Original title: $HYPE Man

Original author: Arthur Hayes, BitMEX co-founder

Original translation: Saoirse, Foresight News

We walked into the frozen forest and climbed the steep volcano. It was just another day of skiing and hiking meditation. Surrounded by the silent snowy woods, my thoughts ran free. When you are fully focused, slowly climbing the volcano step by step, placing one ski in front of the other thousands of times, the creativity that can burst forth is astonishing. I cherish this tranquility for three months.

Both my body and mind crave rest and recovery, which during ski season means going to a real ski resort. On the day at the resort, I removed the grip tape, hopped on the mechanical lift, and in just a few minutes, it transported me hundreds of meters high. The chairlifts and cable cars are great, but sometimes I have to share this tranquility with others.

I’m not much for talking in the lift, sitting quietly in the corner, but there are always some lively people in the resort who enjoy chatting with strangers to pass the time.

The questions are harmless but allow the other person to peg me in their mind. We always end up discussing professions—here I am, a person who skis every day, and I'm neither a guide nor a coach, which seems a bit strange. I politely respond, saying only, "I work with computers." The advantage of the tech industry is that everyone assumes you've made some money, but they can’t delve too deeply since they barely understand electricity, let alone the strange things that can be done with a "computer." The topic naturally dies there, and thank goodness, it’s finally time to get off and ski.

What do I or the Maelstrom team actually do?

We are traffic operators, making money by monetizing attention. Our main monetization method is going long on Bitcoin and various altcoins, rarely going short. By attracting market attention to our views, we believe that in the long run, the market will validate our judgments.

Now, please focus on Hyperliquid (HYPE).

I don't like going short because without leverage, your maximum profit is only 100%, while your maximum loss is unlimited. I always aim for positive convexity rather than going short, so I am perpetually a net long in the market.

At this difficult stage, Bitcoin has decisively broken through previous highs; are there any truly high-quality altcoins that can achieve absolute appreciation?

The answer is: yes. Because during every consolidation or bear market in cryptocurrency, the best-performing altcoins are always exchange tokens. Even if their prices drop, exchanges can continue to earn trading fees, sometimes making more than during bull runs, especially when they benefit from the long-term growth in trading volume of decentralized exchanges (DEX).

During the horizontal market to decline period at the beginning of 2023, the most sought-after exchange token was GMX. In April 2023, GMX reached an all-time high of $90. Why? Because at that time, it was far ahead in perpetual contract DEX trading volume, open interest and trading volume skyrocketed, driving protocol revenue up significantly, and more importantly, the vast majority of revenue was distributed to GMX holders.

When the consensus on fiat credit expansion shifts from growth to contraction, which exchange token can still soar?

Data sourced from DefiLlama on March 7, 2026

Hyperliquid is currently the leading perpetual contract DEX and is the highest-earning project besides stablecoins. 97% of its revenue is used to repurchase HYPE from the market. In the entire crypto industry, no project can return such a high proportion of money to token holders like Hyperliquid.

Unfortunately, if you hold stablecoins like USDT or USDC, you will not benefit from their net interest income. Therefore, if the market believes in HYPE, absolute appreciation is possible. My target price for HYPE in August 2026 is $150, which is about five times the price of around $30 when I wrote this article.

To move from "hell" to "Valhalla," Hyperliquid needs to restore its 30-day revenue to an annualized level of $1.4 billion—this level was reached last August. To make the following text easier to understand, I will place the financial model at the forefront.

The key assumptions I need to verify are: Price-to-Earnings ratio (P/E), and the amount of HYPE tokens that the team unlocks monthly. P/E formula:

P/E = (Circulating supply × Price) ÷ (30-day annualized revenue × Repurchase ratio)

My model predicts that total revenues from HIP-3 and non-HIP-3 will grow from $843 million in March to $1.4 billion in August.

I will explain how Hyperliquid can reclaim its historical highest 30-day annualized revenue level against the backdrop of increasing competition in perpetual contract DEX.

The last part estimates how many HYPE tokens the team will receive monthly based on the data from the past three months.

Stress-testing the model under different scenarios can effectively enhance the credibility of the assumptions. I will examine some assumptions from a pessimistic perspective to see how "overzealous" one must be to believe in the $150 target price I provided.

