Systematic Review of the Background, Style, and Representative Tokens of Seven Leading Market Makers

Introduction

The sharp decline on October 11 taught the market a clear lesson: prices are not simply pierced by a "single sell order," but are consumed by a vacuum of liquidity. As several market makers paused their operations to reduce risk exposure, traders lost their counterparties, exacerbating margin calls and deleveraging, which led to a rapid and amplified price drop, becoming a significant accelerator of the "waterfall" crash. In the crypto market, token prices are not merely generated by the natural collision of buy and sell orders, but are supported by the continuous quotes and depth provided by market makers. Market makers are not only the lubricants of trading but also the central nervous system of price discovery. Once this "invisible hand" withdraws, the market loses its gravitational balance. So, how does this invisible hand stabilize price discovery, and why does it "absent" during extreme moments, thereby altering the path and speed of market trends?

This article will use simple language to break down the role and profit model of market makers in the crypto world, systematically reviewing the background, style, and representative tokens of seven leading market makers, the controversies they face, and suggestions for rebuilding trust, opening the black box of market-making mechanisms for readers to better understand "market-making behavior."

Understanding the Functions and Roles of Market Makers

Market makers serve as both price stabilizers and risk buffers for the system. When they operate efficiently, the market is stable, deep, and has low slippage; when they are absent or malfunctioning, the entire system can become unbalanced in an instant.

1. Functions and Roles of Market Makers

Market Makers (MM) are the "invisible hand" of the crypto market, performing important functions:

Continuous two-sided quoting and depth maintenance: Continuously posting buy/sell prices in CEX order books, DEX RFQs, and AMM pools, dynamically adjusting spreads and order sizes based on flow and risk thresholds, maintaining 1%/2% depth and replenishment speed, reducing slippage and impact costs (including AMM position rebalancing and concentrated liquidity range management).

Price discovery and cross-scenario linkage: Quickly aligning dispersed market prices through arbitrage trading across exchanges, chains, futures, and stablecoins/anchored assets; connecting ETF/ETP/RFQ networks to promote OTC-on-chain and on-chain-off-chain linkages and basis repair.

Inventory management and risk underwriting: Absorbing short-term buy/sell imbalances and "packaging" dispersed trading demands; using perpetuals/futures/options/borrowing tools to neutralize inventory and bring funding rates and futures basis back to normal ranges.

New product launches and cold-start liquidity: Providing minimum depth and market-making quotas at TGE/new product launches, using token lending/inventory pledging and market-making rebate agreements to smooth opening volatility; accommodating institutional/whale large orders, reducing explicit spreads and implicit impact costs, helping assets quickly enter a "tradable state."

It is evident that the social attribute of market makers lies between public goods and competitive games. On one hand, they enhance market efficiency with capital, algorithms, and expertise, allowing everyone to trade at reasonable costs; on the other hand, they possess significant structural information and decision-making power, which can turn them from "market stabilizers" into "volatility amplifiers" if incentives misalign or risk controls fail.

2. Main Types of Market Makers

Market makers of different sizes, strategies, and positions play different roles in the crypto market. The following are the three main types:

Professional Market Makers: These market makers use advanced algorithms and high-speed matching to fill order book liquidity, narrow spreads, and improve trading execution experiences. They typically have large capital, algorithm-driven operations, cross-scenario coverage (CEX, DEX, OTC, ETF/ETP), and mature risk control systems. They often provide continuous quotes and depth for mainstream assets (such as BTC, ETH, SOL) and deploy market-making algorithms and hedging mechanisms across multiple exchanges/chains.

Advisory/Project Market Makers: These market makers enter the market in the form of "new product support + liquidity packages," usually signing market-making agreements with project parties to provide token lending, initial orders, and rebate incentives. Once a project is launched, they are responsible for early quotes and matching to maintain a minimum tradable state. Although these institutions may not have the capital scale of large professional market makers, they are more active in "new coin cold starts vs. long-tail tokens." Market-making contracts often include terms for "token lending," "market-making rebates," and "minimum liquidity guarantees."

Algorithmic Market Makers or AMM LPs: This includes liquidity providers (LPs) in AMM models, some algorithmic and low-human-intervention quoting systems, as well as small market-making institutions or bot services. These participants typically have small to medium capital scales and mainly participate in on-chain AMM pools or customized matching agreements; their risk control and hedging capabilities may be weaker than those of professional market makers, making them prone to liquidity withdrawal or depth shrinkage during extreme market conditions; they are more fragmented in the market, providing "thin liquidity" support for long-tail tokens or multi-chain protocols.

3. Market Making Mechanisms and Profit Models

Although outsiders often imagine market makers as "the house within the system," in reality, their profit model resembles a "high-frequency fee factory," accumulating profits through small but stable spreads.

Spread Capture: This is the foundation of all market-making activities. Market makers maintain stable two-sided quotes between the bid and ask prices, and when market transactions occur, they profit from the difference between the buy and sell prices. For example, if BTC is quoted at $64,000 for buying and $64,010 for selling, when a user sells at the asking price, the market maker earns a $10 spread profit. Although the profit per transaction is small, at a transaction frequency in the millions, the annualized returns can be substantial.

Fee Rebates and Incentives: Most exchanges adopt a maker-taker fee structure: the maker enjoys lower fees or rebates for providing liquidity, while the taker pays higher fees. Market makers can maintain positive rebate income over the long term due to their large transaction volumes and algorithmic automation capabilities. Additionally, exchanges or project parties often provide extra market-making incentives, such as returning a certain percentage of fees, distributing token incentives, or establishing market-making subsidy pools in the early stages.

Hedging and Basis Trading: The inventory held by market makers inevitably bears the risk of price fluctuations. To maintain a "neutral position," they hedge through perpetual contracts, futures, options, or borrowing. For instance, when they hold too much ETH in inventory, they may short an equivalent amount of ETH in the futures market to lock in risk exposure. Meanwhile, if there is a discrepancy between spot and futures prices (i.e., basis), market makers may also engage in arbitrage by "buying low and selling high" to earn risk-free profits.

