In July of last year, we detailed the operational strategy of Meteora, and the highly consensual community concept indeed provided much assistance for managing our own project. (Related reading: How to build a strong LP Army like Meteora?)

Now, at the transition between bull and bear markets, Meteora still manages to maintain relatively stable liquidity and revenue compared to other products in the same track.

Reflecting on Meteora's product iteration thinking may give us a more intuitive understanding of the traits a product needs to possess in order to traverse bull and bear markets.

1. Capital Efficiency Revolution: The Structural Issues Meteora Attempts to Solve

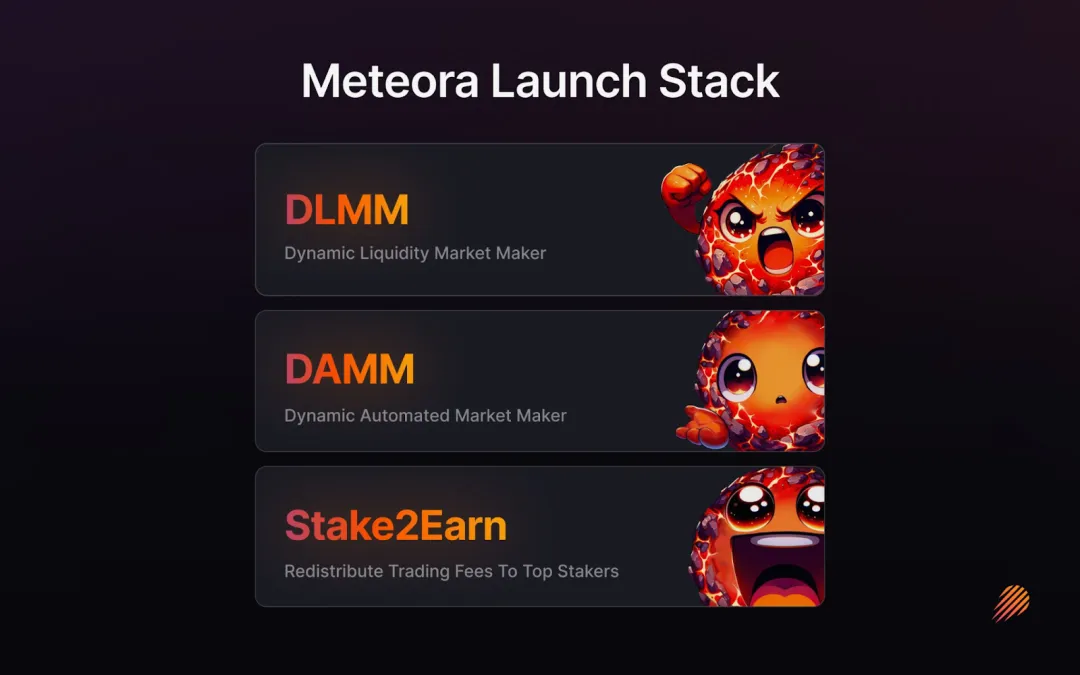

The core of Meteora lies in optimizing liquidity and capital efficiency. Traditional AMMs face issues such as liquidity dispersion, high slippage, and limited returns, which Meteora resolves through DLMM (Dynamic Market Maker) and dynamic AMM mechanisms.

For example, DLMM divides liquidity into multiple "intervals" (bins) based on price and can adjust transaction fees in real-time: when market volatility increases, fees rise, offsetting LP losses in a volatile market. This dynamic fee and precise liquidity concentration design enables trades within the same interval to have almost zero slippage, significantly enhancing trading efficiency and LP returns.

Meteora's Dynamic AMM product also automatically allocates some assets in the background to lending protocols, generating additional returns and avoiding sustainability issues that arise solely from mining incentives. In summary, Meteora has greatly improved capital efficiency and potential LP returns through technological upgrades and incentive mechanisms (such as fee sharing, MET points, etc.).

