For traders in the global market, the past week can be described as a "Game of Ice and Fire." One moment, the market was anxious about the impact of artificial intelligence on employment; the next moment, the sudden outbreak of conflict in the Middle East completely took over the headlines.

Tonight (March 6) at 21:30, the highly anticipated U.S. February non-farm payroll report will be released as scheduled. However, on this special "non-farm night," everyone's attention must be split, with half tightly focused on the smoke rising over the Persian Gulf. When a geopolitical black swan collides with an economic data gray rhino, the Federal Reserve's monetary policy faces an unprecedented dilemma of "burning at both ends."

1. The "Gunfire" and "Oil Fire" in the Strait of Hormuz

Just before the non-farm data is released, the situation in the Middle East escalates again.

● On March 5 local time, Hezbollah claimed to have hit the assembled Israel Defense Forces with guided missiles. Even more chilling for the market, the Iranian Revolutionary Guard announced it had launched missiles hitting a U.S. oil tanker in the northern Persian Gulf, explicitly drawing a red line: prohibiting U.S., Israeli, and European vessels from passing through the Strait of Hormuz.

● The Strait of Hormuz, a "major artery" for global energy, translates any minor disturbance directly into the "war premium" in oil prices. Since the outbreak of conflict, international oil prices have risen nearly 20%, with WTI crude spiking above $77 and Brent crude nearing the $85 mark.

● Superficially, this is a military strike; in reality, it is the "oil fire" igniting the fuse of inflation. Soaring energy prices are like "high blood pressure" in the economy, instantly tightening the nerves of the Federal Reserve, which had just seen a glimmer of cooling hope. After all, according to the International Monetary Fund (IMF), every 10% increase in oil prices pushes global inflation up by 0.4 percentage points.

2. The Federal Reserve's "Zero Rate Cut" Script: From "Possible" to "Mainstream"

● If a week ago, the market was debating whether to cut rates twice or once this year, now a more extreme script is taking center stage — "zero rate cuts for the whole year," even reigniting expectations for rate hikes.

● Data from the Atlanta Federal Reserve as of Wednesday revealed this jaw-dropping expectation reversal: traders are now betting that the probability of the Fed maintaining the interest rate unchanged by the end of this year has soared to 25%, up from 17% the day before the conflict erupted. Among all scenarios, "holding steady" has become the most probable scenario. Even more extreme, the market now believes the probability of a rate hike has reached 16%, doubling from 8% last Friday.

● This sudden shift in sentiment has directly detonated the bond market. The U.S. Treasury, traditionally a safe-haven asset, has rare encounters with selling, with the 10-year Treasury yield soaring above 4.1%, completely overturning the traditional logic of "safe-haven funds rushing into Treasuries." Analysts at Orient Jin Cheng pointed out that the core reason lies in the market's concerns have rapidly switched from "risk aversion" to "defense against inflation." Faced with the import inflation brought by rising oil prices, investors are demanding higher yields to compensate for future losses.

● The remarks of Richmond Fed President Barkin further doused cold water on the market. He pointed out that the recent strong labor market combined with sticky inflation and the ongoing Middle Eastern conflict could drive prices even higher, meaning the "risk outlook" faced by the Fed has changed. Fed Governor Bowman also bluntly stated that the stabilizing labor market supports maintaining interest rates unchanged at the next meeting.

