Author: Yokiiiya

Today, we continue to deeply analyze the product logic and technical architecture of Polymarket, stripping away complex financial terminology and obscure code logic, and trying to explain it in plain language.

The main content includes: exploring how it uses blockchain technology to ensure fairness, how it designs incentive mechanisms to encourage thousands of traders to spontaneously maintain market order, and how it reshapes our understanding of "prediction" relying on decentralized technology moats amidst fierce competition from traditional financial giants like Robinhood.

A glossary of related terms is at the end.

1. The Revival of Prediction Markets and the Information Revolution

1.1 What is a Prediction Market

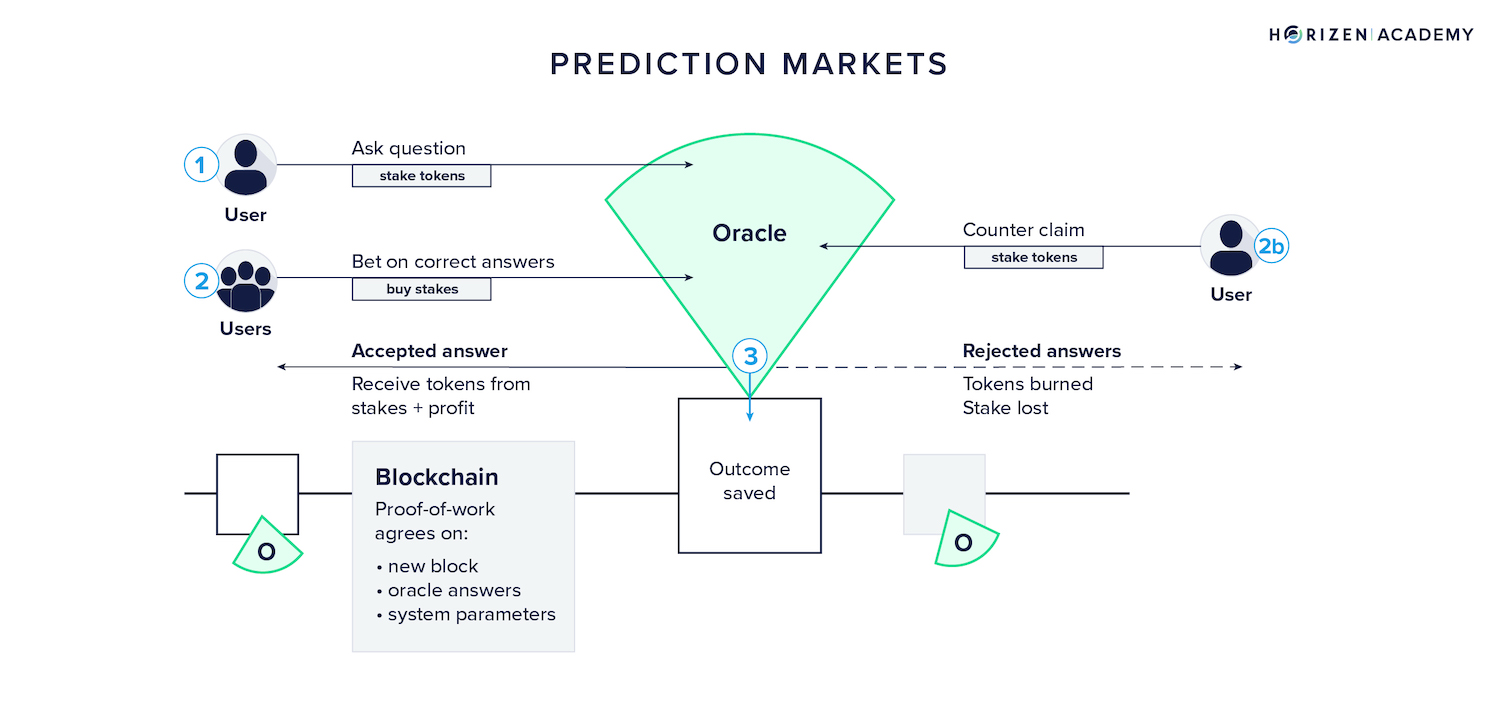

To understand Polymarket, we first need to establish a core understanding: the essence of prediction market trading is the ownership of future facts.