2. DLMM: How the Dynamic Liquidity Model Reshapes the Market-Making Logic on Solana

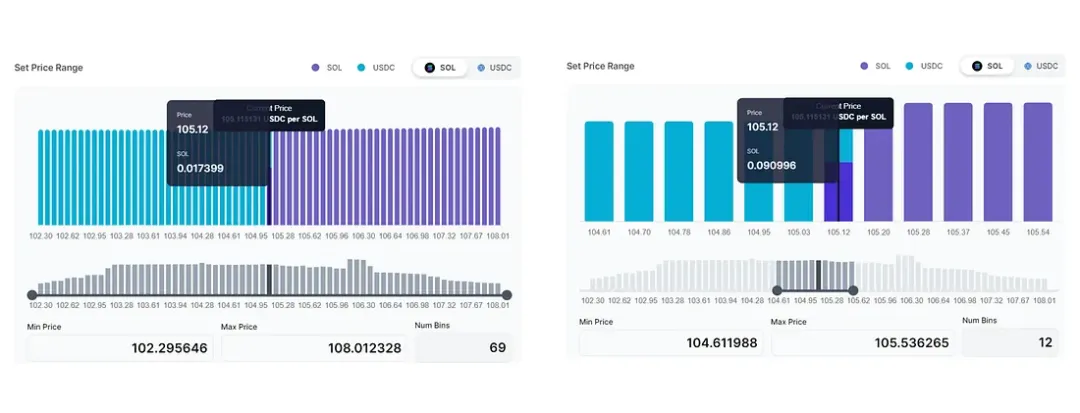

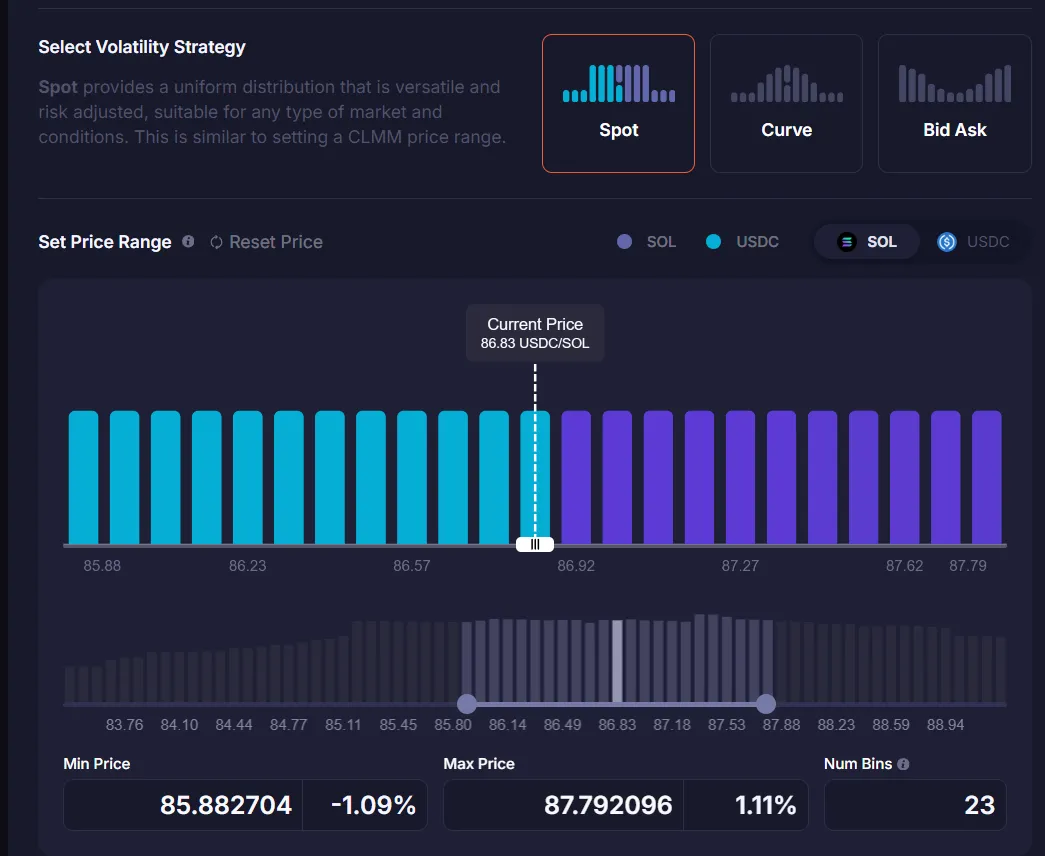

DLMM is Meteora's core innovative product and can be seen as a "segmented centralized" liquidity pool. Unlike traditional constant product pools, DLMM allocates liquidity for a trading pair across multiple price intervals and allows LPs to choose different volatility distributions according to their strategies.

