Written by: Michiel Milanovic

Translated and Organized by: BitpushNews

In the past two weeks, payment giant Stripe announced a tender offer valuing the company at up to $159 billion.

Meanwhile, financial technology infrastructure provider Plaid also completed a tender offer with a valuation of $8 billion.

A few days later, Robinhood's first venture capital fund (Ventures Fund I) was listed on the New York Stock Exchange (NYSE), allowing retail investors direct access to a basket of private equity companies.

These events are interlinked and reflect a structural shift in how companies raise funds, provide liquidity, and ultimately consider going public.

Why do I say that?

Let’s start with Plaid.

The company, founded in 2013, serves as an infrastructure layer that connects consumers' bank accounts to financial apps like Venmo, Robinhood, and Chime. Applications pay Plaid to enable users to seamlessly connect their banks, verify credentials, and share account information. This is particularly valuable in the U.S. because the regulations do not mandate banks to share information with third parties (unlike the UK's open banking and the EU’s PSD2).

In fact, reports say that half of Americans have indirectly used Plaid's services through various financial applications. The company reached a peak valuation of $13.4 billion in 2021 and was once planned to be acquired by Visa for $5.3 billion, but regulators ultimately blocked the deal. After being repriced at $6.1 billion in April 2025, its latest $8 billion tender offer reflects a resurgence in momentum, with projected revenue of $430 million in 2025, and 20% of new customers now being AI companies.

Meanwhile, Stripe, founded in 2010 by brothers John Collison and Patrick Collison, is a giant in payment services.

With exponential growth in e-commerce over the past decade, the company recently reported astonishing performance for 2025. The total payment transaction volume reached $1.9 trillion, a year-on-year increase of 34%, equivalent to about 1.6% of global GDP. Although revenues have not been disclosed, sources estimate minimum revenue of $5 billion for 2024. Today, Stripe’s revenue suite (including Stripe Billing, Invoicing, Tax, etc.) is expected to achieve an annual run rate (ARR) of $1 billion.

In addition to payments, Stripe is actively positioning itself around cryptocurrency and agentic commerce, viewing them as catalysts for online consumption. It acquired the stablecoin platform Bridge for $1.1 billion, purchased wallet infrastructure provider Privy, and is building Tempo—a payment-focused L1 blockchain currently being tested by Visa, Nubank, and Klarna. Its latest tender offer price of $159 billion has increased by 74% compared to last year.

ARK Invest Big

ARK Invest Big

A tender offer is a type of secondary transaction that allows new investors or existing investors to buy shares directly from employees and early shareholders. It provides liquidity without diluting company equity and without being affected by IPO regulations and structural burdens.

Stripe and Plaid are part of this larger trend: companies successfully bypassing the public market in favor of private transactions.

Reports indicate that Anthropic is exploring a tender offer with a valuation exceeding $350 billion, while Revolut recently completed an employee stock sale with a valuation of $75 billion.

