Text | Lin Wanwan

On March 24, 2026, Circle's CEO Jeremy Allaire probably experienced the toughest trading day since the company's IPO.

The stablecoin company he co-founded saw its stock price evaporate by one-fifth during trading. Over 30 million shares changed hands that day, and panic was clearly written across the market.

The cause of all this was a few pages of paper that leaked from an office building in Washington.

$78 Billion "Water Supply" Business

To understand this crash, we must first grasp how Circle makes money.

Many believe that stablecoin companies are tech firms, but what Circle does is more like banking. You give it $1, and it gives you one USDC token; you can freely transfer or spend that token on the blockchain while it uses your dollar to buy U.S. Treasury bonds.

The interest from the Treasury bonds is Circle's profit.

How profitable is this business? In the fourth quarter of 2025, just the reserve interest contributed $733 million.

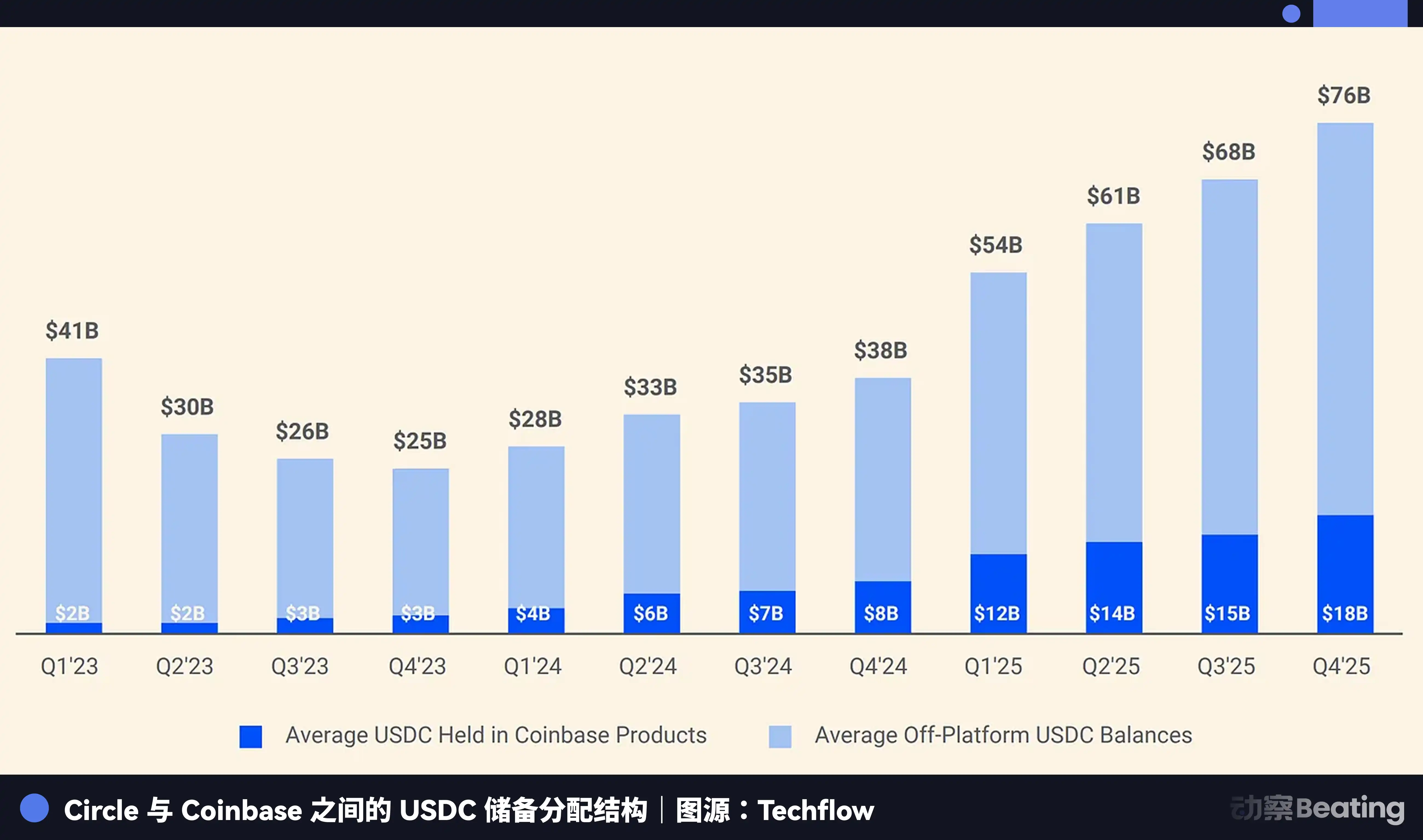

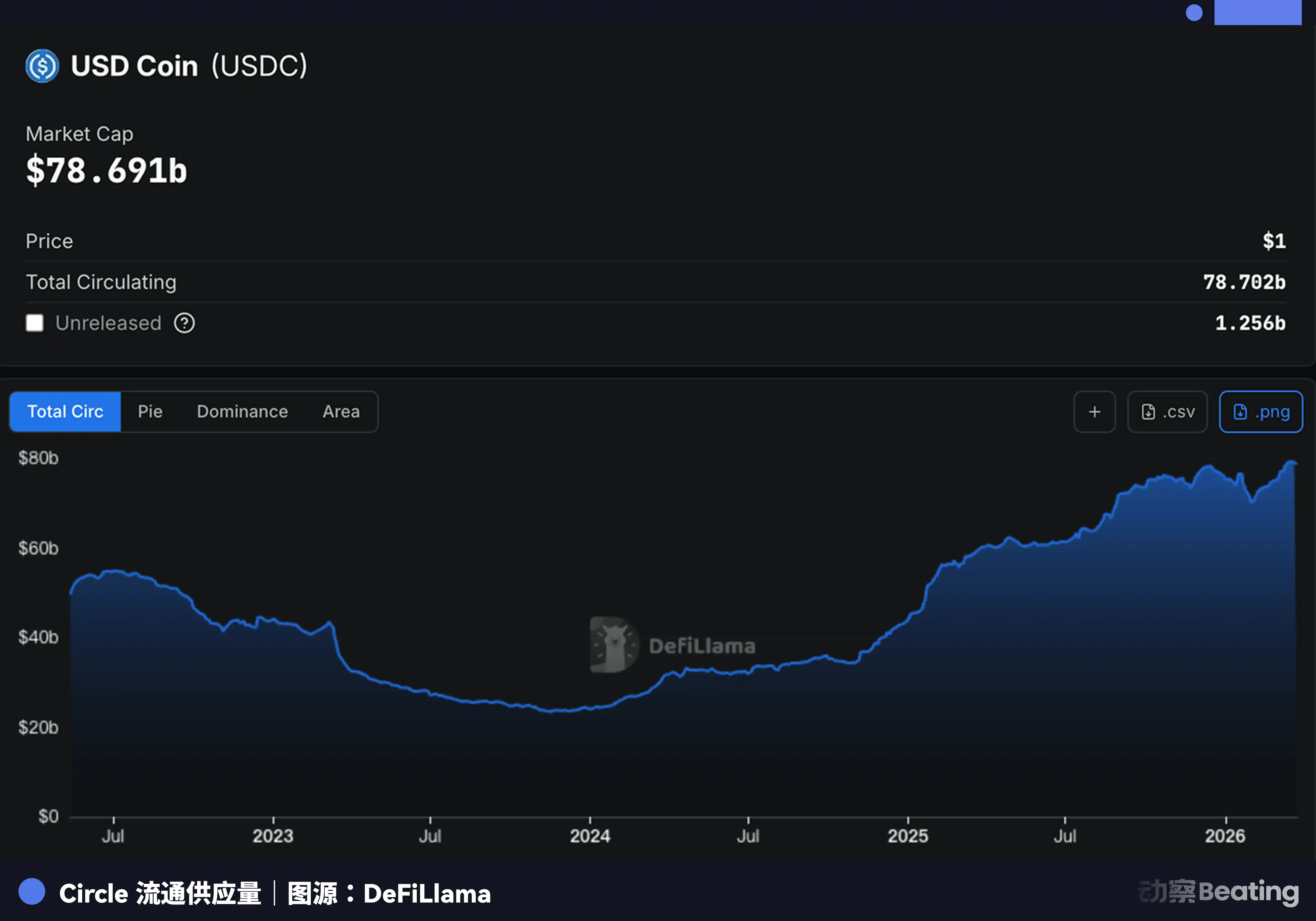

The circulation of USDC skyrocketed by 72% within a year, reaching $78 billion. Circle holds a $78 billion pool of funds, with interest flowing in like tap water, nonstop for a day.

Just attracting deposits isn't enough; more people need to be willing to exchange their money for USDC. So, Circle made a deal with Coinbase: Circle shares part of the interest income with Coinbase, which in turn offers users holding USDC a 3.5% annualized return. You deposit your money, and it earns interest without requiring knowledge of blockchain or any action; the earnings automatically credit to your account.

