Author: FinTax

On March 9, 2026, the UK Treasury published the "Individual Savings Accounts (Amendment) Regulations 2026" (SI 2026/248), which adjusted the access rules for different assets under the ISA framework. This amendment legally clarified that Cryptoasset exchange traded notes (Cryptoasset ETNs) can qualify as eligible investment products for tax benefits; meanwhile, it limited them to the category of Innovative Finance ISA (IFISA) investments. Although this arrangement formally allows crypto ETNs to enjoy tax benefits under the ISA framework, there may actually be various obstacles in policy implementation, such as the compliance obligations of the IFISA potentially constraining the popularity of crypto ETNs among investors. In this context, whether crypto ETNs have gained an institutional admission opportunity or have been substantively marginalized is worth further discussion. This article will outline the core content of the aforementioned ISA regulations, review the evolution of the regulatory policies concerning crypto ETNs, and analyze their real impact in conjunction with market structure and regulatory logic.

1. Background of the UK ISA Regulation Amendments

1.1 Tax-advantaged Account Framework

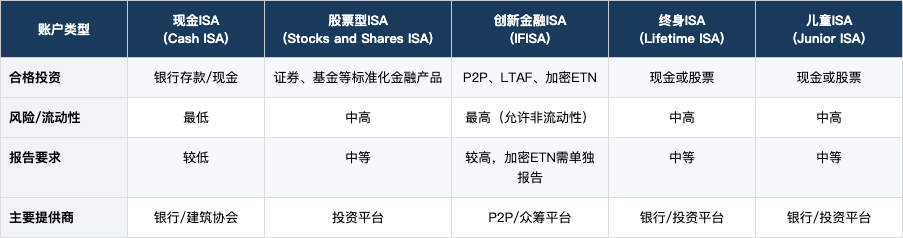

To encourage savings and investments, the UK government launched a tax-advantaged tool—Individual Savings Accounts (ISA)—in 1999, allowing investors to open ISA accounts through investment platforms, brokers, or banks, and to hold various financial assets within these accounts, with investment income generated within the accounts being tax-free. Based on the risk attributes and regulatory requirements of investment products, ISA accounts are categorized into different types, each differing in terms of eligible investment products, product risk or liquidity, regulatory reporting requirements, and types of providers.

Table 1: Comparison of Different ISA Accounts

Cash ISAs primarily correspond to low-risk assets existing in the form of bank deposits or cash, with high liquidity. Stock ISAs correspond to medium to higher-risk standard financial assets, including stocks, funds, and ETFs, whose value fluctuates with market changes, potentially offering higher returns but also facing risks of price declines. Innovative Finance ISAs accommodate more complex or higher-risk investment tools such as P2P loans, Long-Term Asset Funds (LTAFs), and crypto ETNs; these products tend to be less liquid and might not be protected under the Financial Services Compensation Scheme (FSCS), representing the highest overall risk level.

All types of ISAs require the financial institutions providing the products to submit annual information reports to HM Revenue and Customs (HMRC), mainly including subscription amounts, transfers in and out, and position overviews, to ensure tax benefits are correctly applied. This reporting obligation is generally consistent across all types of ISAs. According to the 2026 amendments, crypto ETNs need to be reported as a separate category. Additionally, the relevant financial institutions have an obligation to report information to the Financial Conduct Authority (FCA) level. Cash ISAs typically involve only deposit-type assets and usually do not entail complex suitability assessments or investment information disclosure obligations, thus having relatively lower reporting requirements; stock ISAs, due to securities investments, require platforms to adhere to FCA general rules on suitability assessments and disclosures; Lifetime ISAs must also manage government bonus payment records; and Child ISAs require attention to guardian information management. Due to the higher risk of IFISA products, platforms often have to bear stricter ongoing monitoring, suitability assessments, capital requirements, and specific disclosure obligations. Overall, the complexity of reporting requirements increases with rising product risk.