Statistical Arbitrage and Structured Opportunities: In addition to conventional spread profits, market makers also seek various micro-structural opportunities:

Inter-period arbitrage: Price differences between different contract expirations for the same asset;

Cross-asset arbitrage: Price deviations between correlated assets (e.g., stETH and ETH);

Volatility arbitrage: Utilizing differences between implied volatility from options and historical volatility;

Funding rate arbitrage: Balancing funding costs across different markets through borrowing or hedging.

These strategies collectively form the "profit matrix" of market makers. They do not bet on direction like speculators but rely on scale, speed, risk control, and algorithms to win. In a market with daily trading volumes exceeding $10 billion, even an average spread of just 0.02% is sufficient to support a massive profit system.

Review of Mainstream Market Makers

The existence of market makers has transformed the crypto market from "disorderly quoting" to a "sustainable matching" system. The most mainstream market makers currently include Jump Trading, Wintermute, B2C2, GSR, DWF Labs, Amber Group, and Flow Traders. This chapter will analyze the background, style, scale, and token holding structures of these market makers.

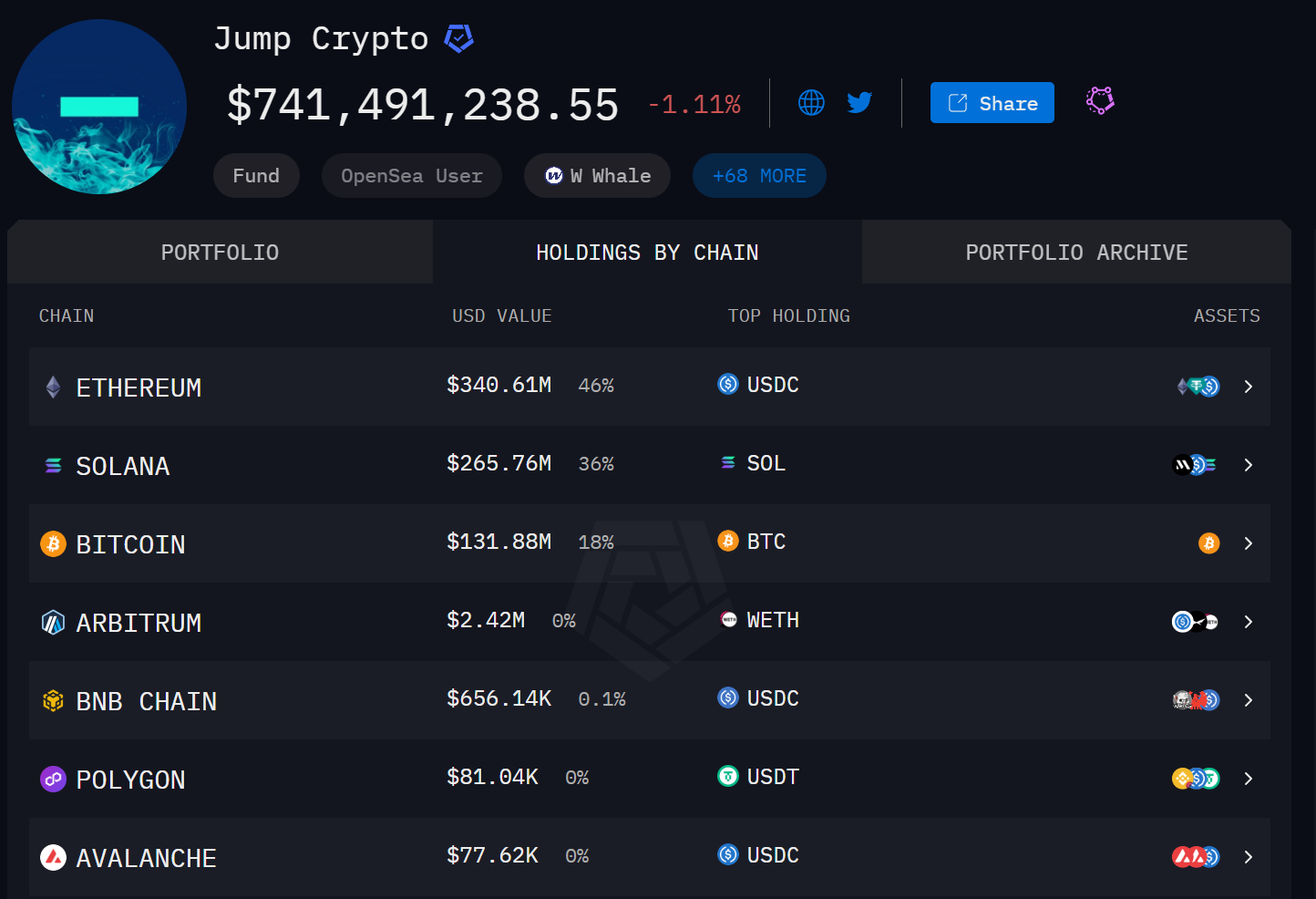

1. Jump Trading

Source: Jump Trading

Overview: A traditional high-frequency quant firm, involved in market making and research infrastructure. According to Arkham data, as of October 23, 2025, Jump Trading's holdings amount to approximately $740 million.

Market Making Style: The portfolio leans towards "capital management + low to medium beta positions": a high proportion of stablecoins and staking derivatives; dynamically adjusting staking/re-staking positions and conducting large redemptions and exchanges during significant market fluctuations.

Representative Holding Tokens:

Top five holding assets: SOL, BTC, USDC, USDT, ETH

Notable holding assets: USD1, WLFI, W, SHIB, JUP, etc.

