I have also read Brother Wu's analysis and completely agree with his perspective. Currently, BlackRock and Blackstone do not have core issues, and redemptions are still manageable, all within normal redemption ranges. However, users have begun to show higher redemption requests.

At present, neither BlackRock nor Blackstone has encountered significant core credit issues. Redemptions themselves are not completely out of control, but are being handled within the framework allowed by product rules. This time, BlackRock's HLEND had redemption requests amounting to about 9.3% of net asset value in the first quarter, exceeding the original quarterly cap of 5%. Blackstone's BCRED received redemption requests of about 7.9% of fund shares, and Blackstone is responding by increasing repurchase limits and internal funding. In other words, the current issue is not a collapse or bank run, but rather that more investors are clearly wanting to exit.

So what I really want to discuss is not whether BlackRock and Blackstone are currently facing major problems, but why the number of people applying to exit has suddenly reached record levels, even before any core credit events have occurred. This fact itself is part of the risk.

For private credit products, investors' concerns often stem from net asset value, interest income, and default rates as reflected in the data. The default rate for U.S. private credit borrowers is expected to reach a record high of 9.2% by 2025, and market worries about the quality of underlying borrowers have been on the rise. The stock prices of listed BDCs have also clearly fallen, with the median now at about 73% of book value.

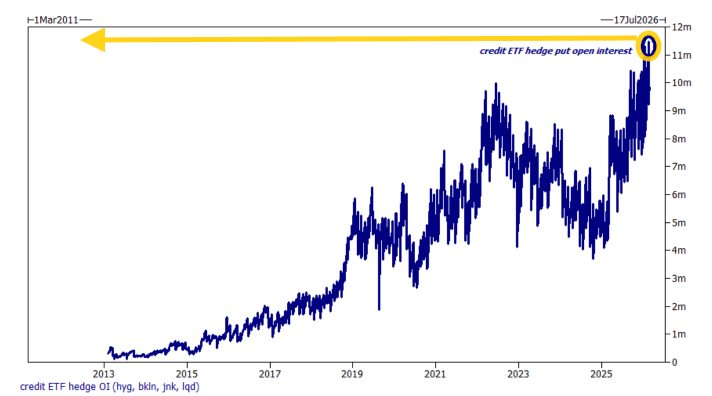

This is also why institutions are shorting credit ETFs now. Even Fitch indicates that the average redemption rate for permanent non-listed BDCs has risen from 1.6% to 4.5% in the fourth quarter of 2025.

America has experienced several credit crises, and for institutions, credit risk can either mean things are good for everyone or it can drag down a whole bunch of people. The current shorting of credit does not necessarily imply a belief that a collapse will definitely happen, but rather a preventive measure against potential dangers, and these dangers do indeed amplify with high interest rates.

Therefore, I personally do not think this is alarmist. Of course, it is also possible that my abilities are insufficient, and in the end, nothing may happen, or the Federal Reserve might cut interest rates faster, reopening refinancing windows and pushing these pressures back down. However, considering that credit ETFs have already reached historic highs, what I prefer to do is clarify the potential issues instead of proclaiming that everything is calm and peaceful now.

After all, institutions are shorting (hedging) with real money, not just talking about it.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。