When trading within each interval, liquidity is precisely concentrated, resulting in almost zero slippage, allowing LPs to maintain higher capital utilization under high transaction volumes. Additionally, DLMM dynamically adjusts transaction fees based on market volatility: increasing fees during periods of high volatility to offset impermanent loss faced by LPs and lowering fees during stable periods. LPs in DLMM earn not only the basic trading fees for providing liquidity but also volatility fees and liquidity mining rewards.

DLMM has also derived a Launch Pool model, designed specifically for new token launches, allowing tokens to quickly gather liquidity and be traded in aggregators like Jupiter. In short, DLMM creates more income opportunities for LPs through high capital efficiency, flexible volatility strategies, and dynamic fee mechanisms.

DLMM organizes liquidity by price interval (Bins), maintaining sufficient funds in each interval to achieve "0 slippage" trading within the interval.

The core algorithm includes a base fee rate and maximum fee rate mechanism, automatically increasing prices when market volatility rises and lowering prices during stable periods to attract more trades. Slippage control is achieved through discrete interval filling: trading only occurs at the price within that interval, avoiding the impact of deep dispersion.

Meteora has also designed various strategies for different market conditions, such as the "Curve Strategy" concentrating liquidity near the current price and the "Buy-Sell Interval Strategy" to hedge extreme volatility, etc.

For stable trading pairs like USDC/USDT, most trades are concentrated in a narrow interval, causing a large amount of traditional AMM funds to be idle. Under the DLMM design, LPs can concentrate more liquidity in this narrow interval, thus earning more transaction fees and significantly improving capital efficiency.

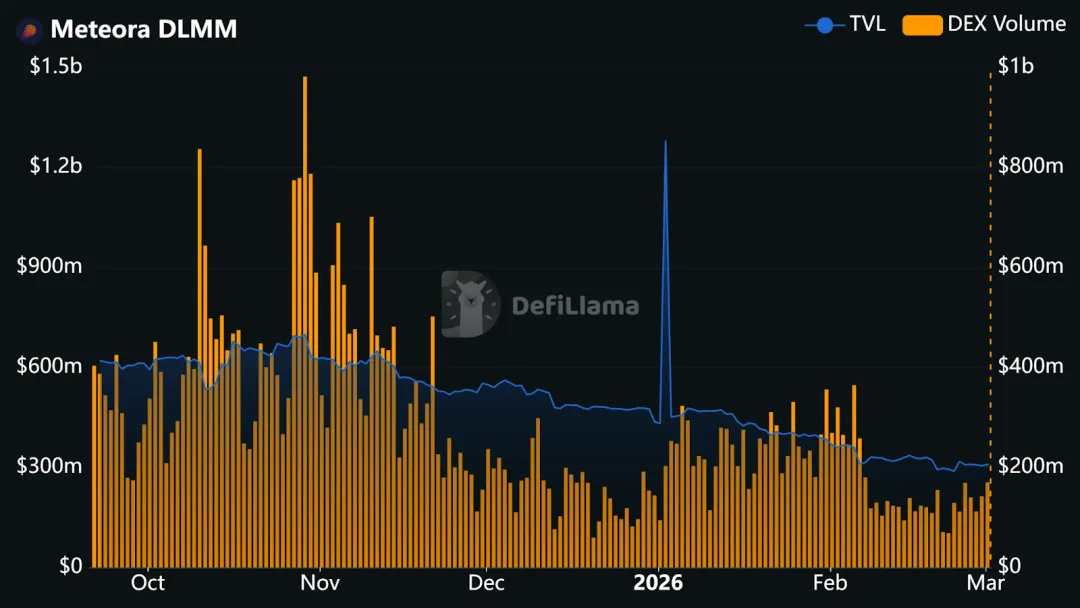

More importantly, DLMM is not just about price interval distribution; it can automatically adjust fees based on actual trading activity and volatility. This "on-demand charging" mechanism cannot be realized in traditional fixed-rate AMMs. Because fees are tied to volatility, LPs can obtain higher fee compensation during high volatility periods, fundamentally alleviating the risk of impermanent loss and increasing profitability potential. On a data level, as DLMM gets integrated for use in aggregators like Jupiter, the participation volume in DLMM pools on Meteora continues to increase.

By early 2026, the total locked value of DLMM reached approximately $300 million, bringing billions of dollars in trading volume over the past 30 days, occupying a significant position in the Solana DEX ecological landscape.

3. From DAMM v1 to v2: Two Key Leapfrogs in the Meteora AMM Mechanism

Meteora's Dynamic AMM (DAMM) series of products are similar to traditional constant product pools but integrate more flexible features.

