Author: David, Deep Tide TechFlow

On March 18th, another blockchain mainnet was launched.

It's called Tempo, backed by Stripe and Paradigm. Stripe is one of the largest online payment companies in the world, handling $1.9 trillion in transactions last year; Paradigm is one of the largest venture capital firms in the cryptocurrency industry. Together, they invested $500 million in Tempo last year, valuing the project at:

$5 billion.

This $5 billion blockchain doesn’t hype tokens, doesn’t do DeFi, doesn’t issue memes. On the day of the mainnet launch, Tempo's most prominently announced product is:

Allowing machines to pay machines.

This sounds a bit abstract; you can understand it as AI needing to spend money at every step. Calling an API costs money, buying a segment of computing power costs money, pulling a batch of data from the database costs money...

But the existing payment systems are all designed for people; bank accounts require identification, credit cards require facial recognition, and Alipay requires mobile verification codes.

AI can’t pass any of these.

It can help you complete an entire workflow, but when it comes time to pay, it has to stop and wait for a human to press "confirm."

Thus, alongside the mainnet launch, an open protocol called MPP (Machine Payments Protocol) was launched, co-written by Stripe.

Simply put, it establishes a set of rules for transactions between machines, including how to request payment, how to authorize, how to settle, etc.

The envisioned scenario is that AI can autonomously spend money within a preset limit without needing a human to sign off on every transaction. On the day of launch, over 100 service providers had already connected, including OpenAI, Anthropic, and Shopify.

But Tempo is not the only one doing this this week.