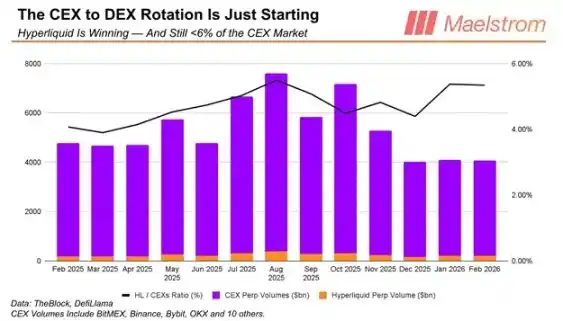

CEX vs DEX

The best thing about Hyperliquid is that its trading volume growth does not require the total trading volume of global crypto perpetual contracts to rise. As long as a few percent of the trading volume from centralized exchanges' perpetual contracts is transferred to Hyperliquid, it could easily double its 30-day annualized revenue in a few months. With just a 3.97% increase in market share, Hyperliquid can achieve its annual revenue target of $1.4 billion. Given that Hyperliquid didn't exist less than three years ago, this is entirely feasible.

Hyperliquid can grab trading volume well from CEX, but which crypto derivatives can attract users? Everyone comes for stock perpetual contracts and binary options, staying for Bitcoin, Ethereum, and Solana trading.

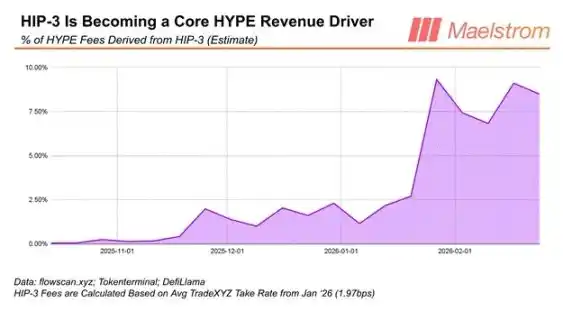

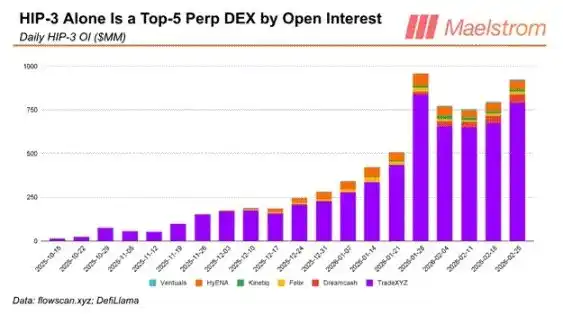

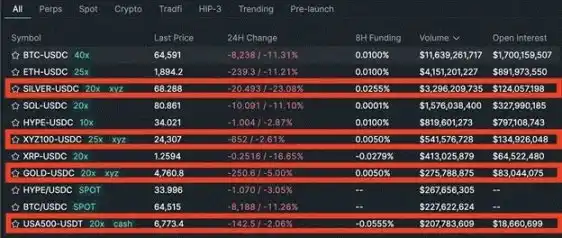

HIP-3 allows anyone to launch perpetual contracts without permission. By staking 500,000 HYPE, you can create any trading market you want using Hyperliquid's matching and margin engine. TradeXYZ does just that, and its flagship products are perpetual contracts for silver, gold, Nasdaq 100, and S&P 500.

By the way, the silver and gold markets launched less than three months ago, and daily trading volume has already reached billions. As the filthy fiat financial system arbitrarily modifies rules and suppresses people's desire to escape centralized currency, this place will become the new price discovery venue.

Screenshot taken on February 5, 2026, 11:20:00 UTC

In just four months, HIP-3's trading volume contributed nearly 10% to Hyperliquid's total revenue. Allowing permissionless token launches has always been the holy grail of DEX, and the rapid increase in trading volume proves this is the key for Hyperliquid to pull ahead of competitors.

For Hyperliquid to increase its revenue from March to August by 66%, HIP-3 must take the lead. Especially with the overall cryptocurrency market cap remaining at its current depressed level. Hyperliquid must offer traders fresh and exciting on-chain trading assets. Precious metals, AI-focused stocks, and crude oil are exactly what ordinary players want to trade. Now, through perpetual contracts, anyone globally can trade 24/7, with higher leverage than traditional financial trading platforms.

Based on these reasons, my model predicts that HIP-3's revenue will increase by 160% in six months.

Adding to the excitement is the prediction market. Hyperliquid recently announced that HIP-4 will support permissionless launch of prediction markets. I expect HIP-4 to launch within the next three months. Players will flock to Hyperliquid's prediction market to trade binary options and day-of-expiration options (0DTE). It's hard to predict revenue growth before the launch, so I haven’t included it in the model. If the Hyperliquid team delivers high-quality code as before, it will almost instantly boost revenue, which would be an added bonus.

Unfortunately, Hyperliquid is not the only perpetual contract DEX. The competition is fierce because this is the next major battlefield for trading. At the end of last year, the emergence of many low-fee and zero-fee DEXs depressed Hyperliquid's expected valuation.