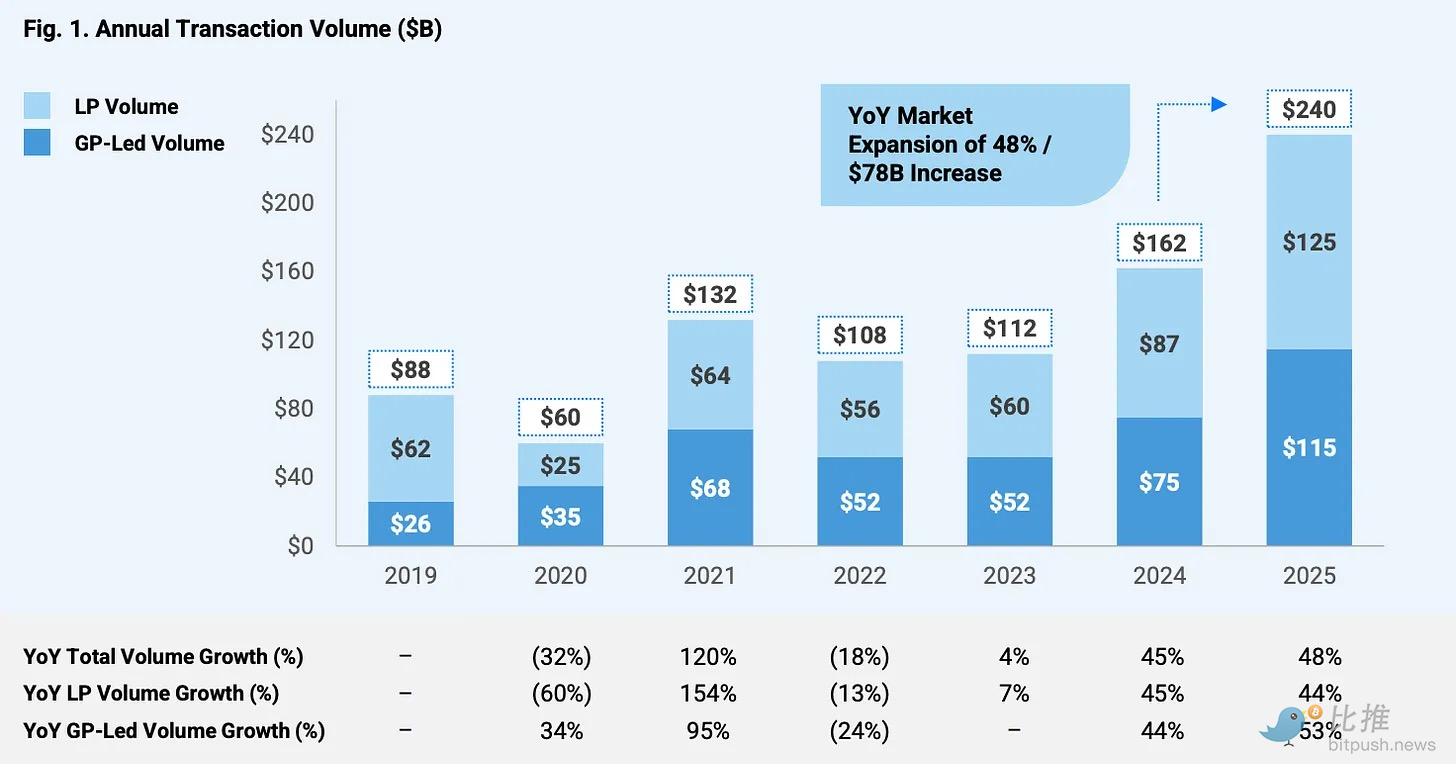

In 2025, the private secondary market transaction volume soared to $240 billion, compared to $162 billion in 2024. In contrast, the global funds raised through traditional IPOs amounted to about $140 billion.

