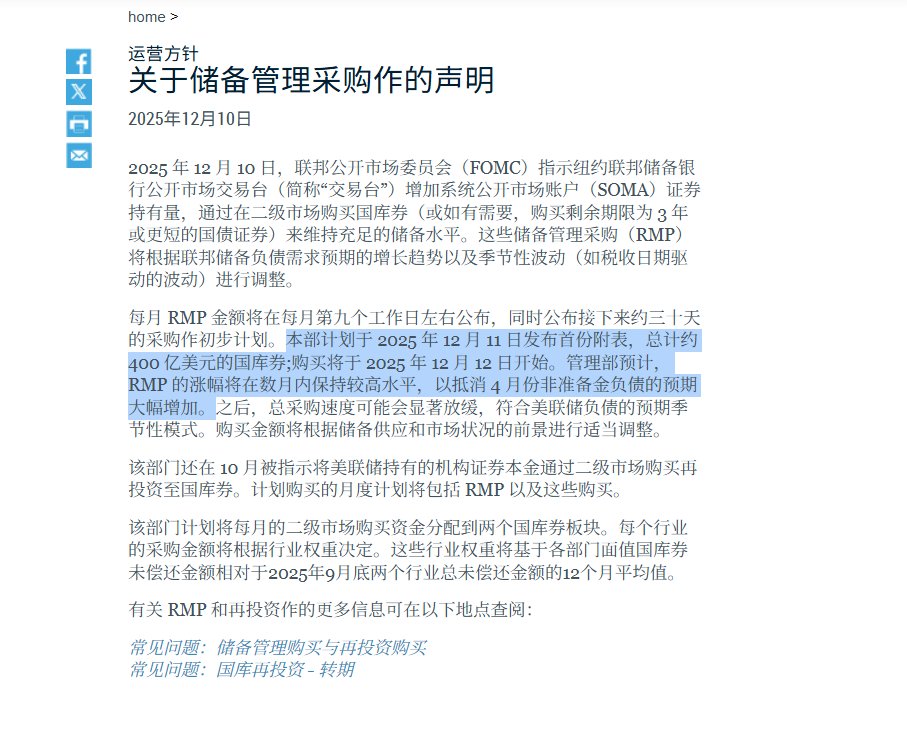

The Federal Reserve is also preparing to buy $40 billion in government bonds by the end of the year. Some may think this is an expansion of the balance sheet, but it actually is not.

First of all, this $40 billion falls under RMP (Reserve Management Purchases), and its purpose is not to stimulate the economy or actively inject liquidity, but rather to maintain the minimum reserve safety threshold of the banking system. It is to prevent the banking system from being stripped too much by factors such as the Treasury's fund scheduling, tax payments, and year-end corporate settlements.

Let me briefly explain the differences between RMP, QE, and QT:

QE = Actively expanding the balance sheet, aimed at lowering long-term interest rates and increasing system liquidity. This is commonly referred to as injecting liquidity.

QT = Actively shrinking the balance sheet, aimed at withdrawing liquidity and tightening financial conditions.

RMP = Completely different from QE; it is about maintaining the water level and avoiding systemic water shortages.

The essence of RMP is that the Federal Reserve is replenishing the water that has fallen out, not adding more water to the pool.

So this is not an expansion of the balance sheet. Additionally, the $40 billion in government bond purchases also includes reinvestment, meaning that after MBS matures, it will be used to purchase U.S. Treasuries. This part does not increase the size of the balance sheet; it is merely an adjustment of the asset structure.

More importantly, the Federal Reserve clearly stated two points in its announcement: RMP will maintain a high pace until April 2026 (because the Treasury will significantly increase non-reserve liabilities in April), but after April, as seasonal factors disappear, the purchase scale will quickly decline.

What truly determines liquidity is not RMP, but whether SLR is relaxed, whether banks can expand their balance sheets, whether the Treasury continues to replenish reserves, and whether the Federal Reserve will reduce the scale of ON RRP.

Bitget VIP, lower fees, better benefits

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。