In daily life, everyone has made bets with friends. For example, Zhang San believes it will rain this weekend, while Li Si believes it will not. They agree that the loser will pay the winner 100 yuan. This primitive betting has several obvious flaws: first, the funds are not guaranteed, and the loser may default; second, since only two people are involved, this bet cannot reflect the objective probability of rain—Zhang San might think it will rain just because he recently washed his car, which is a highly subjective and limited judgment.

Polymarket has highly standardized and financialized this primitive social interaction.

On Polymarket, the aforementioned "bet" is transformed into a binary options contract. The system abstracts the question "Will it rain this weekend?" into an asset package with a total value of 1 dollar. This asset package is split into two independent rights certificates (Shares):

"Yes" share: If it rains this weekend, this certificate can be redeemed for 1 dollar.

"No" share: If it does not rain this weekend, this certificate can be redeemed for 1 dollar.

Regardless of the final outcome, one and only one of Yes and No will be redeemable for 1 dollar, while the other will go to zero. Therefore, at any moment, the price of Yes plus the price of No should theoretically be very close to 1 dollar (ignoring transaction friction).

The brilliance of this design lies in the fact that price equals probability. If the trading price of the "Yes" share is currently 0.65 dollars, it means market participants are willing to spend 0.65 dollars to buy a chance that could become 1 dollar or could become 0. The collective subconscious behind this indicates that the market believes the probability of rain is 65%.

This probability, built from the real money of millions of people, is often more accurate than the single predictions of polling experts or meteorological stations because it eliminates the noise of "cheap talk"—as the old Wall Street saying goes: "Put your money where your mouth is."

1.2 Why It Has Become Popular Now

The concept of prediction markets was proposed by economists decades ago, and early decentralized attempts like Augur also had their moments, but why has it only been with Polymarket that large-scale breakout has truly been realized? The answer lies in the dual maturity of technological infrastructure and market demand.

From a technical perspective, Polymarket has addressed the fatal flaws of early blockchain applications being "slow, expensive, and difficult." Early prediction markets were built on the Ethereum mainnet, where placing a bet could require paying dozens of dollars in gas fees, and confirmation times could take several minutes, which is unacceptable for high-frequency event trading.