So what has happened since then that makes me believe Hyperliquid's dominance is hard to shake?

Is it true?

For crypto CEX or DEX, faking trading volume is as easy as pie.

Back in the days of BitMEX, we often joked about having a “volume booster”—a trading platform launches a program that automatically generates fake trades to increase activity.

Nowadays, many leading trading platforms regularly use volume boosters to claim they are the "largest," misleading traders into thinking there is real liquidity here. For DEX, creating wallets to fake volume is even simpler; this is the main source of the fake volume.

Liquidity mining is also a common method to increase activity: DEX give points or platform tokens based on trading volume, and traders fake trades between wallets.

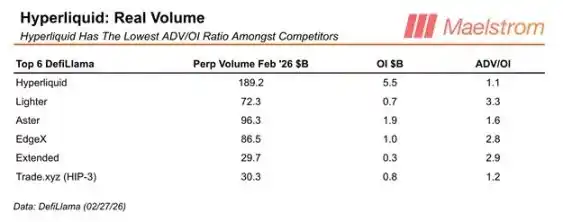

Faking volume and liquidity mining will not deepen real liquidity. We cannot accurately gauge the proportion of these activities in trading volume. The only objective metric to measure the quality of a trading platform is the ADV/OI ratio (average daily volume / open interest).

As traders must inject real funds as margin for opening positions, open interest (OI) reflects the extent of real user usage of the platform. Average daily volume (ADV) can easily be inflated by faking volume and mining, but when adjusted by OI, we can obtain organic trading volume driven by genuinely risk-preferring traders. Therefore: the lower the ADV/OI ratio, the better.

Among the top 5 perpetual contract DEX, Hyperliquid’s trading volume is the most genuine, as it has the lowest ADV/OI ratio. When traders realize that the liquidity on competing platforms is largely fake, or that points/token mining has ended, they will return to Hyperliquid.

In the long run, the proportion of Hyperliquid's true trading volume will continue to increase. This will solidify the narrative that HYPE is "not afraid of competition."

Many people remember that I previously had a tactical short-term bearish outlook on HYPE, and one important reason was the competition from low-fee DEXs. Now I believe Hyperliquid is the industry leader in "real trading volume," and at least for the next six months, I am no longer worried about competition issues.

Regarding competition, the next consideration is: which DEX truly has the best liquidity after accounting for slippage?

I took snapshots of the order books for Bitcoin/USD perpetual contracts from five platforms and calculated the slippage for nominal amounts of $100,000, $1 million, and $10 million market buy and sell orders.

You can see that for large transactions on Hyperliquid, most of the time the costs are the lowest. Therefore, even if competitors have explicitly lower fees by 1–2 basis points, true large traders will still flock to Hyperliquid because they can trade at a larger scale with minimal market impact.

I got rich

Hyperliquid has only a team of 11 people who have created the best DEX product ever. Wealth should flow to them through the locked HYPE tokens.

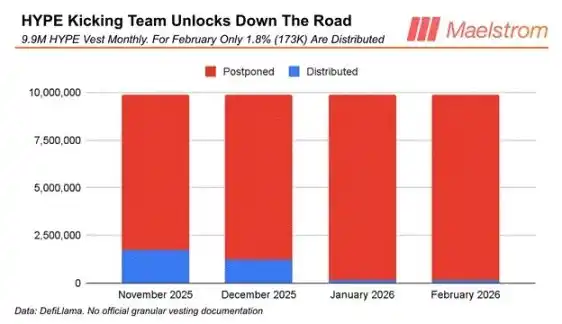

When Maelstrom was bearish on HYPE at the end of last year, there was a concern: how many tokens would the team actually sell to the market monthly, which had uncertainties. Since Hyperliquid has not accepted venture capital investments, whether the team voluntarily refrains from selling newly unlocked tokens essentially comes down to a political decision by Jeff and the team internally. They have already limited token sales.

After distributing nearly 20% of the reward tokens in November and December of last year, the team distributed only about 1% of the reward tokens in January and February. I speculate that the initial high distribution was to cover taxes and improve living conditions; after this demand was met, the team significantly reduced the releases to help HYPE rebound. This is just my speculation.

History does not repeat itself exactly, but it rhymes. Based on this, I assume the monthly release amount is the average of these four months: 815,750 tokens.