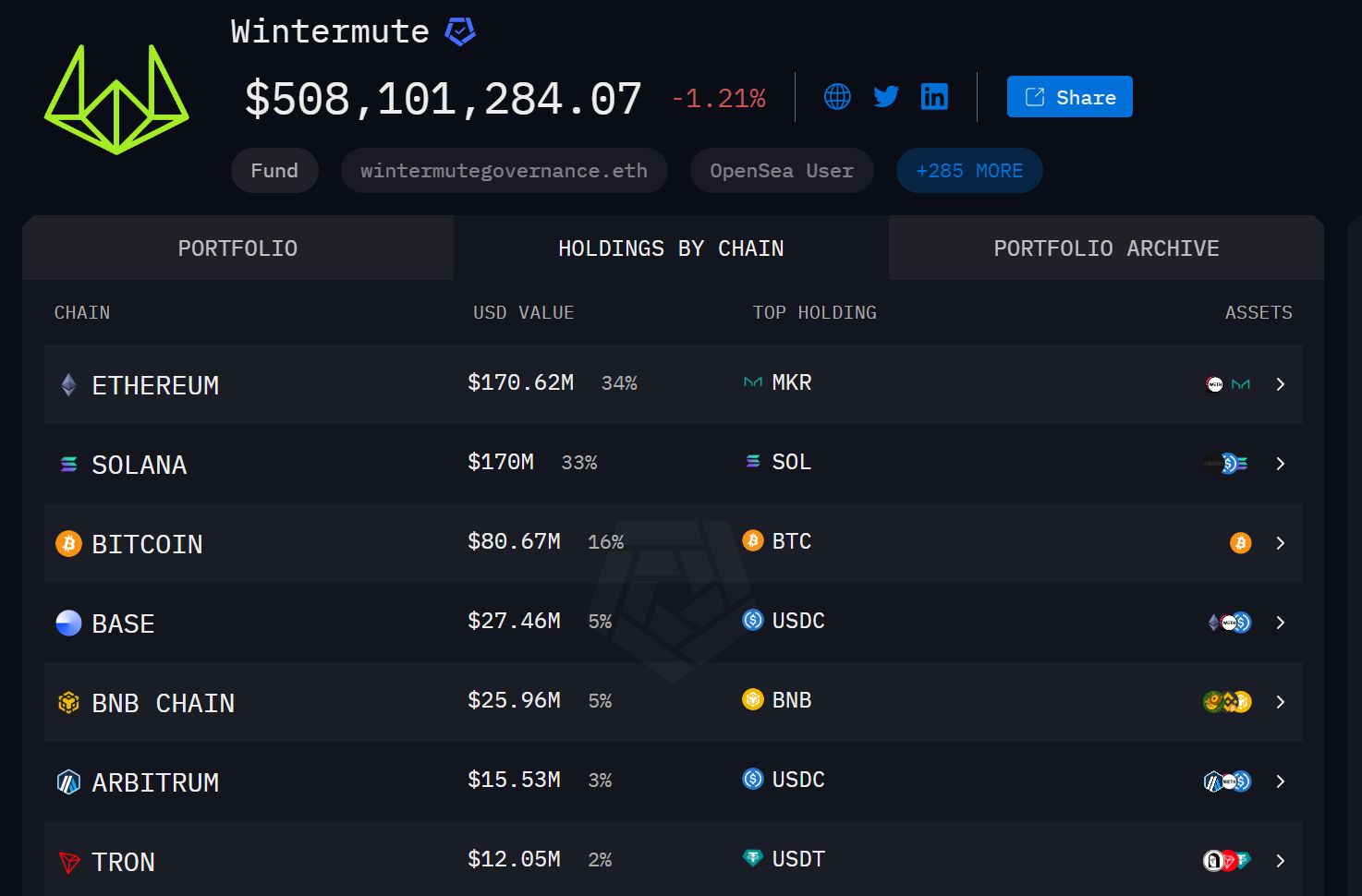

2. Wintermute

Source: Wintermute

Overview: An established quantitative market maker covering both centralized and decentralized scenarios; active in the hot new coin and meme sectors in recent years, providing liquidity for multiple project launches. According to Arkham data, as of October 23, 2025, Wintermute's holdings amount to approximately $500 million.

Market Making Style: Cross-market and cross-asset market making + event-driven (new coins/TGE) + high-frequency and grid strategies combined; typically allocated or accept loans to provide two-sided quotes during the cold start phase of new assets. Previously disclosed as one of the market makers for Ethena (ENA).

Representative Holding Tokens:

Top five holding assets: SOL, BTC, USDC, MKR, RSTETH

Notable holding assets: LINK, ENA, PENGU, FARTCOIN, Binance Life, etc.