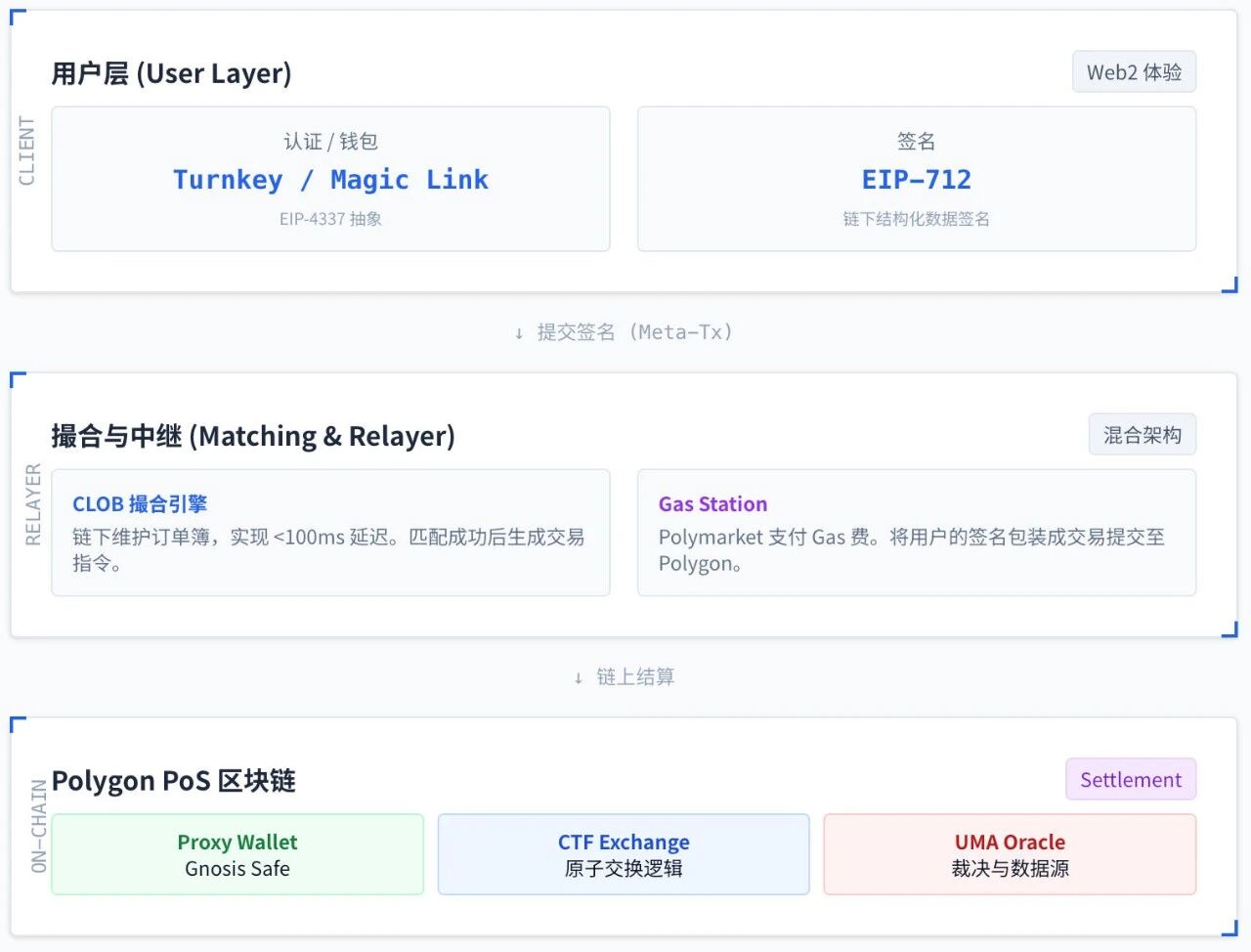

Polymarket creatively adopted a hybrid architecture combining Layer 2 scaling solutions (Polygon) with a centralized limit order book (CLOB), making transaction costs nearly zero and achieving millisecond-level transaction speeds, while also using account abstraction technology to allow users to log in without needing to understand private keys and mnemonic phrases.

From the demand side, the global macro environment from 2024 to 2025 is filled with uncertainty. The tightness of the U.S. elections, geopolitical turmoil, shifts in Federal Reserve monetary policy, and severe fluctuations in the cryptocurrency market have led to a peak in public demand for "certainty."

Financial technology giants like Robinhood have reported that retail investor activity is at historical highs, and they are increasingly inclined to participate in this binary nature of "event contract" trading. Vlad Tenev pointed out that prediction markets are evolving from a niche experimental field to a mainstream asset class alongside stocks and futures, marking the arrival of a super cycle.

2. Core Product Logic and User Interaction Mechanism

2.1 Core Product Logic: Binary Options and Conditional Tokens

Polymarket's product design philosophy is minimalist. Although complex smart contracts run in the background, what is always presented to users in the front end is that simple and intuitive interface: one question, two buttons (Yes/No), and a curve reflecting probability trends.

2.1.1 Standardized Packaging of Binary Options

In Polymarket's product logic, any event with a clearly verifiable outcome can be packaged into a market. This market is represented on-chain as a smart contract address. When users participate in trading, they are actually buying and selling a special crypto asset called "conditional tokens."