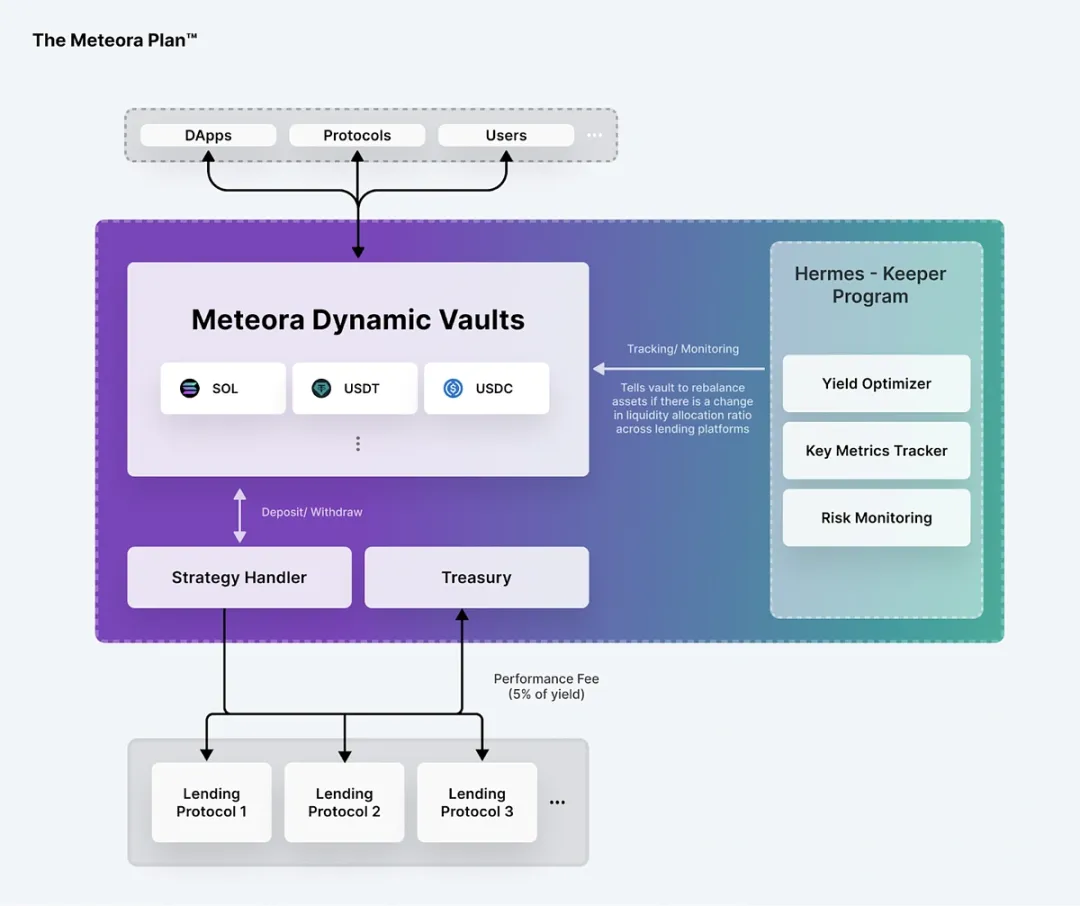

DAMM v1 is the first AMM launched by Meteora, enabling LPs to earn transaction fees and additionally gain lending income. In DAMM v1, the assets deposited by users are automatically allocated to the background dynamic vaults and designated for lending protocols, earning additional interest and rewards.

This mechanism reduces the reliance on a single mining incentive, allowing LPs to simultaneously collect trading fees, lending interest, and mining rewards. LPs can also choose to permanently lock liquidity to enhance community confidence; locked assets can still generate sustainable returns, especially suitable for dynamic fee allocation in memecoin pools.

DAMM v2 is a new generation of AMM, compatible with Solana Token2022 tokens, and offers richer features. Its characteristics include: optional fixed rate or dynamic rate mechanism, on-chain setting of higher dynamic fee caps, built-in anti-sniping mechanism, and the ability to partially concentrate liquidity (Position NFT).

DAMM v2 also supports the creation of single asset liquidity pools (similar to DLMM's one-sided pools) and integrates the mining mechanism into the contract to improve efficiency.

Compared to DLMM, the creation cost of DAMM v2 is lower (creating a single pool costs about 0.022 SOL, while DLMM costs about 0.25 SOL) and provides flexible fee collection and lock-up options. These designs make it easier for project parties to conduct token sales and bring more autonomy and income tools to LPs.

