Written by: Four Pillars

Compiled by: AididaoJP, Foresight News

Key Points

- Tokens ≠ Equity. Assess using enterprise value / holder income, not enterprise value / protocol income.

- The accrual ratio (proportion of the protocol income that holders can ultimately receive) is a key diagnostic indicator. Among the projects we compared, this ratio ranged from 25% to 100%.

- "Dilution" also has distinctions. Team incentives are real operating costs (should be included in valuation multiples), while investor lock-up sell-offs are market events (should not be included in multiples).

- Treasury value should consider "extractability." The issue is not "how much money is in the treasury," but "can holders extract it?"

I often see a common misconception in cryptocurrency valuation: someone pulls out a protocol with annual fee revenue of $500 million, divides market cap by that number, yielding a single-digit multiple, and then concludes that it is "cheap." This algorithm has an incorrect denominator and numerator. Investors think they are purchasing at a 5x valuation, but considering the actual income they can receive, that multiple may be 20x.

The price-to-earnings ratio is a good starting point, but it overlooks the balance sheet and capital structure—this is exactly why traditional finance uses enterprise value multiples (EV/EBITDA). However, when applying the EV/EBITDA concept to tokens, three fundamental issues arise:

- Treasury assets: holders do not have legal claims.

- Protocol income: most may never actually reach holders.

- Maximum cost: not showing up on the income statement, but reflected in new token issuance.

This article aims to construct a valuation framework adapted to the characteristics of tokens. The core metric is enterprise value / holder income—that is, the price you pay for every dollar of income that ultimately enters your pocket (as a token holder), taking into account the impact of the balance sheet and actual operational costs. I will illustrate using five protocols (HYPE, PUMP, MAPLE, JUP, SKY). This is not investment advice; it is merely a method demonstration.

1. How to calculate the "enterprise value" of a token?

Many token valuations begin incorrectly—with market cap directly, but market cap does not equal enterprise value.

In traditional finance, the logic is clear:

Enterprise Value = Market Cap + Debt - Cash

Because if you buy the entire company, you assume the debt while also taking the cash. Subtracting cash is reasonable, since that money is legally yours.

But in the crypto world, things get complicated. From automatic burn (USDC inflows, tokens permanently burned, no one can access that USDC) to foundation wallets (holding hundreds of millions of dollars, but lacking governance rights or distribution mechanisms), the situations vary greatly. The key question is not "what's in the treasury," but "can holders take it out?" (Of course, if someone acquires the entire protocol, the discount disappears, just like in traditional finance. The "claim discount" discussed here primarily targets us minority equity holders.)

I continue to use the term "enterprise value" because the logic remains consistent: you are calculating how much you need to pay to acquire the core business while excluding parts of the balance sheet that do not belong to you. The formula is as follows:

Token's Enterprise Value = Market Cap + Token Debt - Extractable Treasury Assets

Currently, most protocols do not have "token debt," so attention typically focuses on treasury assets.

First, let's break down what is in the treasury. A protocol's treasury typically holds three types of assets:

- Stablecoins: actual cash, which can in principle be fully extracted.

- Native tokens: their own tokens. Subtracting this part is akin to "self-reduction," typically requiring at least a 50% discount.

- Protocol-owned liquidity (POL) and other assets.

Total Treasury Assets = Stablecoins + Native Tokens × (1 - your estimated discount rate) + POL

But total assets ≠ extractable assets, which is the core issue this framework aims to resolve.

Some protocols do not even have treasury assets that can be discounted. For example, a pure burn mechanism (USDC inflows used for token buybacks and burns) will not create any assets that someone can access on the balance sheet. In this case, extractable treasury assets = 0, enterprise value = market cap. This is the clearest case, requiring no subjective judgment.

For treasuries that do hold real assets, I introduce the "claim discount" framework, which varies between 0% to 100% based on the degree to which holders can actually avail themselves:

- 0% discount: automatic buyback burn, requiring no governance vote; or the use of funds is completely decided by token holders.

- 25% discount: has an active DAO and a history of actual distributions.

- 50% discount: possesses governance rights, but it only stays on paper, never actually exercised.

