Written by: @BlazingKevin_, Blockbooster researcher

In 2025, Robinhood witnessed a turning point in its business model. By developing wealth management services, including the launch of disruptive rate IRA retirement accounts, high-yield cash products, and comprehensive Robinhood Banking services, Robinhood successfully guided its young user base from high-frequency options and cryptocurrency trading to long-term savings and investment.

In 2025, Robinhood's financial data fully validated the success of this strategy: annual net revenue reached a record $4.5 billion, a 52% year-on-year increase; annual net profit reached $1.9 billion, a 35% year-on-year increase; assets under custody (AUC) for retirement accounts reached $26.5 billion by the end of the fourth quarter, surging 102% year-on-year; total platform assets reached $324 billion, a 68% year-on-year increase; and annual net deposits reached $68 billion.

This article will analyze the development trajectory of Robinhood's wealth management business in 2025 with data, exploring its strategic advantages across five core dimensions: customer acquisition and asset transfer mechanisms, evolution of the profit model, ecological closed loop, brand reshaping, and operational cost structure.

1. Customer Acquisition and Asset Transfer Mechanisms

Traditional wealth management often relies on financial advisors for high-cost customer acquisition and relationship maintenance, while Robinhood employs a highly internet-driven subsidy and incentive mechanism to break down barriers to asset transfer, achieving rapid scale in asset management.

1.1 Matching Funds Subsidy: The Economics of "Buying AUM"

Traditional retirement account providers (like Fidelity, Charles Schwab) typically rely on brand reputation and advisory services to attract customers, whereas Robinhood adopted a more direct and aggressive strategy: cash matching subsidies. By offering real cash rewards, it reduces the psychological cost for users in transferring assets.

For Robinhood Gold members, the platform offers up to 3% in IRA deposit matching (1% for non-members). Based on the IRS contribution limit of $7,000 for individuals under 50 in 2025, users can receive up to $210 in free matching funds each year. More aggressively, for 401(k) or IRA assets transferred from other brokers (rollovers), Robinhood equally offers a matching reward of up to 3%. This means that a user transferring $100,000 in 401(k) assets to a Robinhood IRA can immediately receive a $3,000 cash reward.

Is this economically viable? We can break it down from the perspective of customer acquisition cost (CAC) and customer lifetime value (LTV). By the end of 2025, customers had accrued over $500 million in matching funds for retirement account transfers and contributions. Robinhood views this expenditure as customer acquisition cost. Given that retirement accounts have extremely high stickiness (typically held for decades), these assets can not only bring long-term net interest income (NIM) and potential advisory fees but also lock users in as Gold members ($50 annual fee). Compared to traditional brokers, which often incur hundreds of dollars in customer acquisition costs with high attrition rates, Robinhood exchanged 3% in subsidies for decades of high-sticky assets, with its LTV far exceeding CAC.

1.2 Frictionless Experience of Account Transfer: Technological Advantage

Having subsidies alone is not enough; if the transfer process is complicated, users will still hesitate. Robinhood has greatly lowered the barriers for users to transfer from traditional brokers using technology.

By integrating the Automated Customer Account Transfer Service (ACATS), Robinhood enables seamless transfers of assets across brokers. Users only need to enter their original brokerage account information within the App, and without manually liquidating existing assets, Robinhood's clearing system can automatically complete the asset transfer in the background. For transfer fees charged by some brokers (typically $75), Robinhood will reimburse them under certain conditions. This "one-click move" experience completely breaks the asset transfer barriers built by traditional institutions relying on cumbersome processes.

