The real danger of private credit is not just that investors are starting to demand redemptions, but that many funds may not have fully reflected the true pressure in the net value, interest income, and default rates that they show on their books.

In plain terms, some borrowers are indeed facing issues, but these problems are just being postponed.

For example, some interest payments are not being paid upfront but are instead being recorded on the books; some are extending the maturity dates; some are adjusting financial metrics to make reports appear less concerning; and some are relying on behind-the-scenes sponsors to temporarily hold off the outbreak of issues.

So on the surface, many funds appear stable, with net value not declining significantly, interest still being collected, and default rates not spiking immediately. But this does not mean the risks have disappeared; it is more likely that the risks have not yet fully manifested.

Once high interest rates continue to persist and refinancing becomes increasingly difficult, the previously underlying issues will start to surface gradually. It may not be an immediate collapse, but rather a very slow process, such as:

1. Net value begins to gradually decline

2. Dividends start to decrease

3. Fundraising becomes increasingly difficult

4. Secondary transfer prices become lower

5. Finally, when it truly comes to liquidation or restructuring, it will be discovered that the recoverable funds are much less than originally anticipated

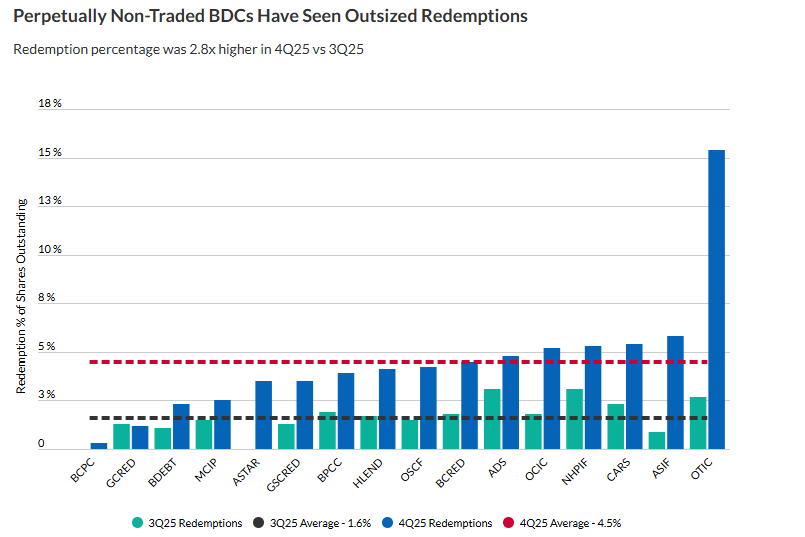

The chart below actually serves as a very intuitive signal. From the chart, it can be seen that the average redemption rate of permanent non-listed BDCs has risen from 1.6% in the third quarter to 4.5% in the fourth quarter of 2025, which is an increase of 2.8 times in just one quarter.

The key issue is not that a particular fund is especially high, but that the redemption pressure across the entire sector is rising concurrently. This indicates that the withdrawal of funds is no longer an issue specific to individual products; rather, the entire retail private credit channel is beginning to confront this reality.

In other words, the most concerning aspect of private credit right now is not just the risks that haven't yet exploded on the books.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。