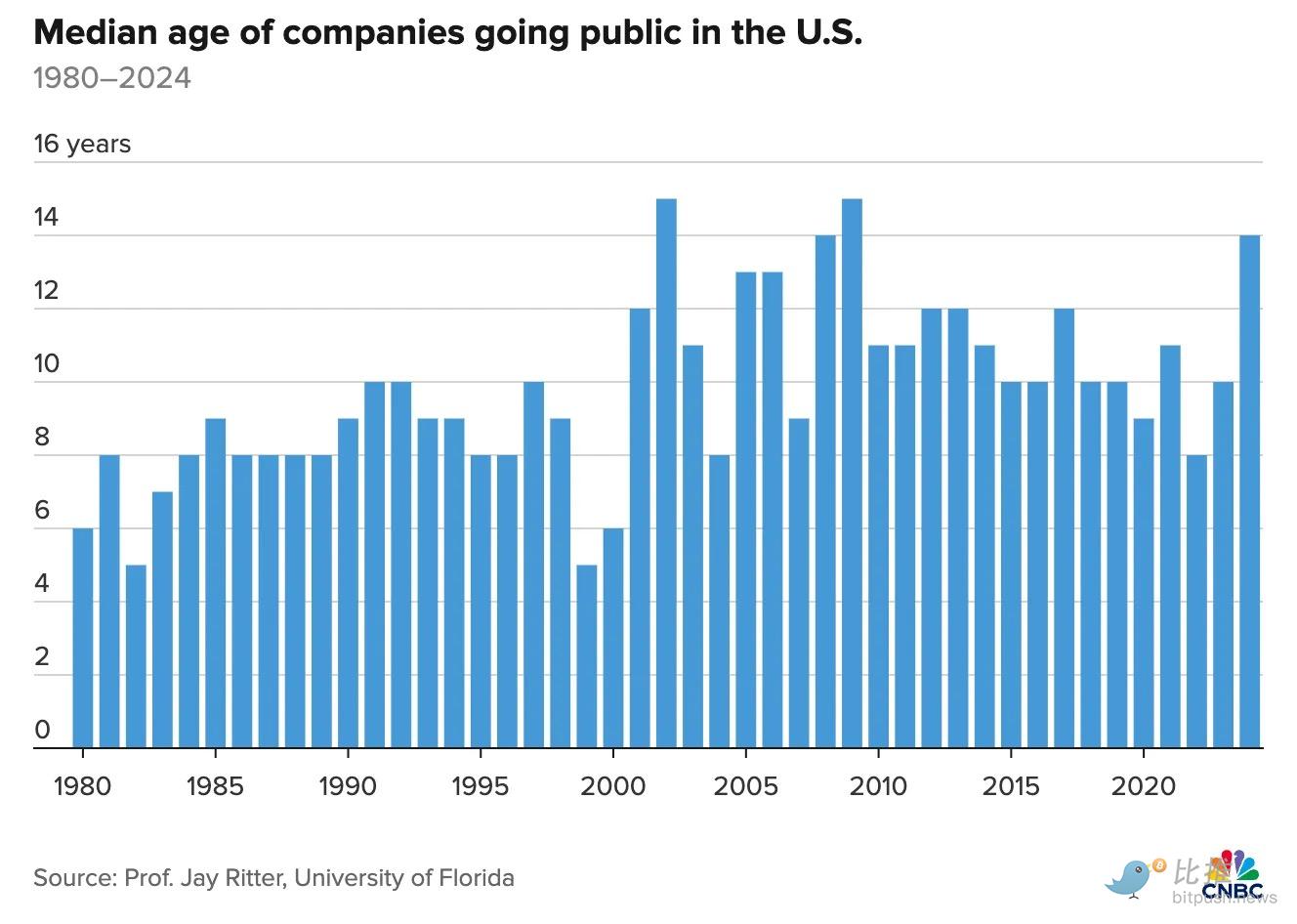

As the private capital market flourishes, the pace at which companies enter the public market has slowed. Currently, companies on average wait 16 years to go public, which is 33% longer than a decade ago. Over the past 12 years, the total asset value in the private market has more than doubled, reaching $22 trillion. Some of the world’s most valuable companies, including SpaceX and OpenAI, remain private, with valuations that rival or exceed those of major public companies.

This has led to two key market developments:

First, the emergence of a new capital market infrastructure layer. We recently analyzed the rise of platforms like Forge and EquityZen, which facilitate secondary trading of private company stock. Charles Schwab acquired Forge in November for $660 million, while Morgan Stanley acquired EquityZen in October (the amount was not disclosed).

Second, the private market is opening up to retail investors. Robinhood’s newly established Ventures Fund I was listed on the NYSE last Friday, raising $658 million and holding stakes in large private companies like Ramp, Stripe, and Revolut. This is not the first of its kind; Destiny Tech100 was listed in March 2024, offering a portfolio of 100 venture-backed companies, including SpaceX and OpenAI. However, Robinhood can distribute directly to its 28 million users, and, as evidenced by its performance in public equities, it has a successful track record in popularizing asset classes that were historically limited to institutional investors.

Additionally, the Trump administration signed an executive order last summer paving the way for investments in alternative assets like cryptocurrencies and private markets through $87 trillion in 401(k) retirement accounts.

We view these as major catalysts for further growth, but they also expose some hidden risks.

One of them is the structural complexity behind purchasing private stock. Brokers typically bundle these stocks into their own special purpose vehicles (SPVs) and charge fees, and these SPVs sometimes hold positions in other instruments. These overlapping counterparty risks and fees can obscure the actual assets that investors own. The next macroeconomic recession will be accompanied by the collapse of SPV positions and the ensuing litigation.

Additionally, there are issues with valuation transparency. Private company valuations are often anchored to the most recent round of funding, which may only occur once or twice a year. This limits price discovery and creates a gap between the reported net asset values (NAVs) and the prices the public market is willing to pay.

The Financial Times recently reported that Robinhood's Ventures Fund I dropped 11% on its first trading day. Meanwhile, Destiny Tech 100's trading price once reached nearly 20 times its NAV. This unpredictability is not good for retirement savings accounts.