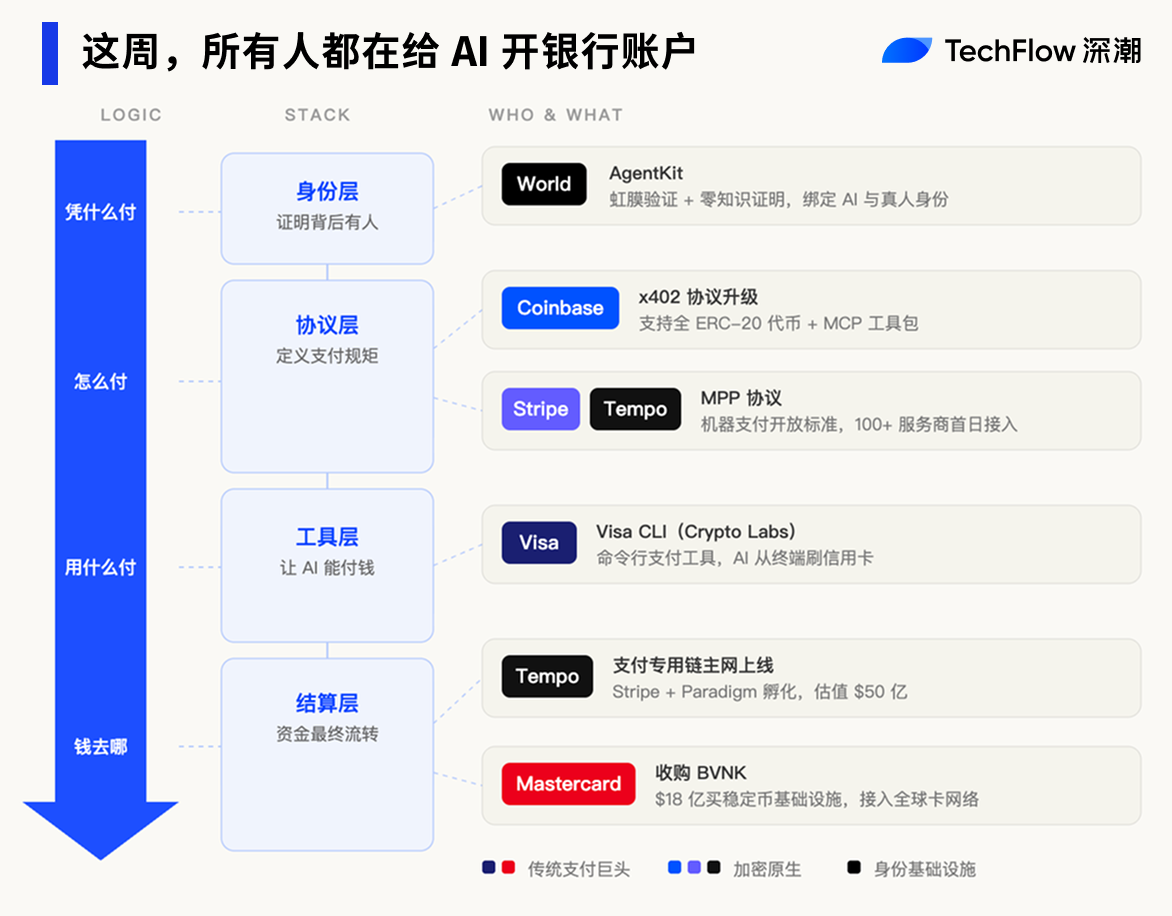

Within five days, Visa established a new department to release AI payment tools, Coinbase’s payment protocol underwent a major upgrade, Mastercard spent $1.8 billion to acquire a stablecoin company, and Sam Altman's World released a toolkit specifically for AI identity verification.

Five giants rushed through the same door in a week, eager to open bank accounts for AI.

Two paths, the same door

Tempo is focused on helping AI settle payments. But settlement is just one part of the payment system. An AI agent must also have payment tools, funding channels, and identity verification to truly spend money autonomously.

Both traditional payment companies and cryptocurrency companies are competing for a piece of the cake in their own ways.

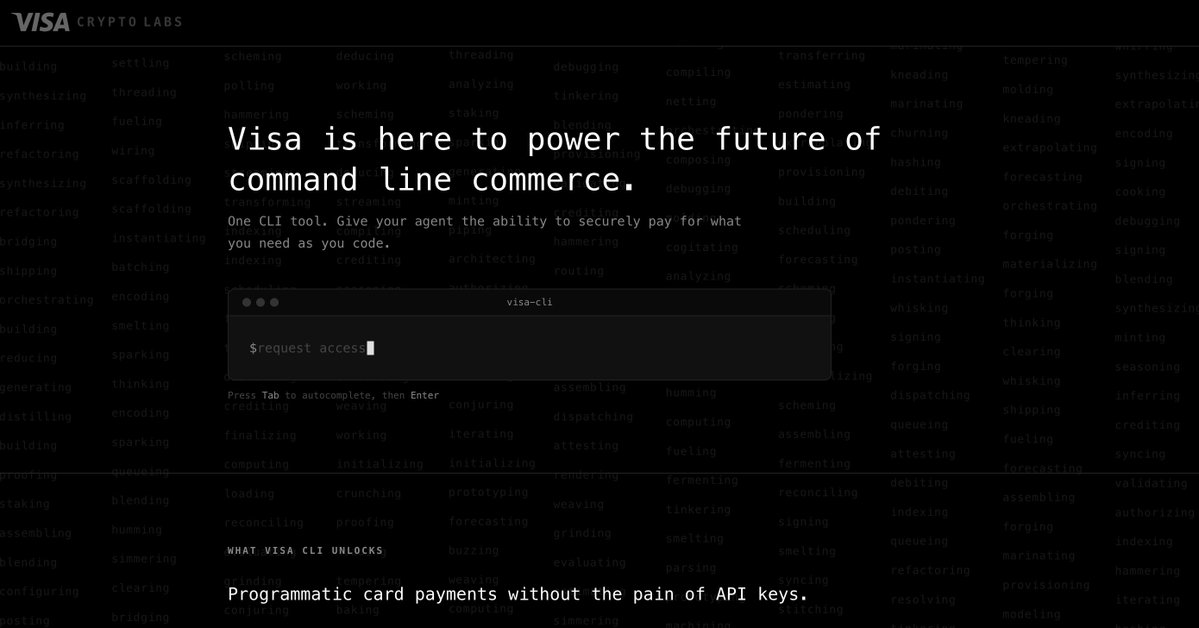

On March 18, the same day Tempo's mainnet went live, payment giant Visa also took action. The newly established Crypto Labs department launched its first product: Visa CLI, a tool allowing AI agents to initiate credit card payments directly from terminals.