This model forms a beautiful flywheel: earnings attract users, users bring in funds, funds generate interest, and interest feeds earnings. The flywheel spins faster and faster, and Circle's stock price soared from about $50 in early February to $135, a 170% increase in six weeks. The market's expectation that the Federal Reserve would maintain high interest rates also helped Circle; the higher the rates, the richer the reserve interest.

Then, someone set their sights on this machine.

The Banking Industry's Counterattack

On March 24, the latest draft of the U.S. Senate's CLARITY Act was exposed.

This legislation, officially titled the "Digital Asset Market Clarity Act," was originally meant to set regulations for the crypto market and had already passed a version in the House of Representatives. However, the Senate added an amendment in the latest version: it prohibits any platform from providing yields for passive holdings of stablecoins, including arrangements that are economically or functionally equivalent to bank deposit interest.

In simple terms, the "earning interest on holdings" approach is not allowed anymore.

This ban strikes at the heart of Circle. If it cannot pay yields, no one will be motivated to hold USDC in the short term, and Coinbase's stablecoin business will shrink in the long term. In the fourth quarter, Coinbase had $364 million in revenue from stablecoins, a figure now hanging in the balance.

The game behind the ban is even more interesting than the ban itself.

The struggle surrounding stablecoin yields has actually been ongoing for nearly a year.

