Original Author: Sanqing, Foresight News

On April 13, Eli Ben-Sasson, CEO of StarkWare, the infrastructure company behind Starknet's ZK-Rollup, announced at an all-hands meeting that the company would be laying off employees and restructuring into two independent business units focused on revenue and Starknet development. The company initially launched the StarkEx scaling engine and brought Starknet, as an Ethereum Layer 2 validity Rollup, to the main net by the end of 2021, developing its own Cairo programming language, Sierra intermediate representation layer, and post-quantum proof system, becoming a technical benchmark in the field of ZK Rollups. In 2022, it completed multiple rounds of financing, totaling about $260 million, and at one point had a valuation as high as $8 billion, making it one of the highest valued ZK projects in the crypto industry at that time.

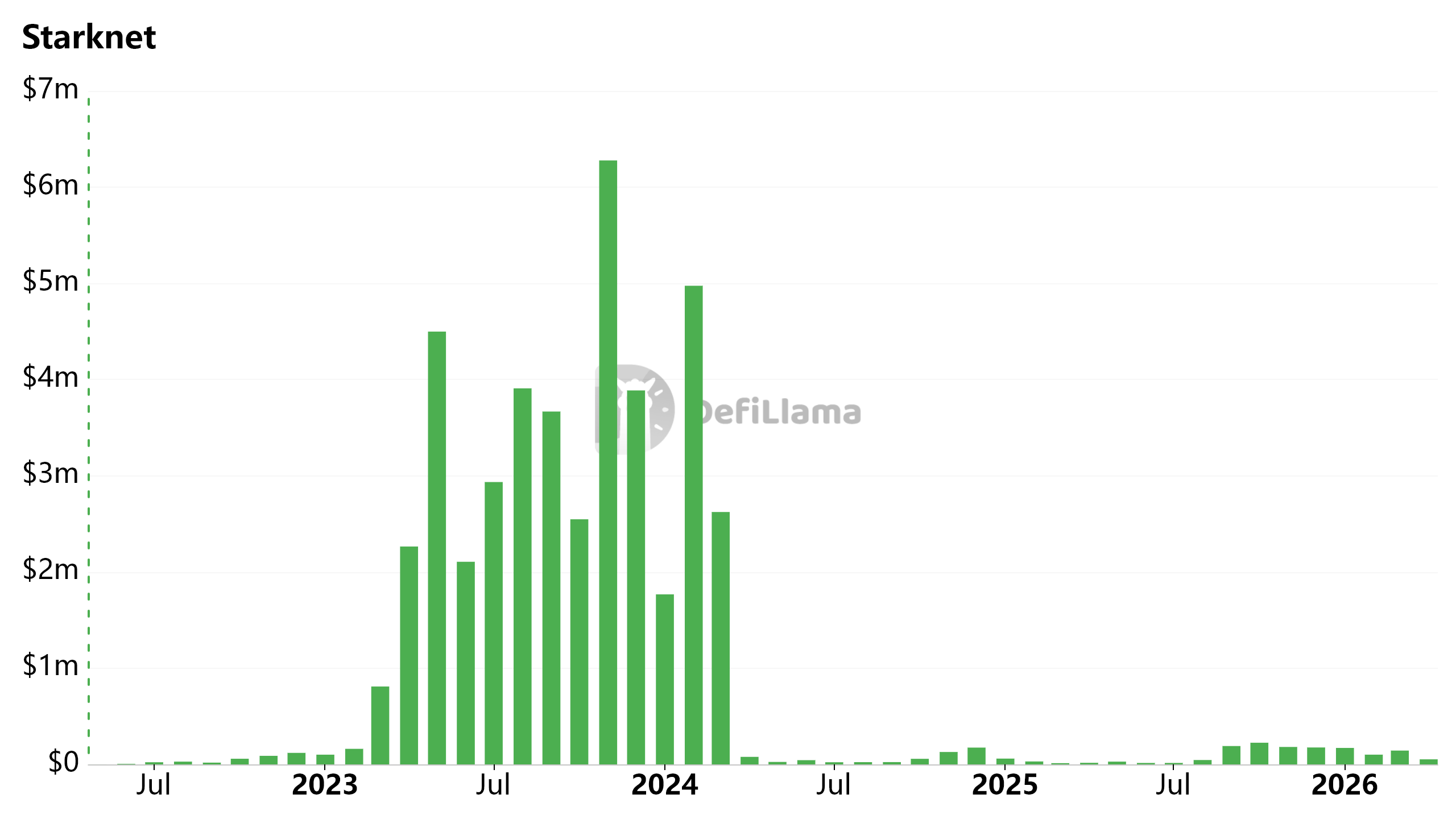

According to DefiLlama data, the on-chain monthly revenue of the Starknet network peaked at nearly $6.3 million in November 2023, while from April 2024 onwards, its monthly revenue dropped to just tens of thousands to over a hundred thousand dollars, a decline of over 95%.

Starknet Chain Fees (Monthly)

Retreating from "Infrastructure" to "Independent Applications"

Faced with the transition from a "platform-type infrastructure company" to a "product-type technology company," Ben-Sasson admitted that the previous StarkWare was "too large and inefficient," and that it must return to a startup mode, rapidly iterating through small teams to find product-market fit.

Image Source: Eli Ben-Sasson Tweet

In this round of industry contraction, StarkWare is not alone. OP Labs (the core development team for Optimism) laid off about 20 people (about 20% of its workforce) in March, aiming to focus on core priorities, accelerate decision-making, and reduce coordination costs; Polygon Labs conducted organizational integration after an acquisition in January, laying off around 60 people across multiple teams, although the company stated that its net manpower remained unchanged.

Additionally, the exchange Crypto.com laid off 12%, the L1 Algorand Foundation cut 25%, and several other companies or projects, including the crypto research firm Messari, also underwent a new round of human resource adjustments.