1.2 Evolution of ISA Policies Concerning Crypto ETNs

Initially, crypto ETNs were not separately defined in the "Individual Savings Account Regulations 1998" and there were no specific access restrictions. As debt securities issued by companies and recognized by investment exchanges in the UK, crypto ETNs met the requirements of "qualifying securities" as per Section 7(2)(b) of the regulations, typically falling into the broad categories of securities under stock ISAs and enjoying the same tax benefits as traditional securities. However, in reality, due to the FCA's retail ban, retail investors could not invest in crypto ETNs within the ISA framework—starting from January 6, 2021, the FCA fully prohibited regulated entities in the UK from selling, marketing, or distributing any derivatives or exchange-traded notes linked to "non-regulated transferable crypto assets" to retail investors, which included crypto ETNs. This means that retail investors could not purchase crypto ETNs on ISA platforms or include them in stock ISAs.

On October 8, 2025, the restrictions on crypto ETN investments underwent a turnaround. On this day, the FCA officially lifted the sales ban, allowing retail investors to trade crypto ETN products through RIEs, but classifying them as Restricted Mass Market Investments (RMMI) subject to consumer protection requirements such as risk warnings and suitability assessments. On the same day, HMRC issued its "Tax Treatment Policy for Cryptoasset Exchange Traded Notes," clarifying that eligible crypto ETNs could be included in registered pension accounts and held tax-free from that day onward, and from April 6, 2026, be categorized as eligible investments under the Innovative Finance ISA (IFISA) for tax benefits. The related policy arrangement was ultimately formalized into legally binding rules through the SI 2026/248 regulations, thereby solidifying HMRC's core arrangement regarding the classification of crypto ETN accounts and setting clear transitional arrangements for those previously held crypto ETNs.

2. Interpretation of SI 2026/248 Regulations

2.1 Changes in the Regulatory Structure of Core Provisions

Before the introduction of SI 2026/248, any investment tool that met the general characteristics of "transferable securities" in legal form could automatically be included in the range of eligible investments under stock ISAs. In this context, crypto ETNs could fall within the category of "qualifying securities" at the regulatory level, thus formally qualifying to enter stock ISAs. This revision made substantive adjustments to the aforementioned regulatory structure, discontinuing the previous abstract classification path. First, a specific definition for crypto ETNs was established, distinguishing them from the general abstract category of "qualifying securities"; second, it clarified that crypto ETNs would no longer be applicable to stock ISAs; finally, it limited them to only being included as eligible investments under Innovative Finance ISAs with explicit classification arrangements.

2.2 Statutory Definition of Crypto ETNs

SI 2026/248 refined the core characteristics of crypto ETNs: First, crypto ETNs must be financial instruments traded on UK RIEs, possessing traits of publicly traded markets; second, these products are defined as debt securities without fixed periodic coupons, with returns not derived from fixed interest but depending on the price performance of specific underlying assets; third, their return structure is explicitly anchored to "unregulated transferable crypto assets," distinguishing them from exchange-traded products supported by traditional financial assets; fourth, the legal definition does not restrict the nature of risk exposure but encompasses various structural arrangements, including delta-1, inverse, and leveraged types. This definition, while acknowledging that crypto ETNs belong to the category of securities, also distinguishes them from traditional securities at the regulatory level, providing the necessary foundation for differentiated access arrangements within the ISA system.

2.3 Compliance Requirements for ISA Managers

ISA managers are financial institutions approved by HMRC in the UK that have the authority to establish, operate, and manage ISA accounts, such as banks and securities firms. Although this revision did not introduce independent obligation provisions specifically for managers, the adjustment of crypto ETN rules indirectly added related compliance obligations for ISA managers, primarily reflected in business eligibility and information reporting aspects.

Regarding business eligibility, only managers qualified to operate Innovative Finance ISAs may provide crypto ETN products under the ISA framework. This operational certification is not an independent financial license but a specific account type authorization formed under the ISA manager approval system. Thus, this revision effectively imposes new requirements on managers; for those solely engaged in stock ISA operations, unless they obtain IFISA qualifications, they may no longer provide crypto ETN products within the ISA framework; if they intend to continue relevant businesses, they must apply for approval from the relevant departments and make the necessary adjustments to their business models and account systems.