The GENIUS Act, which took effect in July 2025, already prohibited issuers from directly paying interest to holders, but the law did not explicitly cover affiliates and third-party platforms. Circle and Coinbase took advantage of this gray area: Circle shares its reserve interest with Coinbase, which then distributes it to users as a "reward," so the funds still arrive as intended.

Over 40 banking associations, led by the American Bankers Association, then collectively wrote to Congress, demanding that this loophole be closed. The yield prohibition in the latest draft of the CLARITY Act is a direct product of this lobbying effort.

The traditional banking industry in America is pushing for this amendment.

The reasoning is straightforward: if Coinbase can offer a 3.5% yield, why would customers keep their money in traditional bank checking accounts? The stablecoin yield model directly undermines the foundation of bank deposits. It has been reported that bank representatives were arranged to review the draft on the day it was released. The crypto industry attempting to do banking will not be ignored by banks watching their deposits being siphoned off by a group of coders.

Lawmakers on Capitol Hill need to choose between two forces, and at least from this draft, the traditional forces seem to prevail for now.

Shay Boloor, Chief Market Strategist at Futurum Equities, pointed out an even more pressing issue: this ban impedes USDC's path to upgrade from a payment tool to a "store of value" product.

That upgrade route was precisely the core logic behind Circle's stock price surge in recent weeks. The 170% stock price increase relied on the market's pricing of USDC's future potential. Now that potential has been chopped down by the legislative draft, and the 170% increase has instead become the best reason to short.