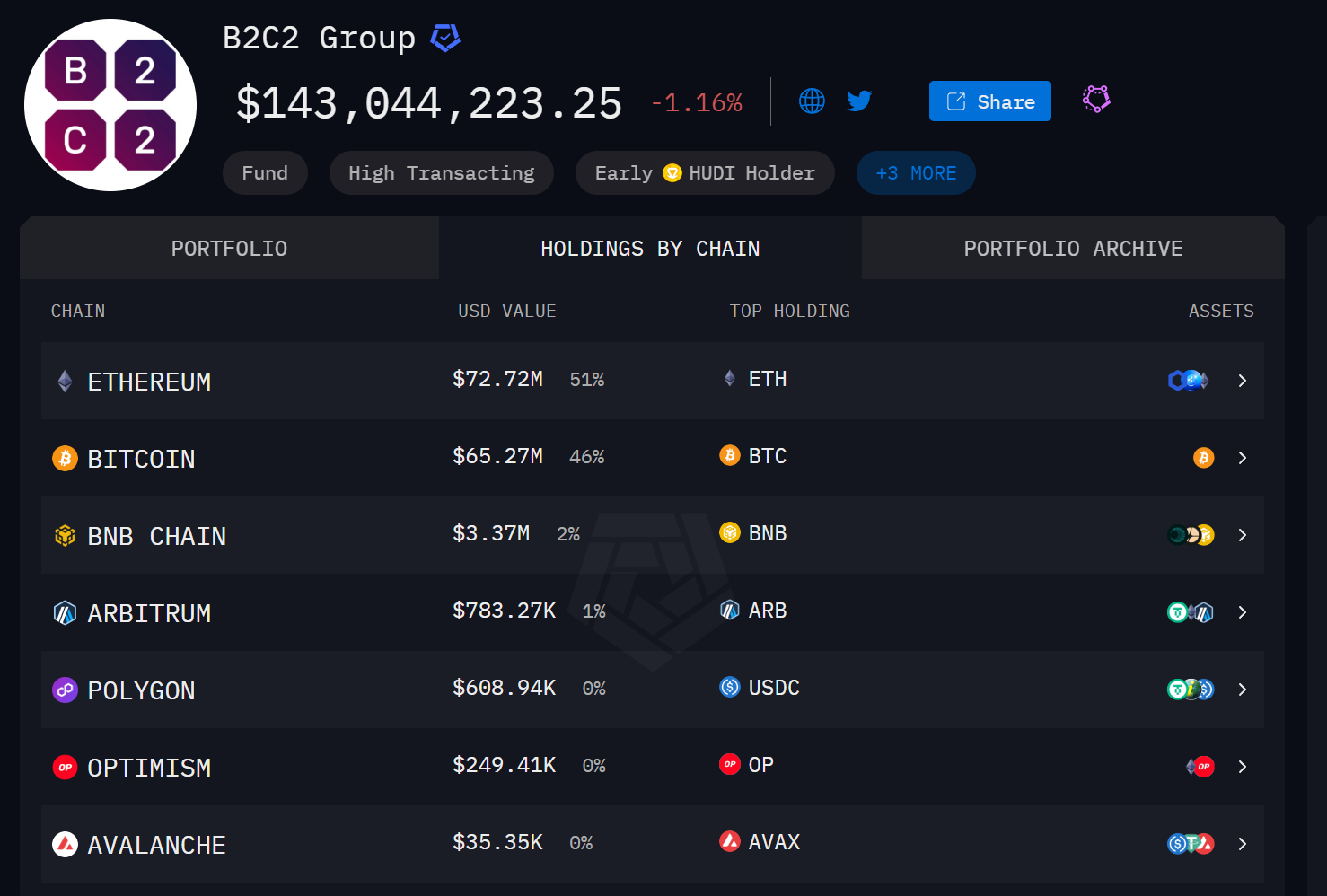

3. B2C2

Source: B2C2

Overview: A well-established institutional market maker and OTC liquidity provider, controlled by the Japanese financial group SBI; deeply collaborates with several large trading platforms and compliant scenarios. According to Arkham data, as of October 23, 2025, the holding scale is approximately $140 million.

Market Making Style: Clearly characterized by "institutional prime brokerage + liquidity outsourcing"; provides stable coverage for both mainstream and long-tail high-liquidity tokens, with market commentary disclosing transaction volumes and buy/sell directions by token.

Representative Holding Tokens:

Top five holding assets: BTC, ETH, RLUSD, LINK, AAVE

Notable holding assets: LINK, BNB, UNI, FDUSD, ASTER, etc.

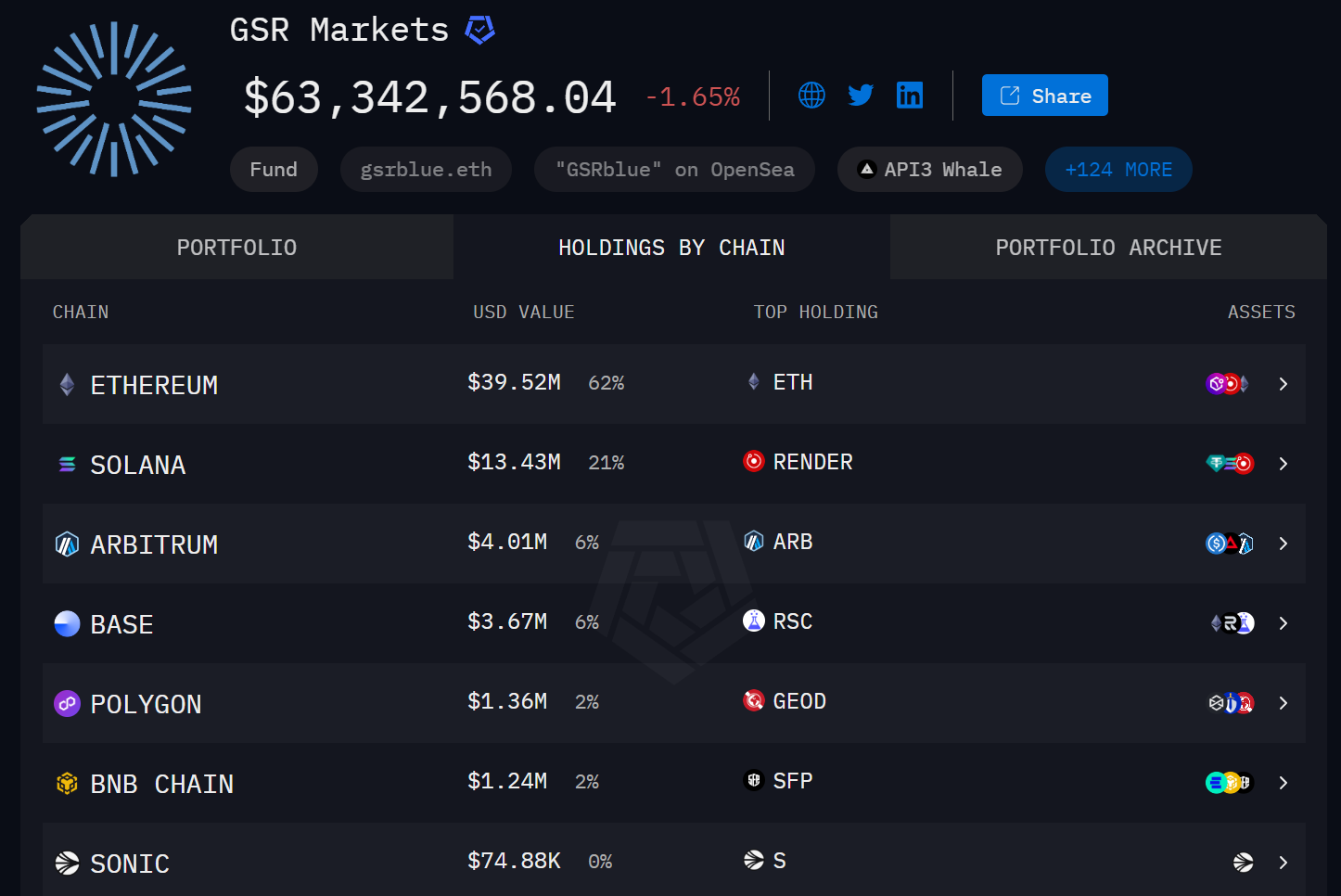

4. GSR Markets

Source: GSR Markets

Overview: Established in 2013, with comprehensive compliance qualifications (including a Singapore license), it is one of the earliest professional crypto market makers. According to Arkham data, as of October 23, 2025, the holding scale is approximately $60 million.