Meanwhile, regulators are beginning to push for reforms to enhance the attractiveness of the public market. SEC Commissioner Hester Peirce expressed concerns about the private market in a February speech: while the pressures to go public have decreased, the private market lacks corresponding price discovery mechanisms, accessibility, and liquidity.

SEC Chairman Paul Atkins recently proposed a three-pillar plan designed to "make IPOs great again" (his words), aiming to achieve this by relaxing disclosure requirements and reforming securities litigation. Whether these reforms will come to fruition remains to be seen.

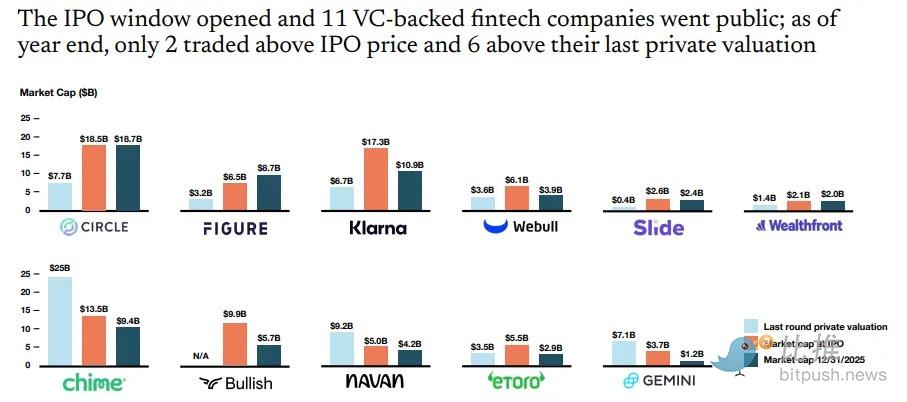

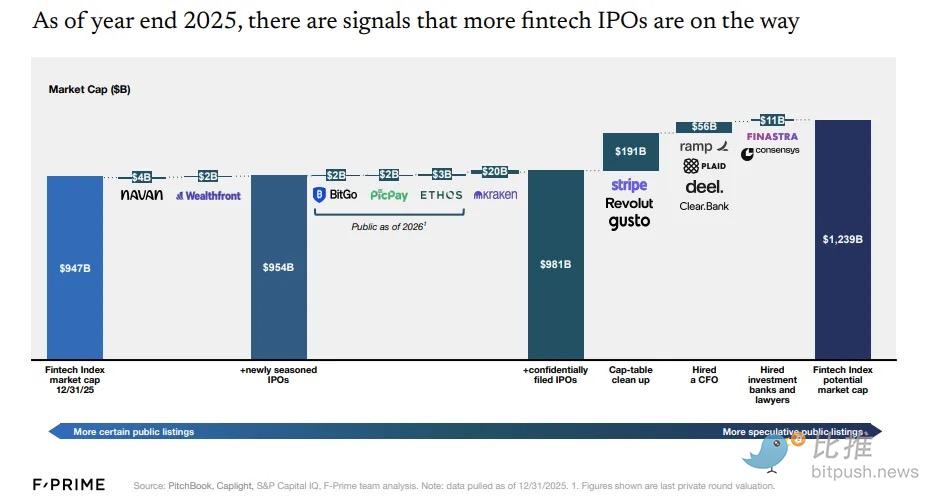

Setting aside private transactions, IPOs have indeed shown a significant rebound in 2025. Eleven venture-backed fintech companies, including Circle and Klarna, have gone public, with more companies on the way. Kraken and Bitgo have filed applications secretly, while companies like Ramp and Gusto are preparing by cleaning up cap tables, hiring new CFOs, or engaging with investment banks. F-Prime estimates the total market capitalization of fintech could grow from $947 billion to $1.2 trillion.

Whether these companies can achieve ideal prices is another question. By the end of the year, only 2 out of 11 companies had trading prices higher than their IPO prices. Chime was privately valued at $25 billion but went public at $13.5 billion. Klarna went public at $17.3 billion but dropped to $10.9 billion by year-end.

With geopolitical tensions rising and macroeconomic outlooks uncertain, companies still on the fence may find that tender offers are the path of least resistance. At least for now, the liquidity in the private market remains ample, enough to absorb the supply of these unicorns.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。