The stock price plummeted from a high of $125 to around $101, marking the largest single-day drop since its IPO in June 2025. Coinbase also fell about 10% along with it.

Tether's "Take Advantage of Your Illness"

As fate would have it, misfortune does not come alone.

On the same day, Circle's biggest competitor, Tether, announced that it had hired a Big Four accounting firm to formally audit all reserves of its USDT.

This news might seem like a side note under normal circumstances, but at this time, its impact was magnified tenfold.

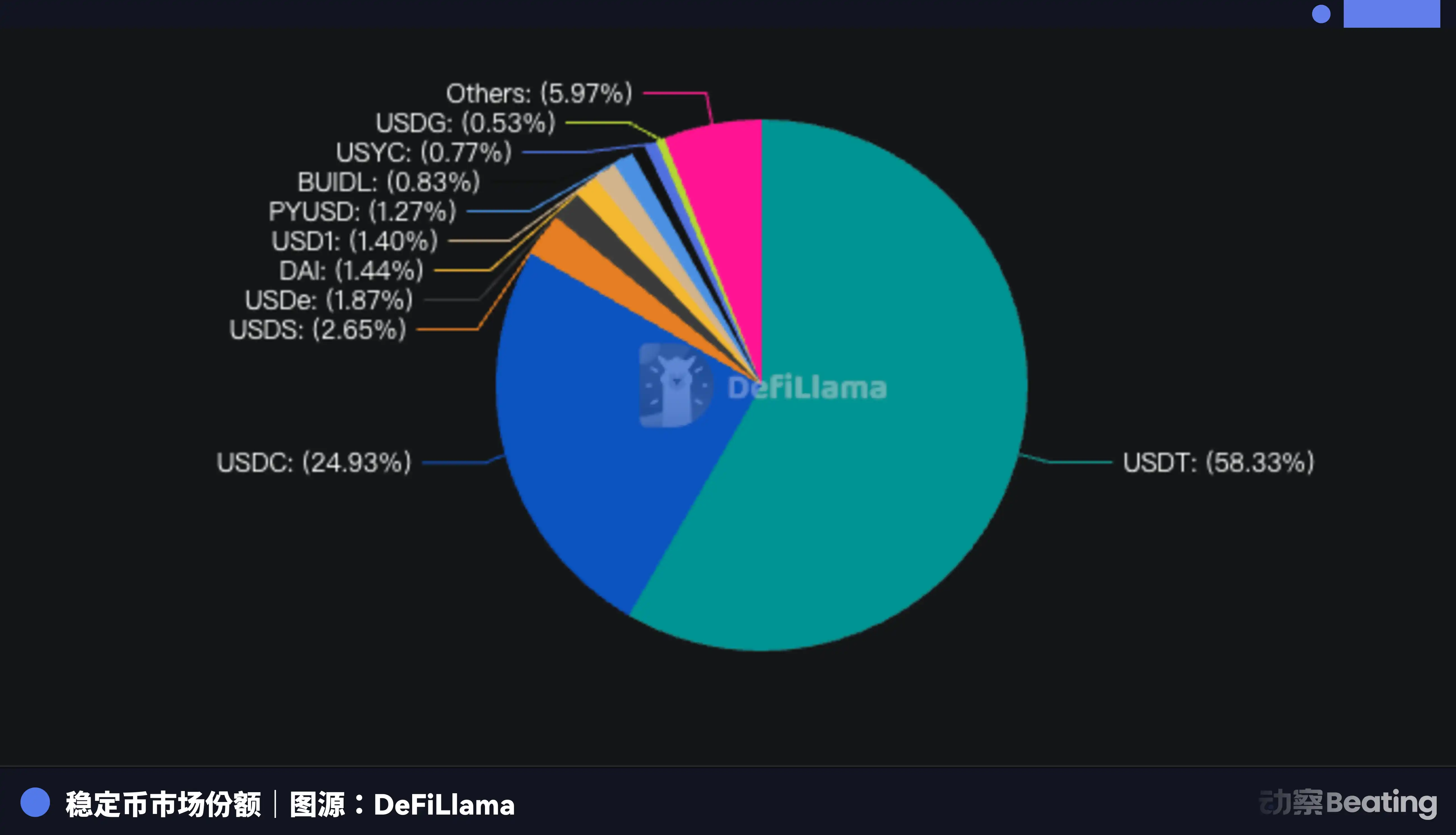

The landscape of the stablecoin industry has always been very distinct: Tether's USDT is the largest in scale but has faced ongoing questions regarding reserve transparency; Circle's USDC is slightly smaller in scale but wins on compliance.

Institutional investors choose USDC largely to buy "peace of mind." At its core, Circle's moat is trust.

Now Tether is looking to fill this shortcoming. Once the audit is passed, the largest gap between USDT and USDC will be erased. Regulations digging at Circle's moat and competitors building their own moats.

Being squeezed from both sides at such a precise timing is hard to call coincidence. On the brink of a reshaping of stablecoin regulatory dynamics, Tether seizes this window to show its sincerity, calculating its moves soundly.

Some market participants candidly state that if Tether secures the endorsement of a Big Four audit, combined with a deeper U.S. market positioning, USDC's share in the institutional sector will be further eroded.

The "compliance honor student" image Circle has worked hard to cultivate over the past few years is shifting from a unique advantage to an entry threshold.

Armor and Shackles

However, there are calming voices as well.

Clear Street analyst Owen Lau believes the market's reaction has been overstated. He claims the actual situation is not as dire as the headlines suggest, but more a knee-jerk reaction to complex legislative news.

He has a point; the CLARITY Act is still a draft in the Senate, and there is a long negotiation process ahead before it officially becomes law.

Although the Trump administration is pushing for the bill's passage, the yield restriction clause could also become a barrier to its advancement. The yield limitation could be modified or even outright removed in the final text.