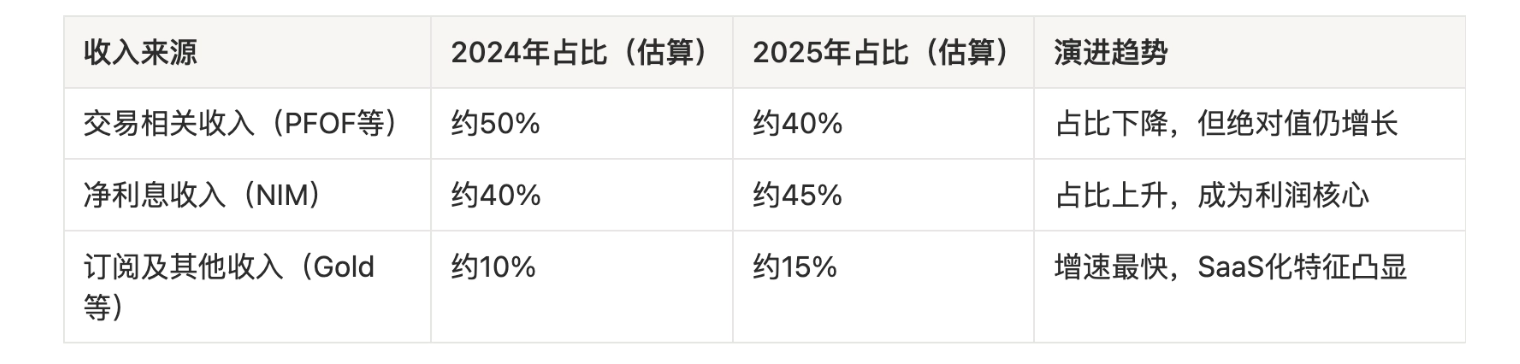

2. Evolution of the Profit Model from PFOF to Recurring Revenue

In the past, Wall Street's skepticism towards Robinhood mainly focused on its heavy reliance on payment for order flow (PFOF) and high-frequency trading. This model is highly effective in bull markets but extremely fragile in bear markets. In 2025, Robinhood successfully evolved towards a more stable asset management profit model.

2.1 Net Interest Income (NIM): Attracting Deposits with High-Yield Cash

By providing highly competitive cash yield rates, Robinhood liberated "cash management" from the low-yield traps of traditional banks, thereby attracting a massive amount of deposits.

By the end of 2023, the uninvested cash APY for Robinhood Gold members reached as high as 5.0%, far exceeding the national average savings account rate at that time. As the Federal Reserve lowered interest rates, the APY gradually adjusted (3.35% by early 2026), but still remained significantly higher than the interest rates offered by large banks for checking accounts. In the fourth quarter of 2025, Robinhood's Cash Sweep balance increased by 26% year-on-year, reaching $32.8 billion.

This enormous interest-bearing asset generated considerable net interest income for Robinhood. In the fourth quarter of 2025, its net interest income grew by 39% year-on-year to $411 million, primarily due to growth in interest-bearing assets and securities lending activities. In a specific interest rate cycle, this "earning interest spread" model provides a robust profit base.

2.2 Subscription Economy (Robinhood Gold): SaaS Transformation of Financial Services

The Robinhood Gold subscription service ($5 per month or $50 per year) is at the core of its profit model evolution. It exchanges a monthly fee for high interest, in-depth research reports, 3% IRA matching funds, and a 3% cash back credit card. This is essentially an attempt to SaaSify financial services.

By the end of the fourth quarter of 2025, the number of Robinhood Gold subscribers reached a record 4.2 million, a 58% year-on-year increase, with a penetration rate exceeding 15% among the 27 million funded customers. This subscription model significantly enhanced user stickiness and average revenue per user (ARPU). The ARPU for the fourth quarter increased by 16% year-on-year to $191, with the third quarter ARPU soaring 82% year-on-year.

The table below illustrates the evolution of Robinhood's revenue structure:

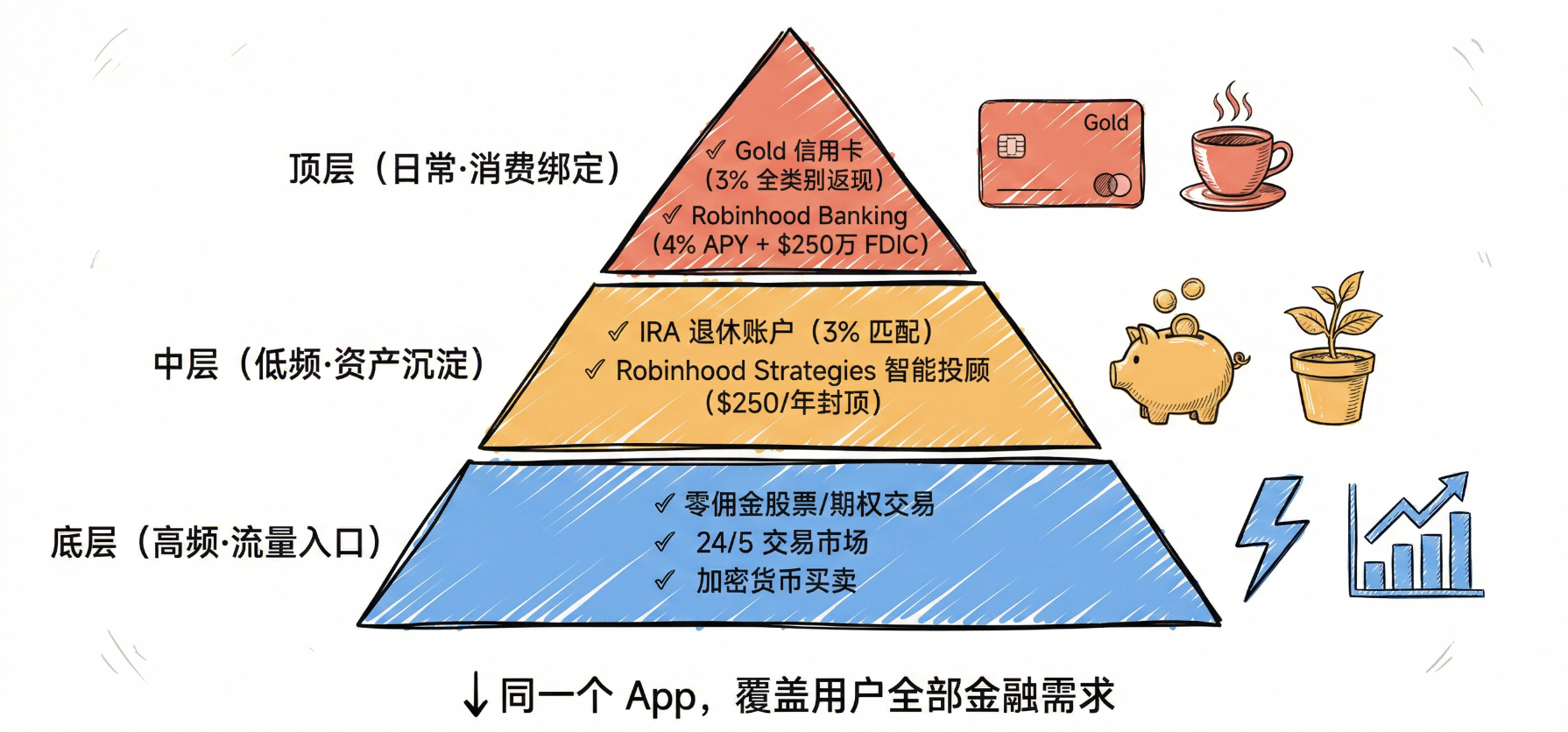

3. Ecological Closed Loop

Young users dislike downloading multiple apps to manage their finances. Robinhood deeply understands this and is building a super app that covers investment, savings, consumption, and lending.

3.1 One-Stop Experience: Seamless Connection of High and Low-Frequency Scenarios

In 2025, Robinhood launched or upgraded several products, forming a complete ecological closed loop:

- High-Frequency Scenarios: Zero-commission stock/options trading, 24/5 trading markets, cryptocurrency buying and selling.

- Low-Frequency Defensive Scenarios: IRA retirement accounts (3% matching), Robinhood Strategies smart advisory (Gold members $250/year cap management fee).

- Everyday Consumption Scenarios: Robinhood Gold credit card (3% cash back), Robinhood Banking (4% savings APY, FDIC insurance).

Seamlessly connecting high-frequency speculative trading with low-frequency retirement investments and daily consumption within the same app is Robinhood's killer advantage.

3.2 Traffic Conversion: Smooth Cross-Selling from "IPO" to "Retirement"

Robinhood has the massive traffic that traditional asset management companies dream of (with 27 million accounts by the end of 2025). Its core strategy is to use high-frequency trading (such as meme stocks and cryptocurrencies) and high-yield cash as traffic entry points and then smoothly cross-sell (cross-sell) low-frequency but high-value wealth management products.

For instance, when a 22-year-old Gen Z user downloads Robinhood to trade Dogecoin, he will be attracted by the 5% cash yield to subscribe for Gold membership; subsequently, the app will send precise push notifications informing him, "As a Gold member, you can receive a 3% matching bonus by opening an IRA"; when his assets reach $100,000, the system will recommend the "smart advisory service for just $250 a year."

This conversion path from "traffic funnel" to "asset accumulation" enables Robinhood to acquire high-net-worth customers at extremely low marginal costs.