Market Making Style: "Institutional temperament + full-stack trading"—simultaneously engaging in market making, structured products, and programmatic execution; often acts as the official market maker for projects, participating in liquidity management during TGE/circulation periods.

Representative Holding Tokens:

Top five holding assets: ETH, RNDR, ARB, SOL, SXT

Notable holding assets: AAVE, FET, RSC, SKY, SHIB, etc.

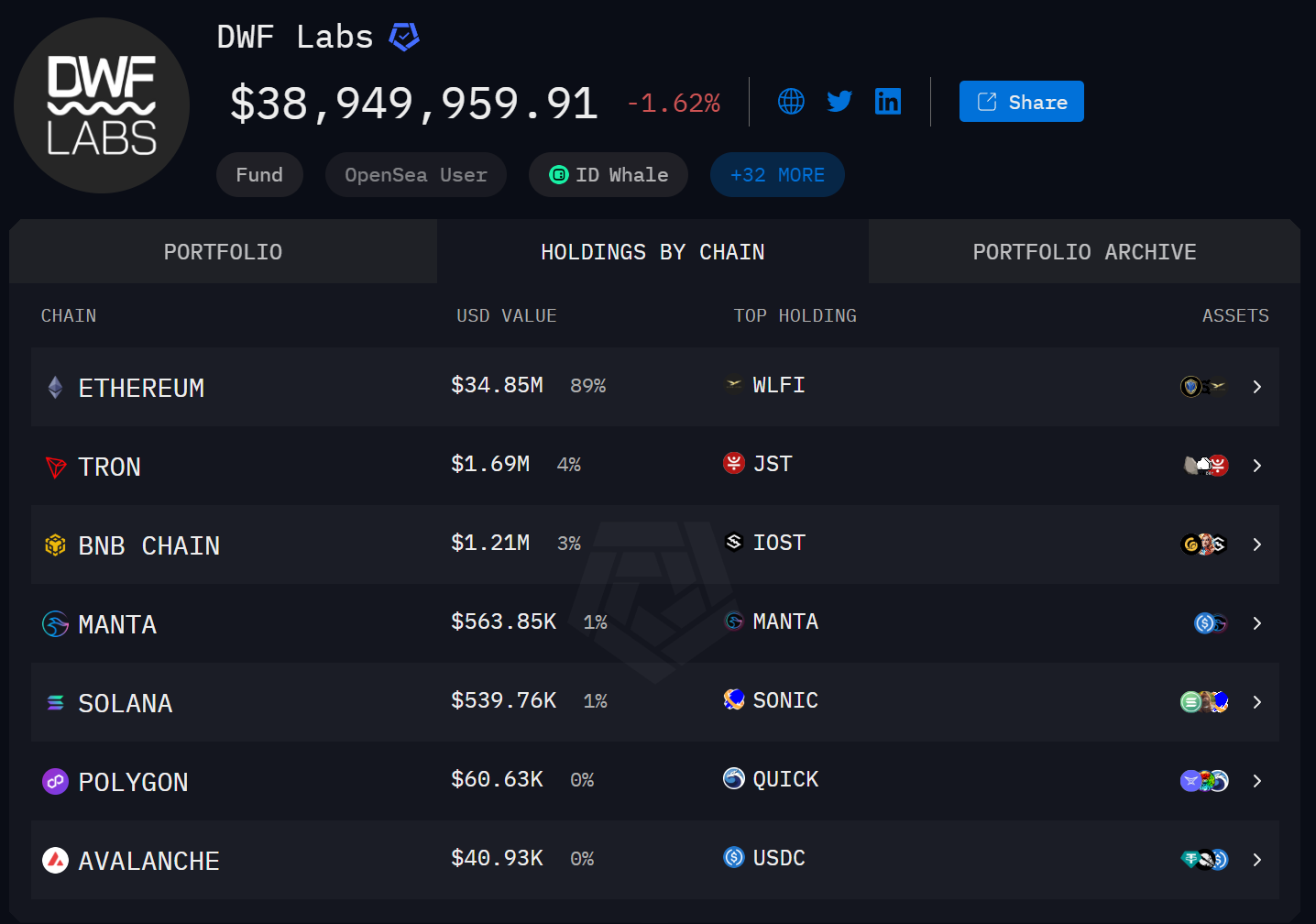

5. DWF Labs

Source: DWF Labs

Overview: Driven by a dual engine of "investment + market making," frequently active with a wide coverage of tokens. According to Arkham data, as of October 23, 2025, DWF Labs' holding scale is approximately $40 million.

Market Making Style: Parallel strategies of new asset cold starts + secondary market making, adept at utilizing broad coverage across exchanges and multi-chain scenarios for spread and inventory management; balanced portfolio style of "Beta + long-tail."

Representative Holding Tokens:

Top five holding assets: WLFI, JST, FXS, YGG, GALA

Notable holding assets: SONIC, JST, PEPE, SIREN, AUCTION, etc.