4. Evolving Protocol: Strategic Intent Behind Functional Iteration

Since 2024, Meteora has continuously iterated new features to enhance user experience and protocol activity.

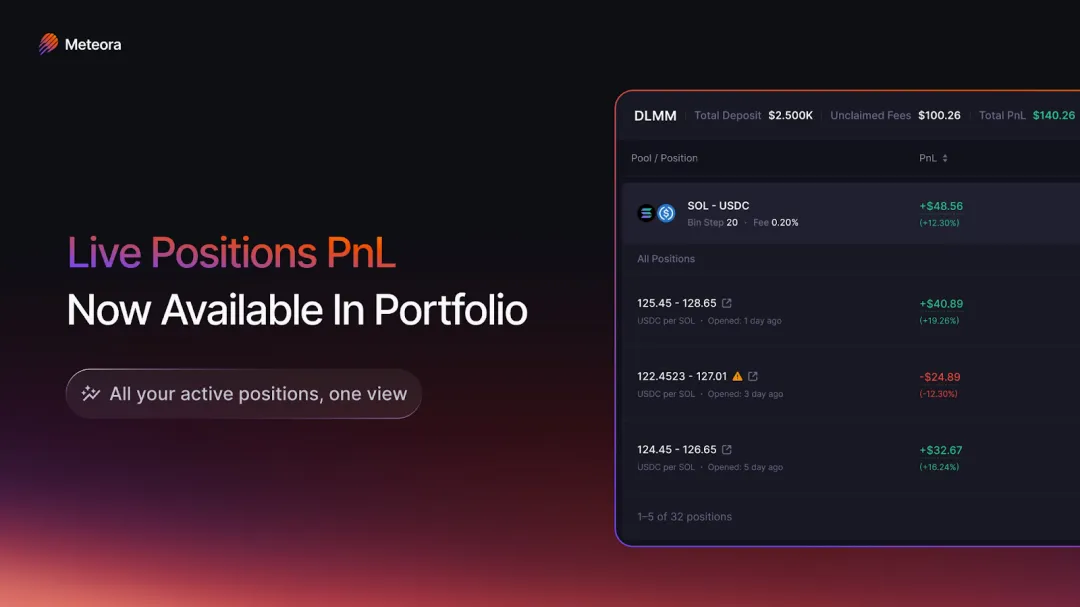

For example, the one-click Rebalance and one-click Ape In functions allow LPs to quickly adjust or invest during market fluctuations or new token launches; the PnL analysis dashboard can track earnings in real-time; the Pool Discovery page helps users quickly filter high-yield liquidity pools; the position merger function allows users to consolidate multiple positions in the same pool, reducing management costs; automatic reinvestment automatically puts earned rewards back into liquidity; the LP points leaderboard quantifies liquidity provision and contribution behaviors into points, incentivizing long-term participation.

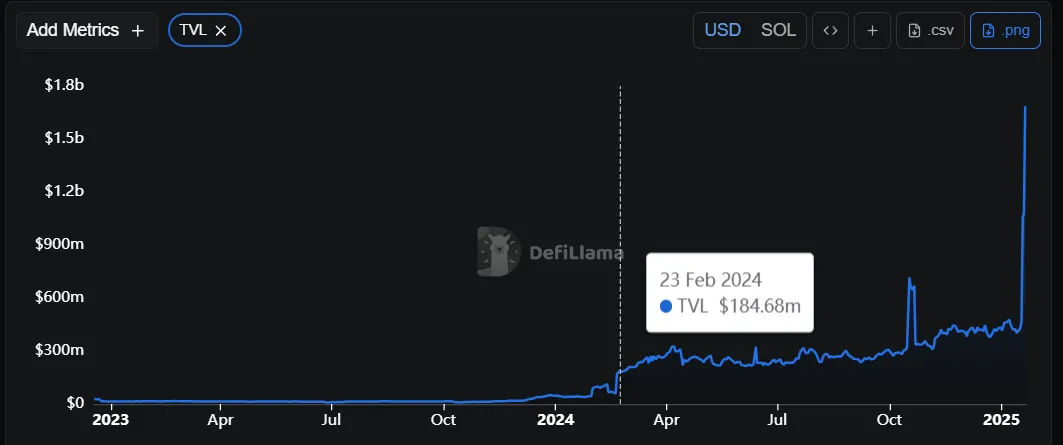

After each feature launch, community feedback has been positive, with a significant increase in the number of users and TVL. According to official data, the point incentive system launched in early 2024 directly propelled TVL from ~$40 million to ~$160 million. Following the features' rollout, community discussions have been enthusiastic, and the new features' usage rates have steadily climbed, further solidifying Meteora’s leading position within Solana protocols.