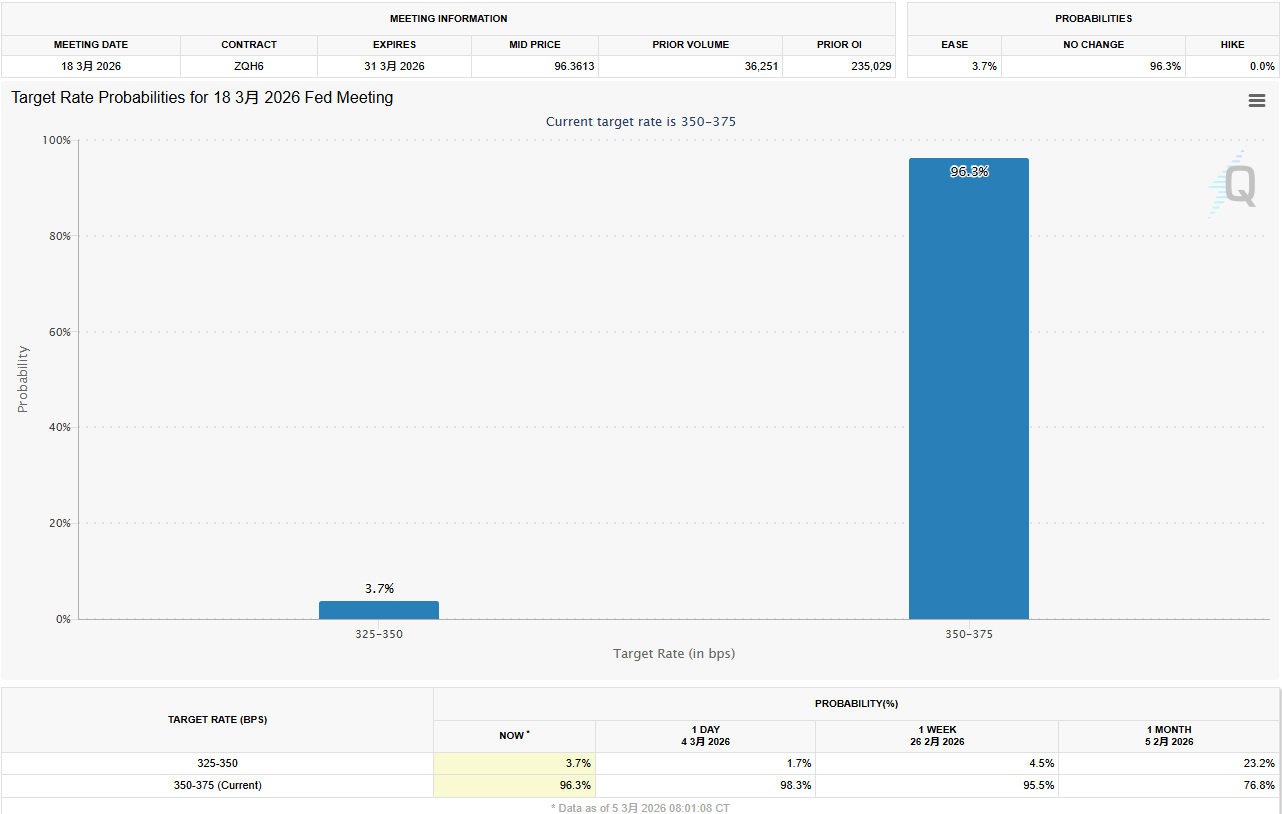

● Currently, the CME Group's FedWatch tool indicates that the probability of maintaining rates unchanged in March has surpassed 97%. The once-anticipated "rate cut in March" has essentially been declared dead amidst the dual onslaught of conflict and data.

3. The "Data Trap" of Non-Farm Night: Weakness May Actually Be a Positive?

In such a tense geopolitical atmosphere, tonight's non-farm data seems somewhat "misaligned."

The market widely anticipates that the number of new non-farm jobs in February will slow significantly to around 60,000 (some expect it to be 59,000), far below January's 130,000, while the unemployment rate is expected to remain at 4.3%. The ADP report released on Wednesday showed that U.S. businesses added 63,000 jobs in February. Although this slightly exceeded expectations, it still indicates that hiring is concentrated in a few sectors like healthcare and education, with growth not being broad-based.

There exists an interesting "data trap":

● If the data is too strong (such as over 100,000 new jobs): coupled with the previously resilient inflation, the market will further strengthen the "no landing" expectation. Together with rising oil prices in the Middle East, the Fed will not only refrain from cutting rates but may be forced to discuss "another rate hike," which would be a major blow to risk assets.

● If the data is moderate or even weak (such as meeting expectations or lower): it may instead become a "lifeline" for the market. A cooling employment report can at least demonstrate that the economy is not overheating and allows the Fed to maintain its current "steady stance" in the face of oil price shocks, framing it as "observation" rather than being forced into tightening.

Ben Ayers, a senior economist at Nationwide Insurance, predicts hiring will be weaker, with an increase of only 40,000, reflecting the current unique economic environment of "low hiring, low layoffs."

4. Beyond the Data, Focus on These Two Details

In addition to the headline numbers, analysts tonight will also focus on two other key points:

● Breadth of Employment: The strength in January was primarily driven by healthcare and social assistance. If February's hiring can expand to more sectors, it indicates strong internal economic momentum. If it remains concentrated in a few areas, the vulnerability of the recovery should be monitored.

● Unemployment Rates Among Specific Groups: Comerica Bank Chief Economist Bill Adams pointed out that unemployment rates for Black and young workers are often leading indicators of a weakening labor market. These two data points fell back in January; if they show continuous improvement in February, it would be a real "confidence booster" for the labor market.

5. Yellen's Warning and the Worst-Case Scenario

● Regarding the current situation, former Fed Chair Yellen has provided a rather pessimistic assessment: this conflict may both drive up U.S. inflation and slow economic growth. This is the classic "stagflation" risk — the monster that central banks fear most.

● Natixis economist Hodge pointed out that if the conflict de-escalates quickly, the impact on oil prices will be limited; but if the conflict expands and prolongs, pushing oil prices to remain above $120, the U.S. economy could shift to negative growth, with rising unemployment. At that point, the Fed may be forced to quickly cut rates to respond to a recession — but this would signal trouble for the economy, rather than a boon for the market.

● Tonight, whether the non-farm data shows 60,000 or 130,000 jobs, it is unlikely to raise the flag for a rate cut by the Fed in March. Until the gunfire in the Strait of Hormuz cools down, "pause" will be the only and helpless choice for the Fed. For investors, rather than guessing the data, it may be more prudent to buckle up and brace for an era of high volatility dominated by geopolitics.

Join our community to discuss and become stronger together!

Official Telegram community: https://t.me/aicoincn

AiCoin Chinese Twitter: https://x.com/AiCoinzh

OKX Welfare Group: https://aicoin.com/link/chat?cid=l61eM4owQ

Binance Welfare Group: https://aicoin.com/link/chat?cid=ynr7d1P6Z

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。