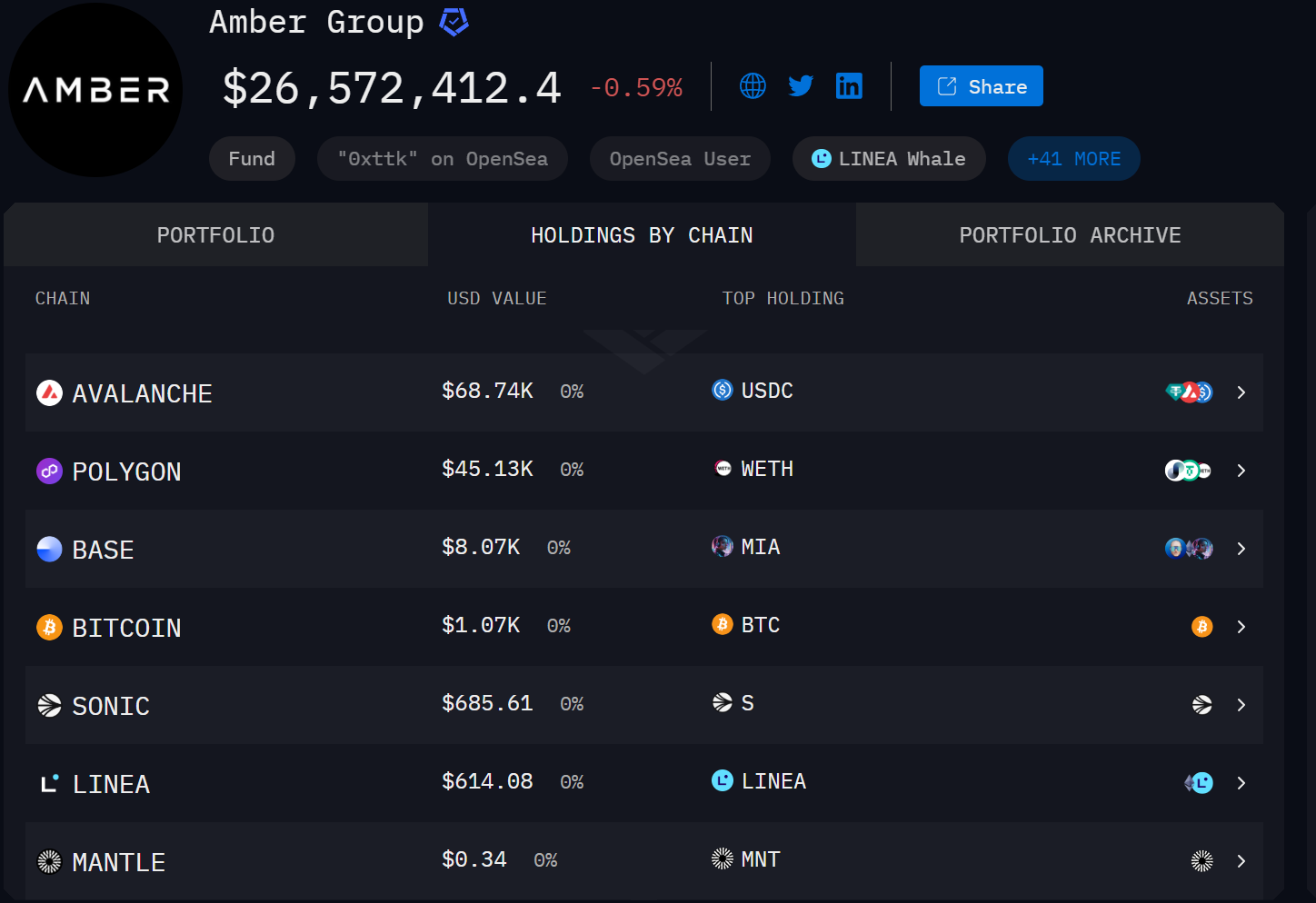

6. Amber Group

Source: Amber Group

Overview: A full-stack trading and liquidity provision institution originating in Asia with a global layout; offers market making, derivatives, and custody/infrastructure services. According to Arkham data, as of October 23, 2025, the holding scale is approximately $26 million.

Market Making Style: Primarily focused on "institutional market making + project cold starts," supplemented by research-driven and event-driven strategies; often stabilizes order books and depth through token lending/limits during TGE/launch phases.

Representative Holding Tokens:

Top five holding assets: USDC, USDT, G, ETH, ENA

Notable holding assets: G, ENA, MNT, LINEA, YB, etc.