The draft does not impose blanket restrictions: rewards linked to payments, transfers, or promotional activities can still be implemented, but "earning interest passively" is no longer allowed. The SEC, CFTC, and Treasury will further define what constitutes "permissible rewards" within a year after the law takes effect, and specific rules have yet to be written.

If Circle can reshape its business model from "holding equals earning" to "usage equals rewards," the game could potentially continue.

Furthermore, USDC's growth is not solely driven by yields. The world's largest prediction market, Polymarket, runs on USDC, and such trading demand won't vanish simply due to a ban.

Last year, Circle also launched Arc, a Layer-1 blockchain designed for stablecoin financial scenarios, covering global payments, foreign exchange, and asset tokenization, attempting to expand its business from stablecoin issuance to financial infrastructure. USDC will not die, but whether it can maintain the growth rate of the past year remains in serious doubt.

Looking back, this crash serves as a wake-up call for all crypto companies.

In recent years, the most successful cohort in the crypto industry has embraced a regulatory-friendly route. Circle epitomizes this route as a model student: actively pursuing an IPO, transparent audits, and proactive lobbying, everything aimed at proving to Wall Street that it is a suited financial innovator. The market has rewarded this, with the stock price soaring several times within less than a year. Fourth-quarter revenue reached $770 million, a year-on-year increase of 76.9%, and earnings per share of $0.43, significantly surpassing market expectations of $0.25. On the surface, this appears to be a rapidly growing good company.

However, the draft of the CLARITY Act exposes an uncomfortable reality: compliance means voluntarily putting yourself within the range of regulatory scrutiny. Tether operates overseas, making this ban not directly impactful to it; Circle, as a publicly listed company in the U.S., can only accept scrutiny obediently. Compliance provides Circle with armor, but it also gives it shackles.

The bill is still under negotiation, and the story is far from over.

But this day in March 2026 is worth remembering: when the innovations of the crypto world touch the interests of traditional finance, which way the scale on Capitol Hill tips ultimately depends on who has the louder voice in Washington.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。