After the restructuring, Chief Financial Officer Ran Grinshtein will oversee backend functions such as finance and human resources, while the front-end business will be split into two units, each equipped with independent BD, engineering, and GTM teams.

- Starknet development department: led by Product Head Tom Brand, continuing the underlying work of the core protocol.

- Application department: led by Chief Product Officer Avihu Levy, responsible for direct revenue generation, committed to building products that "can only be achieved with the StarkWare technology stack, with minimal external dependencies."

Although the official product lines have not been released, combining Levy’s recent statements about implementing quantum-safe transactions (QSB) without modifying the Bitcoin protocol, along with Starknet's launch of Zcash-like privacy features, quantum safety and Bitcoin-related products are likely to be their initial testing directions.

The Impact of EIP-4844 and the Polarization of L2

The predicament of Starknet essentially reflects the collective pains of the entire L2 track following the protocol upgrade.

In March 2024, Ethereum introduced EIP-4844, significantly lowering the cost of Blob data, directly destroying the business model that L2 relied on, which was to "profit from the gas price difference between L1 and L2."

Since then, Ethereum has continued to expand the supply of Blobs through multiple upgrades, with the Pectra upgrade in May 2025 raising the target from 3 per block to 6 per block (with a maximum of 9); after the Fusaka upgrade at the end of 2025, the target will further increase to 14 per block, with a maximum of 21 per block.

In the future, Ethereum still plans to gradually expand Blob capacity through more BPO mechanisms and PeerDAS technology, which will keep the data availability costs for L2 at extremely low levels for a long time.

When the cost of data availability is significantly reduced, the moat of network value will no longer be cost-effectiveness, but the density of its users and the ability to accumulate funds.

Similarly affected by EIP-4844, the performance of the L2 market is extremely polarized.

According to DefiLlama data, Base, leveraging Coinbase's strong user flow and fiat deposit channels, garnered $75.4 million in revenue in 2025 (accounting for 62% of total L2 revenue), processing over 60% of the total transaction volume on the network; Arbitrum maintained a stable TVL of around $2 billion, relying on a composable financial stack formed by leading protocols such as GMX and Pendle.