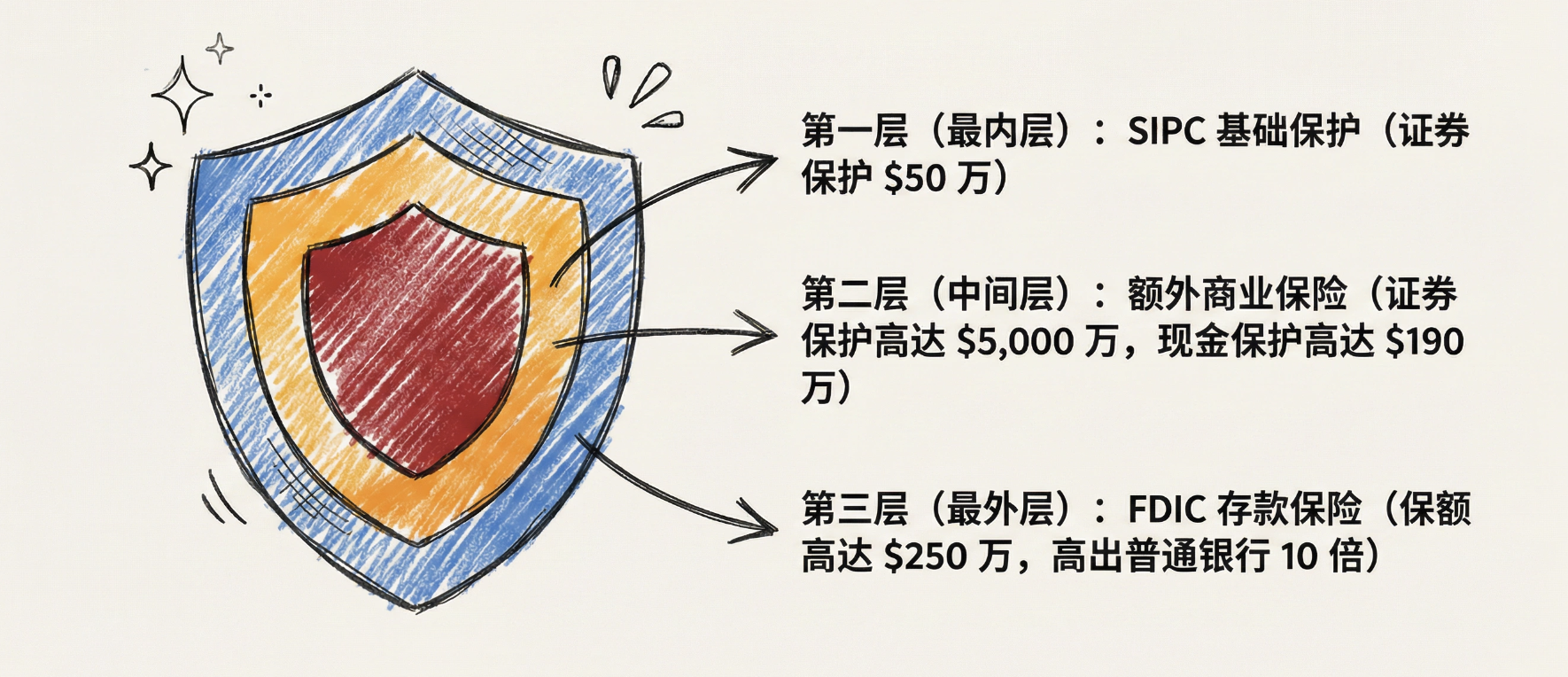

4. Building Trust

4.1 Compliance and Security Endorsement: Leveraging Traditional Finance's Safety Net

To gain users' trust in entrusting their decades-long retirement funds, Robinhood cleverly leverages the safety nets of traditional finance to endorse its innovative products.

SIPC Protection and Additional Insurance: Robinhood emphasizes its status as a SIPC member (providing $500,000 of basic protection) and has purchased additional commercial insurance, offering each customer up to $50 million in securities protection and $1.9 million in cash protection.

FDIC Deposit Insurance: When promoting Cash Sweep and Robinhood Banking, the platform cooperated with several banks to provide users with up to $2.5 million in FDIC deposit insurance, far exceeding the ordinary bank's standard coverage of $250,000.

This "safer than traditional banks" narrative strategy significantly alleviates the young users' trust concerns toward emerging fintech platforms.