5. LP Army: How Meteora Turns Liquidity Providers into “Fighting Units”

Meteora's community operation centers on education-driven initiatives, cultivating loyal LPs through the "LP Army" system.

At its core are the regularly held LP Army Bootcamps: two-day free training camps where attendees learn the basics of LP and conduct practical exercises. Participants must provide ≥$100 liquidity for designated non-stablecoin trading pairs on the first day and hold it for ≥1 hour. On the second day, they can obtain an NFT diploma and the "LP Army Private" identity after passing the profit and operations examination.

After completing training and being confirmed as official members, LPs not only receive protocol airdrop points and community status but also unlock advanced courses, exclusive Discord channels, and a series of strategic analysis tools (like profit trackers and Dune dashboards).

Community co-building tools are abundant: Metlex provides professional dashboards for DLMM LPs, analyzing position performance in real-time; Ultra LP acts as an LP "partner," aggregating all earnings and PnL; DLMM Profiler from GeekLad assists LPs in optimizing strategies; MetEngine enables one-click positioning and copying of top strategies via Telegram and other channels.

Additionally, the community promotes a one-on-one mentorship program led by experienced LPs for newcomers, covering liquidity strategies, impermanent loss management, and more. In terms of governance, user behavior is closely tied to incentives: Meteora has established a MET points system, where LPs can earn points by providing liquidity and inviting friends, which can be redeemed for future MET token airdrops or community privileges. For instance, after the system's launch, TVL surged from $40 million to $160 million, demonstrating significant incentive effects.

Ultimately, this "points + tokens + honors" multi-layer incentive ensures rewards are distributed to long-term contributors rather than short-term "scalpers." The upcoming MET token release will further link with the points system, providing early community members with more governance and economic incentives.

6. Survival Model in Bear Market Cycles: Analyzing Meteora's Resilience Mechanism

Since 2023, the overall crypto market has entered a deep bear market cycle, and DeFi protocols generally face structural pressures such as TVL contraction, declining trading activity, and user loss.

However, Meteora's on-chain performance has displayed a relatively robust recovery curve. This "resilience" is not a result of occasional market windfalls but rather the outcome of multiple strategies working together in incentive design, product architecture, risk control, and community organization.

In terms of the incentive mechanism, Meteora not only attracts users to participate long-term through traditional lock-up rewards and fee sharing but also creatively implemented the Stake2Earn model. This mechanism was designed to transform the memecoin ecosystem, which could lead to rapid sell-offs, into a yield system based on "staking competition."

In traditional token economics, memecoin projects often generate strong selling pressure during the early launch phase since holders tend to sell quickly after short-term arbitrage, a behavior that intensifies, especially in the late bull market or during a bear market. The construction logic of Stake2Earn directly counteracts this, allowing token holders to stake MEME tokens into designated Stake2Earn contracts and participate in fee-sharing, focusing not on short-term speculation but encouraging holders to lock tokens in the protocol long-term to earn transaction fees generated from the liquidity pool trades.

Participation in Stake2Earn does not rely on holding LP; it only requires users to stake native memecoins. This design has two significant meanings: first, users do not have to bear the impermanent loss risk unique to LPs since they are staking a single token instead of LP tokens; second, stakers have the opportunity to directly participate in fee revenues from the protocol, directly linking personal interests with protocol growth, thus encouraging users to become long-term supporters rather than short-term arbitrageurs.

Specifically, the Stake2Earn mechanism will rank users based on the amount staked, with only those stakers ranking among the top (e.g., Top 5 to Top 100, specific range configurable) enjoying fee-sharing benefits. The higher the rank and the larger the stake, the more fee-sharing users earn from liquidity pool transactions. The system updates rankings in real-time and dynamically allocates income based on current rankings. This "real-time earnings growth" design not only incentivizes users to continuously increase their staked amounts but also encourages participants to compete to maintain their eligibility for earning.

The reward structure of Stake2Earn is also very unique, adopting a dual reward system: once users meet ranking conditions, they can receive fee earnings in the form of pegged tokens (such as SOL, USDC, etc.), while memecoin stakers also receive additional memecoin rewards that will automatically be added back into users' total staked amount, reinvesting the rewards. This reinvestment mechanism not only enhances long-term earnings but also alleviates the market pressure of memecoins being sold off, thereby enhancing overall market stability during bear phases.

