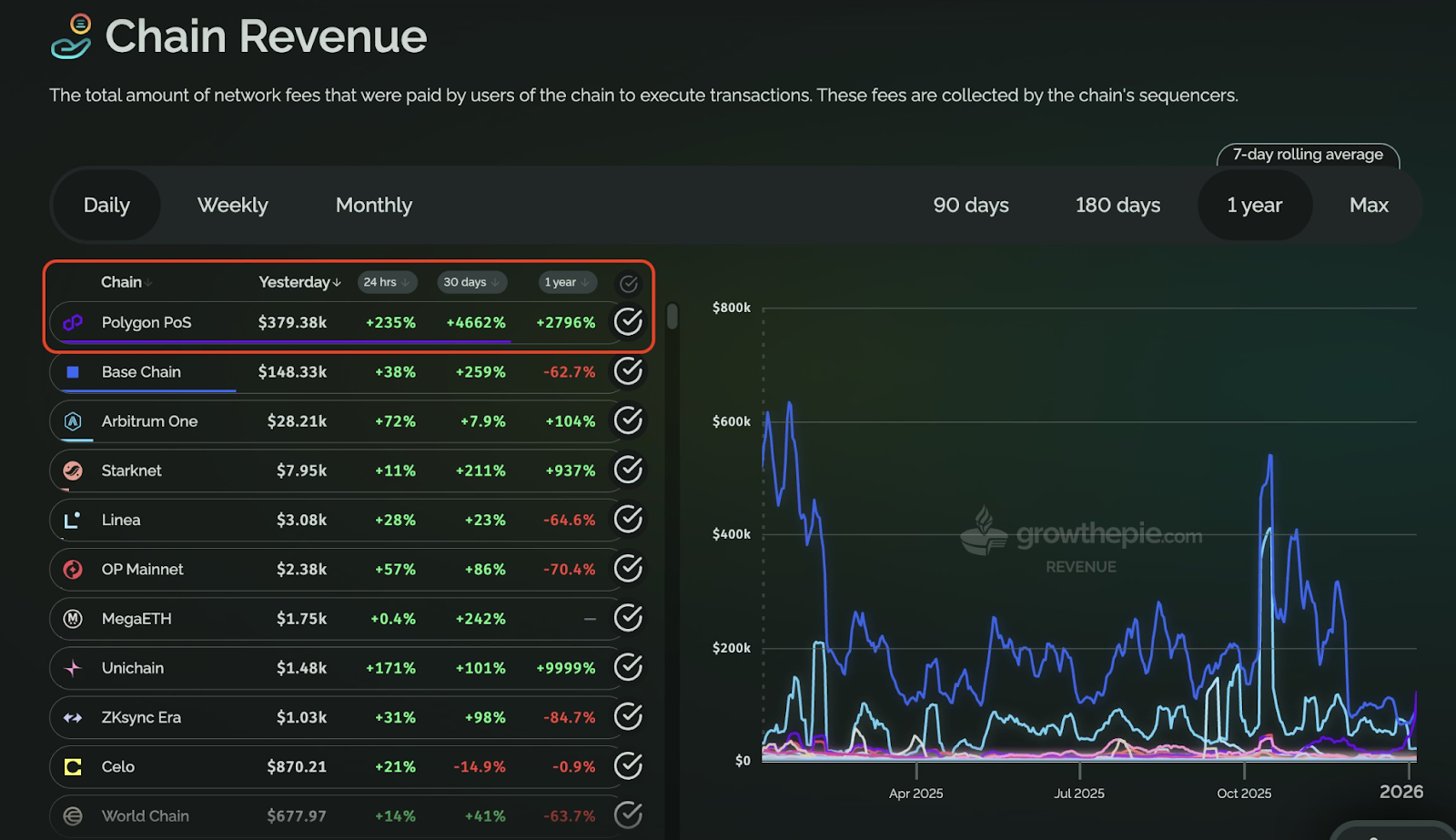

In the past period, the explosive popularity of the prediction market project PolyMarket has taught the industry a lesson: when a truly demanded and product-oriented application takes off, it can not only bring users and topics but can even push a long-dormant network back into the spotlight—Polygon once surpassed Base to top Chain Revenue, which is a highly representative signal. But what is even more noteworthy is PolyMarket's repeated emphasis on its "primary task" amidst the heat: to build its own chain.

This sounds like a further technical upgrade, but essentially it is an inevitable choice when an application enters the deep waters of growth. Once product validation is complete, trading behavior stabilizes, and user scale expands, the application begins to be dissatisfied with "renting someone else's underlying infrastructure" and hopes to control key experiences and revenue segments itself. A similar path has also appeared in another more typical case: the leading Perp DEX Hyperliquid. It did not settle for being an "application" on a mainstream public chain but directly unified the trading system, execution environment, and user experience by building its own App Chain, ultimately achieving a level of smoothness and throughput close to that of a "centralized exchange," thereby establishing a competitive moat.

When looking at these two cases together, they point to the same trend: App Chains are becoming the new Alpha.

Why do "successful applications want to build their own chains"?

The more successful an application is, the more likely it is to reach the "self-built chain" step, and the reason is very practical: when you move from "validating whether the product can run" to the "scalable operation" stage, the public chain brings not just traffic and tool dividends, but a host of external variables that you cannot control. In the early stages, choosing a public chain is certainly the most cost-effective—deployment is quick, the ecosystem is mature, and users and assets are already there. The most important thing is to get the product running smoothly and ensure users are willing to continue using it; however, once the business explodes, your key paths will increasingly be affected by congestion, fee fluctuations, confirmation times, and other public network states, and the uncertainty of the experience begins to directly consume conversion and retention. At the same time, costs will shift from "user complaints" to "financial structure": in high-frequency, high-volume scenarios, gas and infrastructure expenses will become a curve that must be meticulously calculated, managed, and may fluctuate dramatically with external environments.

