Article | Sleepy.txt

Editor | Kaori

On October 28, Trump Media & Technology Group announced the launch of a prediction market product called "Truth Predict" on its social platform Truth Social. The company's CEO stated that this platform aims to encourage more people to participate in information judgment or prediction, allowing individuals not just to voice their opinions but to validate their judgments through betting.

This marks the Trump family's third significant move in the prediction market sector.

As early as January 2025, Donald Trump Jr. joined the regulated prediction platform Kalshi as a strategic advisor.

In August of the same year, his venture capital firm 1789 Capital led a new round of financing for Kalshi's main competitor, the crypto prediction market Polymarket. The latter is a platform that has received investment from ICE, the parent company of the New York Stock Exchange, and was valued at up to $9 billion. Following the completion of the transaction, Donald Trump Jr. also joined its advisory board.

A family occupying key positions in three core companies within the same sector is considered an unconventional operation in traditional venture capital logic.

Chris Perkins, managing partner at CoinFund, stated, "From a venture capital perspective, we generally do not invest in competing projects; we want to bet on the ultimate winner."

The Trump family clearly does not care about these conventional logics; what they seek is not victory, but certainty.

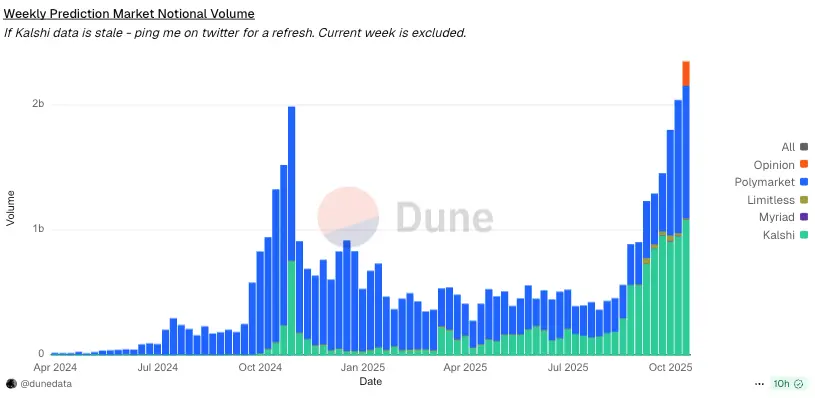

The prediction market is at a critical point of explosion. According to a research report by investment management firm Certuity, the industry is expected to reach a scale of $95.5 billion by 2035, with a compound annual growth rate of 46.8%, while Polymarket and Kalshi currently control over 96% of the market share.

Market share of mainstream prediction market platforms | Source: Dune

The allure of this new sector lies in its ability to price "information" itself for the first time, allowing it to be freely bought and sold in the market. During the 2024 U.S. presidential election, such platforms were even praised by several media outlets as being more sensitive and possessing greater potential as a "truth engine" than traditional polls.

In prediction markets, prices are not statistical figures but results formed by thousands of people betting real money, reflecting people's judgments on the direction of events more accurately than surveys.

However, when power and information begin to be controlled by the same group of people, this market, which prides itself on "collective wisdom," may aggregate not the truth, but a carefully crafted illusion.

Carnival in a Regulatory Vacuum

The story of Polymarket is key to understanding the entire prediction market industry. In 2022, this platform, which was gaining momentum, was deemed by the U.S. Commodity Futures Trading Commission (CFTC) as an "unregistered derivatives trading market," fined $1.4 million, and ordered to cease services to U.S. users.

Days later, Polymarket announced a geographic blockade, officially withdrawing from the U.S. market.

In November 2024, just before the U.S. elections, a team of federal agents knocked on the apartment door of Polymarket CEO Shayne Coplan in Brooklyn, confiscating his computer and phone.

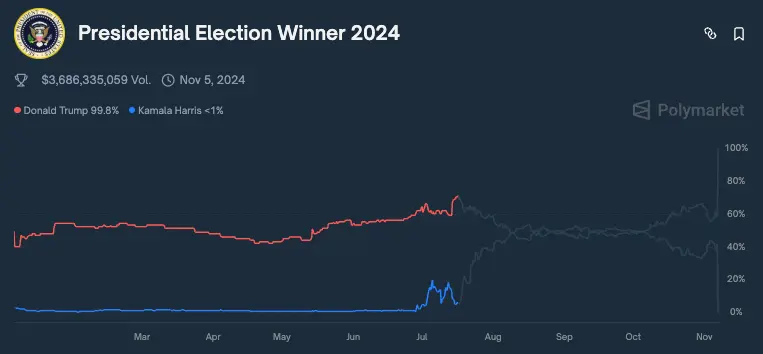

The focus of the investigation was whether the company violated the settlement agreement from the previous year by still accepting bets from U.S. users in secret. At that time, the trading volume related to the "2024 Presidential Election" on Polymarket had already exceeded $3.6 billion—this was the largest bet in the platform's history.

Over $3.6 billion wagered on the 2024 U.S. presidential election on Polymarket | Source: Polymarket

On January 20, 2025, Trump was sworn in, returning to the White House. Six months later, the U.S. Department of Justice announced the end of its investigation into Polymarket, neither filing any charges nor releasing results.