Moreover, to prevent malicious rapid withdrawal actions, Stake2Earn has a cooldown period for unstaking. When a staker requests to withdraw, their memecoins enter a preset waiting time (e.g., at least 6 hours) during which these tokens will not participate in earnings calculations; if the staker changes their mind and withdraws the unstaking request, those tokens will immediately be counted back into income eligibility. This design ensures both fairness in rewards and liquidity stability, preventing short-term games from affecting system income allocation.

If the incentive system locks in user behavior, the continuous evolution of product architecture ensures efficiency and safety of funds. Between 2023 and 2024, the team launched key modules such as dynamic vaults and dynamic AMM to further strengthen the protocol's capital attractiveness in bear market environments. The Dynamic Vault system adopts a minute-based automatic rebalancing mechanism, which can allocate funds in real-time between multiple lending protocols, seeking optimal yield paths. When a lending platform is over-utilized or has abnormal risk indicators, the system automatically withdraws funds and reallocates assets, thus protecting LPs' capital. This structure is not just simple yield aggregation but introduces risk parameter judgments and fund dispersion logic to build a dynamic risk buffer layer. Relevant mechanisms have been audited by institutions such as Quantstamp and Halborn, and have withstood market fluctuations, enhancing user trust.

Dynamic AMM automatically connects funds provided by LPs into the dynamic vault system, allowing liquidity to not only earn transaction fees but also accumulate lending interest and liquidity mining rewards, forming a structure of multiple overlapping yields. Capital no longer stays statically in the pools but maximizes returns under the premise of controllable risks. Meanwhile, Meteora continues and optimizes its predecessor Mercurial's multi-asset stable pool technology, allowing non-homogeneous assets to be efficiently aggregated in the same pool, such as Allbridge or Wormhole bridging assets mixed with SOL/USDC liquidity structures. This design improves the liquidity efficiency of cross-chain stable assets and maintains a high fund turnover rate in an overall declining trading volume market environment.

At the on-chain data level, it can be observed that this dual structure of products and incentives has indeed produced tangible results. After the launch of the points system in early 2024, TVL surged from approximately $40 million to $160 million within a short period and subsequently entered the hundreds of millions range. During the same period, compared to the mainstream DEX Raydium on Solana, Meteora's TVL experienced a relatively smaller decline and a faster recovery. In terms of trading activity, its 30-day trading volume remained in the tens of billions range, indicating that liquidity has not significantly dwindled due to the bear market. The locking structure and automatic reinvestment mechanism have reduced the speed of capital outflow, while dynamic rates and capital efficiency optimizations have increased the motivation for capital retention.

Overall, Meteora's survival and growth in the bear market do not rely on a single "traffic dividend" or short-term subsidies but instead construct a sustainable flywheel model through product mechanism innovation, incentive structure reconstruction, real earnings-driven approaches, and community collaborative governance. For other projects in the bear market cycle, the greatest insight is this: rather than using high-emission tokens to exchange for temporary TVL, it's better to build cash flow capabilities around genuine trading demands; rather than amplifying market sentiment, it’s preferable to optimize the value-capturing paths within the protocol; and instead of being worried about user loss, it's wise to convert users from "liquidity mercenaries" to "members of a community of interest" through long-term locking, revenue sharing, and behavioral binding mechanisms.

The real test of a bear market is not the ability to finance, but whether products and mechanisms can self-generate. Meteora's practice demonstrates that only when protocol income, user returns, and token value form a closed-loop interaction, does a project possess the structural resilience to traverse cycles. This strategy, centered around prioritizing efficiency, genuine earnings, and sustainable incentives, provides a clear evolutionary direction for all DeFi projects in bear markets: reduce external blood transfusions, strengthen internal circulation, and win time with mechanisms instead of subsidies.