- 75% discount: treasury controlled by the team, weak governance.

- 100% discount: funds controlled by a foundation, holders have no claims.

These percentages are the most subjective and vulnerable parts of the entire framework, I admit. However, a debate between two analysts that argues whether it should be 25% or 50% is far more significant than both ignoring the treasury and only discussing the P/E ratio.

Let's look at actual cases:

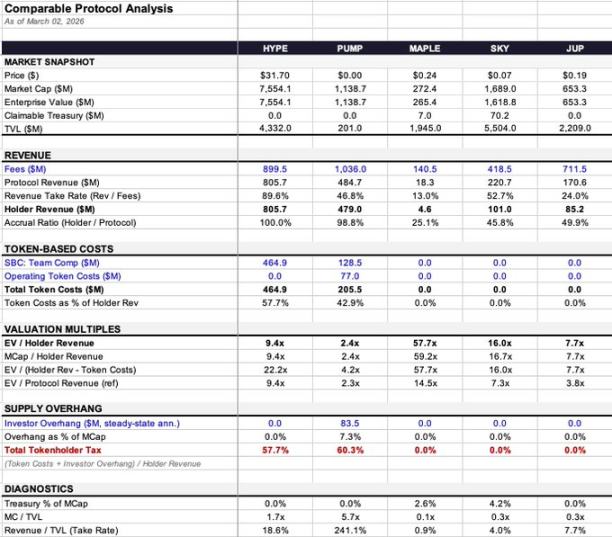

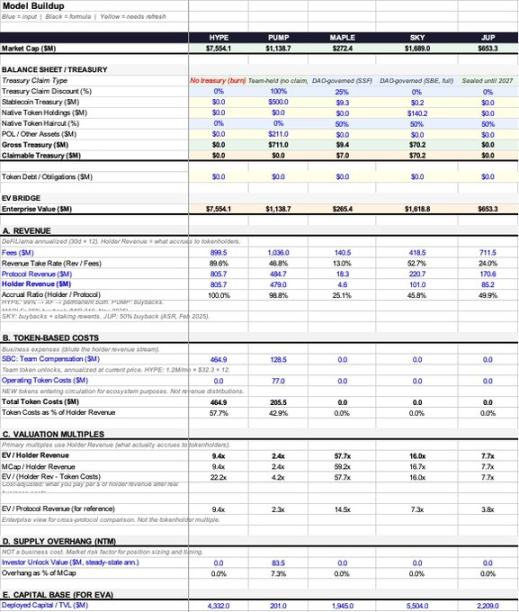

- Maple: Treasury has $9.36 million (99.7% is stablecoins), a small amount. Enterprise value was adjusted from $272 million to $265 million, a minor impact.

- SKY: Treasury has $140.3 million, but 99.9% are its own tokens. After applying a 50% discount, I estimate the extractable value at $70.2 million, causing enterprise value to drop from $1.69 billion to $1.62 billion.

- PUMP: Reportedly holds about $700 million in stablecoins, but lacks governance mechanisms and distribution channels, meaning holders cannot access it. Therefore, extractable assets = 0, enterprise value = market cap.

- HYPE and JUP: Similarly pure destruction or closed treasury, with no judgments needed, enterprise value = market cap.

2. Income and Token Costs: How Much Actually Ends Up in My Pocket?

The gap between what the protocol earns and what the holders receive is where most valuation frameworks fail and is the key factor influencing valuation multiples.

Think of income as a three-tiered waterfall:

- Fees: total amount paid by users.

- Protocol income: the portion left after payments to LPs, validators, and other "suppliers."

- Holder income: the amount that ultimately reaches token holders through buybacks, burns, or direct distributions.

There are two key conversion rates in between:

- Retention Rate = Protocol Income ÷ Fees (how much the protocol retains from total fees)

- Accrual Rate = Holder Income ÷ Protocol Income (of the retained portion, how much ultimately reaches holders)

These two ratios combined can yield vastly different effects:

- HYPE: Retention Rate 89.6%, Accrual Rate 100%. Out of nearly $900 million in fees, $805.7 million ultimately flowed to holders.