These tokens follow the ERC-1155 standard, which is a more advanced token standard than the common ERC-20 (like USDT). If ERC-20 is likened to individual banknotes, then ERC-1155 is like a container that can hold various items with different attributes. Within the same smart contract, thousands of different prediction event tokens can exist simultaneously without needing to deploy a new contract for each event, greatly reducing system resource consumption and user interaction costs.

2.1.2 Price Discovery Mechanism: The Evolution from AMM to CLOB

For novice users, understanding "who is selling me this token" is crucial. Polymarket has undergone a key transformation from "machine pricing" to "everyone pricing."

Early Stage (AMM Model): Initially, Polymarket used an automated market maker (AMM) mechanism. This is like a vending machine, where prices are determined by a fixed mathematical formula (constant product formula). When more people buy Yes, the Yes in the pool decreases, and the price automatically rises. The advantage of this model is that there is always liquidity, but it suffers from significant slippage when facing large amounts of capital and has low capital utilization.

Current Stage (CLOB Model): To accommodate institutional-level capital entry, Polymarket has transitioned to a centralized limit order book (CLOB). The current trading interface resembles a stock exchange, where users can see the depth of buy and sell orders. If you want to buy Yes, your counterparty is no longer a machine, but another real user or market maker who believes the event will not happen (selling Yes or buying No). This mechanism not only makes price discovery more accurate but also allows users to place limit orders, thus gaining pricing power.

2.2 Money Printer: Automatic Correction System

In Polymarket's advanced player community, there is a feature known as the "Money Printer," which includes Split and Merge. This is not only a technical feature but also the economic cornerstone that maintains the rigor of Polymarket's price logic.

Let’s explain why this mechanism is needed using ETFs.

Why do ETF prices in the stock market usually not stray too far from their net asset value (NAV)? It relies on "creation/redemption":

ETF price too high: Institutions take a basket of stocks to exchange for ETFs (creation), then sell the ETFs, driving down the ETF price.

ETF too cheap: Institutions buy ETFs and then exchange them back for that basket of stocks (redemption), driving up the ETF price.

This logic is almost isomorphic to Split/Merge: both involve "creatable/redeemable" to anchor the price. However, Polymarket anchors the sum of Yes + No ≈ 1, while ETFs anchor ETF price ≈ NAV.

In Polymarket's binary prediction market, contracts provide a "perpetually available official exchange window," allowing you to convert 1 USDC into a pair of complementary positions (Yes + No), and also to convert this pair of complementary positions back into 1 USDC at any time. Once this window opens, market prices will be voted back to "where logic should be" by arbitrageurs.

The reason why Split/Merge is considered "the economic cornerstone that maintains the rigor of Polymarket's price logic" is that it transforms this market from a "pure secondary exchange" (where you can only buy shares others sell) into a structured market with a "creation/redemption mechanism." As long as there is creation/redemption, prices will be locked by a hard constraint, and arbitrageurs will automatically pull deviations back.

Suppose at a certain moment, the market is in extreme panic, with someone selling Yes at 0.60 and someone selling No at 0.35.

At this time: $0.60 + 0.35 = 0.95 < 1.00$.

Sharp arbitrageurs (or bots) will immediately execute the following operations:

Spend 0.60 in the market to buy Yes, spend 0.35 to buy No, with a total cost of 0.95 USDC.

Immediately call the "Merge" function to exchange this pair of tokens for 1.00 USDC.

Net profit of 0.05 USDC (risk-free profit).

This arbitrage behavior will instantly raise the prices of Yes and No until their sum returns to around 1.00. Conversely, if the sum of prices is greater than 1 (for example, Yes 0.7 + No 0.4 = 1.1), arbitrageurs will execute the "Split" operation: spend 1 USDC to mint a pair of tokens, then sell them separately at 0.7 and 0.4, making a profit of 0.1.

In the prediction market circle, such mechanisms have existed in the Conditional Tokens framework of Augur and Gnosis/Omen; Polymarket has turned it into a scalable, robot-participatable "automatic correction system," allowing it to truly serve as market infrastructure.