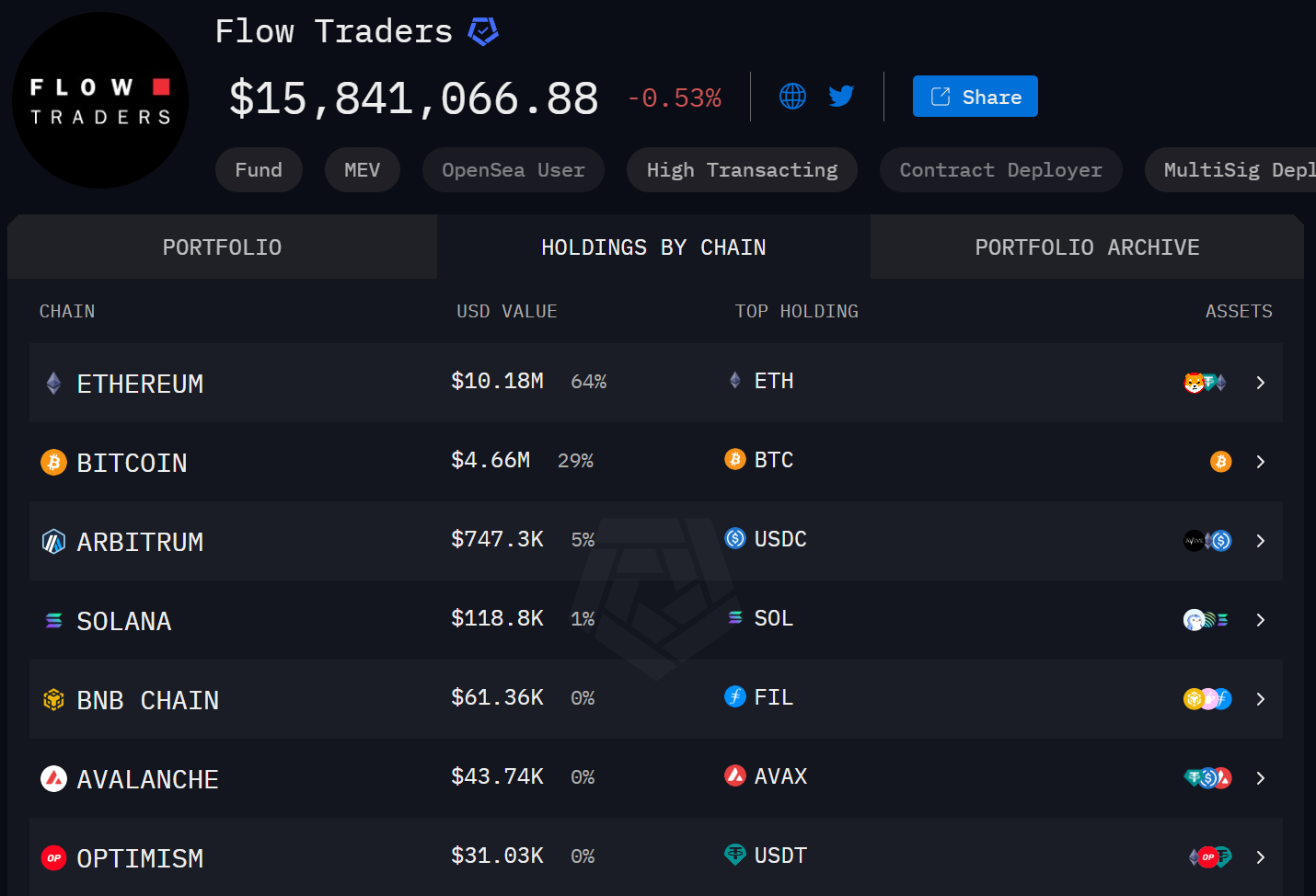

7. Flow Traders

Source: Flow Traders

Overview: A leading ETP/ETF market maker based in Europe, entered the crypto space in 2017, and is now one of the core market makers and risk hedgers for crypto ETPs. According to Arkham data, as of October 23, 2025, the holding scale is approximately $15 million.

Market Making Style: Centered around on-exchange ETPs, providing continuous quotes and redemption connections for passive/active products to secondary market investors; covers over 200 crypto ETPs, with underlying assets extending to over 300 tokens.

Representative Holding Tokens:

Top five holding assets: ETH, BTC, USDT, USDC, SOL

Notable holding assets: FIL, AVAX, SHIB, WLFI, DYDX, etc.

These seven market makers collectively manage and operate on-chain visible assets exceeding $1.5 billion, playing roles in depth provision, price discovery, and risk assumption across multiple exchanges and on-chain protocols. From high-frequency quant trading to institutional market making, from new coin cold starts to ETF hedging, and from Asia to Europe and America, these seven market makers cover nearly all mainstream and hot tokens ranked in the top five hundred by market capitalization, forming the core framework of global crypto liquidity.

Controversies and Conflicts Faced by Market Makers

Due to factors such as information asymmetry, misaligned incentives, and opaque contract terms, market making can shift from a public good to a private interest game. The conflicts faced by market makers include price manipulation versus liquidity provision, rational risk control versus market volatility, and public good attributes versus profit-driven motives.

1. Conflict Between Price Manipulation and Liquidity Provision

In the early days of the crypto market, the role of "market maker = spontaneous quoting + investment + consulting" was quite common. However, this overlapping role also means that liquidity providers may face conflicts of interest: on one hand, they are responsible for providing quotes and stabilizing liquidity for projects, while on the other hand, they may hold or be allocated large amounts of tokens for sale, creating an incentive to push prices up and then cash out at lower prices. For example, the contract between Movement Labs and its designated market maker sparked serious controversy: approximately 66 million MOVE tokens (about 5% of the public circulation) were transferred to a dedicated market-making entity, which was granted a clause allowing them to sell once the market cap reached a certain level, and they sold the tokens within a day of the token's launch, profiting about $38 million.

It is evident that market makers can be both liquidity providers and tools for price manipulation, so any lack of transparency in market-making arrangements can be seen as "gray area trading," eroding the trust foundation of the entire market.

2. Conflict Between Rational Risk Control and Market Volatility

Market makers' profits mainly come from spreads, rebates, and hedging gains, while risks can spike during extreme volatility. Rational profit maximization can drive market makers to prioritize self-preservation over "maintaining depth." In extreme market conditions, market makers may collectively withdraw liquidity, becoming accelerators of market collapse. The crash on October 10-11, 2025, is a typical scenario. When a sudden risk event triggers the market, the risk models of multiple market makers (such as single-asset exposure, VaR, hedging failures, liquidity pressure thresholds, etc.) are triggered simultaneously, forcing them to choose "active exit" or "temporary reduction of orders."

Although this behavior is a result of rational risk control by market makers, from a macro market perspective, when liquidity providers withdraw simultaneously, the market turns into a situation with only "sell orders" and no "effective buy orders," leading to a "drained" depth, where ordinary market orders can be quickly consumed, and transaction prices deteriorate instantly. The liquidation system triggers more position liquidations, creating a second-level chain reaction, further driving prices down, and market makers' risk control thresholds are triggered again, resulting in a vicious cycle that ultimately leads to a waterfall decline. In other words, the market collapse is not due to "too aggressive selling," but rather "too weak buying."

3. Conflict Between Business Expansion and Depth

As the total number of crypto tokens grows exponentially and the narrative lifecycle shortens, market makers face unprecedented structural challenges. The past high-frequency market-making model centered around mainstream tokens and a few exchanges now has to cope with a multi-chain, multi-asset, and fragmented trading ecosystem. Although leading institutions have advantages in algorithms and capital scale, their models are often designed around high-liquidity tokens like BTC and ETH, making it difficult to quickly replicate to hundreds or thousands of new tokens. For market makers, the biggest challenge is no longer "can they be profitable," but "how to expand service boundaries without sacrificing depth."

Market making essentially requires a triad of investment in capital, computing power, and data, but these resources become scarce during rapid market expansion. To cover more assets, market makers must enhance automation and strategy reuse—improving response speed when new assets are listed through unified market-making engines, cross-chain algorithm routing, and AI parameter scheduling. However, this scale expansion inevitably comes with risk spillover: delayed strategy migration leads to distorted quotes, amplified volatility in low-liquidity tokens, and increased difficulty in position management.

4. Conflict Between "Public Good" and Profit-Driven Motives

Market making is essentially private capital providing public liquidity: it reduces friction for all traders and enhances price discovery, but individual institutions bear inventory and tail risks. Project and market-making contracts often include terms for borrowing tokens, rebates, and exit thresholds, and KPIs may focus on "price/market cap" rather than "sustainable depth," inducing "push price—dump tokens" behavior.