- Maple: Retention Rate 13% ($140.5 million fees → $18.3 million protocol income), Accrual Rate 25.1% ($18.3 million protocol income → $4.6 million holder income). Total accrual rate is only 3%, whereas HYPE's is 90%.

Under the same framework, one is 3% and the other is 90%. If you directly use "EV/ fees" or even "EV/ protocol income" to compare these two protocols, the differences are staggering.

Why use "holder income" as the denominator instead of "protocol income"?

In traditional finance, EV/income works because equity holders have the residual claim—legally it belongs to them. However, token holders do not have this right; they can only obtain the portion designated for them by the token economic model. If income is locked up in a treasury controlled by the team, with no distribution mechanisms for holders, then simply holding governance tokens does not make that income "yours."

Using "protocol income" as the denominator would embellish those protocols with low accrual rates, making them appear cheaper than they really are. I refer to this gap as "accrual discount."

Take Maple as an example:

- EV/ protocol income = 14.5x

- EV/ holder income = 57.7x

A full 4x difference! The same data, based on different denominators, leads to completely different judgments about "market pricing."

3. Costs: Dilution is Not Created Equal

The term "dilution" is used too broadly in the crypto circle; misclassifying it leads to valuation errors.

First type: Team incentives (equity incentives)—this is an operating cost

Buffett stated decades ago: If incentives are not counted as costs, what are they? Gifts? In traditional finance, it shows up on the income statement, reducing profits. In the crypto world, it manifests as new tokens entering the market, but the economic essence is identical—this is the true cost of operating the business.

- HYPE: Team incentives annualize to $464.9 million, consuming 57.7% of holder income.

- PUMP: Team incentives annualize to $128.5 million.

These should all be included in valuation multiples.

Second type: Operational token costs (ecosystem incentives, user acquisition, etc.)—this is also an operating cost

Their role is akin to customer acquisition costs, and they too represent actual costs that should be included in multiples. In addition to team incentives, PUMP has $77 million in operational token costs, leading to a total token cost of $205.5 million.

The judgment standard is simple: Does it create new token supply?

If the protocol only distributes existing income to stakers without issuing new coins, that cost has already been reflected in the previous cash flows (i.e., the difference between protocol income and holder income).

If the protocol mints or unlocks previously non-circulating tokens, then it is real dilution and an operating cost.

Third type: Investor lock-up expirations—this is a market event, not an operating cost

You wouldn't subtract VC sell-offs from Apple's profits to get an "adjusted profit." Similarly, this should not be included in operating multiples.

PUMP has an annual potential investor selling pressure of $83.5 million, accounting for 7.3% of market cap. This significantly affects price movements and market dynamics, but does not constitute operating costs. I place it separately in a diagnostic metric called "total token holder tax" (token cost + investor potential selling pressure, as a percentage of holder income), but it is not included in the core valuation multiple.

4. Four Core Multiples and One Diagnostic Metric

Based on the above logic, we derive the following metrics (defined uniformly here, referenced directly later):

- EV/ holder income (core metric): How much you pay for every dollar of income that ultimately enters your pocket.

- Market Cap / Holder Income: Same as above, but without treasury adjustments. The difference reflects the impact of the balance sheet.

- EV/(Holder Income - Token Costs) (cost-adjusted multiple): Deducts actual operating costs (team incentives, operational costs), but not including investor selling pressure.

- EV/ Protocol Income (for reference only): The difference from EV/ holder income indicates the size of the "accrual discount."

- Total token holder tax (diagnostic metric): = (token costs + investor selling pressure) ÷ holder income. It reflects the dual impact of operating costs and supply pressure in one number. For example, PUMP is 60.3%, meaning for every $1 of income reaching holders, there’s an extra $0.603 impacting the market through new supply. This figure itself does not directly indicate valuation levels, but hints at the dynamic relationship between cash flow and supply.

5. Data Overview and Case Highlights

- HYPE: Accrual rate 100%, 9.4x holder income. However, due to high team incentive costs, the cost-adjusted multiple rises to 22.2x. Revenue structure is clear; complexities do not arise from the income side.