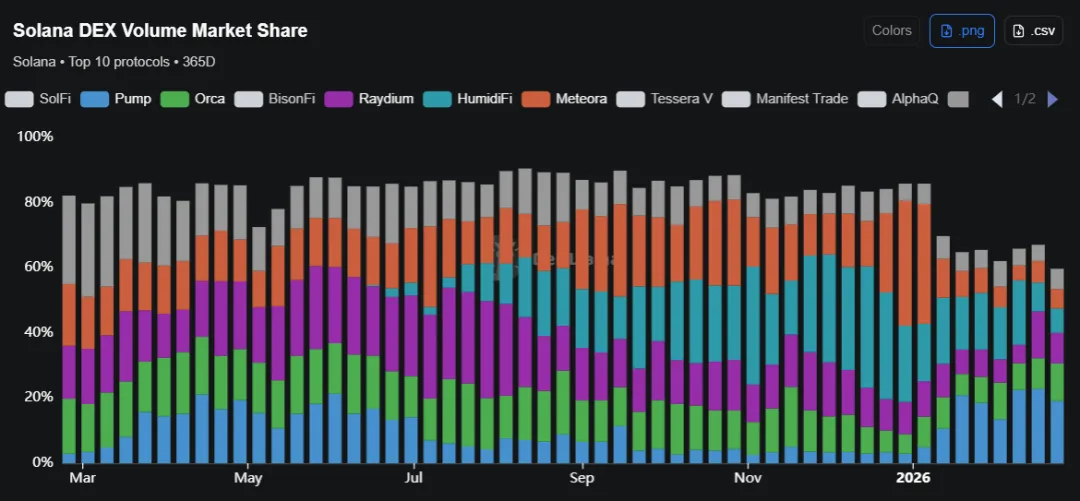

7. Liquidity Competition: Differing Approaches of DeFiTuna and HumidiFi

In the Solana ecosystem, the competition surrounding liquidity and order flow is heating up. Besides Meteora, DeFiTuna and HumidiFi are competing for market share through completely different paths. The former emphasizes product structure and functional innovation, trying to attract professional users with more complex on-chain trading tools; the latter adopts a "Prop AMM" model, establishing advantages in execution quality and trading efficiency through efficient internal capital turnover and deep routing integration.

DeFiTuna (TUNA) positions itself as an advanced centralized liquidity DEX on Solana, using a hybrid AMM architecture and integrating on-chain lending capabilities into the same protocol framework. Its mechanisms not only support dual-path liquidity from Orca AMM and native DeFiTuna AMM but also introduce on-chain limit order functions to allow users to execute more refined trading strategies without custody.

Additionally, DeFiTuna deeply integrates leveraged trading with its lending system, achieving manageable leverage within the same protocol, providing LPs and borrowers with an integrated capital efficiency solution. This structural innovation makes it appealing to professional traders and high-frequency strategy users. However, in terms of scale, its liquidity is still in a developmental stage. According to DefiLlama data, DeFiTuna's TVL is approximately $4.1 million, with about $115 million in trading volume over the past 30 days. Compared to top protocols, its market depth and brand recognition still have room for improvement, and the long-term retention effects of new features remain to be validated over time.

In contrast, HumidiFi (WET) takes a completely different route. As an exclusive market maker model (Prop AMM) on Solana, all of HumidiFi's liquidity is provided internally by professional market-making teams, not open to the public, and there are no traditional external LPs. Its protocol does not have an official frontend interface, mainly accessed through routing aggregators, with a particularly critical integration with Jupiter. With a private liquidity pool structure, HumidiFi can achieve tighter spreads and lower slippage, especially suitable for large transaction demands. Since its launch in mid-June 2025, its trading scale has rapidly increased, with nearly $15 billion in transaction volume over the past 30 days, at one point accounting for 35%–40% of trading volume on Solana. Statistically, because there are no publicly locked assets, its TVL is usually counted as 0, but this does not affect its actual liquidity depth on the execution level.

Essentially, HumidiFi is closer to a "dark pool" trading model, sacrificing openness and visual liquidity for better execution efficiency and capital turnover rates; while DeFiTuna represents the extension of an open DeFi architecture, attempting to enhance the complexity of on-chain trading and capital efficiency through structural innovation. The two approach the competition of liquidity and order flow on Solana from the dimensions of "product capability" and "capital efficiency" respectively, intensifying the competitive landscape and presenting more diversified and targeted challenges for Meteora.

Conclusion

Looking at the overall experience, with Meteora, I see both the ambition of technology and the cohesion of the community. From DLMM, DAMM to dynamic vaults and liquidity locking, each product iteration feels like participating in a capital efficiency upgrade; "Meteora distinguishes itself from traditional AMMs through dynamic adjustments of fees and liquidity allocation, as well as mechanisms designed for fair distribution." From liquidity tools to ecological hubs, positioning itself as indispensable in the ecosystem may be the key to achieving stable profits.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。