Today, after watching Oracle's financial report in the US stock market after hours, I stared at the data for quite a while.

To be honest, the feeling I have about this company is completely different from a few years ago.

In the past, when people mentioned Oracle, it was mostly regarded as a "traditional database vendor" and a "conventional software company." But this financial report gives me the impression of a #AI infrastructure company.

Here's a simple record 📝 of a few points I've observed, just as an investment note, DYOR:

1️⃣ The revenue growth rate is indeed a bit above expectations.

This quarter's numbers were actually quite surprising; after all, Oracle's stock price had once halved, and there were worries about capital expenditures and cash flow depletion. This high growth has swept away those concerns:

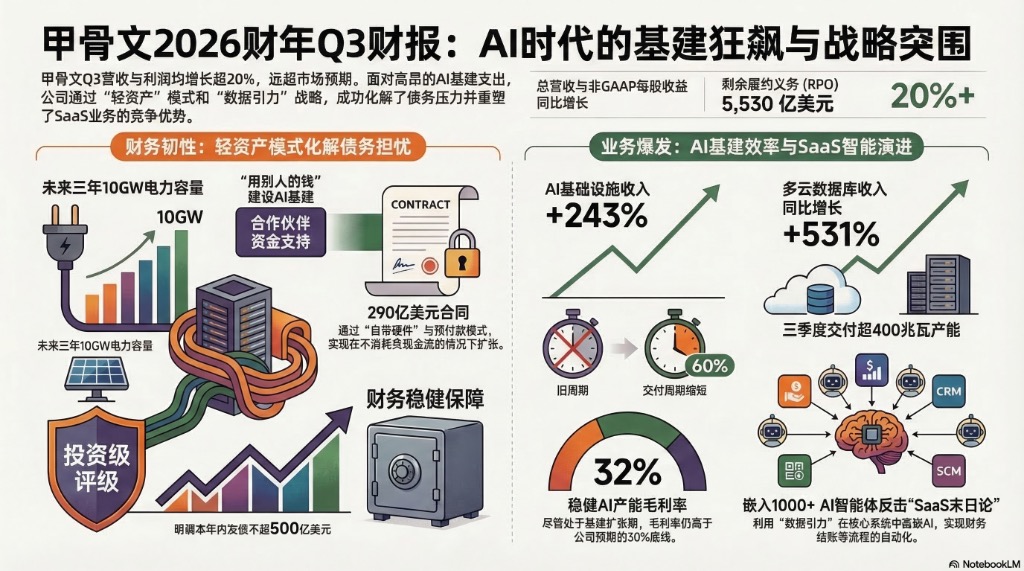

· Revenue of $17.2 billion, a year-on-year increase of 22%

· EPS of $1.79, higher than market expectations

For a company of this size, a growth rate above 20% is already quite rare. I looked through historical data and haven't seen a combination of "revenue + profit over 20%+" like this in about 15 years. So the post-market stock price increase 📈 of over 10% isn't surprising at all.

2️⃣ The demand for #AI computing power is starting to be reflected in cloud revenue.

I have always been quite conservative in my view of Oracle's cloud business, thinking it would be difficult to capture much space between Amazon Web Services and Microsoft Azure.

But this time a number stood out: "IaaS revenue year-on-year +84%."

This growth rate is basically a result directly driven by AI demand. Many AI companies actually do not rely on just one cloud provider. During the training and inference phases, they will simultaneously use multiple computing power suppliers.

The high-performance GPU clusters and network architecture that Oracle has bet on in recent years are perfectly positioned to take advantage of this wave of demand. The earnings call also mentioned that some major clients are migrating to Oracle's computing power clusters.

3️⃣ One indicator that shocked me: RPO

There is an indicator in the report that I looked at twice: RPO (Remaining Performance Obligations) $553 billion.

Simply put, RPO represents orders that have been signed but not yet recognized as income. This number has nearly tripled year-on-year.

For me, this is more important than the profits of the current quarter because it signifies the "visibility" of future income over the next few years.

What's more interesting is that the company revealed many of the orders are actually clients pre-paying or bringing their own GPUs to collaborate in building data centers. This point is crucial in the current AI infrastructure cycle.

4️⃣ About "capital expenditures," I have changed some of my views.

I had been worried that Oracle's investments in data centers might be too heavy, as the company's CapEx approaches $50 billion this year.

But a detail mentioned in the earnings call indicated that many projects are actually collaborative models, where clients lock in orders or even invest in advance.

This alleviated a lot of investors' worries in the market about capital expenditures consuming cash flow. "Client funding" essentially means that part of the infrastructure is "built with client money."

If this model can be sustained, the cash pressure will actually be much smaller.

5️⃣ Will SaaS be replaced by AI?

Recently, there has been a sentiment in the market that #AI will render many traditional SaaS software solutions valueless, leading to a halving in the stock prices of many representative SaaS companies, such as Salesforce (#CRM) and Adobe (#ADBE).

Although Oracle has also not been exempt from this SaaS massacre, its logic is quite different, or it feels like it has been misjudged.

Core systems familiar to us in enterprises, such as finance, ERP, and banking settlements, have very high migration costs.

So what is more likely to happen is the overlay of AI Agents on these systems rather than a complete replacement.

As long as the data is still within Oracle's systems, #AI will find it hard to bypass them, and Oracle's moat essentially lies in the data itself.

🧐 The final point is something I will continue to observe. In the earnings call, management provided a relatively aggressive target of $90 billion in revenue for FY2027.

Given the current order scale, although it is quite challenging, there is still a certain possibility of achieving this.

So I will focus on two things next: first, whether GPU supply remains stable; second, whether the company will initiate equity financing (ATM).

If there are future financing expansions, the stock price may see fluctuations in the short term, but it also indicates relatively high market demand, increasing the likelihood of meeting annual revenue goals.

Overall, this financial report has caused me to reevaluate Oracle. It is no longer just a traditional software company but has found its place in this cycle of AI infrastructure.

The post-market response of +10% 📈 basically reflects a repricing of the logic behind #AI mega infrastructure. If orders gradually turn into revenue, its future potential is undoubtedly immense, considering it has dropped from a peak of $344 to just $149 now, with a market cap of only $429.2 billion. Compared to other trillion-dollar AI giants, there is undoubtedly greater room for growth.

The companies mentioned above are all tradable on #MSX. When trading US stocks, I choose to use the #RWA tokenized platform #MSX to participate in the US stock market: http://msx.com/?code=Vu2v44

Early fans and partners of US stock investments can message me to fill out a form to gain free entry into the US stock discussion and exploration community (currently limited to 10 people per week, approval by assistant may take some time, thank you 🙏)!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。