- PUMP: Appears cheapest (2.4x), accrual rate 98.8%. But treasury is non-extractable, and there’s a large unlocking in August 2026. Cost-adjusted multiple rises to 4.2x, with a total token holder tax of 60.3% (the highest in the sample).

- MAPLE: Largest accrual discount (4x). Protocol income 14.5x vs. holder income 57.7x, with a huge gap. No token costs, hence the cost-adjusted multiple remains unchanged.

- JUP: Cleanest balance sheet. Through "net-zero emissions" governance, no token costs, no investor selling pressure, no extractable treasury. All multiples trend towards 7.7x.

- SKY: Accrual rate 45.8%, best showcases how "denominator choice affects valuation." Protocol income multiple is 7.3x (seemingly cheap), while holder income multiple is 16.0x (not so cheap anymore). Treasury is primarily (99.9%) its own tokens, needing a discount.

6. Conclusion

This framework certainly has weaknesses:

- The treasury claim discounts are subjective: I may rate it 25%, you may rate it 50%, and neither can convince the other.

- The judgment of "whether to mint" can become complicated: some protocols have minting functions open, but distribution channels are dead, leading to unclear situations where tokens accumulate in undeployed pools.

- Data sources have noise: DeFiLlama's 30-day annualized data may make the same protocol appear one time cheap or expensive due to different monthly snapshots.

But at least it serves as an operational starting point. EV/ holder income, adjusted for the balance sheet and actual operating costs, allows you to better understand how much real income you are buying for every dollar you spend.

The gap between what the protocol earns and what holders actually receive is the largest fundamental mismatch in the current market. Many protocols generate hundreds of millions in fees, yet holders receive only a small fraction, and most valuation frameworks do not even distinguish between the two.

Fortunately, the industry is beginning to focus on value capture: fee switches are being activated, buybacks are replacing inflationary staking, and governance layers are pausing incentive voting. We are building tools to measure what is truly happening more accurately.

7. Data Sources and Methodology Notes

- Income Data: DeFiLlama annualized data (recent 30 days × 12). The advantage is that it is more responsive compared to half-year data, but the drawback is that single-month fluctuations may introduce noise.

- Holder Income: Directly using DeFiLlama's "holder income" field, which includes only buybacks, burns, and direct distributions.

- Treasury Data:

- MAPLE: $9.36 million (DeFiLlama, 99.7% stablecoins)

- SKY: $140.3 million (DeFiLlama, 99.9% own tokens)

- JUP: $0 (closed)

- PUMP: Stablecoins estimated to be $500 million at median (actual range $286 million - $800 million)

- Token Costs:

- MAPLE: $0. The MIP-019 proposal (October 2025) has concluded the staking distribution. Although a smart contract with 5% inflation may still be minting, there are no distribution channels. (Source: docs.maple.finance, The Defiant October 31, 2025)

- SKY: $0. The savings module (STR) now distributes SPK and Chronicle Points instead of SKY tokens. (Verified March 2026 at app.sky.money/rewards). The data mentioned by Rune in August 2024 regarding "600 million SKY annually" is outdated; governance can restart at any time. (Source: sky.money FAQ, vote.sky.money)

- JUP: $0. The "net-zero emissions" proposal passed on February 22, 2026 (75% approval). The DAO treasury is closed until 2027.

- Investor Selling Pressure:

- PUMP: Steady state annualized $83.5 million. Actual unlocking cliff starts in August 2026, with an estimated selling pressure of about $48.7 million in the next 12 months (based on 7/12 months).

- Lending Protocol Metrics:

- MAPLE: Uses actual assets under management (AUM) ($3.79 billion, Q1 2026 report) rather than DeFiLlama's TVL ($1.94 billion). Net interest margin (NIM) = protocol income / AUM. See the Excel appendix for detailed metrics.

- Cash Operating Expenditure: Not estimated. As the protocol does not disclose it, speculation may lead to false accuracy.

- Equity Incentive Valuation: Calculated at current token prices. Sensitive to price changes.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。