When there is insufficient disclosure and constraints, market making can deviate from the role of liquidity providers, degrading from a public good to a timing-based supply. They can stabilize the market, but they can also become points of liquidity fracture.

Future Direction: From "Invisible Depth" to "Institutionalized Liquidity"

The true vulnerability of the crypto market lies not in the scale of funds or volatility itself, but in the uncertainty of "who provides liquidity and when they will withdraw." As the number of tokens surges and narratives accelerate, the role of market makers is being forced to evolve: from quantitative teams serving only mainstream assets to a distributed liquidity network covering thousands of tokens, cross-chain assets, and stablecoins. The future challenge is not only "how to do more," but also "how to do it more steadily, transparently, and compliantly."

1. Information Symmetry and Disclosure Transparency

For the market-making ecosystem to be truly healthy, information transparency is the baseline. The collaboration between project parties and market makers should not remain at the vague slogan of "liquidity support," but should institutionalize contract disclosure:

Disclose the core terms of market-making contracts, including limits, token lending quantities, rebate ratios, and exit conditions;

Disclose the list of main market makers and address whitelists, allowing the public to verify the true source of orders;

Regularly publish depth data, spread changes, and market-making efficiency indicators (such as order response time, cancellation rate, fill rate).

For exchanges, market maker behavior should also be included in routine monitoring: monitoring for abnormal spreads, concentrated positions, and unusual cancellation speeds; if signs of manipulation such as "fake orders," "self-trading," or "circular trading among related accounts" are found, they should have the power to suspend or downgrade. In the future, blockchain explorers and analysis platforms can further standardize these indicators, forming a publicly assessable "liquidity quality score." When market participants can visually see which market maker "provides the most stable depth and fastest response," market making will no longer be a black box, but a competitive and auditable service.

2. Circuit Breaker and Recovery Mechanism

In extreme market conditions, self-preservation by market makers is a rational choice, but the market needs "system-level buffering devices." Therefore, circuit breakers and recovery mechanisms will become an important direction for institutionalization in the crypto market.

When major market makers trigger risk control exits, exchanges or protocol layers should automatically initiate a "backup market maker access mechanism," where a pre-registered pool of market makers sequentially replaces the exiting ones, ensuring that depth does not evaporate instantly; at the same time, combined with the depth replenishment plan of the matching engine, smooth transitions at critical price points using algorithmic limit orders or virtual orders.

Additionally, a layered liquidity circuit breaker similar to traditional finance can be introduced:

Mild Stage: When spreads become excessively wide or depth falls to a warning threshold, pause matching for 3-5 seconds and restrict market orders;

Moderate Stage: When multiple market makers exit and market depth falls below 30% of historical averages, suspend transactions and broadcast risk control announcements;

Severe Stage: The platform or on-chain governance contract temporarily takes over the support orders until new market makers are restored.

The goal of this multi-layered protective design is not to "force market makers to stay," but to prevent the market from falling into a vacuum the moment they withdraw.

3. Balancing Efficiency and Risk Control

As the total number of tokens in the crypto market grows exponentially and the narrative half-life continues to shorten, traditional high-frequency market-making models clearly cannot cover all assets. For market makers, the biggest challenge is how to expand the range of quotes without distorting risk control.

One of the future solutions is RFQ 2.0 and intent-based matching. Such systems allow users to issue "intents," which are then responded to competitively by different market makers or "solvers," greatly enhancing the matching efficiency of long-tail assets. For example, intent-based matching protocols like CowSwap and UniswapX have already provided the infrastructure for "distributed market making" at the technical level.

On the other hand, the relationship between project parties and market makers must also shift from implicit incentives to transparent cooperation. Currently, many new tokens still rely on "token lending + market-making rebates" gray arrangements, which provide short-term liquidity convenience but also lay the groundwork for price manipulation. In the future, both parties should replace hidden subsidies with on-chain contract-based inventory incentives: every token lending, order placement, and recovery should be recorded on-chain, clearly stating terms and time windows to avoid the perception of "subsidy—pump—dump."

4. Multi-Dimensional Regulation and Self-Discipline: Professionalization and Accountability of Market Making

As the crypto market integrates with traditional finance, market makers will gradually fall under a clearer regulatory framework. Regulation should not only focus on "manipulation" or "insider trading," but also establish a "market-making license + behavior record" system.

After obtaining a market-making license issued by exchanges or regulators, institutions must sign liability clauses and accept regular reviews;

Market-making behavior records (including cancellation rates, abnormal spreads, and triggered circuit breaker counts) should be archived on-chain and be auditable;

Non-compliant or high-risk behaviors (such as abusing rebates or failing to disclose self-trading) will trigger "gray lists" and suspension mechanisms.

Additionally, the industry should also promote self-discipline: establish a market-making industry association or alliance to unify SLA standards and disclosure templates; introduce third-party data audits and publish quarterly "market-making performance rankings" to incentivize transparency and robust operations. Only when market making is seen as a "profession that can be evaluated and held accountable" will liquidity no longer depend on trust, but truly become a regulated infrastructure.

Conclusion

Over the past decade, the liquidity of the crypto market has mainly relied on a small group of algorithm teams; in the next decade, it will be supported by institutions, data, and trust. The boundaries of market makers are also being reshaped—they are no longer just operators of "invisible depth," but co-builders of transparency, robustness, and accountability. When on-chain data platforms make market-making behavior "visible," when circuit breaker mechanisms teach the market to self-heal, and when disclosure systems and regulatory frameworks hold liquidity providers to greater obligations, the crypto market can truly transition from "flash depth" to "institutionalized liquidity." At that time, prices will no longer be driven by isolated trades, but will be supported by a transparent liquidity network; and market makers will evolve from being questioned as "behind-the-scenes manipulators" to trusted "market infrastructure operators."

About Us

Hotcoin Research, as the core research institution of Hotcoin Exchange, is dedicated to transforming professional analysis into your practical tools. Through "Weekly Insights" and "In-Depth Reports," we analyze market trends for you; leveraging our exclusive column "Hotcoin Selection" (AI + expert dual screening), we help you identify potential assets and reduce trial-and-error costs. Every week, our researchers also engage with you face-to-face through live broadcasts, interpreting hot topics and predicting trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and seize the value opportunities of Web3.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。