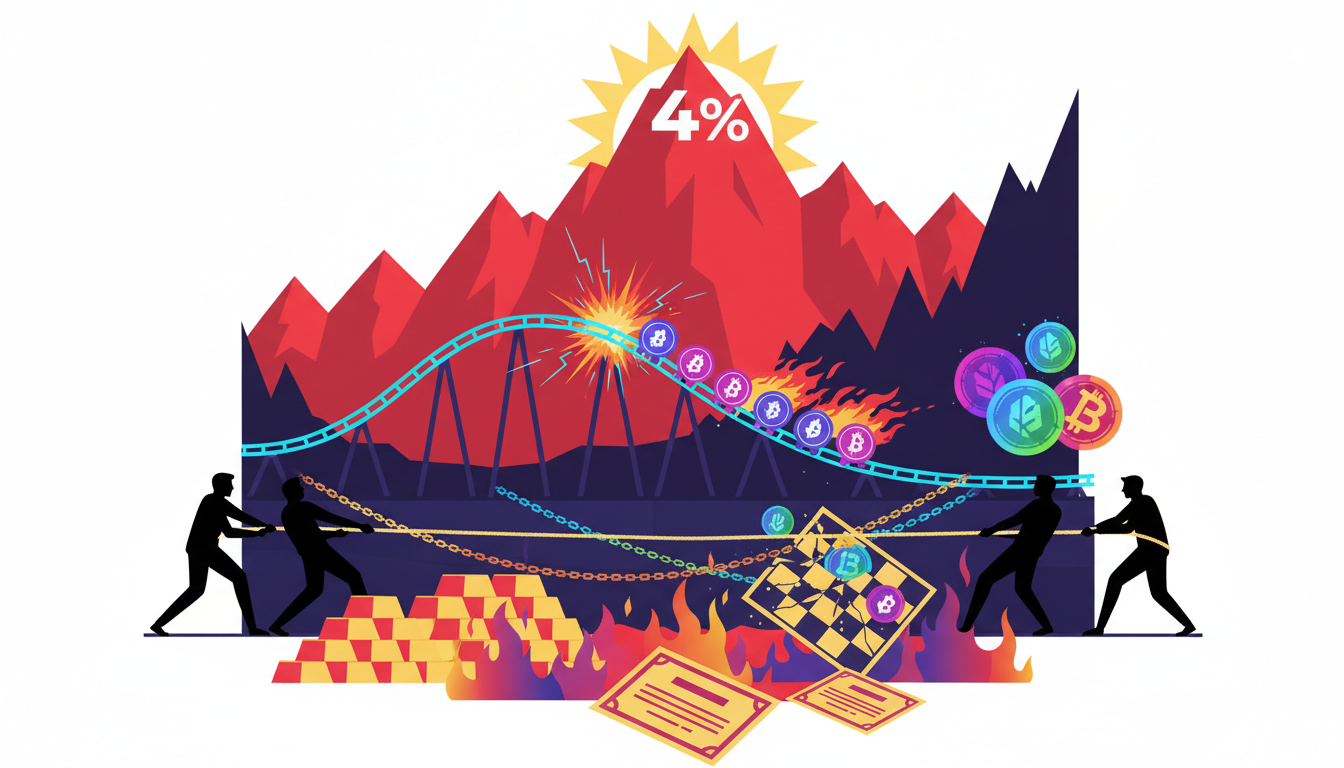

This week, under Eastern Standard Time, the tensions between the U.S. and Iran have continued to escalate, initially triggering a collective plunge in risk assets during the Asian trading session. The South Korean stock market experienced a sharp decline, and the Nikkei saw significant drops, with even gold, which is usually regarded as a safe haven, experiencing a rare and substantial retracement. The market was at one point close to a shutdown and critical clearing state. KOSPI, Nikkei 225, and gold futures all dropped simultaneously in the same time window, with overseas contracts such as EWY also softening, demonstrating a magnified downward resonance across stock indices, currency markets, commodities, and derivatives. On the surface, geopolitical sentiment is spreading, but deep down, it is compounded by high leverage structures and the failure of traditional safe-haven assets, triggering a systemic pressure test that crosses traditional and crypto markets.

Near Market Shutdown for Korean Stocks: A 6% Plunge and Fund Stampede

In response to the direct shock of escalating U.S.-Iran tensions, the South Korean stock market became the first major battleground in Asia to react sharply. KOSPI plummeted by 375.45 points in a single day, a drop of 6.49%. Throughout the day, there were multiple instances of sudden liquidity contraction and withdrawal of buy orders, as the trading floor shifted from active speculation to passive defense. For many local institutions, risk management models were forced to quickly reassess related assets, with risk control lines being breached one after another. Trading volume conspicuously shifted from price discovery to position adjustments and stop-loss exits.