No API keys, no pre-registration needed; whenever AI needs to buy a service during tasks, it can pay with just one command. Visa calls this "command line commerce."

Visa's global card network connects billions of cards and tens of millions of merchants. If AI payments can run on this existing network, it won't need to wait for any new infrastructure to mature.

Visa is extending the old path. Its competitor Mastercard chose a different approach: directly buying the path.

On March 17, Mastercard announced its acquisition of London-based stablecoin infrastructure company BVNK for $1.8 billion. This is the largest stablecoin acquisition in history.

The purpose of this acquisition is straightforward: if AI payments need to be made in stablecoins, then those stablecoins will flow through my pipeline.

On the cryptocurrency side, the moves are similarly intensive.

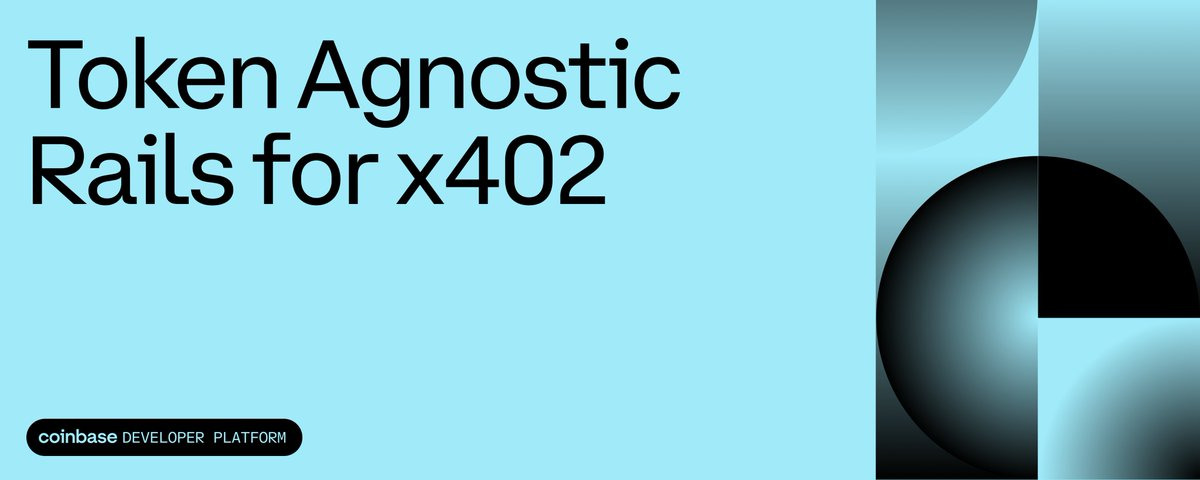

Coinbase's x402 protocol completed a major upgrade, expanding payment scope from a few stablecoins to all ERC-20 tokens, while releasing the MCP toolkit, allowing developers to connect AI tools to payment networks with one click.

Although it seems both sides start from different points, their actions point in the same direction: traditional payment companies are embracing cryptocurrency, and cryptocurrency companies are embracing AI. Ultimately, the cryptocurrency infrastructure is transforming into the foundational pipeline for AI payments.

One piece remains. AI can spend money, but how do merchants know that the AI spending is backed by a responsible party?

On March 17, Sam Altman's co-founded World launched AgentKit, integrating with Coinbase's x402. Its sole function is to ensure that while AI is making payments, it also proves that a verified real person stands behind it. Merchants can confirm someone is responsible for the transaction, but they cannot see who that person is.