Looking ahead

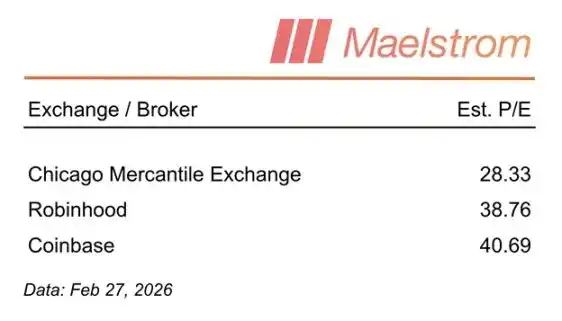

The market is forward-looking. How much are players willing to pay for Hyperliquid's future earnings? Currently, HYPE's P/E ratio is about 12 times. How does this compare to traditional financial trading platforms?

To determine a reasonable valuation level, I referenced the current P/E ratios of the world’s top trading platforms, the Chicago Mercantile Exchange (CME), the newer brokerage firm Robinhood targeting young aggressive investors, and the crypto trading platform Coinbase, which is heavily influenced by US regulations. The P/E ratios of these institutions vary widely, roughly between 26 to 40 times. In contrast, $HYPE is only at a P/E ratio of 12 times, clearly undervalued.

One reason for the low valuation is that Hyperliquid is not a publicly traded company and carries smart contract and counterparty risks, leading to a naturally lower valuation multiple. Furthermore, most mainstream centralized spot trading platforms do not support $HYPE trading, making it difficult for ordinary investors to purchase it, which prevents it from being hyped to extremely high valuations like many altcoins. Even so, a P/E ratio of 12 times is still absurdly low.

Within just a few months, Hyperliquid's HIP-3 index and precious metals trading market have become critical price discovery venues when traditional financial trading platforms like CME are closed on weekends. I don't know about you, but computers still need to go play golf on weekends.

At least from an industry trend perspective, HYPE deserves a higher valuation premium.

Regarding market capitalization and fully diluted valuation (FDV):

I use market capitalization rather than FDV, as the two differ due to circulating supply. Market capitalization only counts the currently circulating tokens, unlike FDV which represents all future tokens. Given this is a six-month cycle trade, using current market capitalization makes sense. Admittedly, Hyperliquid may initiate another airdrop in the future, thus expanding the circulating supply. Yet so far, the team has not hinted at an impending airdrop, so I will not consider this risk and the resulting impact on circulating supply for now.

Stress Test

If the team unlocks 9.91 million HYPE monthly, and the market only gives a forward P/E ratio of 12 times, but Hyperliquid's 30-day annualized revenue still rebounds to the historical high of $1.4 billion, what would happen?

The target price would drop to $58, still about 75% higher than the current $30. This result is not bad.

I did not make a pessimistic assumption about revenue, for the simple reason: if Hyperliquid's revenue cannot grow from its current level, the tokens will not appreciate. If you think that way, then under any circumstances, don’t buy HYPE.

HYPE Expert

Source: CoinGecko

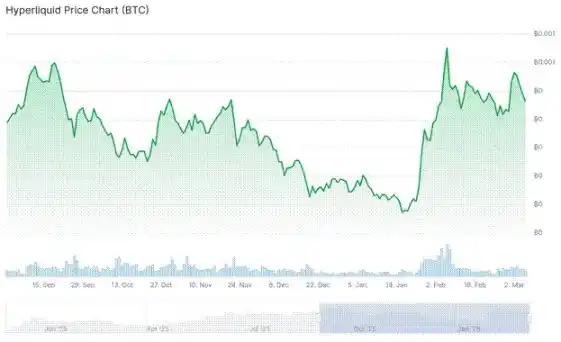

I created a chart using HYPE/BTC to illustrate that the market has recognized the value of this token.

We all painfully know that unless you short, Bitcoin fell from last September's HYPE to a local low of about $20. I think the catalyst for HYPE's resurgence is the dramatic drop in the amount of tokens released by the team from 9.91 million in January to just 140,000.

Furthermore, the incentives from the competitor DEX's points and tokens have gradually expired, rapidly reducing their attractiveness to traders. The remaining trading volume may be fake, but as I previously demonstrated regarding order book liquidity, Hyperliquid stands as the place with the lowest trading costs.

Our Maelstrom team started to test the waters with small positions above $20. On the way up the mountain skiing, I kept thinking: if the macroeconomy remains sluggish in the short term, what should I position in? What kind of projects count as genuinely high quality—those with real users, real revenue, and can return profits to token holders?

From these dimensions, Hyperliquid is the highest quality project in the entire crypto industry. After researching deeply and writing this article, my confidence is further strengthened.

As the macro investment giant Druckenmiller said: "Invest first, research later."

Thus, HYPE quickly became our largest liquidity altcoin position. We plan to continue selling all other inferior assets, continuously increasing our position in HYPE within the current price range.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。