In sync with the local market, overseas instruments tracking Korea also began to reflect the attitude of capital withdrawal. The price of EWY contracts dropped to $122.5, a single-day decline of about 4.2%, indicating that it was not just a single market sentiment out of control, but a global contraction of risk exposure to Korea. Some hedge funds quickly reduced positions or hedged inversely through EWY, further amplifying the spread volatility between index futures and spot, making an already tense order book even weaker.

The sudden drop at the index level directly increased margin requirements, with a large number of financing and derivative positions based on KOSPI component stocks passively raising margin ratios. For accounts already operating at high utilization rates, there was limited room for additional margin, and they could only fill the gap by rapidly selling liquid blue chips, which in turn pushed down the index level. The chain of stock index dropping—margin adjustment—passive selling—further decline pushed the market toward the edge of a shutdown, with clearing risk continually amplifying during trading.

Nikkei's Sharp Decline and Thailand's Trading Halt: Acceleration of Risk Spread in Asia

Korea is not an isolated case; the expansion of risk within the Asian region has occurred almost simultaneously. The Nikkei 225 index fell by 1857.04 points in a single day, a drop of 3.48%, which, although slightly more tempered compared to KOSPI, is a highly abnormal single-day shock for the typically less volatile Japanese market. This trend indicates that capital is not limiting risk to Korea but is instead compressing the weight of Asia-Pacific equity assets overall, with regional risk premiums rapidly increasing.

More intuitive panic signals appeared in the commodity and derivative markets. In Thailand, amid increasing volatility in the precious metals market, a temporary trading halt was implemented for gold futures, forcing trading to pause, freezing the market screen at a moment of intense volatility. For traders holding high-leverage positions, this state of being “locked in volatility” is more oppressive than a simple price drop: unable to adjust positions or stop losses, they can only passively wait for repricing after the market opens.

When regional stock indices and commodity contracts simultaneously suffered declines in a short period, Asia's overall risk premium was significantly raised. The stock market's downturn weakened local wealth effects and risk tolerance, while trading limitations on bulk commodities and precious metals also diminished traditional hedging channels. Capital started paying higher premiums for assets that could be “quickly realized and controllable in volatility.” For cross-market investment portfolios, the expected hedging effect that was originally anticipated through multi-asset diversification was significantly weakened in this correlated plunge, with systemic risk exposure passively amplified.

Gold Breaks Below 4200: Traditional Safe-Haven Logic Questioned

Against the backdrop of geopolitical tension and stock market plummets, gold dropped about 6% in a single day, falling below the critical level of $4200, sharply contrasting with many investors' traditional expectation of “risk escalation—strengthening of gold.” The market performance did not show an influx of panic buying, but was instead dominated by long stop losses and leveraged liquidations, with the breach of key points triggering technical sell-offs combined with program trading, creating a rare scene of a “reverse plunge” in safe-haven assets.

The pricing in the foreign exchange and interest rate markets provides important clues to this “failure” of gold. Justin Low pointed out that the price of precious metals in this round of rise was highly dependent on expectations of central bank interest rate cuts, and once the policy expectations turn, the core logic supporting gold prices will quickly weaken. In other words, what has driven gold up in recent times has been more about liquidity and interest rate expectations, rather than pure geopolitical hedging demand. When interest rates and dollar expectations change, the previous gains become difficult to sustain.

BMI's report highlights from a macro perspective that a strong dollar and a shift in Federal Reserve policy are dominating the current market landscape. When the dollar returns to a strong cycle, global liquidity flows back into U.S. assets, with gold often under pressure in the pricing system: on one hand, a strong dollar directly suppresses gold prices denominated in dollars; on the other, higher or more “stubborn” interest rate expectations raise the holding costs of gold. In the interplay between geopolitical conflicts and dollar cycles, gold's current drop essentially shows that “interest and currency expectations” have triumphed over “hedging narratives.”

Leverage and Whale Game: Risk Amplifier Behind an $8 Million Profit

While most investors are busy cutting losses amid gold's sharp fall, there are also those standing on the other side of this “flash crash of safe-haven assets.” According to a single source, a whale positioned in short positions for GOLD and SILVER holds a book profit of about $8 million, making them a rare contrarian winner. Although the specific scale of their position and opening price have not been verified by multiple parties, this case alone reveals that in high volatility environments, betting against safe-haven assets that cannot move up or may even plummet, can yield profits far exceeding typical returns.

However, the leveraged shorts in the gold and silver markets are also amplifying both profits and risks. For heavily leveraged shorts, any sudden increase driven by geopolitical events could trigger margin calls or even forced liquidations; once the market moves up and then down, capital has to endure the dual test of “multiple liquidations + correct directional judgment.” The simultaneous drop of gold and silver has concentrated profits for those who held out through prior volatility, but this pathway itself is based on high volatility, high leverage, and high psychological thresholds.