5. Operational Cost Structure

Robinhood's ability to offer 3% IRA matching and $250 cap on advisory fees comes not only from confidence in LTV but also from its far superior workforce efficiency and underlying technology costs compared to traditional institutions.

5.1 Technology-Driven Automation and High Efficiency Ratio

Robinhood does not have extensive offline branches or financial advisory teams. All its advisory services (such as ETF portfolios recommended by Robinhood Strategies) are highly automated, relying on algorithmic models for asset allocation and rebalancing.

This "light asset" model brings astonishing efficiency. According to public data, by the end of 2025, Robinhood had approximately 2,900 employees. With annual revenue of $4.5 billion, its revenue per employee reached as high as $1.55 million. In contrast, traditional financial giants with tens of thousands of employees often have revenue per employee figures that are half this number or even lower.

5.2 Decreasing Marginal Costs: The Power of In-House Clearing System

As early as 2018, Robinhood eliminated its reliance on third-party clearing institutions (such as Apex Clearing) by establishing its own clearing system. This infrastructure investment exhibited significant operational leverage during the asset scale explosion in 2025.

When AUC soared from $193 billion to $324 billion, the marginal cost of processing additional trades and asset transfers was nearly negligible due to the in-house and highly automated clearing system. Based on macro trend data, Robinhood's total operating expenses for the year 2025 were $2.379 billion; despite revenue surging by 52%, the growth of operating expenses was relatively controllable, directly propelling the GAAP net profit for the year to $1.9 billion and significantly enhancing adjusted EBITDA profit margins.

6. Changing User Profile

The core driving force behind the success of Robinhood's wealth management business is the profound shift in the investment behavior of its young user base.

6.1 Younger User Base: Structural Advantages

According to research from ARK Invest, 63% of Robinhood's user base consists of Gen Z and millennials, while this proportion is only 14% at Charles Schwab and relatively limited at Vanguard as well. The median age of Robinhood users is approximately 32 to 35 years (2025 data), while clients of traditional brokers like Schwab average over 50 years of age.

This structural advantage is also reflected in platform asset density. Currently, Schwab's average assets under custody (AUC) per client are approximately $250,000, significantly higher than Robinhood's current level of around $12,000. However, the essence of this gap is the age difference. As Robinhood's young user base gradually enters its wealth accumulation peak, this gap is expected to narrow over time.

6.2 From "Meme Stocks" to "Long-Termism": Deep Change in Investment Behavior

Robinhood CEO Vlad Tenev pointed out at the end of 2025 that a trend is occurring: 19-year-old Gen Z individuals are actively opening retirement accounts.

This trend is backed by data. According to the latest savings data cited by USA Today, the retirement savings rate for Gen Z has consecutively increased for several years, reaching 6.2% in 2025, up from 5.9% in 2024, while all other age groups have seen a decline. Fidelity data shows that Gen Z investors contribute up to 95% of IRA contributions into Roth accounts, demonstrating a clear understanding of long-term tax optimization.

6.3 Bridging "The Largest Wealth Transfer in Human History"

In the coming decades, approximately $124 trillion in assets are expected to transfer from the Baby Boomer generation to millennials and Gen Z. Given that Robinhood holds overwhelming market share among young people, when these young users inherit wealth, they are highly likely to choose to keep their funds within the Robinhood ecosystem they are familiar with and have a better experience, rather than transferring to traditional brokers used by their parents.

Conclusion: The Rise of a Financial Super App

2025 is a watershed year in Robinhood's development history. It successfully shed the label of "a casino for retail speculation" and has transformed into a comprehensive, mature, and highly competitive "super financial application."

The core logic of this transformation lies in Robinhood's profound understanding of its user base's lifecycle value. A 22-year-old Gen Z user today may only buy a few ETFs with Robinhood; tomorrow, he will open an IRA account and enjoy a 3% matching reward; the following year, he will rollover his 401(k) from work into Robinhood; in a few more years, when his asset scale grows to $100,000, he will open Robinhood Strategies to enjoy capped-rate professional advisory services; ultimately, when he inherits a sum from his parents, he will naturally deposit it into Robinhood Banking.

Through aggressive customer acquisition mechanisms, a stable recurring revenue model, a one-stop ecological closed loop, reshaped trust brand, and an extreme low-cost structure, Robinhood has excellently prepared its infrastructure for the upcoming "largest intergenerational wealth transfer in human history."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。