┈➤SKY Temporarily Reduces Buyback

Following JUP's consideration to pause or reduce token buybacks in January this year (the final buyback remained unchanged, but the airdrop release was reduced), the SKY community has recently voted on a proposal to temporarily reduce the buyback ratio of SKY from 75% of net profit to about 7.5%, expected to last for 3 months.

The saved funds will be used to increase SKY's "surplus reserve buffer" to cope with the "potential oil price shock caused by the Iran war." This shock could affect global interest rates, credit risks, and stablecoin demand.

The buyback proposal for SKY mentioned that the existing "surplus reserve buffer" is only about $50 million. Given the $11.26 billion market cap of USDS, there is indeed a need to supplement the "surplus reserve buffer" under the current circumstances, which is why the proposal was passed with a rate of 99.85%.

In the medium to long term, there is indeed not much impact on the price of SKY, neither negative nor positive.

However, in the short term, the expected reduction in buybacks may have an uncertain emotional impact.

From JUP to SKY, the buyback mechanism has sparked discussions once again. In terms of buybacks, debridge is a case that Bee Brother continues to pay attention to.

┈➤Path of debridge Foundation's Buybacks

Firstly, the early stage will accumulate the profits from the debridge protocol into a fund.

Secondly, a portion of the funds will be reserved, with the remaining part of the fund deposited into different ecological chains and various types of DeFi protocols to obtain diversified liquidity returns to maintain the project's continued operation. This includes Meteora and Kamino on the Solana chain, and Aave and Kamino and Aave on Ethereum and Arbitrum.

Finally, starting in June 2025, the protocol profits will be used to buy back DBR.

Unlike JUP and SKY, on one hand, debridge will use all protocol profits to buy back DBR.

On the other hand, this buyback from debridge has been ongoing for nearly 9 months since June 2025. The project team has not expressed any intention to pause or reduce the buybacks. This is because the foundation funds provide debridge with relatively sufficient risk resistance capabilities.

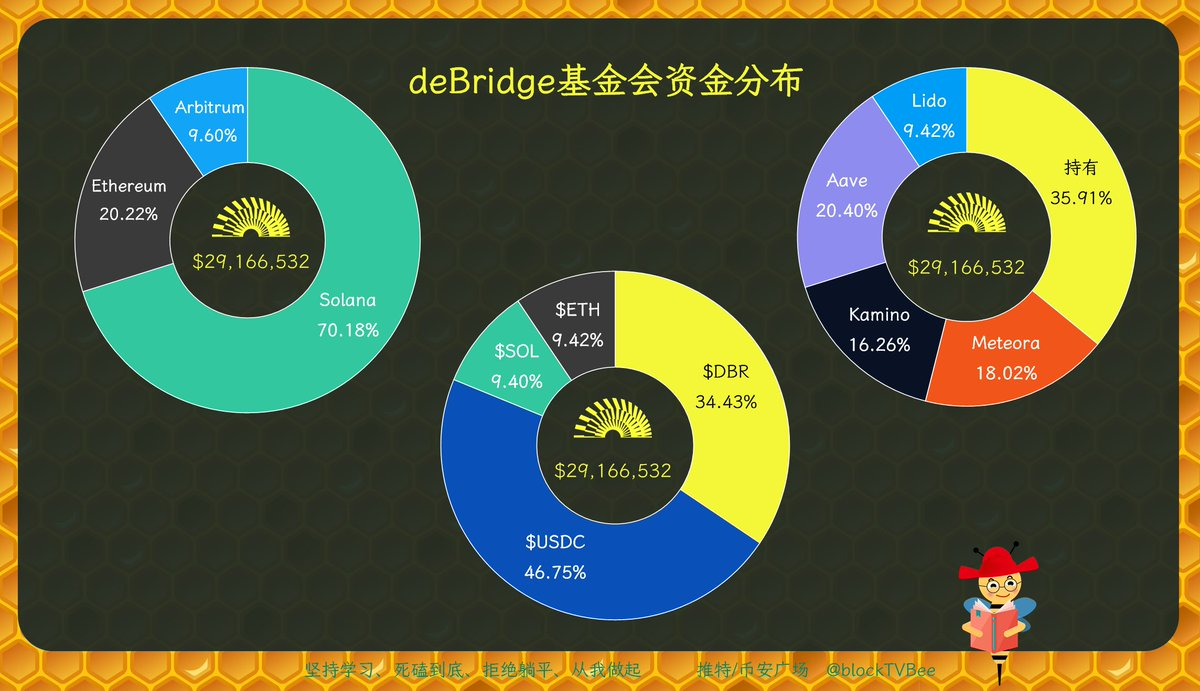

┈➤Funding Distribution of debridge Foundation

The total amount of deBridge foundation funds is about $29.17 million, of which 70.18% is on the Solana chain, 20.22% is on the Ethereum chain, and 9.6% is on the Arbitrum chain. These three ecosystems are exactly the thriving ecosystems of DeFi.

46.75% is stablecoin $USDC, providing stability for the deBridge fund. 34.43% is $DBR, and 9.4% and 9.42% are $SOL and $ETH respectively.

The portion held in funds but not deposited into DeFi protocols accounts for 35.91%, preventing risks from DeFi protocols. Other funds are distributed across different DeFi protocols, with the maximum accounting for 20.4% and the minimum for 9.42%, showing a non-concentrated distribution.

┈➤In Conclusion

Teacher Jtsong2 once wrote an article analyzing the design thinking of the project, the first point being asset design, and deBridge has two major characteristics in this regard.

In dynamics, deBridge first conducted an airdrop, and after the token selling pressure was sufficiently released, the buyback began, perhaps considering both market conditions and macro factors at the same time; and a significant portion of the early profits was used to establish the fund; the fund provides a cash flow for the continuous operation of deBridge and risk defense.

In terms of static aspects, the distribution of deBridge's funds also needs attention, with most in the Solana ecosystem, which is deBridge's starting point, followed by Ethereum and Arbitrum, providing liquidity to the core DeFi ecosystem; a large portion is stablecoins, which provide certain guarantees for the foundation's stability; a significant portion of funds has not participated in DeFi, while other funds are more evenly distributed across various DeFi protocols. Overall, deBridge's fund distribution is relatively balanced, helping to diversify risks.

Of course, DBR buybacks and JUP buybacks have a certain degree of comparability; fundamentally, both are DEX. However, SKY is a lending platform with stronger risks, hence the comparability is relatively weaker. What is certain is that how to design the path for token buybacks and make adequate preparations before buybacks are both crucial.

Finally, since we mentioned $DBR, I would like to remind $DBR holders that multiple platform data indicates that 618.33 million DBR will be unlocked on April 17, accounting for 12.9% of the total token supply.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。