Now, Polymarket is preparing to return to the U.S. market at the end of November, focusing on sports betting.

From the raid to the investigation's dismissal, only seven months passed, and the entire situation flipped completely around Trump's return to the White House. Crypto entrepreneur Zach Hamilton put it more directly: "If you want to explain why prediction markets can re-enter the U.S., you only need one name—Donald Trump."

Almost simultaneously, Donald Trump Jr.'s personal trajectory also overlapped with this turning point.

On January 20, the day his father returned to the White House, he announced his joining of the regulated prediction platform Kalshi as a strategic advisor. In August, just as the Department of Justice's investigation was settling, his firm 1789 Capital led a new round of financing for Polymarket, and he himself subsequently joined the advisory board.

Behind this carnival is the regulators' helplessness.

The CFTC is a federal agency that has been established for nearly fifty years, initially responsible for regulating commodities futures like corn and beef. Now, it has to face the rapidly expanding crypto derivatives and prediction markets simultaneously. This agency has an annual budget of less than $400 million and fewer than 700 employees. In contrast, the SEC, which oversees the securities market, has a budget of $2 billion and over 4,000 employees.

A former CFTC official, speaking anonymously, admitted that they are almost powerless to cope with all of this, saying, "We simply do not have the capacity to regulate cryptocurrency or sports betting, let alone the combination of the two. The CFTC will be overwhelmed, and you will see more and more insider trading appearing in prediction markets because we have no ability to monitor it; we can only rely on whistleblowers and self-reports."

Regulation relying on whistleblowers and self-reports is essentially no regulation at all.

Is Insider Information Considered Prediction?

The regulatory vacuum has turned prediction markets into a hunting ground where information advantages can be directly monetized.

On October 10, the day the Nobel Peace Prize was announced, a sudden insider trading controversy erupted on Polymarket that caught global attention.

As early as three months prior, the platform had opened a prediction market for "2025 Nobel Peace Prize Winner," attracting over $20 million in trading volume. Popular candidates included Russian opposition leader Alexei Navalny's widow, U.S. President Trump, environmental activist Greta Thunberg, and WikiLeaks founder Julian Assange.

In contrast, the odds for Maria Corina Machado, the leader of Venezuela's opposition party, hovered between 3% and 5%, with almost no one betting on her.

However, just hours before the results were announced, Machado's odds suddenly skyrocketed from the low position that no one favored to over 70%. Data showed that at least three accounts placed large bets during the same period, with individual account bets exceeding tens of thousands of dollars. The precision of these trades was astonishing.

The Nobel Committee's final decision is usually finalized only a few hours before the award is announced, with very few insiders. Yet these accounts were able to place large bets hours in advance, and their odds curve almost perfectly predicted the final outcome.

Whether insider trading should be allowed in prediction markets has been a focal point of debate in the industry.

Robin Hanson, an economist at George Mason University and an early advocate of prediction markets, believes that insider trading can actually improve market accuracy because information is aggregated into prices more quickly. "If the goal of prediction markets is to obtain accurate information, then you certainly want to allow insider trading."

This viewpoint sounds self-consistent but overlooks a more fundamental premise: when information advantages are overly concentrated in the hands of a few, and insider trading becomes the norm, ordinary traders will be quickly squeezed out of the market.

Without retail investors providing liquidity, the market will ultimately shrink, becoming a place where a few insiders compete against each other. Such a market is neither accurate nor fair, as it loses the foundation of "collective wisdom."

The regulatory vacuum makes this debate seem somewhat hollow.

Under the current system, the SEC's insider trading regulations do not apply to prediction markets because the targets of these trades are "events" rather than "securities." Meanwhile, the other regulatory body, the CFTC, has yet to establish a clear prohibition against insider trading.

The original intention of prediction markets was to use prices to measure the likelihood of future events. But now, it resembles more of an information game, where whoever holds more insider information can turn the future into profit in advance.

$500,000 Entry Fee

If information can be priced, then in Donald Trump Jr.'s new business, power has a more direct price tag.

In April 2025, Donald Trump Jr. and his venture capital firm 1789 Capital established a private membership club called Executive Branch in Georgetown, Washington, D.C. The entry fee is $500,000, with an annual fee of $25,000. Even so, less than two months after its establishment, a waiting list had already formed.

The founding member list of this club could almost serve as a condensed power structure diagram.

David Sacks, the "crypto czar" of the White House, the founders of the crypto trading platform Gemini, the Winklevoss twins, and tech investor Chamath Palihapitiya are all included.

More notably, a collective appearance of high-ranking government officials was observed.

At the launch party of Executive Branch, at least six cabinet-level officials from the Trump administration were present, including Secretary of State Marco Rubio, Attorney General Pam Bondi, SEC Chairman Paul Atkins, FTC Chairman Andrew Ferguson, FCC Chairman Brendan Carr, and Director of National Intelligence Tulsi Gabbard.

In addition, FBI Deputy Director Dan Bongino was also present, raising a toast alongside several CEOs and founders from Silicon Valley.