In five days, five companies have filled the slots for settlement, channels, tools, protocols, and identity.

The AI cake is distributed, only the cash register remains

Over the past three years, the positions in the AI industry chain have mostly been taken.

The model layer is bench-marked by OpenAI, Anthropic, Google, and numerous Chinese companies, while computing power is tightly locked by Nvidia, and the application layer is a bloody sea, from programming assistants to search engines...

Every layer is crowded, and the competitive barriers are getting higher.

However, this payment layer remains relatively vacant.

It’s not that no one has thought about it; the timing just hasn’t been right. AI agent payments have a prerequisite condition: AI must first have the ability to independently complete an entire task chain. If it can only chat without needing to call APIs, buy computing power, or hire other agents to work, then payments are not a necessity.

Over the past year, this prerequisite has gradually been established.

OpenClaw allows AI to directly operate computers, the MCP protocol enables AI to connect to external services, and the capabilities of various large models' agents are expected to break through significantly in the second half of 2025. AI is transforming from a "dialogue tool" into a "work tool," and working requires spending money...

The need for spending has arisen, but the infrastructure for spending does not yet exist.

That’s why Stripe, Visa, Mastercard, and Coinbase are all taking action at the same time. For traditional payment companies, this is their first opportunity to gain a home-field advantage amidst the AI wave. They cannot build models, nor can they manufacture chips, but payment is something they have been doing for decades.

Visa's global card network connects billions of cards and tens of millions of merchants, Mastercard covers over 200 countries, and Stripe processed $1.9 trillion in transactions last year. If every AI expenditure can flow through these pipelines, the more capable the AI becomes, the more profit they make.

For cryptocurrency companies, the logic is somewhat different.

Coinbase CEO Brian Armstrong has previously made a straightforward statement: "AI can have a cryptocurrency wallet, but cannot open a bank account."

Every step of the traditional financial system confirms "who you are." Opening bank accounts requires identification; obtaining credit cards requires facial recognition; every transaction requires SMS verification codes. AI is software, not a person, and it cannot pass any of these checkpoints.

But cryptocurrency wallets do not need these. A private key is an account; for AI agents, on-chain payments are the path of least resistance.

Whether encrypted or not, AI payments will be a new market at the infrastructure level. The only difference is whose pipeline is more suitable for machines.

The road is built, but no cars have arrived

As the story goes, it seems everything is ready, the five giants are in their positions.

But there is one number worth noting.