Regarding information reporting, the new regulations strengthened the reporting obligations of ISA managers. First, it amended the original Regulation 31, on the basis of annual information returns, to list crypto ETNs as a special investment type that requires separate identification and distinction in reporting, with required reporting content including market value and relevant cash amounts to facilitate HMRC's understanding of the scale, valuation, and risk exposure of crypto ETN holdings. Second, the system must have the capability to identify the crypto ETN asset category and ensure its correct allocation to IFISA accounts and separate reporting in the format designated by HMRC.

3. Regulatory Logic and Market Impact

3.1 Gradual Regulation from Stock ISAs to Innovative Finance ISAs

The price volatility, complexity, and information asymmetry characteristics of the underlying assets of crypto ETNs suggest that their risks may exceed those of traditional stocks, bonds, or funds. The new ISA regulations detached crypto ETNs from stock ISAs and included them in IFISA accounts, preserving a tax-exempt investment channel for investors while placing high-risk assets in specialized risk-bearing accounts. This arrangement reflects the regulatory agency's intent to manage different asset classes through risk layering and account functionality matching. Additionally, when the FCA lifted the retail ban on crypto ETNs at the end of 2025, the UK Treasury did not directly incorporate crypto ETNs into IFISA but provided necessary transitional arrangements to allow holders of crypto ETNs in stock ISAs before April 6, 2026, to continue holding without needing to transfer them to IFISA. This setting of a six-month transitional window reserved technical preparation time for related platforms and facilitated investors' gradual acclimatization to the new regulations.

3.2 Impact on Relevant Market Participants

For ISA managers, the new regulations require them to obtain IFISA-related licenses to engage in crypto ETN business, while also needing to redesign account classifications and product management processes, and upgrade systems to support the independent identification, valuation, and reporting for crypto ETNs. Although the new regulations legally incorporate crypto ETNs into IFISA for tax benefits and provide a clearer regulatory framework, the limited number of IFISA managers, insufficient platform experience, high operational costs, and compliance pressures combine to create cost pressures and reputational risk challenges for conducting IFISA crypto ETN business.

For crypto ETN issuers, the most direct impact is the contraction of retail distribution channels. Previously, stock ISAs were seen as significant growth gateways for crypto ETNs; under the new regulations, if there are no willing IFISA managers to undertake related business, the retail distribution scale for issuers may contract. Next is the adjustment of liquidity expectations; as retail demand slows, the activity level in the secondary market will weaken, affecting overall market trading volumes, forcing issuers to reassess market liquidity conditions and implement measures such as optimizing indices and adjusting fees to maintain product competitiveness.

For ordinary investors, the new regulations limit crypto ETNs to IFISA accounts, institutionally strengthening investor protection for high-risk assets, but actual accessibility may decrease. Under current market conditions, the supply of managers qualified for IFISA and willing to offer crypto ETN products is relatively limited, making it more difficult for ordinary investors to hold crypto ETNs within the ISA framework. Furthermore, existing transitional arrangements are relatively generic and lack detailed rules for handling existing holdings. According to the new regulations, crypto ETNs included in stock ISAs before April 6, 2026, can continue to be held, but there is insufficient clarity regarding subsequent trading, conversion, or account migration paths. For example, uncertainties remain regarding whether investors can continue to increase holdings in their original accounts and the specific arrangements for transfers between different managers.

4. Conclusion

The introduction of the SI 2026/248 regulations marks the formalization of the UK's differentiated risk management policy for crypto ETNs within the ISA framework. This amendment maintains a tax-exempt investment channel for retail investors by incorporating crypto ETNs into the Innovative Finance ISA (IFISA) while isolating the systemic risk of crypto ETNs through account classification, reflecting the regulatory authority's balanced consideration between promoting financial innovation and strengthening consumer protection. However, as previously mentioned, the limited supply of IFISA managers may restrict the degree of crypto ETN adoption within the ISA system in the short term, which also reflects the need for further coordination between policy design and market realities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。