The core problem it truly solves can be summarized in three words: self-consistency.

1) Supply self-consistency: Even if no one sells, shares can still be "created," and the market will not freeze due to a lack of supply.

2) Price self-consistency: The hard constraint of Yes + No can be executed through arbitrage, pulling prices back into logical ranges.

3) Governance self-consistency: There is no need for a centralized administrator to monitor and correct; corrections are automatically driven by arbitrage incentives.

When viewed together, its "core function" is to upgrade the pricing of prediction markets from being "strenuously maintained by human sentiment and matchmaking" to being "automatically maintained by executable arbitrage constraints." The platform does not need to arrange for a centralized administrator to monitor and correct prices, nor does it need to rely on the morality and financial strength of a single market maker; all arbitrageurs serve as a free correction system.

2.3 Smooth and Seamless User Experience Design

For novice users accustomed to Web2 applications (like Robinhood, Alipay), the usage threshold of Web3 is often discouraging: it requires downloading wallet plugins, saving 12 mnemonic words, purchasing ETH for gas fees, and understanding complex signature mechanisms. Polymarket's success largely stems from its technical means of "hiding" this complexity.

2.3.1 Email Login and Custodial Wallets

Polymarket integrates Magic Link or similar account abstraction technologies. Users only need to enter their email and click a verification link, and the system will automatically generate a non-custodial Ethereum wallet for them in the background. For users, this is no different from logging into a regular website, but in reality, they now own their own on-chain address. The private key of this wallet is typically split and encrypted for storage, ensuring security while avoiding the risk of users losing their private keys.

2.3.2 Relayer and Gasless Transactions

On the blockchain, every operation (such as placing an order, canceling an order, merging tokens) theoretically requires paying miner fees. To provide a smooth experience, Polymarket introduces a Relayer architecture.

When a user clicks "Buy," the front end does not directly initiate an on-chain transaction but instead has the user sign a data packet containing the transaction intent (EIP-712 standard signature). This signature is free.

The user's browser sends this signature to Polymarket's Relayer server. Once the Relayer verifies the signature, it packages it into a real transaction and pays the MATIC token as the miner fee out of its own pocket, sending it to the Polygon network for execution.

Through this method, users perceive it as "click to complete," without needing to worry about gas fees and on-chain congestion issues. This is a typical "Web2 experience, Web3 settlement" architecture model.

3. In-Depth Technical Architecture Analysis

3.1 Infrastructure Layer: Why Choose Polygon?

Polymarket is not built directly on the Ethereum mainnet (Layer 1) but has chosen the Polygon PoS sidechain (which is gradually migrating to more advanced Layer 2 solutions like zkEVM). This choice is based on a trade-off between cost and speed.

Cost considerations: The transaction amount in prediction markets can be very small (a few dollars or even a few cents). If using the Ethereum mainnet, the gas fee for a single transaction could be as high as 5-10 dollars, which would directly destroy market liquidity. Polygon's gas fees are typically only a few cents or even lower, making the Relayer payment model economically sustainable.

Speed considerations: Polygon's block time is about 2 seconds, much faster than the Ethereum mainnet. Although 2 seconds is still too slow for high-frequency trading, combined with an off-chain matching engine, it is sufficient to meet settlement needs.

3.2 Asset Layer: Gnosis Conditional Token Framework (CTF)

This is the core engine of Polymarket, a set of smart contract codes running on the blockchain. The Gnosis CTF framework addresses the most challenging "path dependency" and "combinatorial prediction" issues in prediction markets.

3.2.1 Conditions and Their Combinations

In the simplest binary market, the CTF handles Condition A (for example, Trump winning). However, in more complex markets, the CTF demonstrates its powerful logical nesting capabilities.