Party scene | Source: Axios

An insider from the club later revealed in an interview that they deliberately refused media and lobbyists' entry, hoping to create an "absolutely private" environment where people could converse without reservations.

The value of this so-called "private conversation" lies precisely in its ability to systematically bypass the existing political oversight framework.

According to the U.S. Lobbying Disclosure Act, lobbying activities must publicly record the subjects, issues, and expenditures involved, but the closed-door meetings of the Executive Branch club are clearly outside the scope of disclosure. Similarly, it is not bound by the Federal Advisory Committee Act.

In other words, that $500,000 entry fee is not just an ordinary ticket; it is a pass that can directly access the core of power, bypassing institutional scrutiny.

This model inevitably evokes memories of the Trump International Hotel in Washington during Trump's first presidential term.

That golden-facade building almost became a transit point for power.

Government officials, Republican lawmakers, foreign dignitaries, and business leaders frequently came and went, with the exchanges over drinks often proving more effective than meetings. An investigation by The Washington Post revealed that during Trump's presidency, officials from at least 22 foreign governments stayed at that hotel, leading to accusations against Trump of violating the "Emoluments Clause" in the U.S. Constitution.

However, unlike that hotel, the Executive Branch club is more secretive, more expensive, and more exclusive. After all, the Trump hotel was a semi-public commercial venue, where guests' comings and goings could still be captured by the media. In the Executive Branch, all meetings, conversations, and transactions occur under the protection of "privacy."

When 1789 Capital is both an investor in Polymarket and Donald Trump Jr. serves as the founder of this club and an advisor to Polymarket, a closed-loop interest network begins to take shape.

More subtly, the membership list of this club includes regulators such as the SEC chairman and the Attorney General, as well as investors and executives from the prediction market. When regulators and the regulated, investors and the invested, sit at the same table, the so-called "boundaries" become impossible to discuss.

Jeff Hauser, executive director of the Revolving Door Project, an organization that specifically monitors the appointments and behaviors of U.S. executive branch officials, publicly expressed skepticism about this.

He pointed out that Polymarket itself is already a politically controversial entity, and the dual identity of the Trump family can influence regulatory direction while potentially benefiting from regulatory loosening, blurring the lines between power and capital. This overlapping relationship is a typical and should be strictly avoided "conflict of interest."

In response to external doubts, White House Press Secretary Karoline Leavitt stated that the president and his family "have never and will never engage in any conflict of interest."

A Future No Longer Unknown

The theoretical foundation of prediction markets can be traced back to the "knowledge dispersion" theory proposed by Nobel laureate Friedrich Hayek.

Hayek believed that prices are not only the result of transactions but also a social signal that can aggregate fragmented and localized knowledge dispersed among countless individuals into a cohesive information system.

Prediction markets are an extension of this idea, attempting to condense the judgments and beliefs dispersed among the crowd into a probability expressed by price by allowing people to bet real money on the future.

However, there is a commonly overlooked premise in Hayek's theory. The market can aggregate knowledge because information is relatively dispersed among participants.

When a few individuals hold overwhelming information advantages, prices no longer represent collective wisdom but merely reflect the flow of power and resources. At that point, the market degenerates from an aggregator of knowledge into a tool for wealth transfer.

The precise bets placed just before the Nobel Prize announcement did not prove the market's efficiency; rather, they served as a reminder that the so-called market rationality is sometimes just an illusion of information controlled by a few.

The core promise of prediction markets is to turn an uncertain future into a tradable asset. This promise is based on a fundamental assumption: the future is unknown, and all participants are guessing the future direction using their localized information.

But for those who truly hold power, the future is largely not unknown. For them, the so-called "prediction" has never been about "guessing the unknown future."

When the Attorney General can decide whether to prosecute Polymarket, and the SEC chairman can redefine the regulatory boundaries of the entire industry, while family members of these decision-makers are deeply involved and directly hold investment interests in this market, what they are trading is no longer an uncertain future but the "certainty" defined by their own power.

The launch of Truth Predict pushes this logic to its extreme. When the operators of the platform, and their family members, have the ability to influence the outcomes of these events, the term "prediction" loses its meaning; it no longer points to the uncertainty of the future but merely to the pre-pricing of outcomes by power.

From left to right: Vivek Ramaswamy, Ohio Senator Bernie Moreno (Republican), Omid Malik, Vice President J.D. Vance, and Donald Trump Jr. | Source: POLITICO

Blockchain technology allows all transactions to be recorded on a public ledger, seemingly enabling everyone to trace the origins of each bet. However, this transparency only extends to the visibility of wallet addresses, not the identities of the operators behind them.

No one knows who placed precise bets on Polymarket just hours before the Nobel Prize announcement, nor who made accurate trades on HyperLiquid before policy releases.

In the future, when the same logic is replicated on Truth Predict, and a platform directly or indirectly led by the presidential family allows people to bet on elections, interest rates, and wars, the transparency of transactions becomes less important. What truly matters is who can know the outcomes in advance and even make the results occur according to their own will.

And these answers likely exist only in the corner of the Executive Branch club, guarded by "privacy."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。