From on-chain derivatives to over-the-counter (OTC) contracts, high-leverage structures are turning precious metal prices into more easily magnified variables. Perpetual contracts in on-chain protocols and traditional off-exchange options will generate a series of "chain liquidation" actions through hedging and rebalancing at key price levels: when capital on one end is forced to liquidate, it triggers hedging adjustments in the market on the other end, compounded by automated liquidation mechanisms, ultimately forming a passive acceleration of prices through a “waterfall effect.” In such a system, the story of an “$8 million profit” is often just the tip of the iceberg above many liquidated accounts.

On-chain Derivatives and Trading Platforms: Who is Amplifying Volatility?

During the same period of intense fluctuations in traditional markets, leading crypto platforms are also playing out their rhythms. Bitget chose to launch a new trader promotion during the period of extreme volatility, which could objectively attract a batch of incremental short-term capital, attempting to capture “mispriced” or “overly volatile” through high-leverage contracts. For trading platforms, such activities help amplify transaction volumes and market participation in the short term, but amidst unclear macro risks, they also mean more emotional and path-dependent leveraged funds flooding the market.

The high-leverage contracts offered by on-chain derivatives and centralized trading platforms are forming a resonance mechanism with the volatility of traditional markets. When Asian stock indices plunge and gold flash crashes, the funding rates, leverage multiples, and liquidation lines of crypto contracts are rapidly pushed up, with some traders using BTC, ETH, or even gold and silver tokens as “shadow assets” to hedge against or amplify their judgments on traditional markets. This causes a shock that was originally confined to stocks and commodities to be transmitted into the on-chain ecosystem along the chain of risk expectations and trading logic, evolving into volatility across markets and multiple assets.

Driven by activities, the short-term increase in trading volume intertwines with the liquidation chain, having a bidirectional impact on market depth and slippage. On one hand, the new orders and counterparties enhance the apparent depth within a short period, misleading traders into believing “any direction can be executed quickly”; on the other hand, when prices near the liquidation range of significant leveraged positions, automatic liquidation orders surge, instantly consuming the true liquidity of the order book, dramatically magnifying the slippage between actual transaction prices and expected quotes. Behind the surface excitement lies a more fragile microstructure and a more easily triggered systemic liquidation.

From Geopolitical Conflict to On-chain Liquidation: How to Respond to the Next Shock

Looking back at this round of events, the tensions between the U.S. and Iran were the spark, but what truly drove the escalation of market volatility was the multiple overlaps of geopolitical issues, dollar cycles, safe-haven asset logic, and leverage structures. The collective decline of Asian stock indices, coupled with gold falling below $4200 and the sudden 6% drop, shows that when the dollar strengthens and Fed policy expectations shift, the traditional notion of “buy gold for hedging” is not robust. Meanwhile, from the margin pressures triggered by KOSPI's plummet to the strong liquidation chains in precious metals and crypto derivatives, leveraged tools are both risk management instruments and volatility amplifiers in this shock.

It is foreseeable that, under the backdrop of global funds allocating across markets more frequently and Asian investors extensively using leverage and derivatives, the sensitivity of Asian markets to geopolitical risks is being structurally amplified. News of a regional conflict will not only rapidly reflect in local stock markets but will also create a multi-channel echo chamber effect through ETFs, futures, forex hedges, and even on-chain perpetual contracts and options. The market is no longer a series of isolated ponds but resembles a highly coupled water system: any “release or withdrawal” on one end can provoke disproportionately large ripples on the other end.

For investors, the primary prerequisite for responding to future similar shocks is to reexamine the boundary roles of “safe-haven assets” and “leverage tools.” Gold, yen or bonds do not necessarily serve as a cushion in the same direction in all scenarios; and leverage itself is neither a monstrous flood nor a free lunch to amplify profits, but rather a strict magnifying glass for risk awareness and discipline execution. On a strategic level, incorporating scenarios that weigh liquidity shocks and liquidation paths more heavily while controlling overall leverage multiples and diversifying single event exposure will prove more valuable for survival than merely chasing short-term volatility.

In a market where a geopolitical event can penetrate to on-chain liquidation structures within hours, the real advantage does not lie in “who runs faster,” but in who builds a more stable position and clearer risk control framework beforehand. The next black swan may not come from the same sky, but the market's response paths are likely to become increasingly similar.

Join our community to discuss and strengthen together!

Official Telegram Community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX Welfare Group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance Welfare Group: https://aicoin.com/link/chat?cid=ynr7d1P6Z

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。