For example, we can create a composite market: "If interest rates are cut in 2025 (Condition A) and the S&P 500 rises (Condition B)." The CTF allows the Outcome Token of Condition A to be used as collateral to further split into tokens based on Condition B. This is like a Russian nesting doll, with layers nested within each other. This architecture enables Polymarket to support extremely complex derivatives trading in the future, although it currently mainly focuses on simple binary markets for the general public.

3.2.2 Technical Advantages of ERC-1155

As mentioned earlier, the CTF uses the ERC-1155 standard. In terms of technical implementation, this means there is a ledger in the smart contract with a Mapping(ID => Balance). The ID is a unique identifier calculated through a hash algorithm (Keccak256), containing information such as the question ID and outcome index (Yes/No).

This structure allows for "batch transfers." If a market maker needs to adjust positions in 100 different markets simultaneously, they can complete all operations in a single transaction, greatly saving on gas fees and reducing the risk of on-chain congestion.

3.3 Oracle Layer: UMA's Game Theory Design

All prediction markets face the same ultimate question: who decides the outcome?

If the results are input by Polymarket officials, it becomes a centralized bookmaker, with risks of malfeasance or running away. Polymarket introduces the UMA (Universal Market Access) optimistic oracle mechanism, using a clever game theory model to solve the problem of decentralized trust.

The design of UMA is based on the assumption that most people are honest most of the time, especially when honesty can earn money.

Under the UMA mechanism, the confirmation process for market results is as follows:

Proposal: After the event ends, anyone (usually an incentivized bot) can propose a result (for example, "Yes").

Challenge Window: After the proposal is made, it enters a public notice period of about 2 hours. During this time, if no one raises an objection, the system defaults (optimistically assumes) that this result is correct and settles based on it.

Dispute: If someone believes the proposal is wrong (for example, if No actually won but someone proposed Yes), they can stake a sum of money to initiate a challenge.

DVM Ruling: Once a challenge occurs, the dispute escalates to UMA's highest court—the DVM. At this point, all UMA token holders will vote.

Schelling Point Mechanism: Voters not only vote based on facts but also to maintain the system's credibility. If the UMA system is proven to be manipulable, UMA tokens will become worthless. Therefore, to protect the value of their assets, rational token holders will tend to vote in accordance with objective facts.

Rewards and Penalties: Those who vote correctly share the staked funds of those who vote incorrectly.

This mechanism ensures that as long as the cost of malfeasance (bribing 51% of token holders across the network) is higher than the benefits of malfeasance, the results will be credible. For Polymarket users, this means their funds' safety does not rely on the company's conscience but on mathematical and economic game theory.

4. Finally, Super Cycle and Regulation

The "super cycle" proposed by Robinhood CEO Vlad Tenev is not unfounded. With the involvement of AI, prediction markets are undergoing a qualitative change.

The main participants in future prediction markets may not be humans but AI agents.

Imagine thousands of AI entities monitoring global news, weather, earnings reports, and social media sentiment 24/7. Once they detect a slight change in the probability of a certain event occurring, the AI will immediately trade on Polymarket.

This will lead to two outcomes:

Extreme market efficiency: The prices in prediction markets will become the fastest and most accurate channels for humanity to obtain information, even faster than news media.

Exponential liquidity explosion: Trading volume will no longer be limited by human schedules and attention but will be driven by endless algorithmic games.

However, the regulatory environment will be a key variable determining the industry's landscape: if regulators deem prediction markets equivalent to gambling, the compliance pressure on Polymarket will increase significantly. Conversely, if it is recognized as a new type of "information derivative," it will become one of the infrastructures of the global financial market.

The rise of Polymarket is not just a success of a cryptocurrency application; it represents a deeper social transformation: the assetization of information. By encapsulating the "future" in code and transforming "judgment" into "trading," Polymarket is building a decentralized truth machine.

For ordinary users, they can all try to understand how this machine operates. Because it is changing the way we perceive the world—from listening to what experts say to watching how the market moves. In this new world, money is no longer just a symbol of purchasing power; it has become a measure of honesty.

Attached is the glossary of technical terms.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。