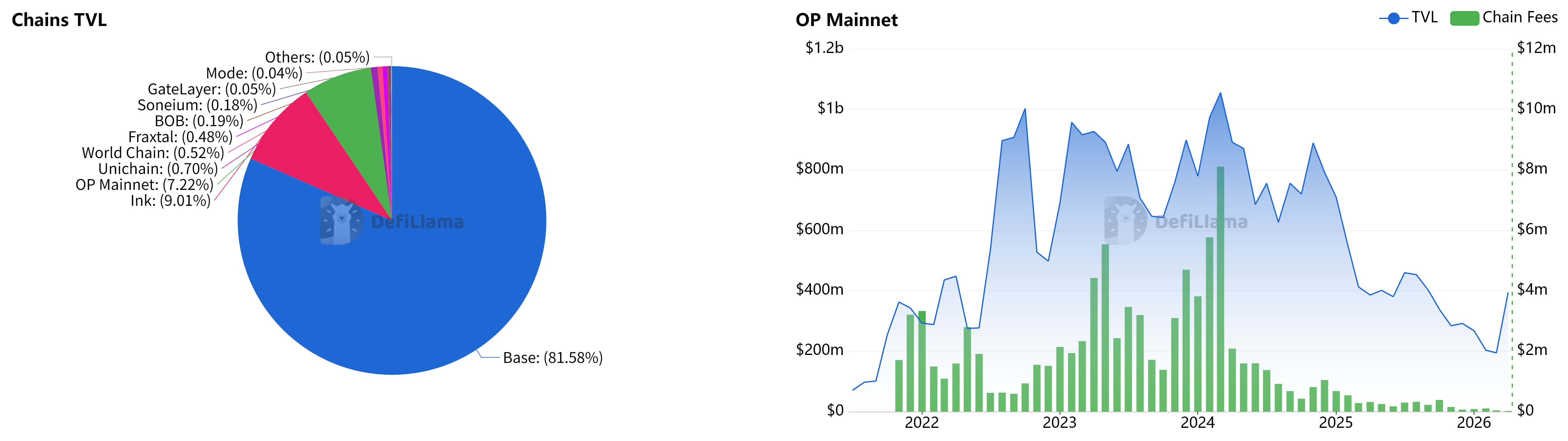

Optimism once relied on the OP Stack and the Superchain ecosystem, but now the Superchain's TVL is heavily dependent on Base (over 80%), while the OP Mainnet's share is only in the single digits. Its TVL and on-chain fee revenue have also significantly declined in 2025-2026. To make matters worse, Base announced in February 2026 that it would separate from the OP Stack and shift to a self-sustained unified tech stack, which will further weaken Optimism's central position in the L2 ecosystem.

Left: Superchain Chain TVL Pie Chart | Right: OP Mainnet TVL and Chain Fees (Monthly)

Starknet is facing an even worse situation, with its TVL currently at approximately $241 million, less than one-twentieth of Base; its native token STRK has plummeted from the airdrop peak of $0.033 in February 2024, with a total market capitalization of about $187 million. This is even lower than the company's historical financing total of $260 million.

Starknet TVL, STRK Price, and STRK Market Cap

Distribution Ability Determines Who Remains at the Table

"Infrastructure alone cannot win the game." Ben-Sasson's statement reflects a reconsideration of StarkWare's past eight years of "building the network and waiting for customers to come."

StarkWare's investment in cryptographic engineering far surpasses that of its peers, with its Cairo language and anti-quantum STARK systems built from scratch being extremely robust. However, in reality, its refusal to be compatible with EVM has built a high migration barrier for developers, limiting the prosperity of the ecosystem.

The core driving force of L2 growth is no longer technological differentiation, but distribution capability and strategic alliances. Currently, Base and Arbitrum together account for nearly 75% of the total value of L2.

21Shares predicts that the L2 track will consolidate into "a more streamlined and resilient set of networks" by the end of the year. In this winner-takes-all elimination race, retreating to self-researched applications has become one of the few differentiated paths left for StarkWare.

Technical reserves are merely a ticket to enter, not the finish line. StarkWare now needs to prove to the market not what cutting-edge technology it can "invent," but what products it can truly "sell."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。