Furthermore, successful applications will pay more attention to "value closure" and "iteration speed." A significant portion of the transactions and growth you achieve is often naturally captured by the underlying and intermediate layers, making it difficult for you to accurately return incentives to the core users who truly contribute liquidity and trading; you want to customize rules for key processes and optimize the execution environment, but you can only make minor adjustments within the public framework. Thus, projects like PolyMarket that have already gained momentum will treat "building their own chain" as the main line for the next stage; strong trading products like Hyperliquid directly bind the execution environment, experience, and economic system together with an App Chain, turning controllability into a competitive moat. At this stage, the chain is no longer just a deployment location but a part of the product.

Chains can be launched, but network effects may not keep up

App Chains are indeed becoming a trend, but this does not mean the barriers to entry have lowered—more accurately, it is becoming "easier to launch a chain," while "making the chain truly operational" is becoming increasingly difficult. Many teams believe that after building their own chain, they can reclaim the experience, costs, and rules, only to find out upon launch that the most challenging part has shifted from engineering implementation to network operation: users will not migrate just because you have an additional chain, and funds will not automatically flow in just because you changed the execution environment. Once the chain is independent, it will immediately face the reality of "starting from scratch": how to onboard the first batch of users, how to ensure assets flow smoothly, and how to stabilize transaction and usage frequency—none of these can be solved merely by launching the chain itself.

More specifically, App Chains commonly encounter three walls:

- Cold start: New chains lack default entry points and locations, requiring users to learn, switch, and trust additionally.

- Liquidity fragmentation: Once assets cross chains, versions and paths emerge, pools become fragmented and lack depth, leading to a user experience that becomes more expensive, slower, and more complex, even resulting in confusion where "the same coin has different prices in different places."

- Weak ecological synergy: You can make the product more specialized and extreme, but if it cannot be seen by a larger network or cannot form smooth asset and user flows with other chains and applications, it can easily become a "powerful but isolated new island."

Therefore, the truly scarce capability in the App Chain era is shifting from "can we launch a chain" to "can we make the chain a part of the network from day one," allowing the flow of users and funds to be as natural as if they were on the same chain.

Accelerating the App Chain into the flywheel—from "launching" to "using"

The difficulty of App Chains is no longer just about "can we launch a chain," but whether it can be immediately utilized after launch: how users come in, how assets arrive, how liquidity is sustained, and whether cross-chain experiences will be dragged down by fragmentation. Many ambitious teams consider app chains because they essentially want "to own their own underlying infrastructure" (sequencing, block production rhythm, execution model, RPC, transaction revenue, etc.), using more controllable block space to create better products and businesses; but in reality, poor interoperability and fragmentation between chains often turn onboarding into a cost black hole, making the launch of a new chain feel like a "new island" rather than a "network node."

Caldera's entry point is to make this path a reusable product suite: using the Rollup Engine to lower the deployment and operational thresholds, transforming chain launching from heavy engineering into a more controllable routine; then using Metalayer to make "connections" a default configuration, equipping each chain from day one with a complete set of capabilities such as cross-chain messaging, rapid bridging, bridge aggregation, and development tools, reducing friction in the flow of users and funds across chains, making "going live" closer to "joining a ready-made interconnected ecosystem." On this basis, Caldera's growth logic is not a single-point SaaS but a network flywheel: each new chain will bring new users and sources of liquidity, and Metalayer will make it easier for these increments to flow within the ecosystem and feed back into existing chains, thereby enhancing the entire network's attractiveness to the next batch of teams.

The design around $ERA further accelerates and compounds the flywheel: it serves as a universal participation and economic coordination vehicle for Metalayer (the fee pricing basis for cross-chain interactions, etc.), and through staking/node participation and governance, it binds the incentives of chains, applications, users, and infrastructure participants within the same network, transforming collaboration and growth from "possible" to "easier to sustain." A more intuitive example is that ecological linkage incentives themselves will reinforce network effects; for instance, Espresso allocated over 2% of the total supply of $ESP to the Caldera community during its TGE and made holders and stakers of $ERA key targets for airdrops: the value return from high-quality external partners enhances the attractiveness of participating in the $ERA ecosystem; and more holding and staking further strengthen network cohesion and collaboration expectations, in turn facilitating more cooperation and more chains choosing to "join the network." Ultimately, what Caldera aims to solve is to ensure that App Chains not only can be launched but can also be used more smoothly from day one and enter the growth flywheel more quickly.

The Alpha of App Chains lies not in "launching chains," but in "networking"

From PolyMarket to Hyperliquid, the industry is increasingly clear on one thing: when applications enter the stage of scalable operation, "chains" will upgrade from deployment locations to parts of the product, with experience, cost structure, iteration speed, and value return all beginning to be rewritten around it. However, the true threshold for App Chains has also changed: launching chains is becoming easier, but the challenge is to ensure that the chain has entry points, asset paths, liquidity, and collaboration right from the start. Therefore, the next phase of Alpha is not "who has launched more chains," but who can turn "new chain cold starts" into actions of "joining the network," reducing fragmented friction to a sufficiently low level, allowing users to complete deposits, transactions, and cross-chain usage as naturally as if they were on the same chain. When this connectivity capability and incentive mechanism (such as participation and external cooperation returns around $ERA) can continuously self-reinforce, App Chains will transition from single-point successes to replicable systemic victories, thus becoming the truly sustainable new Alpha.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。