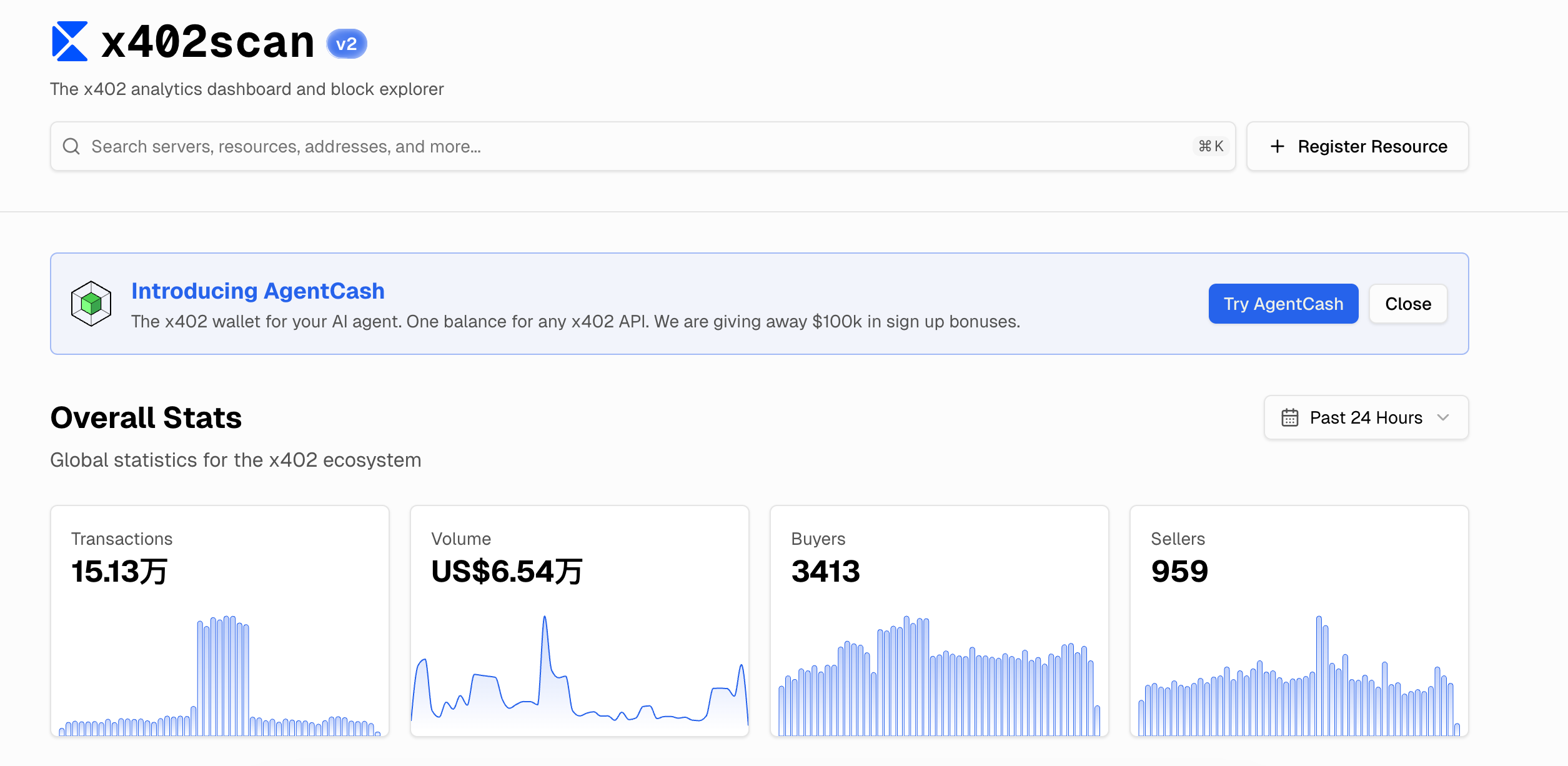

Coinbase's x402 protocol is currently the earliest and most widely adopted AI payment protocol. According to data from x402scan, in the past 24 hours, the total transaction volume across the ecosystem was $65,400. There were 150,000 transactions, averaging less than $0.50 per transaction.

What infrastructure supports this number? Tempo is valued at $5 billion, Mastercard spent $1.8 billion to acquire BVNK, Visa established a new department, and Stripe is personally involved in writing protocols.

Infrastructure valued in billions of dollars serves a market whose daily transaction volume resembles that of a street-side milk tea shop.

All infrastructure businesses seem to follow this norm.

On the eve of the internet bubble in 2000, telecom companies laid millions of kilometers of fiber optics under the sea. After completing this, they found that global internet traffic only utilized 5% of it. Most of those companies went bankrupt, but the fiber optics remain.

Ten years later, video streaming and mobile internet filled those pipes. The road builders did not profit, but the road is real.

AI payments are currently at this stage. The logic of demand is established: AI agents are indeed becoming more capable, needing to spend autonomously, and require a new financial infrastructure.

Everyone has reached the starting line, but after the starting gun fires, they find there is only themselves on the track for now.

As for whose path will ultimately win out and when the first truly autonomous transaction by an AI agent will happen in your life, it may occur faster than everyone expects, or perhaps slower than everyone anticipates.

The only certainty is that this battle has already begun, and our wallets may be the last to know.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。