, both assets can fluctuate indefinitely, while the AMM formula is effective precisely because both tokens are designed not to go to zero.

Early Polymarket used an AMM based on logarithmic market scoring rules. Augur also experimented with similar solutions. If automated liquidity pools work for token exchanges, they should similarly be effective for election bets.

This is not the case.

Why Automated Market Makers Fail in Prediction Markets

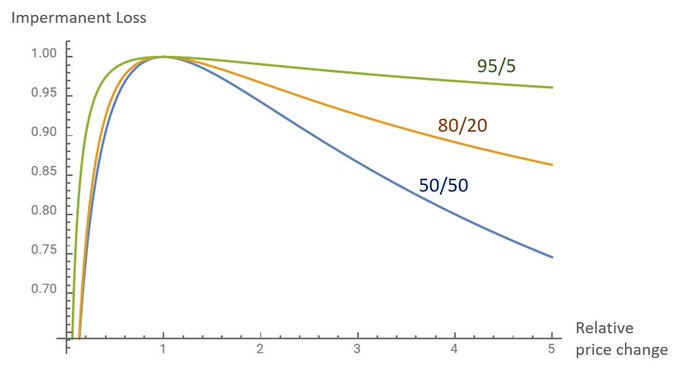

When a prediction market event completes settlement, one side is worth one dollar, and the other side is worth zero. For any liquidity provider to the pool, the mathematical result is nearly brutal. As the market approaches settlement, the liquidity pool automatically rebalances towards the losing side.

Impermanent Loss

What decentralized finance traders call "impermanent loss" here turns into a complete "permanent loss." Every market will settle; every liquidity pool will eventually hold a pile of shares worth zero.

In regular decentralized finance liquidity pools, trading fees can offset impermanent loss over time.

In prediction markets, the loss is structurally inevitable. The only question is how much liquidity providers will lose. Various protocols have tried to persuade users to deposit assets into such liquidity pools through liquidity mining, reward programs, and various incentive structures. All of these are just different ways to subsidize users to lose money more slowly.

Price Discovery

Furthermore, there is the price discovery problem. Automated market makers price assets based on pool ratios and fixed formulas. For tokens, the "correct price" is already a moving target, and a formula-driven approximation is sufficient. Prediction market prices should represent probabilities. The slippage introduced by the constant product curve distorts signals, especially evident in low liquidity markets, where a single transaction can cause the implied probability to fluctuate several basis points.

Central Limit Order Book (CLOB) Better Than Automated Market Makers?

Polymarket recognized this early on. At the end of 2022, the platform migrated from an automated market maker based on logarithmic market scoring rules to a central limit order book. Automated market makers are designed for continuous token exchanges across price ranges. Prediction markets require precise probability pricing on known binary outcomes. The two are entirely different problems.

The revolutionary characteristics that make automated market makers suitable for tokens — permissionless market creation, instant liquidity facilitation, and not relying on professional market makers — are precisely the features that prediction markets need. The problem is that the specific mechanism of the constant function formula built for token exchange, once it encounters binary outcomes and inevitable settlement, becomes difficult to maintain.

The challenge facing prediction markets is how to recreate the above effects with infrastructure that can reflect the actual settlement methods of such markets.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。